What Is Federal Income Tax? How It Works

Federal income tax is the largest single tax most Americans pay — and the one they understand least. If you have ever received a W-2 or a 1099, you are already part of this system. The moment you understand how it is actually calculated, the line between a refund and a surprise tax bill becomes clear.

Key Takeaways

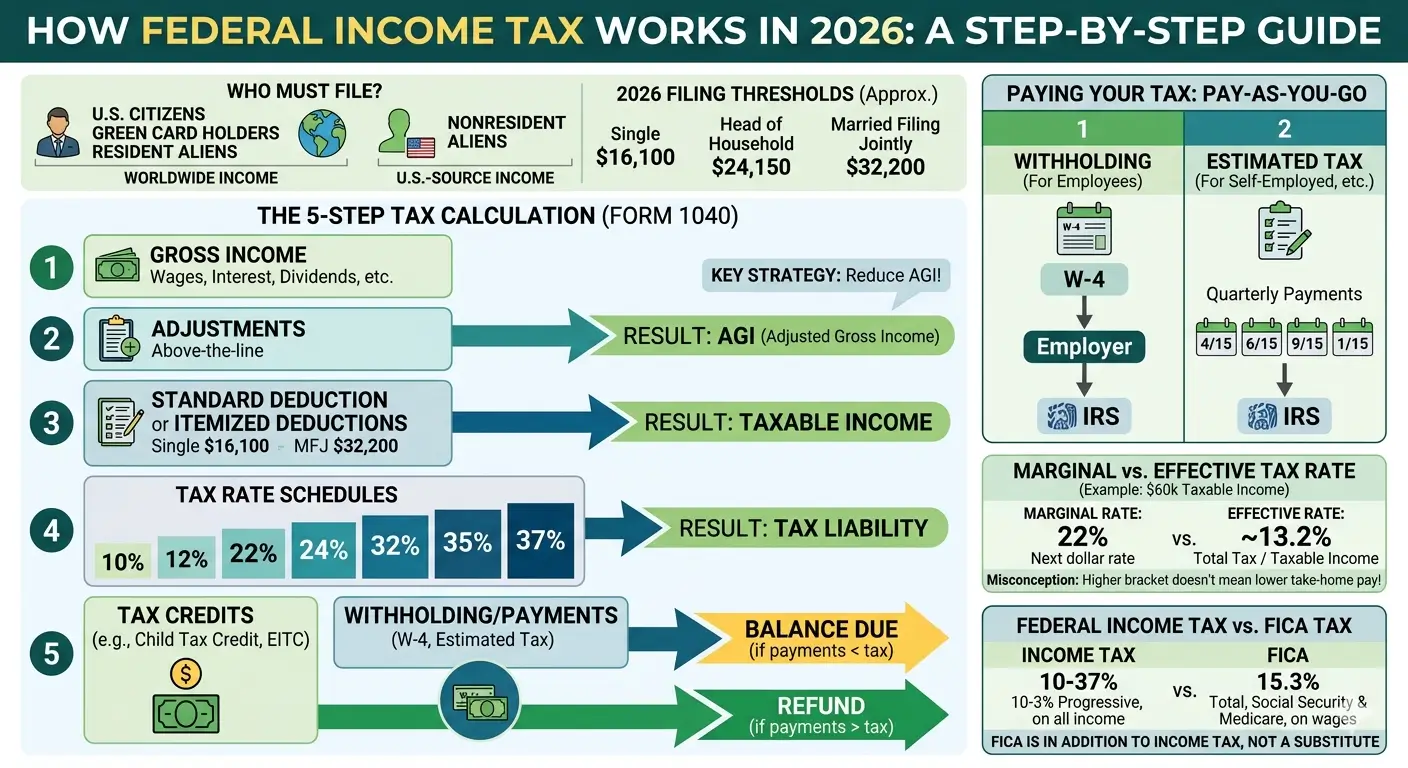

- Federal income tax is collected by the IRS on the worldwide income of U.S. citizens, resident aliens, and certain foreign persons with U.S.-source income.

- The U.S. uses a progressive tax system with seven marginal rates: 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

- Your tax is calculated in five steps: Gross Income → AGI → Taxable Income → Tax Liability → Balance Due or Refund.

- Marginal rate (the rate on your next dollar) and effective rate (your average tax rate) are not the same thing.

- Filing status changes both your bracket thresholds and your standard deduction amount.

- Federal income tax works on a pay-as-you-go basis — through paycheck withholding or quarterly estimated tax payments.

- FICA (Social Security and Medicare) and self-employment tax are separate from federal income tax, not substitutes for it.

Table of Contents

- 1. What Is Federal Income Tax?

- 2. Who Has to Pay Federal Income Tax?

- 3. The Progressive Tax System — Why Brackets Exist

- 4. The Five-Step Calculation

- 5. Marginal Rate vs. Effective Rate

- 6. How Filing Status Shapes Your Tax

- 7. How Federal Income Tax Is Actually Paid

- 8. Federal Income Tax vs. Other Federal Taxes

- 9. EA Insight

- 10. Frequently Asked Questions

- 11. Related Articles

- 12. Official Resources

1. What Is Federal Income Tax?

Federal income tax is the tax the IRS imposes on the income of individuals, corporations, estates, and trusts at the federal level. Its legal foundation is the Internal Revenue Code (IRC), and individuals report and settle this tax each year using Form 1040.

Federal income tax is a separate tax from state income tax. Federal rules apply uniformly in every state, while state income tax varies — and nine states (Texas, Florida, Nevada, Washington, South Dakota, Wyoming, Alaska, Tennessee, and New Hampshire) do not impose an income tax on wages at all.

The constitutional basis for the modern federal income tax is the Sixteenth Amendment, ratified in 1913. The very first Form 1040 was introduced that same year.

2. Who Has to Pay Federal Income Tax?

The scope of the U.S. federal income tax is broader than many people realize:

- U.S. citizens and lawful permanent residents (green card holders) — taxed on their worldwide income, regardless of where they live.

- Resident aliens — taxed on worldwide income if they meet the Substantial Presence Test.

- Nonresident aliens — taxed only on U.S.-source income and income effectively connected with a U.S. trade or business (filed on Form 1040-NR).

Whether you are required to file depends on your filing status, age, dependent status, and gross income compared to the IRS filing threshold — which is adjusted annually. As a general rule, once your income exceeds roughly the standard deduction for your filing status, a return is required.

Important: Not being required to file is not the same as not needing to file. If federal tax was withheld from your pay, or if you qualify for a refundable credit like the Earned Income Tax Credit, you must file a return to get that money back.

3. The Progressive Tax System — Why Brackets Exist

The U.S. federal income tax is progressive. Income is divided into tiers, and each tier is taxed at its own rate. The current structure uses seven marginal rates: 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

Here is the single most common misunderstanding about tax brackets:

Myth: “If I move into the 24% bracket, all of my income is taxed at 24%.”

Reality: Only the portion of income inside each bracket is taxed at that bracket’s rate.

Consider a single filer with gross income of $76,100. After subtracting the standard deduction of $16,100, taxable income is $60,000. Here is how federal income tax actually applies to that $60,000:

| Income Range | Rate | Income Taxed in This Bracket | Tax in This Bracket |

|---|---|---|---|

| $0 – $12,400 | 10% | $12,400 | $1,240 |

| $12,400 – $50,400 | 12% | $38,000 | $4,560 |

| $50,400 – $60,000 | 22% | $9,600 | $2,112 |

| Total | — | $60,000 | $7,912 |

This taxpayer’s marginal rate is 22%, but the actual tax owed is $7,912 — about 13.2% of taxable income. That gap is exactly the difference between a marginal rate and an effective rate.

4. The Five-Step Calculation

Federal income tax is calculated in five sequential steps. The output of each step becomes the input for the next:

| Step | Action | Result |

|---|---|---|

| 1 | Add all taxable income (wages, interest, dividends, business income, capital gains, etc.) | Gross Income |

| 2 | Subtract adjustments (above-the-line deductions on Schedule 1) | Adjusted Gross Income (AGI) |

| 3 | Subtract the standard deduction or itemized deductions | Taxable Income |

| 4 | Apply the tax rate schedule to taxable income | Tax Liability Before Credits |

| 5 | Subtract tax credits, then withholding and estimated payments | Balance Due or Refund |

Because each step’s result feeds into the next, anything that lowers AGI also lowers everything below it. That is why so many tax planning strategies — retirement contributions, HSA contributions, pre-tax elections — begin with managing AGI, not chasing deductions at the bottom of the return.

5. Marginal Rate vs. Effective Rate

These are two of the most important numbers in your tax picture — and they are often confused.

| Concept | Definition | Example ($60K Single) |

|---|---|---|

| Marginal Rate | Rate applied to your next dollar of taxable income — the top bracket you reach | 22% |

| Effective Rate | Total federal income tax divided by taxable income — your average rate | ~13.2% |

Use the marginal rate when you are evaluating a bonus, a raise, a side income opportunity, or a deductible contribution — it tells you what the next dollar will cost in tax, or what a deduction will save.

Use the effective rate when you want to understand your overall tax burden or compare it across years. It is also the honest answer to “how much of my income actually goes to federal tax?”

6. How Filing Status Shapes Your Tax

There are five federal filing statuses:

- Single

- Married Filing Jointly (MFJ)

- Married Filing Separately (MFS)

- Head of Household (HoH)

- Qualifying Surviving Spouse (QSS)

Your filing status affects three major components of your federal tax:

- Bracket widths. The same 37% top rate, for example, starts at $640,600 of taxable income for Single filers but at $768,700 for Married Filing Jointly.

- Standard deduction amount. Currently, Single and MFS filers claim $16,100, Head of Household filers claim $24,150, and Married Filing Jointly filers claim $32,200.

- Credit and deduction phase-out thresholds. Income limits for the Earned Income Tax Credit, the Child Tax Credit, student loan interest deduction, and many other provisions all depend on filing status.

Choosing the wrong filing status — or failing to qualify for Head of Household when you could — can easily cost several thousand dollars on a single return.

7. How Federal Income Tax Is Actually Paid

Federal income tax is not a once-a-year April payment. The IRS expects to receive your tax in installments throughout the year. This is the pay-as-you-go principle.

There are two main mechanisms:

- Withholding — Your employer withholds tax from each paycheck based on your Form W-4 and sends it to the IRS on your behalf.

- Estimated Tax — Self-employed individuals, landlords, and people with significant investment income pay quarterly on their own using Form 1040-ES. The standard due dates are April 15, June 15, September 15, and January 15 of the following year.

April 15 is a settlement date, not a payment date. When the tax you already paid during the year is less than your actual liability, you owe the difference. When you paid more than needed, you get a refund. A large refund is not a bonus — it means you lent money to the IRS interest-free for the entire year.

If you underpay throughout the year, the IRS can assess an underpayment penalty. You generally avoid it if your total payments during the year equal at least 100% of last year’s tax (or 110% if your prior-year AGI exceeded $150,000) or 90% of the current year’s tax, whichever is smaller.

Practical point: The percentage safe harbor is not the only protection. Under IRC §6654(e)(1), no underpayment penalty applies if your total balance due on the return is less than $1,000 after subtracting withholding and refundable credits. For many W-2 employees with modest side income, this de minimis rule is the first line of defense.

8. Federal Income Tax vs. Other Federal Taxes

“Federal taxes” is a broader category than federal income tax alone. Several other federal taxes exist side by side with it:

| Tax | Applies To | Rate |

|---|---|---|

| Federal Income Tax | All taxable income | 10% – 37% (progressive) |

| FICA (Social Security + Medicare) | Wages (employer matches) | 7.65% employee + 7.65% employer |

| Self-Employment Tax (SECA) | Net self-employment earnings | 15.3% |

| Additional Medicare Tax | High-income wages and self-employment | 0.9% above threshold |

| Net Investment Income Tax (NIIT) | Investment income of higher earners | 3.8% above MAGI threshold |

| Estate & Gift Tax | Transfers above the lifetime exemption | Up to 40% |

| Excise Tax | Specific goods and services (fuel, alcohol, airline tickets) | Varies |

The key point is this: FICA and self-employment tax are not substitutes for federal income tax — they are additional federal taxes. A W-2 employee pays federal income tax and FICA from every paycheck. A sole proprietor pays federal income tax and self-employment tax on the same business earnings.

EA Insight

The question I hear most often in client meetings is some version of “what tax bracket am I in?” A precise answer actually requires three different numbers — the marginal rate, the effective rate, and the withholding rate the employer is applying right now. They are rarely the same, and conflating them is the source of most tax surprises.

The single most persistent myth I encounter is the fear of “moving into a higher bracket.” It is mathematically impossible for a raise or a bonus to leave you with less take-home pay than you had before. Additional income only pushes the dollars above the bracket threshold into the higher rate — everything below stays exactly where it was. If a client ever tells me they turned down extra work to “avoid moving up,” I know we have some rebuilding to do.

One more point worth making: a large refund is not a win. It means you gave the government an interest-free loan for twelve months. If your refund is consistently in the thousands, adjust your Form W-4 — that money belongs in your own account earning interest, paying down debt, or funding a retirement contribution. On the other side, if you owe every April, run the numbers against the safe harbor rules before the year ends. Quarterly estimated payments are not just for the self-employed.

The fastest way to truly understand federal income tax is to fill out Form 1040 once, line by line, and watch each number flow into the next. Once you see it happen on paper, ninety percent of the confusion disappears.

Frequently Asked Questions

Is the federal income tax actually constitutional?

Yes. The Sixteenth Amendment, ratified in 1913, explicitly grants Congress the power to lay and collect taxes on income. Every federal income tax return filed since then rests on that constitutional authority.

Is any income not subject to federal income tax?

Yes. Interest on most municipal bonds, qualified Roth IRA withdrawals, gifts (for the recipient), inheritances (for the recipient), qualified scholarships, and certain employer-provided fringe benefits are not subject to federal income tax. See our article on tax-exempt income for a fuller list.

Are FICA taxes the same as federal income tax?

No. They are entirely separate federal taxes. W-2 employees have federal income tax and FICA withheld from every paycheck — both of them, not one or the other.

What if I do not earn enough to owe any federal income tax?

If your income is below the filing threshold for your filing status, you are not required to file a return. However, if federal tax was withheld from your pay, or if you qualify for a refundable credit like the Earned Income Tax Credit, you must file a return to receive the refund or credit.

Can I deduct my state income tax from my federal tax?

Only to a limited extent. If you itemize deductions on Schedule A, state and local income taxes can be deducted as part of the SALT deduction, subject to a statutory cap. If you take the standard deduction, state income tax does not reduce your federal tax.

How are tax brackets adjusted each year?

The IRS publishes annual inflation adjustments in a Revenue Procedure each fall. Since the Tax Cuts and Jobs Act, the inflation measure used is the Chained Consumer Price Index (C-CPI-U), which grows more slowly than the traditional CPI.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.