Tax Credits vs. Deductions

— What’s the Real Difference?

Both reduce your tax bill — but they work in completely different ways. Understanding the distinction can save you hundreds or even thousands of dollars.

Key Takeaways

- A tax deduction reduces your taxable income — the amount of income subject to tax.

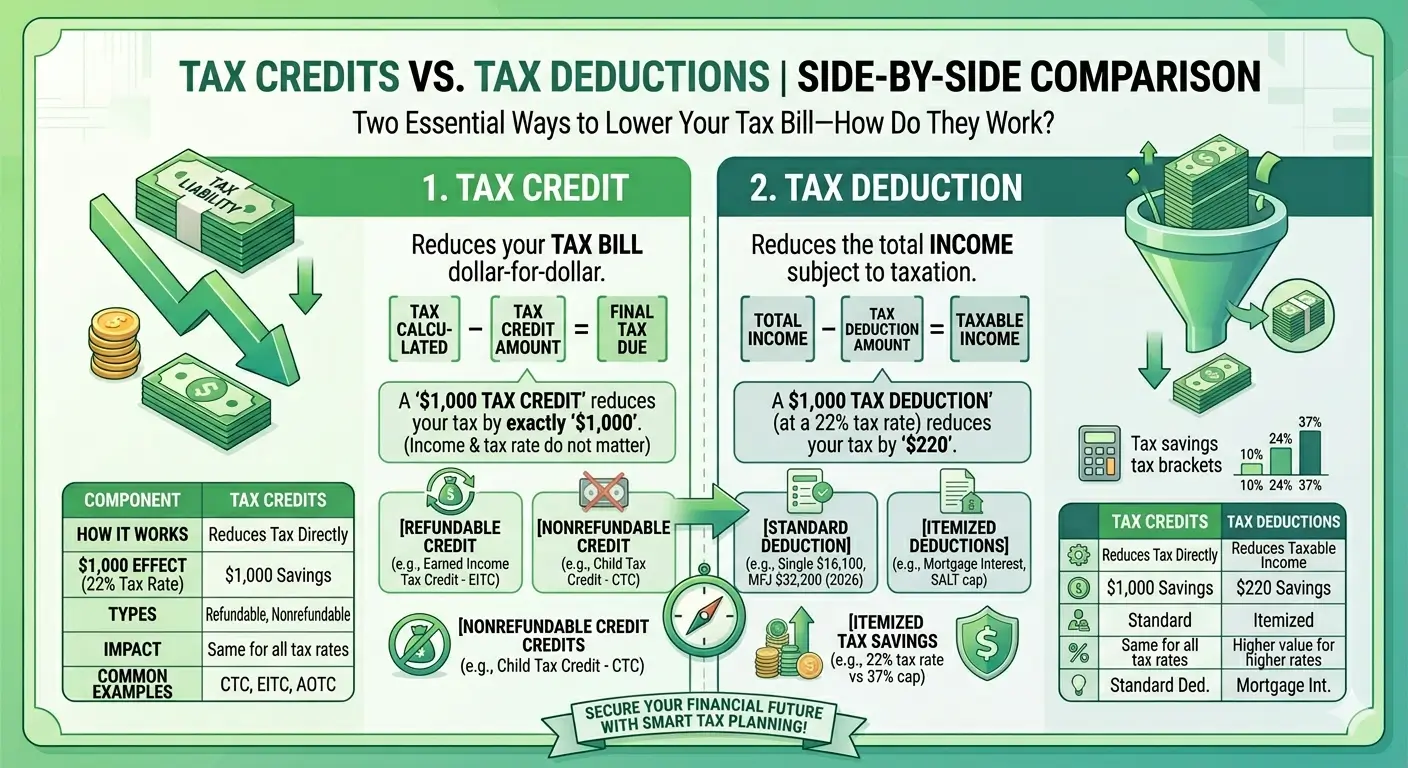

- A tax credit reduces your actual tax bill — dollar for dollar.

- A $1,000 deduction in the 22% bracket saves you $220. A $1,000 credit saves you the full $1,000.

- Credits can be refundable (you get money back even if you owe $0) or nonrefundable (limited to the tax you owe).

- Deductions can be taken as the standard deduction or as itemized deductions — but not both.

- Many taxpayers are eligible for both credits and deductions at the same time.

- The IRS adjusts many credit and deduction amounts annually for inflation.

Table of Contents

What Is a Tax Deduction?

A tax deduction is an amount you subtract from your gross income before the IRS calculates how much tax you owe. In other words, deductions reduce your taxable income — not your tax bill directly.

There are two ways to claim deductions on your federal tax return:

Standard Deduction: A fixed amount set by the IRS each year. Most taxpayers choose this option because it is simple and requires no documentation. For the current tax year, the standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly (IRS Revenue Procedure 2025-32). If you are 65 or older, you can claim an additional standard deduction of $2,050 (single) or $1,650 per person (married filing jointly).

Itemized Deductions: If your total qualifying expenses exceed the standard deduction, you may choose to itemize instead. Common itemized deductions include state and local taxes (SALT), mortgage interest, and charitable contributions. You cannot claim both the standard deduction and itemized deductions — you must choose one or the other.

The key point to remember is that a deduction’s actual tax savings depends on your marginal tax rate. A $1,000 deduction does not reduce your tax by $1,000. If you are in the 22% bracket, a $1,000 deduction saves you $220. If you are in the 12% bracket, it saves you only $120.

What Is a Tax Credit?

A tax credit is a dollar-for-dollar reduction in the amount of tax you owe. Unlike a deduction, which lowers your taxable income before tax is calculated, a credit is applied after your tax has been calculated — directly reducing your final tax bill.

This is why credits are generally more valuable than deductions of the same dollar amount. A $1,000 tax credit saves you exactly $1,000, regardless of your tax bracket. Compare that to a $1,000 deduction, which might save you only $120 to $370 depending on your marginal rate.

Some of the most widely used federal tax credits include the Child Tax Credit, the American Opportunity Tax Credit (AOTC), the Earned Income Tax Credit (EITC), and the Saver’s Credit. Each has its own eligibility requirements, income limits, and rules — which we will cover later in this guide.

Refundable vs. Nonrefundable Credits

Not all tax credits work the same way. The most important distinction is whether a credit is refundable or nonrefundable.

Refundable Credits can reduce your tax below zero. If the credit exceeds the tax you owe, the IRS sends you the difference as a refund. The Earned Income Tax Credit (EITC) is the most well-known refundable credit — for qualifying taxpayers with three or more children, it can be worth up to $8,231.

Nonrefundable Credits can reduce your tax to zero, but no further. Any unused portion of the credit is lost (unless the credit has a carryforward provision). The Lifetime Learning Credit (up to $2,000) and the Saver’s Credit (up to $1,000 for single filers) are common nonrefundable credits.

Partially Refundable Credits fall somewhere in between. The American Opportunity Tax Credit (AOTC) is a good example: the maximum credit is $2,500 per eligible student, but only 40% of it (up to $1,000) is refundable. The Child Tax Credit is also partially refundable — the maximum credit is $2,200 per qualifying child, and up to $1,700 of that amount can be refunded through the Additional Child Tax Credit (ACTC).

| Type | Can Reduce Tax Below $0? | Example | Maximum Amount |

|---|---|---|---|

| Refundable | Yes — excess is refunded | EITC | Up to $8,231 |

| Nonrefundable | No — stops at $0 | Lifetime Learning Credit | Up to $2,000 |

| Partially Refundable | Partially — limited refund | AOTC | $2,500 (40% refundable) |

Side-by-Side Comparison

The table below summarizes the core differences between tax deductions and tax credits.

| Feature | Tax Deduction | Tax Credit |

|---|---|---|

| How It Works | Reduces taxable income | Reduces tax owed directly |

| $1,000 Value (22% Bracket) | Saves $220 | Saves $1,000 |

| Affected by Tax Bracket? | Yes — higher bracket = bigger savings | No — same savings regardless of bracket |

| Types | Standard or Itemized | Refundable, Nonrefundable, or Partially Refundable |

| When Applied | Before tax is calculated | After tax is calculated |

| Common Examples | Standard Deduction, Mortgage Interest, SALT | CTC, AOTC, EITC, Saver’s Credit |

How They Work Together — A Real Example

Deductions and credits are not either/or — most taxpayers use both on the same return. Here is how they work together step by step.

Scenario: Sarah is a single filer with a gross income of $55,000 and one qualifying child.

| Step | What Happens | Amount |

|---|---|---|

| Gross Income | Sarah’s total earnings | $55,000 |

| Step 1 — Deduction | Subtract Standard Deduction ($16,100) | −$16,100 |

| Taxable Income | Income subject to tax | $38,900 |

| Tax Calculated | 10% on first $12,400 + 12% on next $38,000 + 22% on remainder | $4,440 |

| Step 2 — Credit | Apply Child Tax Credit ($2,200) | −$2,200 |

| Final Tax Owed | Tax after both deduction and credit | $2,240 |

Notice how the deduction and the credit work at different stages. The standard deduction reduced Sarah’s taxable income from $55,000 to $38,900 before tax was calculated. The Child Tax Credit then reduced her actual tax bill from $4,440 to $2,240 after tax was calculated. Together, they saved her a significant amount — the deduction lowered the income subject to tax, and the credit directly cut the final bill.

Common Tax Deductions

Standard Deduction

The standard deduction is the most widely used deduction in the U.S. tax system. Most taxpayers choose this option because it is simple and does not require receipts or documentation. The IRS adjusts the amount each year for inflation.

| Filing Status | Standard Deduction | Additional (Age 65+) |

|---|---|---|

| Single | $16,100 | +$2,050 |

| Married Filing Jointly | $32,200 | +$1,650 per person |

| Head of Household | $23,500 | +$2,050 |

Source: IRS Revenue Procedure 2025-32. These amounts apply to the current tax year. The IRS updates them annually.

📌 Recent Legislative Updates

The One Big Beautiful Bill Act (OBBBA), signed into law in July 2025, made several changes that affect deductions:

SALT Cap Increase: The deduction for state and local taxes (SALT) was raised from $10,000 to $40,000 for most filers. This is a significant change for taxpayers in high-tax states. Verify the current cap and any income-based limitations at IRS.gov.

Senior Deduction: Taxpayers age 65 and older may claim an additional deduction of up to $4,000. This deduction phases out for those with modified adjusted gross income above $75,000 (single) or $150,000 (married filing jointly). This provision applies to tax years 2025 through 2028.

Itemized Deductions

If your total qualifying expenses exceed the standard deduction, itemizing may give you a larger tax benefit. Common itemized deductions include mortgage interest on a primary residence, state and local taxes (SALT), charitable contributions to qualified organizations, and unreimbursed medical expenses that exceed 7.5% of your AGI.

Above-the-Line Deductions (Adjustments to Income)

Some deductions are subtracted from your gross income before you decide whether to take the standard deduction or itemize. These are called “above-the-line” deductions, or adjustments to income. They directly reduce your Adjusted Gross Income (AGI) — which is especially important because many credits and deductions have AGI-based income limits. Lowering your AGI can help you qualify for benefits you might otherwise miss. Common above-the-line deductions include contributions to a Traditional IRA, Health Savings Account (HSA) contributions, and student loan interest (up to $2,500 per year). See IRS Publication 17 for a complete list.

Common Tax Credits

Below are some of the most commonly claimed federal tax credits. Each credit has its own eligibility rules and income limits.

| Credit | Maximum Amount | Refundable? | Key Requirement |

|---|---|---|---|

| Child Tax Credit (CTC) | $2,200 per child | Partially (up to $1,700 via ACTC) | Qualifying child under 17 with SSN |

| Earned Income Tax Credit (EITC) | $664 – $8,231 | Yes — fully refundable | Earned income below AGI threshold |

| American Opportunity Tax Credit (AOTC) | $2,500 per student | Partially (40%, up to $1,000) | First 4 years of college; MAGI under $90,000 (single) |

| Lifetime Learning Credit (LLC) | $2,000 per return | No — nonrefundable | Any postsecondary education; MAGI under $90,000 (single) |

| Saver’s Credit | $1,000 (single) / $2,000 (MFJ) | No — nonrefundable | Retirement plan contribution; AGI under $40,250 (single) / $80,500 (MFJ) |

Source: IRS Revenue Procedure 2025-32 and IRS Notice 2025-67. Credit amounts and income thresholds are adjusted annually. Always verify eligibility at IRS.gov.

Common Mistakes to Avoid

1. Thinking a deduction equals a dollar-for-dollar savings. A $5,000 deduction does not save you $5,000 in taxes. The actual savings depend on your marginal tax bracket. Many taxpayers overestimate the value of their deductions because of this misunderstanding.

2. Trying to claim both the standard deduction and itemized deductions. You must choose one or the other. If your itemized expenses total less than the standard deduction, the standard deduction gives you a better result.

3. Assuming nonrefundable credits will generate a refund. If you owe $500 in tax and have a $2,000 nonrefundable credit, you get $500 in tax relief — not a $1,500 refund. The remaining $1,500 is lost.

4. Overlooking income limits for credits. Most tax credits have income phaseouts. Even if you meet every other requirement, exceeding the AGI threshold can reduce or eliminate the credit entirely. Check the IRS income limits each year before filing.

💡 EA Insight — Deborah Park, EA

One of the most common misconceptions I see in my practice is taxpayers believing that a $1,000 deduction reduces their tax by $1,000. It does not. A deduction reduces your taxable income, so the actual tax savings depend on your bracket — typically somewhere between $120 and $370 for every $1,000 deducted.

A $1,000 credit, on the other hand, saves you exactly $1,000 — regardless of your bracket. That is a fundamentally different impact on your tax return.

In my experience, understanding this single distinction helps taxpayers make better decisions about retirement contributions, education expenses, and charitable giving. If you are choosing between two strategies and one offers a credit while the other offers a deduction of the same amount, the credit is almost always more valuable.

Frequently Asked Questions

Is it better to have a tax credit or a tax deduction?

In most cases, a tax credit is more valuable because it reduces your tax dollar for dollar. A deduction only reduces the income that is subject to tax, so its value depends on your marginal tax rate. For example, a $1,000 credit saves $1,000, while a $1,000 deduction in the 22% bracket saves only $220.

Can I claim both credits and deductions on the same return?

Yes. Deductions and credits apply at different stages of the tax calculation. You first subtract deductions from your income to find your taxable income, then calculate your tax, and then apply credits to reduce the tax you owe. Many taxpayers benefit from both.

What is the difference between a refundable and nonrefundable credit?

A refundable credit can reduce your tax below zero, meaning the IRS will send you the difference as a refund. A nonrefundable credit can only reduce your tax to zero — any remaining credit amount is generally lost.

Does a tax deduction give me money back?

Not directly. A deduction lowers your taxable income, which may result in a lower tax bill or a larger refund — but it does not produce a refund on its own. Only refundable tax credits can result in a direct payment from the IRS.

What are the most common federal tax credits?

The most widely claimed federal tax credits include the Child Tax Credit ($2,200 per qualifying child), the Earned Income Tax Credit (up to $8,231 for families with three or more children), the American Opportunity Tax Credit ($2,500 per eligible student), the Lifetime Learning Credit ($2,000 per return), and the Saver’s Credit (up to $1,000 for eligible retirement savers). Each has specific income limits and eligibility requirements.

Related Articles

Official Resources

This article is for educational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual circumstances vary. Consult a qualified tax professional for advice specific to your situation. eataxwise.com is not affiliated with the IRS or any government agency.