Maxing Out Their 401(k) Wasn’t the Answer — Their Health Insurance Was

David and Karen did exactly what a coworker told them to do: put as much into the 401(k) as the match allowed. Good advice for retirement. The trouble sat somewhere else entirely. What was really on the line for this couple wasn’t their retirement — it was next year’s health insurance.

Key Takeaways

- An employer match is an immediate 100% return. Capturing it almost always makes sense.

- Pre-tax (Traditional) retirement contributions do more than build savings — they lower the MAGI that decides your health insurance subsidy.

- Roth doesn’t do this. Only a Traditional 401(k) and a deductible Traditional IRA bring MAGI down.

- A spouse with no workplace plan can still lower MAGI through their own Traditional IRA.

- Contributing past what your budget can handle turns a tax-saving plan into a household strain. The goal isn’t “the most” — it’s “the right number.”

Table of Contents

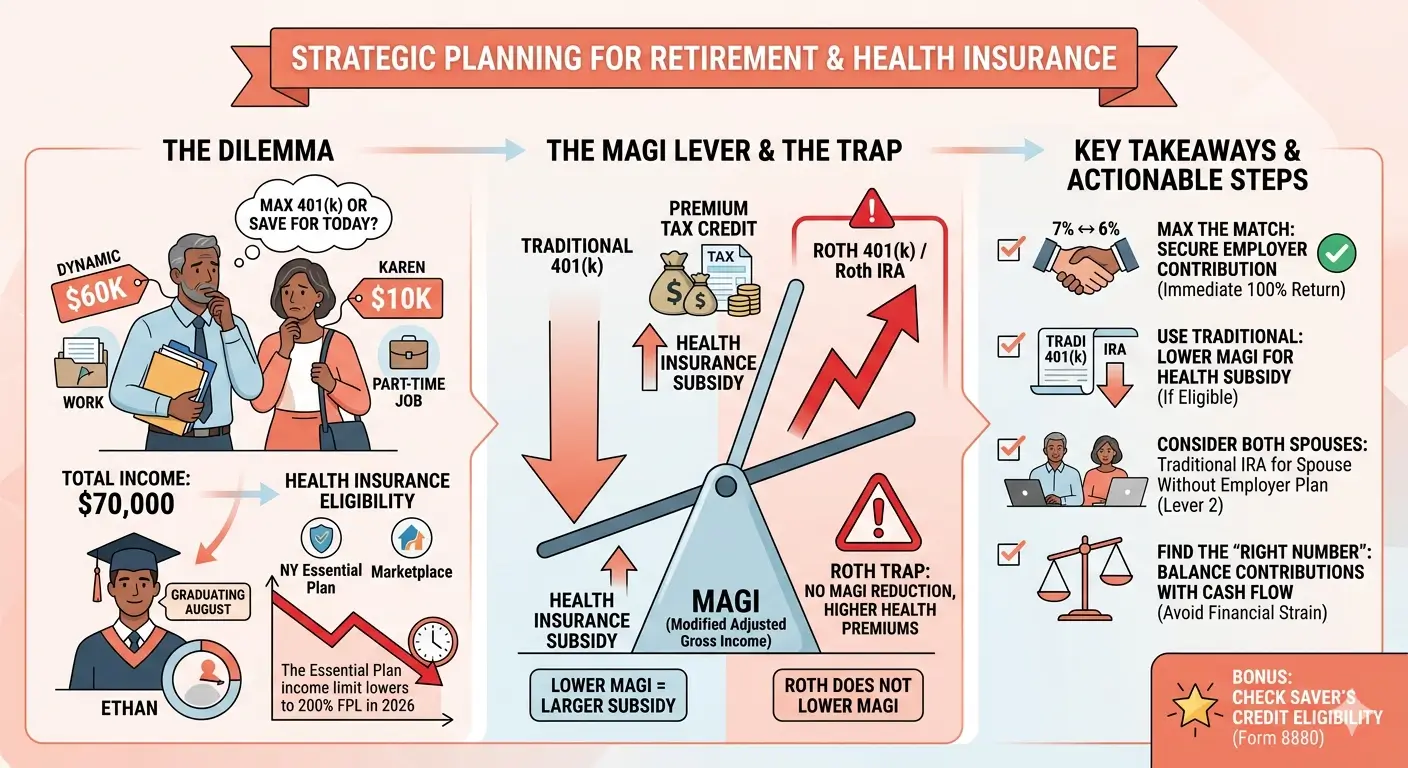

1. David and Karen’s Dilemma

David earns $60,000 this year. His employer offers a 3% match on the 401(k). Karen works part-time and brings in around $10,000. Together, that’s roughly $70,000. Their son Ethan is 22, a full-time student, and graduates in August.

For years this family kept health coverage through New York’s Essential Plan at almost no cost. Their income climbed this year, and David started to worry.

David got stuck between the advice to fund retirement and the reality of the monthly budget. The problem he actually needed to solve sat on the side his coworker never mentioned.

2. The Real Issue Is the Income Line for Coverage

New York’s Essential Plan stays available only while household income falls below a set share of the federal poverty level (FPL). Right now that line sits at 250% of FPL — about $66,625 for a three-person household. David and Karen’s combined $70,000 already crosses it.

A bigger change is coming. Because of federal funding cuts, New York’s Essential Plan drops its income limit to 200% of FPL on July 1, 2026 — roughly $53,300 for a household of three. Pulling income down to that line would take tens of thousands of dollars in retirement contributions. That’s nowhere near what this couple can afford.

So the realistic answer isn’t chasing a disappearing Essential Plan line. The next stop is a Marketplace health plan (a Qualified Health Plan) and the Premium Tax Credit (PTC) that helps pay for it.

Bottom line

As income rises, families move from a free Essential Plan to a subsidized Marketplace plan. The size of that subsidy comes down to one number: MAGI.

3. One Lever: MAGI

The Marketplace subsidy gets calculated from your household’s MAGI (modified adjusted gross income). One more thing matters this year. The “subsidy cliff” is back — earn more than 400% of FPL and the credit disappears entirely. For a three-person household, 400% of FPL runs about $106,600. David and Karen sit well below that, so they clearly qualify for help.

Here’s the part that changes everything. A lower MAGI means a larger PTC. Pre-tax retirement contributions push that MAGI down directly. Every dollar David puts into a pre-tax 401(k) is retirement savings and a cut to next year’s insurance bill at the same time. One dollar, working in two places.

4. What If They’d Chosen Roth?

This is where the most common mistake shows up. Someone hears “max it out” and routes the money into a Roth.

Look only at the match, and Traditional or Roth makes no difference — the employer’s contribution is the same either way. Look at the subsidy, and they’re worlds apart. Only a Traditional 401(k) and a deductible Traditional IRA lower MAGI. Roth money is already taxed, so it does nothing to your MAGI.

For a family sitting near the subsidy line, the same dollar lands very differently depending on where it goes. That single choice can swing next year’s premium by hundreds of dollars.

5. When the Situation Changes

Karen Has No Workplace Plan

Karen’s part-time job comes with no retirement plan. She can still open and fund her own Traditional IRA. Their income sits far below the deduction phase-out, so her contribution is fully deductible. Add Karen’s IRA to David’s 401(k), and there’s more room to bring MAGI down. You only see it when you treat the couple as one unit.

Practical point

A spouse without a workplace plan isn’t out of options. Their Traditional IRA is a second MAGI lever.

Ethan Graduates in August

Once Ethan finishes school and starts working, he’ll likely drop off his parents’ return as a dependent next year. That shrinks the health insurance household from three people to two. A smaller household pulls every income line down with it. Income that’s fine against a three-person limit this year can bump into a two-person limit next year. Half of David’s “what do we do next year” worry lives right here.

When the Match Is Enough

“Contribute more” isn’t the answer for everyone. When cash flow is genuinely tight, funding the match and stopping there is the right call. The match is free money, so walking away from it costs you. Beyond that point, though, there’s no reason to contribute at the expense of paying the rent. Overfunding turns a tax plan into pressure on the very household it was meant to help.

Important: Income limits, FPL figures, and the Marketplace subsidy rules can shift from year to year. Estimate your own numbers before open enrollment, and confirm current limits on IRS.gov and your state Marketplace before you decide how much to contribute.

6. What to Check Right Now

- Find your employer’s match rate and the minimum contribution needed to get all of it.

- Confirm whether your contributions are pre-tax (Traditional) or Roth. If the subsidy is the goal, it needs to be pre-tax.

- Estimate next year’s MAGI before Marketplace open enrollment.

- Look at whether a spouse without a workplace plan can fund a Traditional IRA.

- Check your Saver’s Credit eligibility (Form 8880).

EA Insight

More retirement savings sounds like nothing but good news. It isn’t always.

The case that still bothers me involved a couple who followed the “max it out” advice to the letter. They built a solid retirement balance — and lost their entire health insurance subsidy doing it. They’d funded a Roth, so their MAGI never moved, and their benchmark premium came in about $3,000 higher for the year than it needed to be. They saved well and overpaid for coverage at the same time.

Pre-tax contributions do three jobs at once. They capture the match, they lower the MAGI that sets your subsidy, and — when income is low enough — they unlock the Saver’s Credit. For 2026, a married couple can claim that credit with income up to $80,500, and the lower the income, the higher the credit rate. With pre-tax contributions, David and Karen can reach for a better rate than they’d get otherwise.

As an Enrolled Agent — a tax practitioner federally authorized to represent taxpayers before the IRS — I don’t tell people to “put in the max.” I tell them to capture the match, then decide the rest with both the budget and the subsidy line in view. The right number isn’t “the most.” It’s the point where this household keeps the most while still living comfortably.

EA Summary

The match is the floor, not the ceiling. For a household near the health insurance subsidy line, pre-tax retirement contributions deserve a second look as a MAGI tool. Done right, they build retirement savings, trim the insurance bill, and can open the Saver’s Credit — all without stretching the budget past what it can bear.

Frequently Asked Questions

Can I just take the match and not contribute more?

When money’s tight, that’s often the smart move. Capture the match for sure, but you don’t need to force extra contributions that leave you short on living expenses.

Does putting money in a Roth help with my health insurance subsidy?

No. Only a Traditional 401(k) and a deductible Traditional IRA lower your MAGI. Roth contributions are made with after-tax money, so they leave your MAGI unchanged.

What about a spouse with no workplace retirement plan?

They can fund their own Traditional IRA. When household income is modest and falls below the deduction phase-out, that contribution is usually fully deductible — which gives you a second way to bring MAGI down.

What changes when my child graduates?

If they come off your tax return as a dependent, your health insurance household gets smaller. A smaller household means lower income limits for both Marketplace subsidies and programs like New York’s Essential Plan, so the same income can produce a different result the following year.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.