What Is a W-9?

Form W-9 is how businesses collect your taxpayer identification number before paying you as a non-employee. The form itself never goes to the IRS — but the information on it does, through a 1099 at the end of the year. If you skip or misfile your W-9, the payer may withhold 24% of your income automatically.

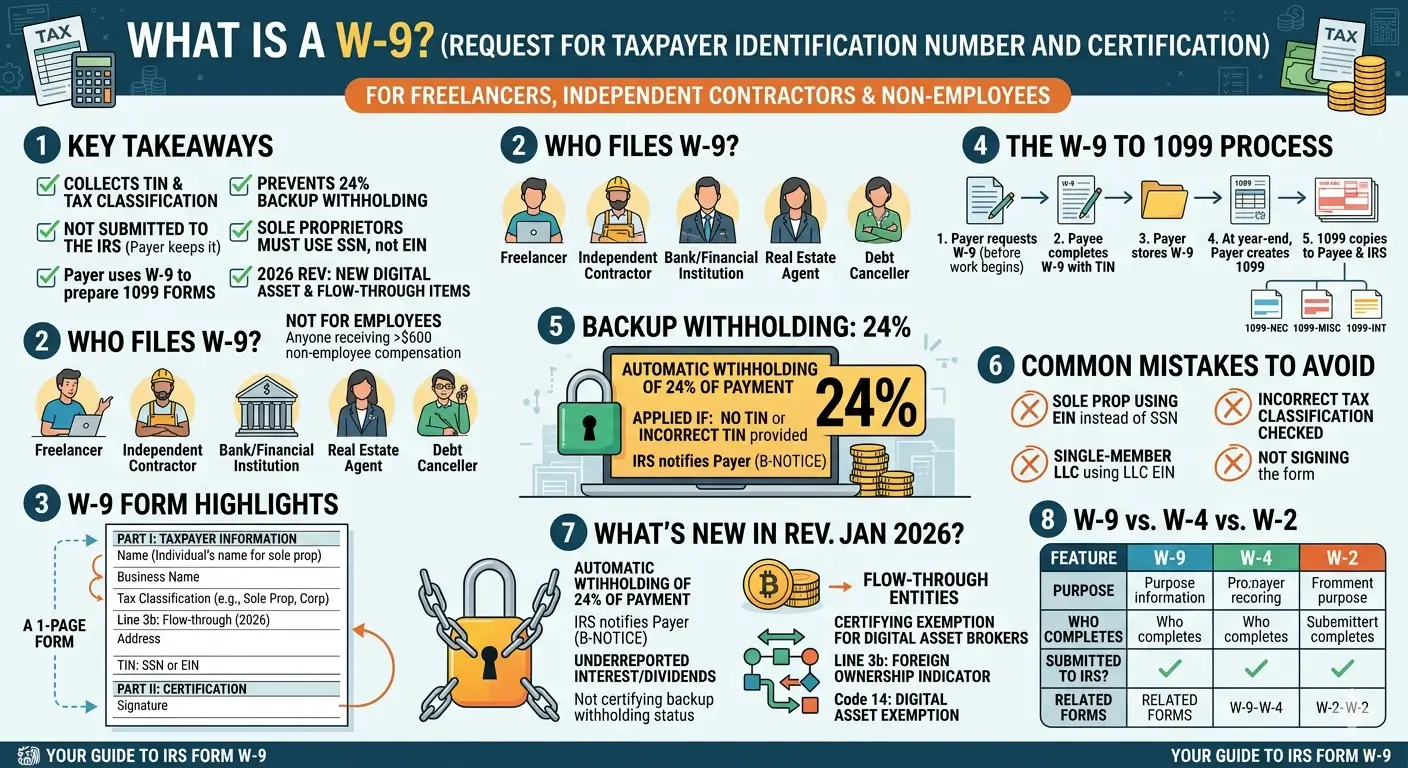

Key Takeaways

- Form W-9 collects your Taxpayer Identification Number (TIN) and tax classification — it is not filed with the IRS.

- The payer uses your W-9 information to prepare year-end information returns such as Form 1099-NEC or 1099-MISC.

- Failing to submit a W-9 — or submitting one with incorrect information — can trigger backup withholding at 24% of your payments.

- Sole proprietors must enter their SSN, not an EIN. Single-member LLCs (disregarded entities) must use the owner’s TIN.

- The January 2026 revision adds new fields for digital asset brokers and a new Line 3b for flow-through entities with foreign ownership.

- W-9 applies only to non-employees — employees complete Form W-4 instead.

Table of Contents

- 1. What Is Form W-9?

- 2. Who Needs to Fill Out a W-9?

- 3. What Information Does a W-9 Collect?

- 4. How a W-9 Connects to 1099 Reporting

- 5. What Is Backup Withholding?

- 6. Common W-9 Mistakes

- 7. What Changed in the 2026 Revision?

- 8. W-9 vs. W-4 vs. W-2

- 9. EA Insight

- 10. Frequently Asked Questions

- 11. Related Articles

- 12. Official Resources

1. What Is Form W-9?

Form W-9, Request for Taxpayer Identification Number and Certification, is a one-page IRS form that a payer uses to collect a payee’s Taxpayer Identification Number (TIN) and federal tax classification. The payee — the person or entity receiving payments — fills out the form and returns it to the payer.

The most important thing to understand about the W-9 is this: it is never sent to the IRS. The payer keeps it on file and uses the information to prepare information returns — primarily Forms 1099-NEC, 1099-MISC, or 1099-INT — at the end of the year. Those 1099 forms are what the IRS actually receives.

In other words, the W-9 is a data collection tool. It gathers the information that flows into 1099 reporting.

2. Who Needs to Fill Out a W-9?

You may be asked to complete a W-9 if you are a U.S. person receiving payments that the payer must report to the IRS. Common situations include:

- Freelancers and independent contractors — anyone receiving $600 or more in non-employee compensation

- Bank and brokerage account holders — for reporting interest, dividends, or investment income

- Real estate transaction participants — sellers, landlords, and others involved in reportable property transactions

- Debt cancellation recipients — when a lender forgives $600 or more in debt

- IRA contributors — for reporting contributions to individual retirement accounts

The person who fills out the W-9 is always the payee — the one receiving money. The payer (the business or person making payments) is the one who requests the form.

Important: Employees do not fill out a W-9. If you are hired as an employee, you complete Form W-4 (for income tax withholding) instead. The W-9 is exclusively for non-employees.

3. What Information Does a W-9 Collect?

Form W-9 has two parts. Part I collects your taxpayer information, and Part II is a certification that you sign under penalties of perjury.

Part I — Taxpayer Information

| Line | What You Enter |

|---|---|

| 1 | Your legal name (sole proprietors enter the owner’s personal name) |

| 2 | Business name or DBA (if different from Line 1) |

| 3a | Federal tax classification (Individual, C Corp, S Corp, Partnership, Trust/Estate, or LLC with tax code) |

| 3b | Whether the flow-through entity has direct or indirect foreign partners, owners, or beneficiaries (new in 2026) |

| 4 | Exempt payee code and FATCA exemption code (if applicable) |

| 5–6 | Address (street, city, state, ZIP) |

| 7 | Account number(s) (optional — used by the requester) |

| TIN | Social Security Number (SSN) or Employer Identification Number (EIN) |

Part II — Certification

By signing Part II, you certify under penalties of perjury that the TIN you provided is correct, that you are not subject to backup withholding (or, if you are, you cross out that line), that you are a U.S. person, and that any FATCA exemption code is correct.

Note on Line 3b: This line was added in the January 2026 revision. It applies only to flow-through entities (partnerships, trusts, and certain LLCs) that are providing a W-9 to another flow-through entity in which they hold an ownership interest. If this does not describe your situation, you can skip Line 3b.

4. How a W-9 Connects to 1099 Reporting

The W-9 and the 1099 are two halves of the same reporting cycle. Understanding how they connect is the key to understanding why the W-9 matters.

| Step | What Happens |

|---|---|

| 1 | The payer sends a blank W-9 to the payee before making payments |

| 2 | The payee fills in their TIN, name, and tax classification, then returns the form |

| 3 | The payer keeps the W-9 on file (it is not submitted to the IRS) |

| 4 | At year-end, the payer uses the W-9 data to prepare a 1099 form |

| 5 | Copies of the 1099 go to both the payee and the IRS |

The type of 1099 depends on the nature of the payment:

| Payment Type | 1099 Form Issued |

|---|---|

| Non-employee compensation ($600+) | 1099-NEC |

| Rent, royalties, prizes, other income ($600+) | 1099-MISC |

| Interest income ($10+) | 1099-INT |

| Digital asset sales via custodial broker | 1099-DA |

Without a completed W-9, the payer cannot accurately prepare a 1099 — and may be required to apply backup withholding on your payments.

5. What Is Backup Withholding?

Backup withholding is a mechanism that requires the payer to withhold 24% of your payments and send it directly to the IRS. It is triggered when the IRS cannot reliably match your income to your tax return.

Backup withholding applies in four situations:

- You did not provide a TIN on your W-9

- The IRS notified the payer that the TIN you provided is incorrect (known as a B-Notice)

- The IRS notified the payer that you underreported interest or dividend income

- You failed to certify in Part II of the W-9 that you are not subject to backup withholding

The withheld amount is reported on your 1099 (Box 4) and treated as federal income tax already paid. If the withholding exceeds your actual tax liability, you can claim a refund when you file your return. However, the process creates unnecessary cash flow disruption — which is why submitting an accurate W-9 from the start is the simplest way to avoid it.

Key point: Backup withholding at 24% is not a penalty — it is a prepayment of tax. But recovering it requires filing a tax return, which can delay access to your money by months.

6. Common W-9 Mistakes

Mistake 1: Sole Proprietor Enters an EIN Instead of SSN

The IRS requires sole proprietors to provide their Social Security Number on the W-9 — not an Employer Identification Number. Entering an EIN creates a name-TIN mismatch in the IRS system, which can trigger a B-Notice from the IRS to the payer. If the mismatch is not corrected, backup withholding begins.

Mistake 2: Single-Member LLC Uses the Wrong TIN

A single-member LLC that is treated as a disregarded entity for tax purposes must enter the owner’s TIN — not the LLC’s own EIN. If the owner is an individual, this means the owner’s SSN. The tax classification box should be checked as “Individual/sole proprietor,” not “LLC.”

Mistake 3: Incorrect Tax Classification on Line 3a

If you check the “LLC” box, you must also enter the appropriate tax classification code: C for C corporation, S for S corporation, or P for partnership. Leaving this blank — or checking the wrong box — can cause processing errors and delay 1099 issuance.

Mistake 4: Missing Signature in Part II

An unsigned W-9 is not valid. Without a signature, the payer cannot rely on the form to prepare a 1099, and backup withholding may apply. The signature can be handwritten or electronic.

7. What Changed in the 2026 Revision?

The IRS released a revised Form W-9 dated January 2026 (Rev. 1-2026) with several notable updates:

Digital Asset Broker Provisions

A new checkbox has been added to the Part II certification section. It allows certain U.S. digital asset brokers to certify that they are exempt from information reporting requirements under specific IRS regulations. A new exempt payee code — Code 14 — has also been introduced for digital asset transactions that qualify for backup withholding exemption. These changes align the W-9 with the broader rollout of Form 1099-DA for digital asset reporting.

New Line 3b for Flow-Through Entities

Line 3b is a newly added field for flow-through entities — partnerships, trusts, and certain LLCs taxed as partnerships. When providing a W-9 to another flow-through entity in which they have an ownership interest, these entities must now indicate whether they have direct or indirect foreign partners, owners, or beneficiaries. This information helps the receiving entity determine its own reporting obligations.

TIN Clarifications

The 2026 revision reinforces existing rules with greater emphasis: sole proprietors must use their SSN (not an EIN), and disregarded entities must use the owner’s TIN. These clarifications are intended to reduce the volume of IRS B-Notices caused by name-TIN mismatches.

8. W-9 vs. W-4 vs. W-2

| Feature | W-9 | W-4 | W-2 |

|---|---|---|---|

| Purpose | Collect TIN from non-employees | Set payroll withholding for employees | Report employee wages and withholding |

| Filled Out By | Non-employee (freelancer, contractor) | Employee | Employer (provided to employee and IRS) |

| Filed With IRS? | No — kept by the payer | No — kept by the employer | Yes — filed with SSA/IRS |

| Connected Form | 1099-NEC, 1099-MISC, etc. | Payroll withholding calculation | Individual tax return (Form 1040) |

| Tax Withholding | None (24% backup withholding if W-9 is missing or incorrect) | Income tax + FICA withheld from paycheck | Reports amounts already withheld |

The fundamental difference: a W-9 means “I am not an employee, and I handle my own taxes.” The payer does not withhold income tax or FICA from payments to a W-9 payee (unless backup withholding applies). In contrast, an employee who submits a W-4 has income tax and FICA automatically withheld from every paycheck by the employer.

EA Insight

The two most common W-9 problems I see in practice come down to the same root cause: using the wrong TIN.

First, freelancers and independent contractors ignore or delay a W-9 request. Without a TIN on file, the payer is required to apply backup withholding — 24% is automatically deducted from every payment. Getting that money back requires filing a tax return, and in the meantime, your cash flow takes a hit. Even if the freelance income is modest, losing nearly a quarter of each payment adds up fast.

Second, sole proprietors and single-member LLC owners enter an EIN instead of their SSN. When the IRS system cannot match the name on the return to the TIN on the 1099, a B-Notice is issued. If it is not resolved, backup withholding starts. I’ve seen new freelancers assume that “having a business means using an EIN,” but the IRS rule is clear — sole proprietors report under their SSN. If your single-member LLC’s owner is a corporation rather than an individual, then the corporation’s EIN is the correct TIN — but that is a less common situation.

The W-9 is a simple one-page form, but filling it out incorrectly leads to B-Notices, backup withholding, and unnecessary refund delays. Take the time to get it right the first time.

Frequently Asked Questions

Do I need to submit a new W-9 every year?

No. A W-9 remains valid as long as your information — name, address, TIN, and tax classification — has not changed. You only need to submit a new one if any of those details change or if the payer requests an updated form.

Does the IRS see my W-9?

Not directly. The W-9 stays with the payer. At the end of the year, the payer uses the W-9 information to prepare a 1099 form, and the 1099 is what the IRS receives. The IRS can request the W-9 during an audit or examination, but it is not routinely submitted.

My employer asked me for a W-9. Is that correct?

If you are a regular employee, you should be filling out a W-4 — not a W-9. A W-9 request from an employer may indicate that they are classifying you as an independent contractor rather than an employee. This distinction matters because it affects your tax obligations, benefits, and labor protections. If you are unsure about your classification, review the terms of your working relationship carefully.

I’m uncomfortable putting my SSN on a W-9. Can I refuse?

If you decline to provide a TIN, the payer is required to apply backup withholding at 24% on your payments. A TIN — either your SSN or EIN — is a mandatory field on the W-9. If security is a concern, you can ask the requester to use a secure delivery method such as an encrypted file or a secure online portal rather than email.

What happens if I provide an incorrect TIN?

The IRS may impose a penalty of $50 per incorrect TIN under IRC §6723. If the incorrect information is provided intentionally, the civil penalty can reach up to $500, and criminal penalties may also apply. Additionally, an incorrect TIN triggers the B-Notice process, which can lead to backup withholding.

Do non-U.S. persons fill out a W-9?

No. Form W-9 is for U.S. persons only. Under IRS rules, “U.S. person” includes U.S. citizens, permanent residents (green card holders), and resident aliens who meet the substantial presence test. If you do not fall into any of these categories, you would complete a Form W-8 series (such as W-8BEN for individuals or W-8BEN-E for entities) instead.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.