He Tried the Backdoor Roth — and Got a Surprise Tax Bill

A coworker gave Marcus the same tip he’d heard a dozen times: “Too high-income for a Roth? Just do the backdoor Roth. No tax.” A solid strategy — but only when one condition holds. For Marcus, it didn’t. What he never knew was that a Traditional IRA balance he’d carried for years would quietly unravel the whole plan.

Key Takeaways

- The backdoor Roth is legal and widely used. But “tax-free” only holds when your existing pre-tax IRA balance is at or near zero.

- When you convert, the IRS adds up all your Traditional, SEP, and SIMPLE IRAs (the pro-rata rule). Opening a separate account doesn’t isolate the new money.

- If your pre-tax balance is large, most of the amount you convert gets taxed — even though you just contributed after-tax dollars.

- Not counted in the pot: workplace plans like a 401(k) or 403(b), inherited IRAs, and your spouse’s IRAs.

- You must file Form 8606 for every year you contribute or convert. Skip it, and the IRS may tax the full conversion.

Table of Contents

1. Marcus’s Plan

Marcus earns too much to contribute to a Roth IRA directly — high earners hit an income limit on direct Roth contributions. So a coworker walked him through the workaround: put $7,500 into a Traditional IRA as a non-deductible contribution, then convert it to a Roth right away. There’s no income limit on non-deductible contributions, so anyone can use this door.

True enough — if you look only at that fresh $7,500. The trouble is that the $7,500 wasn’t the only thing sitting in Marcus’s IRA picture.

2. Why “Tax-Free” Falls Apart — the Pro-Rata Rule

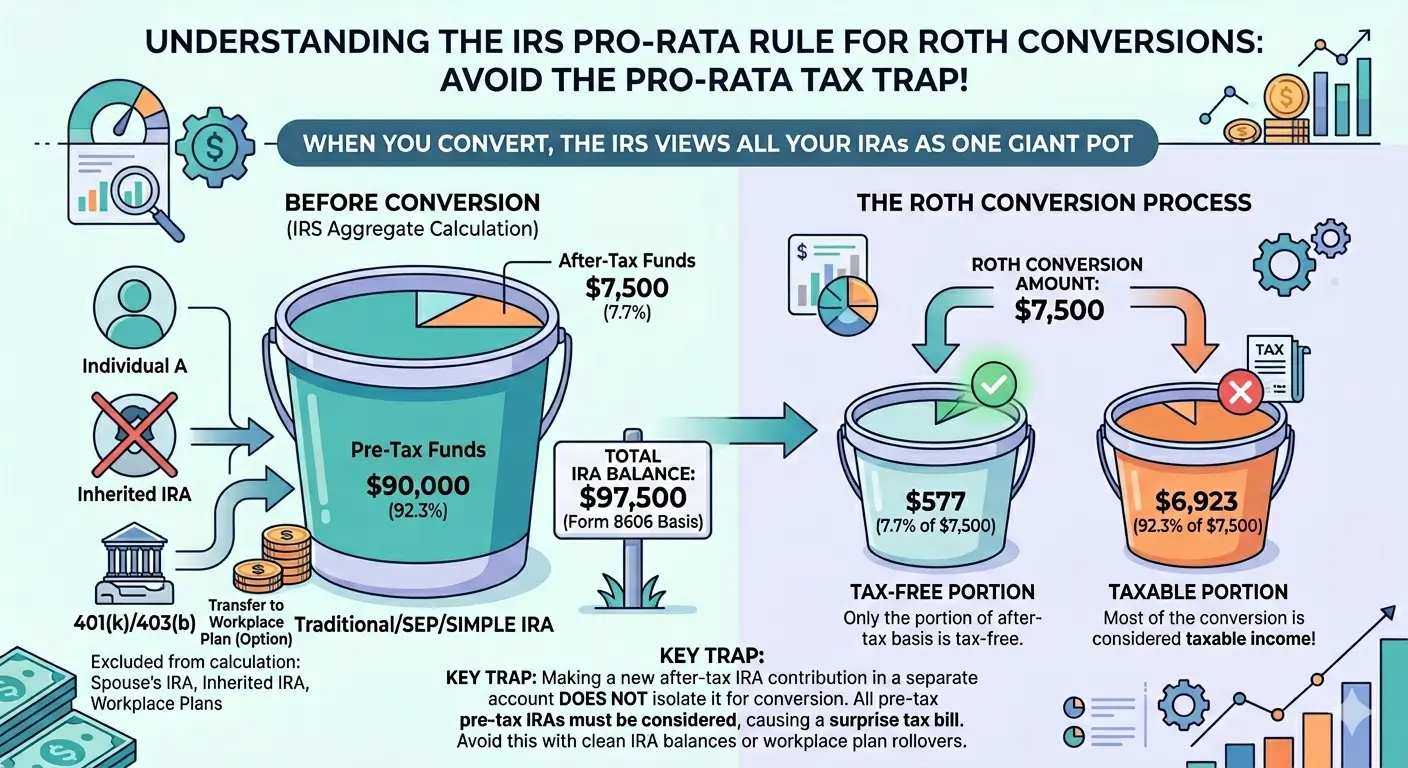

Marcus had a Traditional IRA built from an old 401(k) he’d rolled over years earlier. The balance was $90,000, all of it pre-tax — money that had never been taxed. If you’ve rolled an old workplace 401(k) into an IRA, a balance in the tens of thousands isn’t unusual at all.

Here’s where most people trip. “Can’t I just open a separate account and convert only from there?” No. When you convert, the IRS treats every Traditional, SEP, and SIMPLE IRA you own as one combined pot. The number of accounts doesn’t matter.

Bottom line

Only the share of your total IRA that is already-taxed money (your basis) comes out tax-free. The rest of any conversion is taxed — no matter which account the money leaves from.

3. Marcus’s Numbers

Say Marcus puts in his $7,500 non-deductible contribution and converts $7,500 to a Roth. His total IRA is now $97,500 — the old $90,000 pre-tax plus the new $7,500 after-tax.

| Item | Amount |

|---|---|

| Existing pre-tax IRA | $90,000 |

| New non-deductible (after-tax) contribution | $7,500 |

| Total IRA balance | $97,500 |

| After-tax share | about 7.7% |

| Tax-free part of the $7,500 conversion | about $577 |

| Taxable part of the $7,500 conversion | about $6,923 |

Marcus expected “no tax.” Instead, about 92.3% of the conversion landed on his return as taxable income. What he got was a surprise tax bill.

Important: The pro-rata calculation uses the combined December 31 balance of all your Traditional, SEP, and SIMPLE IRAs for the year of the conversion — not the balance on the day you convert.

4. When the Situation Is Different

If Your IRA Balance Is Zero

With no pre-tax Traditional IRA balance (or one near zero), the backdoor works cleanly. You convert what you put in, and only the small amount of earnings that built up in between gets taxed. That’s why it helps to convert soon after contributing.

Practical point

The clean version of the backdoor Roth starts with an empty pre-tax IRA. Check that balance before you contribute, not after.

Clearing Out an Existing Balance

One way to take a pre-tax IRA balance out of the pro-rata pot is to roll it into a workplace 401(k) or a Solo 401(k). Workplace plans aren’t part of the IRA pro-rata calculation, so moving the money there can clear the path. Not every plan accepts incoming IRA rollovers, though, so check the plan’s rules first.

Married Couples Calculate Separately

The pro-rata rule applies per person. One spouse’s IRA balance has no effect on the other spouse’s conversion math. If one of them has an empty IRA, that spouse can run a clean backdoor Roth even while the other can’t.

Important: SEP IRAs and SIMPLE IRAs count in the pot if they hold pre-tax money. Inherited IRAs, on the other hand, are calculated separately and are not aggregated with your own.

5. What to Check Right Now

- Total the balances of every Traditional, SEP, and SIMPLE IRA in your name. Is it at or near zero?

- If the pre-tax balance is large, deal with the pro-rata problem before you attempt a backdoor Roth.

- Check whether your workplace (or Solo) 401(k) accepts incoming IRA rollovers.

- Convert soon after contributing to keep earnings — and the taxable portion — small.

- File Form 8606 with your return for every year you contribute or convert.

EA Insight

Before anyone reaches for the backdoor Roth, I ask the same question first: “How much do you have sitting in your Traditional, SEP, and SIMPLE IRAs right now?”

Skip that one line and things go sideways. Plenty of people assume a separate account keeps the new money walled off. The IRS doesn’t see it that way — at the moment you convert, all of your IRAs are added together. Leave a large pre-tax balance in place, and “tax-free into a Roth” turns into “most of the conversion is taxable.”

The step people skip most often is Form 8606. You file it for every year you make a non-deductible contribution and every year you convert. Leave it out, and the IRS has no record that the money was already taxed — which means it can tax the whole conversion again.

As an Enrolled Agent — a tax practitioner federally authorized to represent taxpayers before the IRS — my job isn’t to say “do the backdoor” or “don’t.” It’s to look at the IRA balances first, check whether the pro-rata rule bites, and if it does, work out whether a 401(k) rollover can clear it. The order matters more than the strategy.

EA Summary

The backdoor Roth is powerful, but an existing pre-tax IRA balance breaks the “tax-free” part through the pro-rata rule. Before you try it, total up the IRAs in your name. If the balance is large, clear it first — a 401(k) rollover is one route. And whatever you do, don’t skip Form 8606 in the year you convert.

Frequently Asked Questions

Can I avoid the pro-rata rule by opening a separate IRA?

No. The IRS adds up all your Traditional, SEP, and SIMPLE IRAs. Splitting the money across accounts doesn’t change the combined total it uses.

Does my 401(k) count in the calculation?

No. Workplace plans like a 401(k) or 403(b) aren’t part of the IRA pro-rata calculation. That’s why rolling a pre-tax IRA into a 401(k) can be a way to clear the path.

Does my spouse’s IRA balance affect my conversion?

No. The pro-rata rule applies per individual. If your own IRA is empty, you can convert cleanly regardless of your spouse’s balances.

What happens if I don’t file Form 8606?

Without it, the IRS has no record that the money was already taxed, so it can tax the entire conversion. File it for every year you contribute or convert.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.