What Is a 1099-MISC?

Form 1099-MISC is the IRS information return used to report miscellaneous income — including rents, royalties, prizes, medical payments, and attorney proceeds. Before 2020, freelancer pay was also reported on this form, but that role now belongs to Form 1099-NEC. Confusing the two can lead to incorrect filings and IRS notices.

Key Takeaways

- Form 1099-MISC reports miscellaneous income such as rents, royalties, prizes, medical and health care payments, and gross proceeds paid to an attorney.

- Nonemployee compensation (freelancer and contractor pay) is reported on Form 1099-NEC — not on 1099-MISC.

- Most payment categories require reporting at $600 or more. Royalties have a separate threshold of $10 or more.

- Under the OBBBA, the general reporting threshold increases from $600 to $2,000 for payments made in the applicable tax year and beyond.

- Even if you do not receive a 1099-MISC, the income is still taxable and must be included on your federal tax return.

- Using the wrong form — 1099-MISC instead of 1099-NEC or vice versa — can trigger deadline violations, IRS mismatch notices, and penalties.

Table of Contents

- 1. What Is Form 1099-MISC?

- 2. Who Issues a 1099-MISC?

- 3. Key Boxes on Form 1099-MISC

- 4. Reporting Threshold Change Under the OBBBA

- 5. 1099-MISC vs. 1099-NEC — The Key Difference

- 6. What to Do When You Receive a 1099-MISC

- 7. No Form Received? You Must Still Report the Income

- 8. EA Insight

- 9. Frequently Asked Questions

- 10. Related Articles

- 11. Official Resources

1. What Is Form 1099-MISC?

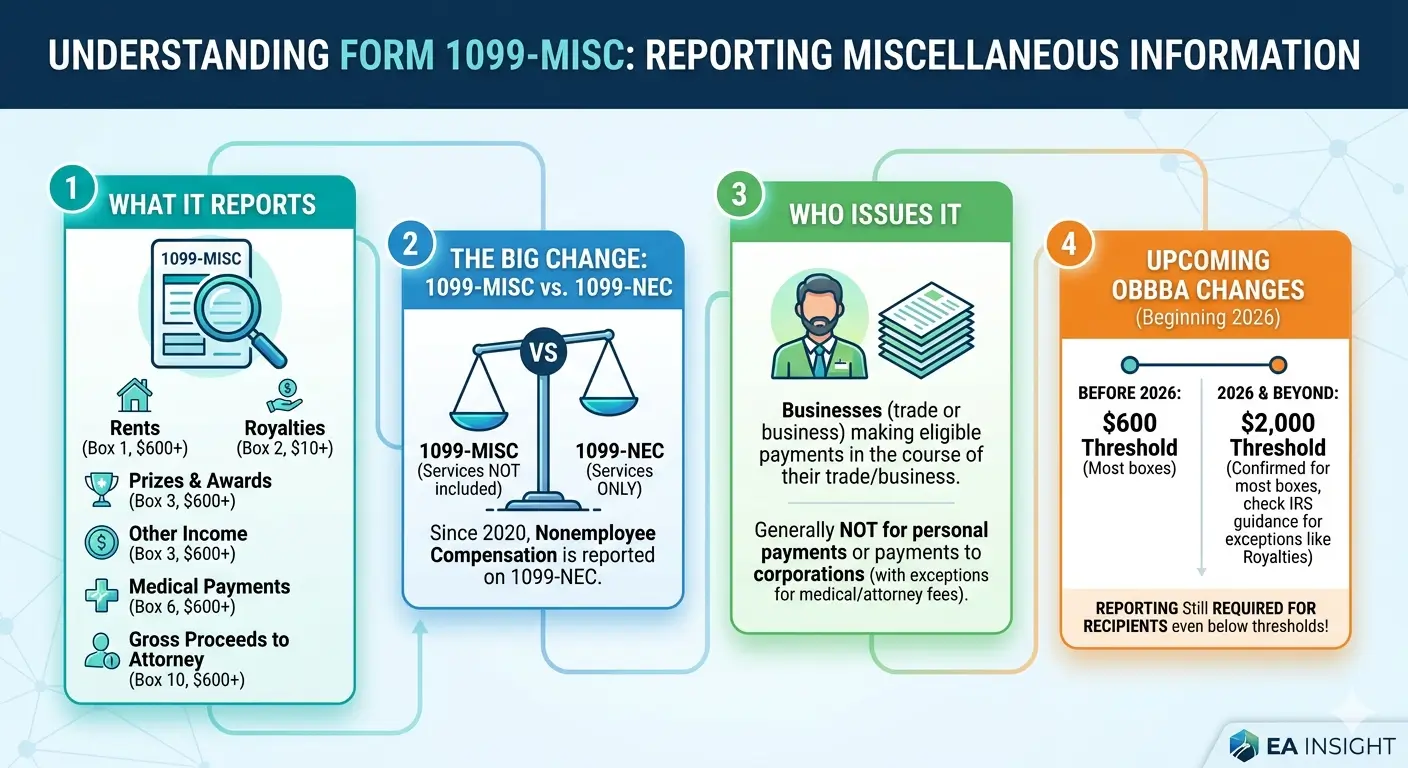

Form 1099-MISC, Miscellaneous Information, is an IRS information return used to report various types of income paid in the course of a trade or business. “MISC” stands for miscellaneous — this form covers payments that do not fit neatly into other 1099 categories.

Common types of income reported on Form 1099-MISC include rents, royalties, prizes and awards, medical and health care payments, gross proceeds paid to an attorney, and crop insurance proceeds.

Before 2020, nonemployee compensation — payments to freelancers and independent contractors — was also reported on this form in Box 7. When the IRS reintroduced Form 1099-NEC, that category was permanently moved off of 1099-MISC. Today, Form 1099-MISC is strictly for miscellaneous income other than service-based compensation.

2. Who Issues a 1099-MISC?

Any business or organization that makes qualifying payments in the course of a trade or business must issue Form 1099-MISC when the payment meets the applicable threshold. The general threshold is $600 or more for most categories and $10 or more for royalties.

Personal payments are not reportable. For example, if you pay someone to repair your personal residence, that payment does not require a 1099-MISC. Only payments made in connection with a trade or business trigger the filing obligation.

Exception for corporations: Payments to corporations generally do not require a 1099-MISC. However, two important exceptions apply — medical and health care payments (Box 6) and gross proceeds paid to an attorney (Box 10) must be reported regardless of the recipient’s corporate status.

3. Key Boxes on Form 1099-MISC

| Box | What It Reports | Threshold |

|---|---|---|

| 1 | Rents (office space, equipment, farmland) | $600+ |

| 2 | Royalties (patents, copyrights, oil/gas/minerals) | $10+ |

| 3 | Other income (prizes, awards, deceased employee wages) | $600+ |

| 4 | Federal income tax withheld (backup withholding) | Any amount |

| 5 | Fishing boat proceeds | $600+ |

| 6 | Medical and health care payments | $600+ |

| 7 | Direct sales of consumer products ($5,000+) | Checkbox only |

| 8 | Substitute payments in lieu of dividends or interest | $10+ |

| 9 | Crop insurance proceeds | $600+ |

| 10 | Gross proceeds paid to an attorney | $600+ |

| 11 | Fish purchased for resale | $600+ |

| 12 | Section 409A deferrals | If applicable |

Box 4 (federal income tax withheld) has no minimum threshold — if backup withholding was applied, it must be reported regardless of the amount.

4. Reporting Threshold Change Under the OBBBA

The One Big Beautiful Bill Act (OBBBA) raised the general reporting threshold for Form 1099-MISC and Form 1099-NEC from $600 to $2,000, effective for payments made in the applicable tax year and beyond. Starting the following year, this threshold will be adjusted annually for inflation.

| Period | General Reporting Threshold |

|---|---|

| Before OBBBA | $600 (royalties: $10) |

| OBBBA effective year | $2,000 |

| Subsequent years | $2,000 + inflation adjustment |

Note: The $2,000 threshold applies to payment categories that previously required reporting at $600. Royalties (Box 2), which have a separate $10 reporting threshold, are not specifically addressed in the OBBBA threshold increase. Check the latest IRS instructions to confirm whether the royalty threshold has been adjusted.

A higher reporting threshold does not eliminate the taxpayer’s obligation to report the income. Even if the payer is no longer required to issue a form because the payment falls below $2,000, the recipient must still include that income on their federal tax return. What changed is the payer’s filing obligation — not the recipient’s reporting obligation.

5. 1099-MISC vs. 1099-NEC — The Key Difference

These two forms are frequently confused. The distinction comes down to what the payment is for.

| Feature | 1099-MISC | 1099-NEC |

|---|---|---|

| What It Reports | Rents, royalties, prizes, medical payments, attorney gross proceeds, and other miscellaneous income | Nonemployee compensation (freelancer and contractor pay for services) |

| Recipient Deadline | Early February (mid-February for Boxes 8 and 10) | January 31 |

| IRS Filing Deadline | Late February (paper) / March 31 (e-file) | January 31 |

| Self-Employment Tax | Generally does not apply | Applies (reported on Schedule SE) |

The most common mistake: reporting freelancer or contractor pay on Form 1099-MISC instead of 1099-NEC. This error can result in missed deadlines, IRS mismatch notices (CP2100), and penalties.

Attorney payments require special attention. Fees paid for legal services go on Form 1099-NEC Box 1. Gross proceeds from legal settlements go on Form 1099-MISC Box 10. If both types of payments are made to the same attorney, both forms must be filed.

6. What to Do When You Receive a 1099-MISC

If you receive a 1099-MISC, you must report the income on your federal tax return. Where the income goes depends on the type of payment:

| 1099-MISC Box | Where to Report on Your Tax Return |

|---|---|

| Box 1 — Rents | Schedule E or Schedule C (Form 1040) |

| Box 2 — Royalties | Schedule E (Form 1040) |

| Box 3 — Other income | Schedule 1 (Form 1040), Line 8z |

| Box 6 — Medical payments | Applicable business return |

If the amounts on your 1099-MISC do not match your records, contact the issuer (the “Filer” shown in the top-left corner of the form) to request a corrected form. The IRS cannot correct your 1099-MISC. Do not delay filing your return while waiting for a correction — file on time using your own accurate records, and amend later if necessary.

7. No Form Received? You Must Still Report the Income

If a payment falls below the reporting threshold, or if the payer simply fails to issue the form, you may not receive a 1099-MISC. That does not change your tax obligation.

For example, if you receive $500 in rental income from a single business in a given year, the payer may not be required to issue a 1099-MISC because the amount is below the threshold. However, that $500 is still taxable income and must be included on your tax return.

This distinction becomes especially important under the higher OBBBA threshold. As fewer forms are issued, more taxpayers may mistakenly assume that unreported income is nontaxable. It is not. “I didn’t receive a form” is not a defense the IRS accepts.

EA Insight

The most common problem I see with Form 1099-MISC is form confusion. Some payers still report freelancer pay on 1099-MISC instead of 1099-NEC, and recipients file their returns using the incorrect form without questioning it. When that happens, the IRS system flags an income-type mismatch — and a notice follows.

The second most frequent issue is the assumption that no form means no income. With the reporting threshold increasing to $2,000, this misconception will likely grow. The threshold change reduces the payer’s paperwork burden — it does not reduce the recipient’s tax obligation. Every dollar of taxable income must be reported, whether or not a form is issued.

Attorney payments also deserve close attention. Legal service fees belong on 1099-NEC. Settlement proceeds belong on 1099-MISC Box 10. If both types of payments go to the same attorney in the same year, you must file both forms. Missing this distinction can result in penalties on both sides of the transaction.

Frequently Asked Questions

Should I receive a 1099-MISC or a 1099-NEC?

If you were paid for services as a freelancer or independent contractor, you should receive a 1099-NEC. If you received rent, royalties, prizes, or other miscellaneous income, you should receive a 1099-MISC.

I didn’t receive a 1099-MISC. Do I still need to report the income?

Yes. Whether or not you receive a form, all taxable income must be reported on your federal tax return.

Does the higher reporting threshold mean income below $2,000 is tax-free?

No. The threshold increase applies only to the payer’s obligation to issue the form. The recipient’s obligation to report the income on their tax return remains unchanged, regardless of the amount.

What if the amounts on my 1099-MISC don’t match my records?

Contact the issuer directly to request a corrected form. The IRS cannot correct your 1099-MISC. File your return on time using your own accurate records, and amend later if a corrected form changes the reported amounts.

I’m a corporation and received a 1099-MISC. Is that correct?

It may be. Medical and health care payments (Box 6) and gross proceeds paid to an attorney (Box 10) must be reported on 1099-MISC even when the recipient is a corporation. If your payment falls into one of these categories, the form is correct.

Can I receive both a 1099-MISC and a 1099-NEC from the same payer?

Yes. If you received both service-based compensation and other miscellaneous income (such as rent) from the same business in the same year, you may receive both forms. Report each one according to its category on your tax return.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.