What Is IRS Circular 230?

The federal ethics and conduct rulebook that every attorney, CPA, and Enrolled Agent must follow when representing taxpayers before the IRS — and the standard every taxpayer should know when choosing a tax professional.

Key Takeaways

- Circular 230 sets the rules of conduct for tax professionals who represent clients before the IRS, including attorneys, CPAs, and Enrolled Agents (EAs).

- It is codified at 31 CFR Part 10, with statutory authority from 31 U.S.C. §330.

- The Office of Professional Responsibility (OPR) investigates violations and imposes discipline.

- Sanctions range from censure to suspension, disbarment, and monetary penalties — which can apply to firms as well as individuals.

- For taxpayers, Circular 230 is a baseline quality standard: it helps separate credentialed professionals from unregulated preparers.

Table of Contents

- 1. What Is Circular 230?

- 2. Who Is Subject to Circular 230?

- 3. What “Practice Before the IRS” Means

- 4. Key Duties Under Circular 230

- 5. Prohibited Conduct

- 6. Sanctions for Violations

- 7. Why Circular 230 Matters to Taxpayers

- 8. EA Insight

- 9. Frequently Asked Questions

- 10. Related Articles

- 11. Official Resources

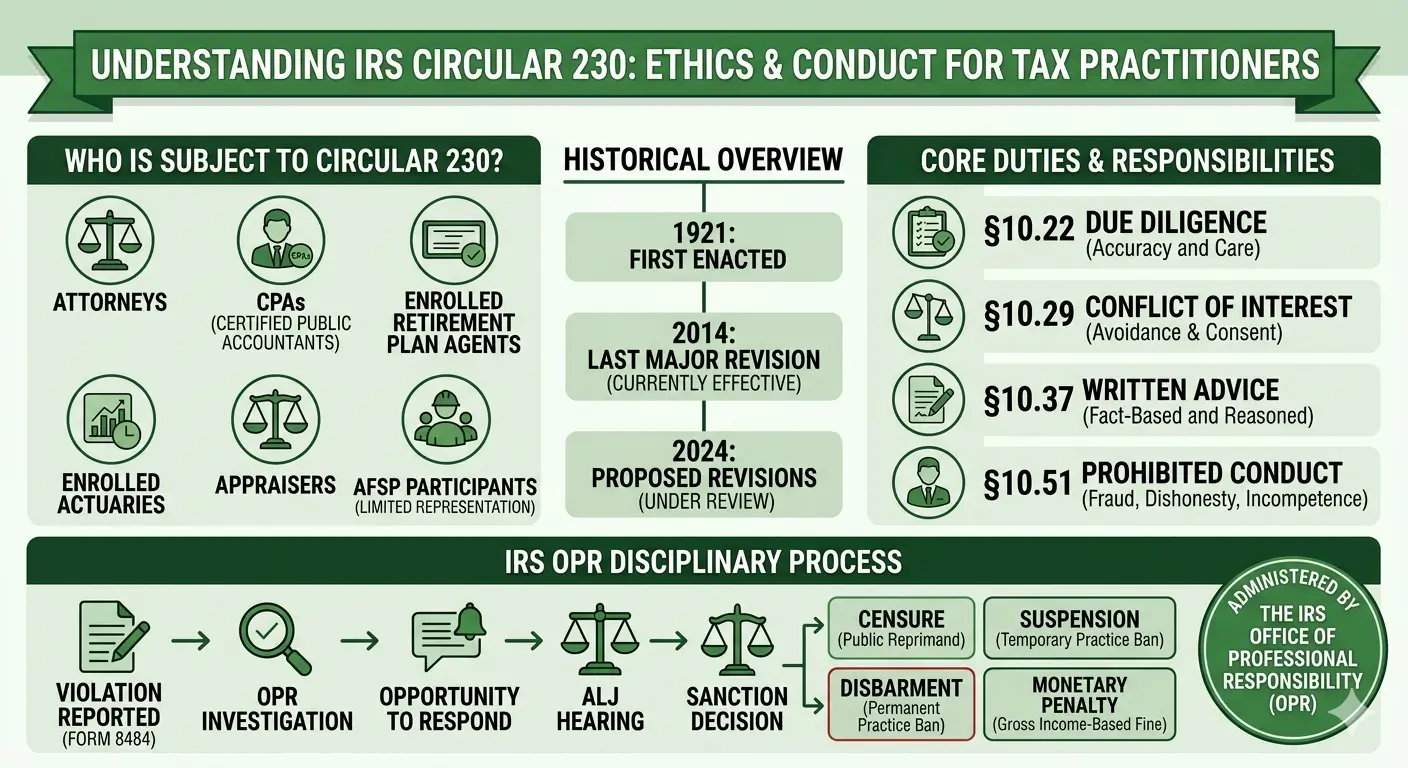

1. What Is Circular 230?

Circular 230 is the common name for Regulations Governing Practice Before the Internal Revenue Service, published by the U.S. Department of the Treasury. It sets the ethical and professional standards that federally authorized tax practitioners must meet when they represent, advise, or submit documents on behalf of taxpayers to the IRS.

The regulation is grounded in 31 U.S.C. §330, which authorizes the Secretary of the Treasury to regulate the conduct of those who practice before the Treasury Department. The operative rules appear in Title 31 of the Code of Federal Regulations, Part 10, and are reprinted as Treasury Department Circular No. 230.

First issued in 1921, Circular 230 has been amended many times over the decades. The most recent fully effective version is the June 2014 revision. Proposed amendments are under consideration to modernize several provisions, but until they are finalized, the 2014 regulations remain in force.

2. Who Is Subject to Circular 230?

Circular 230 applies to individuals who represent taxpayers before the IRS or provide written tax advice — not every person who prepares a return. The covered groups include:

- Attorneys — admitted to practice before a state bar and not currently suspended or disbarred.

- Certified Public Accountants (CPAs) — licensed by a state board and in good standing.

- Enrolled Agents (EAs) — federal tax practitioners authorized directly by the IRS, with unlimited representation rights.

- Enrolled Retirement Plan Agents (ERPAs) — limited to retirement plan matters. New enrollments are no longer accepted.

- Enrolled Actuaries — limited representation for specific pension-related issues.

- Appraisers — individuals submitting valuations used in federal tax matters.

- Annual Filing Season Program (AFSP) participants — non-credentialed preparers who voluntarily agree to follow key Circular 230 provisions in exchange for limited representation rights on returns they prepared and signed.

Important: Following the 2014 federal court decision in Loving v. IRS, the mere act of preparing a tax return is not itself “practice before the IRS.” As a result, unregulated paid preparers who do not represent clients — and do not participate in AFSP — fall outside the full scope of Circular 230.

3. What “Practice Before the IRS” Means

Under §10.2(a)(4), “practice before the IRS” covers all matters connected with a presentation to the IRS relating to a taxpayer’s rights, privileges, or liabilities. In practice, this includes:

- Corresponding and communicating with the IRS on a taxpayer’s behalf.

- Representing a taxpayer during examinations, appeals, collections, or administrative hearings.

- Negotiating settlements or installment agreements.

- Providing written tax advice on transactions, plans, or arrangements with potential for tax avoidance or evasion.

- Preparing and filing documents, responses, and protests with the IRS.

Simple data entry or routine mathematical preparation of a return is generally not practice before the IRS. Giving legal or tax opinions, negotiating with an IRS officer, or filing a protest on behalf of a client clearly is.

4. Key Duties Under Circular 230

Circular 230 Subpart B sets the affirmative duties practitioners owe to clients and to the IRS. The table below summarizes the most frequently cited obligations.

| Section | Duty |

|---|---|

| §10.20 | Promptly respond to lawful IRS requests for information. |

| §10.21 | Inform the client of errors or omissions on returns or documents. |

| ★ §10.22 | Exercise due diligence in preparing returns and verifying client representations. |

| §10.28 | Return client records on request; fee disputes do not justify withholding them. |

| ★ §10.29 | Avoid conflicts of interest; written client consent required in limited cases. |

| §10.31 | Do not endorse or negotiate IRS refund checks payable to the client. |

| §10.33 | Follow “best practices” for competent, ethical representation. |

| §10.34 | Avoid unreasonable positions; frivolous return positions are prohibited. |

| §10.35 | Maintain the competency required to handle the matter undertaken. |

| §10.36 | Supervisory duty: firm leaders must ensure staff compliance with Circular 230. |

| §10.37 | Written advice must rest on reasonable assumptions and consider all relevant facts. |

★ indicates the provisions most frequently cited in OPR disciplinary actions.

Due diligence (§10.22) does not mean distrust of the client, but it does mean that a practitioner cannot accept client-provided figures as true when the numbers look inconsistent with other information on the return. Unusually large charitable contributions, for example, should prompt the practitioner to ask for documentation before signing.

Conflicts of interest (§10.29) arise more often than many taxpayers realize. A classic example is representing both spouses in a joint return matter when the couple is separating. The rule does not automatically forbid dual representation, but it requires reasonable belief of competent service to each client and written, informed consent from both.

5. Prohibited Conduct

Section 10.51 defines incompetence and disreputable conduct, which can lead to discipline. Examples include:

- Conviction of any criminal offense involving dishonesty or breach of trust.

- Making false or misleading statements to the IRS or to clients.

- Counseling a client to submit a false or fraudulent return.

- Falsifying records, documents, or tax submissions.

- Misappropriation of client funds.

- Charging an unconscionable fee for services.

- Willfully failing to file the practitioner’s own federal tax returns or pay tax when due.

- Threatening or misleading a person being represented with intent to defraud.

Contingent fees (§10.27): Charging a contingent fee for preparing an original tax return remains prohibited. Following Ridgely v. Lew (D.D.C. 2014), the government cannot enforce the restriction against contingent fees for ordinary refund claims filed before an examination begins. Contingent fees are permitted in narrow circumstances such as IRS examinations, amended returns filed after an audit notice, and certain judicial proceedings.

6. Sanctions for Violations

When the Office of Professional Responsibility finds a violation, the available sanctions under §10.50 include:

| Sanction | What It Means |

|---|---|

| Censure | Public reprimand; practice continues, but the action is recorded by OPR. |

| Suspension | Practice before the IRS barred for a defined period. |

| Disbarment | Indefinite bar from practice before the IRS; reinstatement is possible only after five years and with the burden on the practitioner. |

| Monetary Penalty | Capped at the gross income the practitioner derived from the sanctioned conduct. |

| Appraiser Disqualification | The appraiser may no longer submit valuations in Treasury or IRS proceedings. |

Important: Monetary penalties can reach beyond the individual practitioner. Under 31 U.S.C. §330(b), if the practitioner acted on behalf of an employer, firm, or other entity that knew — or reasonably should have known — of the conduct, the penalty may also be imposed on that employer, firm, or entity.

The disciplinary process generally moves through four stages:

- Intake and investigation — OPR reviews a referral (often on Form 8484) or a third-party complaint.

- Opportunity to respond — the practitioner receives notice and a chance to present a defense.

- Administrative hearing — an Administrative Law Judge (ALJ) conducts a formal proceeding when charges are contested.

- Decision and sanction — OPR issues the final disciplinary determination.

7. Why Circular 230 Matters to Taxpayers

Circular 230 looks like a regulation aimed only at tax professionals, but its practical impact reaches every taxpayer who hires one.

- A built-in quality standard. Attorneys, CPAs, and EAs operate inside a regulatory structure where serious misconduct can end their career. That accountability is itself a form of consumer protection.

- Representation rights are tied to credentials. Only attorneys, CPAs, and EAs have unlimited rights to represent taxpayers on any matter before the IRS. AFSP participants and unregulated preparers have narrower rights or none at all.

- A path for complaints. If a tax professional misleads a client, misuses funds, or otherwise violates the rules, the taxpayer can file Form 14157 (general preparer complaint) or have misconduct reported via Form 8484 to OPR.

- Verification before engagement. The IRS’s Directory of Federal Tax Return Preparers with Credentials and Select Qualifications lets taxpayers confirm a preparer’s PTIN and credentials before handing over sensitive records.

EA Insight

Circular 230 is often framed as a cage around tax professionals. In practice it works more like a fence — one that protects honest practitioners as much as it restricts bad actors. The fence is what gives a client a reason to trust a signature on a return.

The Enrolled Agent exam devotes an entire section (Part 3) to representation and ethics. Every three years, EAs must complete a minimum of two hours of ethics continuing education as part of renewal. These requirements are not decorative — the practitioners who treat them seriously tend to be the same ones who ask follow-up questions when something on a client document looks off.

The most common trap I see is the assumption that “the client’s numbers are the client’s responsibility.” Section 10.22 due diligence does not require a forensic audit, but it does require a reasonable look at what does not add up. A return signed without that look is a return the preparer is ultimately accountable for.

For taxpayers, one quick question carries more weight than any credential search: “Will you sign my return and include your PTIN?” A legitimate paid preparer will say yes without hesitation. Then verify that PTIN on the IRS Directory — the entry will tell you whether you are working with an attorney, CPA, EA, or AFSP participant, and whether that person is actually inside the Circular 230 perimeter.

Frequently Asked Questions

Who enforces Circular 230?

The IRS Office of Professional Responsibility (OPR) has exclusive authority to investigate and discipline practitioners covered by Circular 230.

Does Circular 230 apply to all paid tax preparers?

No. After Loving v. IRS, simple return preparation is not “practice before the IRS.” Circular 230 applies in full to attorneys, CPAs, EAs, ERPAs, enrolled actuaries, and appraisers. AFSP participants voluntarily agree to follow the core provisions.

How do I report a tax professional for misconduct?

File Form 8484 to report suspected Circular 230 violations to OPR. For broader complaints about preparer conduct, Form 14157 is also available.

What is the difference between an EA, a CPA, and a tax attorney?

All three hold unlimited rights to represent taxpayers before the IRS. An EA is a federal credential issued by the IRS and focused specifically on tax. A CPA holds a state accounting license, and a tax attorney holds a state bar license with legal training.

Has Circular 230 changed recently?

The Treasury Department and IRS have published proposed amendments to modernize several parts of Circular 230, and a public hearing has been held. Those proposals are not yet final, so the operative text remains the June 2014 revision.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation.