What Is a 1099-NEC?

Who Gets It, How to Read It & What to Do With It

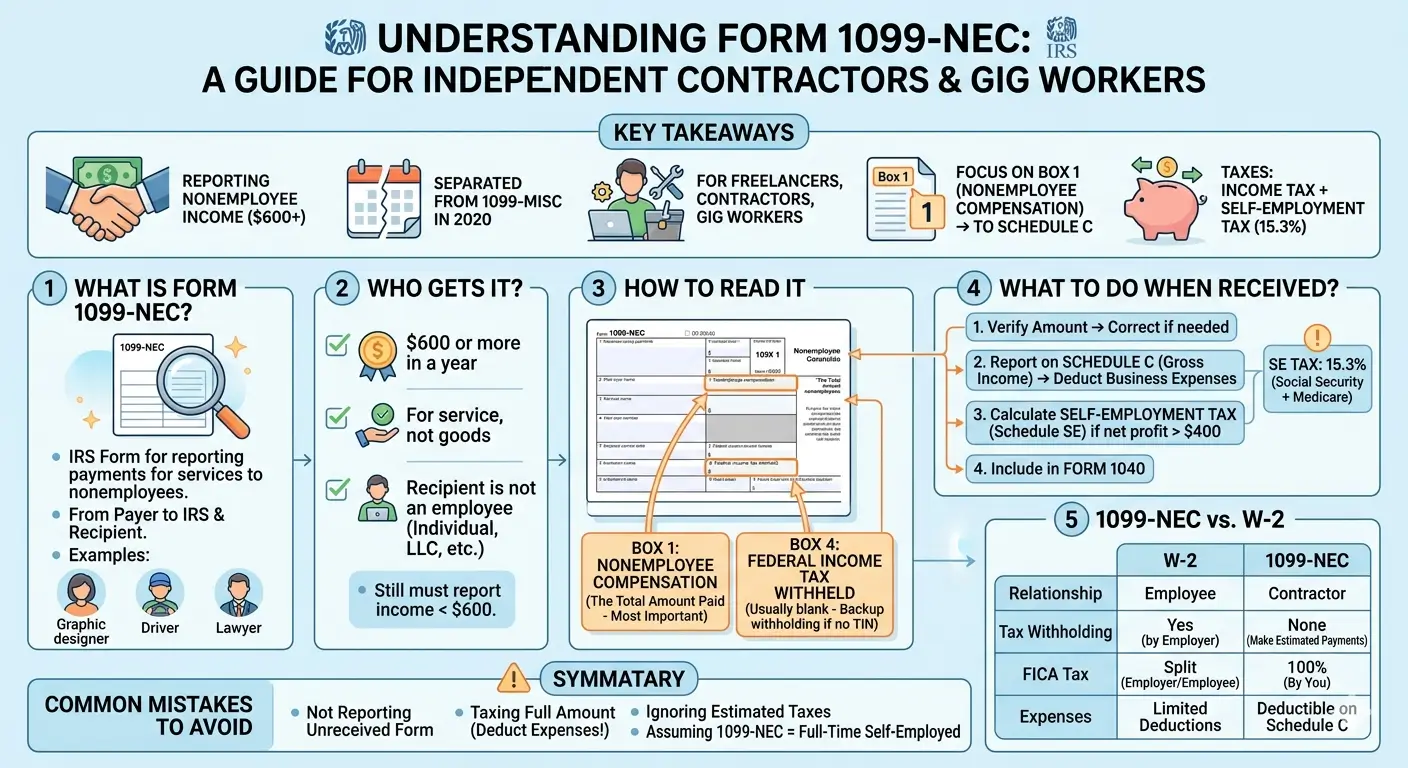

Key Takeaways

- A 1099-NEC reports nonemployee compensation — payments of $2,000 or more made to someone who is not an employee.

- The form was separated from the 1099-MISC in 2020 to reduce filing confusion.

- Freelancers, independent contractors, and gig workers are the most common recipients.

- Box 1 (Nonemployee Compensation) is the key figure — it flows directly to Schedule C.

- 1099-NEC income is subject to both income tax and self-employment tax (15.3%).

- You must report the income even if you never receive the form.

- The reporting threshold increased from $600 to $2,000 for payments made in 2026 and later, under the One Big Beautiful Bill Act (OBBBA).

Table of Contents

What Is a 1099-NEC?

A 1099-NEC (Nonemployee Compensation) is an IRS information return used to report payments made to someone who is not an employee. If a business pays an independent contractor, freelancer, or other nonemployee for services, it must file this form with the IRS and send a copy to the recipient.

The word “nonemployee” is the key here. If you are on a company’s payroll, you receive a W-2. If you are not on the payroll but performed services for the company, you receive a 1099-NEC instead.

Think of it this way: a W-2 is a report of wages paid to an employee. A 1099-NEC is a report of compensation paid to everyone else.

Note that the payer (the business or client) is responsible for preparing and filing the form — not the recipient. If you are a freelancer, you do not create your own 1099-NEC. Your client does.

Why Does the 1099-NEC Exist?

Before 2020, nonemployee compensation was reported in Box 7 of Form 1099-MISC. This created a practical problem: the 1099-MISC had two different filing deadlines depending on which boxes were filled in. Nonemployee compensation was due by January 31, while other 1099-MISC categories were due later. One form with two deadlines caused widespread confusion.

To solve this, the IRS reintroduced the 1099-NEC as a standalone form beginning with the 2020 tax year. (The 1099-NEC actually existed before — it was used until 1982, then discontinued.)

Now the split is clean: all nonemployee compensation goes on the 1099-NEC, while rent, royalties, prizes, medical payments, and other miscellaneous income remain on the 1099-MISC.

Who Gets a 1099-NEC?

A payer must issue a 1099-NEC when all three conditions are met:

- The recipient is not an employee of the payer.

- The payment was made for services (not goods).

- The total payments to that recipient reached $2,000 or more during the calendar year.

Common recipients include: freelance designers, writers, and consultants; rideshare and delivery drivers (Uber, Lyft, DoorDash); independent contractors in construction, IT, or marketing; and attorneys paid for legal services.

Important: Payments to most corporations (S-Corps and C-Corps) are generally exempt from 1099-NEC reporting. The main exception is payments to attorneys for legal services — those must be reported regardless of the recipient’s business structure.

What About the $2,000 Threshold?

Under the One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, the 1099-NEC reporting threshold increased from $600 to $2,000 for payments made in 2026 and later. Starting in 2027, this threshold will be adjusted annually for inflation.

However, the reporting threshold only affects the payer’s filing obligation. If you receive $1,500 in nonemployee compensation, the payer does not need to send you a 1099-NEC — but you are still required to report every dollar of that income on your tax return. All income is taxable regardless of whether a form is issued.

1099-NEC vs. 1099-K: Which One Will You Get?

This is a common point of confusion. If your clients pay you directly (by check, cash, ACH, or wire), the client issues a 1099-NEC. If you receive payments through a third-party platform (PayPal, Venmo, Stripe, or a credit card processor), the platform may issue a 1099-K instead. The income is the same either way — the difference is who reports it.

How to Read a 1099-NEC

Compared to a W-2, the 1099-NEC is simple. There are really only two boxes that matter for most recipients:

| Box | Name | What It Means |

|---|---|---|

| Box 1 | Nonemployee Compensation | Total amount paid to you during the year — the most important number on the form |

| Box 4 | Federal Income Tax Withheld | Amount withheld for backup withholding (usually $0 for most contractors) |

| Boxes 5–7 | State Tax Information | State ID, state income, and state tax withheld — only filled in if applicable |

Box 1 is the number you need. This amount becomes your gross income on Schedule C (Profit or Loss From Business).

Box 4 is blank for most people. It contains a figure only when backup withholding (24%) has been applied — which typically happens when the recipient did not provide a valid taxpayer identification number on Form W-9. If there is an amount in Box 4, make sure to claim it as taxes already paid when you file your return.

What to Do When You Receive a 1099-NEC

Before you receive the form: When you start working with a new client, you will typically be asked to complete Form W-9 (Request for Taxpayer Identification Number and Certification). This is how the payer collects your name, address, and TIN (Social Security number or EIN) so they can prepare the 1099-NEC at year-end. Always provide accurate information on the W-9 to avoid backup withholding issues.

Step 1 — Verify the amount. Compare Box 1 to your own records. If the amount does not match, contact the payer and request a corrected form.

Step 2 — Report on Schedule C. Enter the Box 1 amount as gross receipts on Schedule C (Profit or Loss From Business). Subtract any deductible business expenses — equipment, software, mileage, home office costs, supplies — to arrive at your net profit.

Step 3 — Calculate self-employment tax. If your net profit on Schedule C is $400 or more, you must file Schedule SE (Self-Employment Tax). The self-employment tax rate is 15.3%, which covers Social Security (12.4%) and Medicare (2.9%). This is calculated on 92.35% of your net earnings.

Step 4 — File with Form 1040. Your Schedule C net profit flows to Form 1040 through Schedule 1. Your self-employment tax is calculated on Schedule SE and added to your total tax. You can deduct half of the self-employment tax (the “employer” equivalent portion) as an adjustment to your AGI.

1099-NEC vs. W-2: Key Differences

| Item | W-2 (Employee) | 1099-NEC (Independent Contractor) |

|---|---|---|

| Relationship | Employee | Independent contractor / freelancer |

| Tax Withholding | Employer withholds from each paycheck | No withholding — you pay estimated taxes quarterly |

| FICA Taxes | Split 50/50 with employer (each pays 7.65%) | You pay the full 15.3% |

| Business Expense Deductions | Very limited (suspended for most employees since 2018) | Deductible on Schedule C |

| Where Income Is Reported | Form 1040, Line 1 (Wages) | Schedule C → Form 1040, Schedule 1 |

| Social Security Wage Base (2026) | $184,500 | $184,500 (combined with any W-2 wages) |

Common Mistakes to Avoid

Mistake 1: “I didn’t get a 1099-NEC, so I don’t need to report the income.”

Wrong. The form is an information return for the IRS — it does not create or eliminate your tax obligation. Whether or not you receive the form, all income must be reported. The IRS cross-references payer filings with individual returns through its Automated Underreporter (AUR) program.

Mistake 2: “I owe tax on the entire Box 1 amount.”

Not necessarily. You can deduct legitimate business expenses on Schedule C before calculating your tax. Equipment, software, professional development, mileage, and home office costs can all reduce your taxable profit.

Mistake 3: “I’ll just pay everything at tax time.”

If you expect to owe $1,000 or more in federal taxes for the year, the IRS requires quarterly estimated tax payments. Skipping these can result in an underpayment penalty, even if you pay in full when you file.

Mistake 4: “A 1099-NEC means I’m self-employed full-time.”

Not at all. Many people receive both a W-2 from their day job and a 1099-NEC from a side gig. Having a 1099-NEC simply means you performed services outside of an employer-employee relationship.

💡 EA Insight

The most common problem I see with 1099-NEC income is not the form itself — it’s the estimated tax payments. With a W-2 job, your employer withholds taxes from every paycheck, so there are no surprises. With 1099-NEC income, nobody takes anything out. Every year, I work with clients who are caught off guard by a large tax bill in April because they didn’t set aside money during the year.

Another pattern I see frequently: people who have both a W-2 job and 1099-NEC side income. They understand the income tax portion, but they don’t realize that the side income also triggers self-employment tax at 15.3%. That’s on top of their regular income tax rate. When the bill comes, they often ask, “Why is it so much higher than I expected?”

If you receive a 1099-NEC, keep it simple: report the income on Schedule C, deduct every legitimate business expense, and make quarterly estimated payments. Those three steps will keep you ahead of most problems.

Frequently Asked Questions

What is the difference between a 1099-NEC and a 1099-MISC?

The 1099-NEC is specifically for nonemployee compensation — payment for services. The 1099-MISC covers other types of income such as rent, royalties, prizes, and medical payments. Before 2020, both types were reported on the 1099-MISC. They are now separate forms.

Do I have to pay self-employment tax on all 1099-NEC income?

Self-employment tax applies when your Schedule C net profit is $400 or more. Below that threshold, you do not owe SE tax — but you must still report the income and may owe income tax on it.

I received multiple 1099-NECs from different clients. How do I report them?

Add up the Box 1 amounts from all your 1099-NECs and report the total as gross receipts on a single Schedule C. You do not need to file a separate Schedule C for each form.

The amount on my 1099-NEC is wrong. What should I do?

Contact the payer first and request a corrected 1099-NEC. If you cannot get a corrected form, report the actual amount you received on your tax return and keep records to support the correct figure.

When are estimated tax payments due?

Quarterly: April 15, June 15, September 15, and January 15 of the following year. Use Form 1040-ES to calculate and submit your payments. If a due date falls on a weekend or holiday, the deadline moves to the next business day.

What is the 1099-NEC reporting threshold for 2026?

For payments made in 2026, the payer must file a 1099-NEC only if total payments to a recipient are $2,000 or more. This threshold was raised from $600 under the One Big Beautiful Bill Act (OBBBA). Starting in 2027, the $2,000 amount will be adjusted for inflation. Note that the recipient must report all income regardless of whether a 1099-NEC is issued.