What Is a W-2? Your Wage & Tax Statement Explained

The W-2 is the document your employer sends you each year showing how much you earned and how much tax was withheld. It’s the starting point of your federal tax return — and understanding each box can help you file accurately and spot potential savings.

Key Takeaways

- Form W-2 reports your total wages, tips, and compensation — plus all federal, state, Social Security, and Medicare taxes withheld during the year.

- Your employer must send your W-2 by January 31 each year.

- Box 1 (Wages, Tips, Other Compensation) is the number that flows directly onto your Form 1040.

- Box 1 is often lower than your total salary because pre-tax deductions (401(k), HSA, health insurance) reduce it.

- Box 12 contains coded entries for retirement contributions, health coverage costs, and — starting with the 2026 form — new OBBBA codes for tips (TP), overtime (TT), and Trump account contributions (TA).

- If you worked for multiple employers, you’ll receive a separate W-2 from each one.

- Keep your W-2 for at least 3–4 years after filing, in case of an IRS audit.

Table of Contents

- 1. What Is a W-2?

- 2. Who Gets a W-2?

- 3. W-2 Boxes Explained: A Complete Guide

- 4. Box 12 Codes: What the Letters Mean

- 5. Why Box 1 Is Different From Your Total Salary

- 6. What Changed on the 2026 W-2 (OBBBA Updates)

- 7. How to Use Your W-2 When Filing Your Tax Return

- 8. What to Do If Your W-2 Is Wrong or Missing

- 9. EA Insight

- 10. People Also Ask

1. What Is a W-2?

Form W-2, officially called the “Wage and Tax Statement,” is the document your employer is required to prepare for you at the end of each calendar year. It reports two main things: how much you were paid and how much tax was withheld from your paychecks.

The W-2 is issued by your employer, not by you. You receive a copy, the Social Security Administration (SSA) receives a copy, and the IRS receives a copy. This is how the government knows what you earned before you even file your return — and it’s why the numbers on your tax return need to match your W-2.

If you are a W-2 employee (meaning your employer withholds taxes from your paycheck), this form is the foundation of your federal income tax return. The wages reported in Box 1 of your W-2 flow directly onto Line 1 of Form 1040.

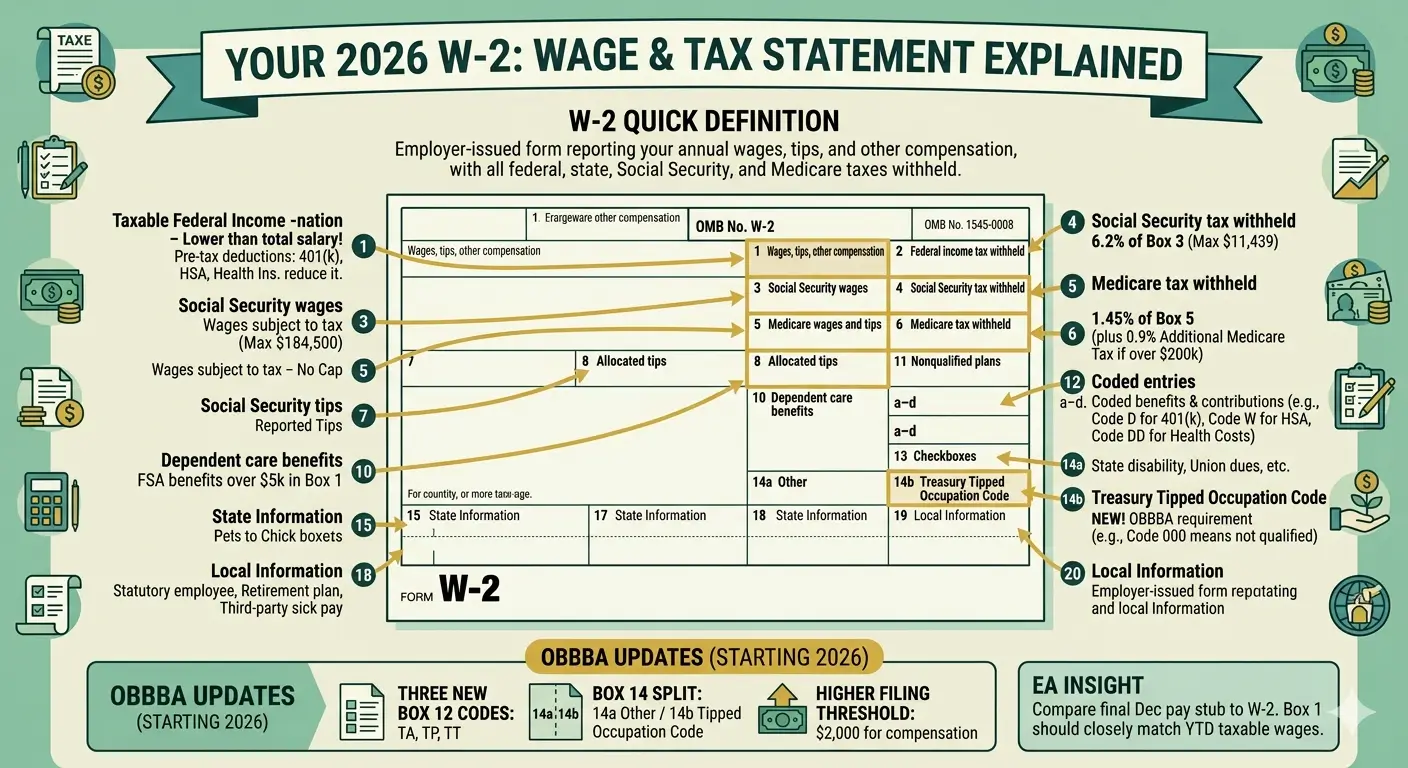

W-2 — Quick Definition

An employer-issued form reporting your annual wages, tips, and other compensation,

along with all federal, state, Social Security, and Medicare taxes withheld.

2. Who Gets a W-2?

You should receive a W-2 if you are an employee — meaning your employer controls what work you do and how you do it, withholds income taxes and FICA taxes from your pay, and reports your wages to the SSA.

You will not receive a W-2 if you are an independent contractor (you’d receive a 1099-NEC instead), self-employed, or receiving income solely from investments, pensions, or government benefits.

If you worked for more than one employer during the year, you will receive a separate W-2 from each one. All of them must be reported on your tax return.

Your employer is required to send (or make available) your W-2 by January 31 of the following year. If you haven’t received it by mid-February, contact your employer first. If that doesn’t resolve it, you can contact the IRS at 1-800-829-1040 for assistance.

3. W-2 Boxes Explained: A Complete Guide

A W-2 has many boxes, and each one serves a specific purpose. The table below explains the most important ones:

| Box | Label | What It Reports |

|---|---|---|

| Box 1 | Wages, Tips, Other Compensation | Your taxable federal income — after pre-tax deductions (401(k), HSA, etc.) |

| Box 2 | Federal Income Tax Withheld | Total federal income tax taken from your paychecks during the year |

| Box 3 | Social Security Wages | Wages subject to Social Security tax (max $184,500 for the current year) |

| Box 4 | Social Security Tax Withheld | 6.2% of Box 3 wages (max $11,439 for the current year) |

| Box 5 | Medicare Wages and Tips | Wages subject to Medicare tax — no cap |

| Box 6 | Medicare Tax Withheld | 1.45% of Box 5 wages (plus 0.9% Additional Medicare Tax if wages exceed $200,000) |

| Box 7 | Social Security Tips | Tips reported to your employer that are subject to Social Security tax |

| Box 8 | Allocated Tips | Tips allocated by your employer (large food/beverage establishments) — not included in Box 1 |

| Box 10 | Dependent Care Benefits | Total dependent care FSA benefits provided (amounts over $5,000 are also in Box 1) |

| Box 11 | Nonqualified Plans | Distributions from nonqualified deferred compensation plans |

| Box 12 | Coded Entries (a–d) | Various benefits and contributions identified by letter codes (see Section 4 below) |

| Box 13 | Checkboxes | Statutory employee, retirement plan participant, or third-party sick pay |

| Box 14a | Other | State disability taxes, union dues, health premiums, educational assistance, etc. (In New York, you may also see PFL — Paid Family Leave — or NYSDI — State Disability Insurance) |

| Box 14b | Treasury Tipped Occupation Code | New — occupation code for employees in tipped positions (OBBBA requirement) |

| Boxes 15–17 | State Information | State employer ID, state wages, and state income tax withheld |

| Boxes 18–20 | Local Information | Local wages and local income tax withheld (if applicable) |

Source: IRS General Instructions for Forms W-2 and W-3 (2026). Social Security wage base of $184,500 per SSA for the current tax year.

4. Box 12 Codes: What the Letters Mean

Box 12 is where employers report specific benefits, contributions, and compensation using letter codes. You may see one or more entries in slots 12a through 12d. These are the codes employees encounter most often:

| Code | Meaning |

|---|---|

| D | Elective deferrals to a 401(k) plan (employee contributions) |

| E | Elective deferrals to a 403(b) plan |

| W | Employer contributions plus employee pre-tax contributions to a Health Savings Account (HSA) — combined total, not employer-only |

| DD | Cost of employer-sponsored health coverage (informational — not taxable) |

| AA | Designated Roth contributions to a 401(k) plan |

| BB | Designated Roth contributions to a 403(b) plan |

| G | Elective deferrals to a 457(b) plan (government/nonprofit) |

New Box 12 Codes — OBBBA (Starting 2026)

The One Big Beautiful Bill Act added three new Box 12 codes to the 2026 Form W-2:

| Code | Meaning |

|---|---|

| TA | Employer contributions to a Trump account (new type of IRA for children under 18) |

| TP | Total amount of cash tips reported — used to calculate the qualified tips deduction |

| TT | Total qualified overtime compensation — used to calculate the overtime deduction |

Employees will use the TP and TT amounts when claiming deductions on Schedule 1-A (Form 1040). These deductions are available for tax years 2025 through 2028.

5. Why Box 1 Is Different From Your Total Salary

One of the most common questions about the W-2 is: “Why is Box 1 lower than my actual salary?” The answer is pre-tax deductions.

Box 1 reports your taxable wages — your gross pay minus certain pre-tax deductions that reduce your federal taxable income. These deductions include:

- Traditional 401(k) or 403(b) contributions (Box 12, Code D or E)

- Health Savings Account (HSA) contributions (Box 12, Code W)

- Employer-sponsored health insurance premiums (your share, paid pre-tax)

- Flexible Spending Account (FSA) contributions

- Commuter/transit benefits

For example, if your annual salary is $75,000 and you contribute $6,000 to a 401(k) and $2,000 to an HSA, your Box 1 would show approximately $67,000 — not $75,000.

Meanwhile, Box 3 (Social Security Wages) and Box 5 (Medicare Wages) may be higher than Box 1 because most pre-tax retirement contributions are still subject to FICA taxes, even though they reduce your federal taxable income.

Example: $75,000 Salary, Single Filer

| Gross Salary | $75,000 |

| 401(k) Contribution (Code D) | − $6,000 |

| HSA Contribution (Code W) | − $2,000 |

| Box 1 (Taxable Wages) | ≈ $67,000 |

| Box 3 / Box 5 (FICA Wages) | ≈ $75,000 |

Simplified example. Actual amounts depend on specific plan types and employer-paid premiums.

6. What Changed on the 2026 W-2 (OBBBA Updates)

The One Big Beautiful Bill Act (OBBBA), signed into law in July 2025, introduced several changes that affect the 2026 Form W-2. These are the key updates:

Three new Box 12 codes were added: TA (Trump account contributions), TP (qualified tips), and TT (qualified overtime compensation). These support the new above-the-line deductions that employees can claim on their individual returns. Important: the tips deduction (TP) and overtime deduction (TT) are temporary — they apply only to tax years 2025 through 2028. These deductions are not permanent and will expire unless Congress extends them.

Box 14 was split into two parts. Box 14a retains the “Other” label for miscellaneous items (state disability taxes, union dues, etc.). The new Box 14b is specifically for the Treasury Tipped Occupation Code — a code that identifies whether an employee’s job qualifies for the tips deduction. If your employer reports code “000” in Box 14b, your tips are not treated as qualified tips for deduction purposes.

Wage reporting threshold increased. For wages paid after calendar year 2025, employers are only required to file a W-2 if total compensation is $2,000 or more (up from $600), provided no federal income, Social Security, or Medicare tax was withheld. This change primarily affects very low-wage or short-term employment situations.

7. How to Use Your W-2 When Filing Your Tax Return

When you sit down to file your federal tax return (Form 1040), the W-2 provides the numbers you need:

Box 1 → Form 1040, Line 1. This is your starting income figure — your wages, salaries, and tips as reported by your employer.

Box 2 → Applied as a credit. The federal income tax your employer already withheld throughout the year is applied against your total tax liability. If Box 2 exceeds what you owe, you get a refund. If it’s less, you owe the difference.

Box 12 codes → Various schedules. If you see Code D (401(k) contributions), that amount already reduced your Box 1 wages — you don’t deduct it again. But Code W (HSA) may need to be reported on Form 8889. Code DD (health coverage cost) is informational only and does not affect your tax calculation.

Boxes 15–20 → State and local returns. Use these boxes when filing your state income tax return. In states like New York, the state wages in Box 16 may differ from the federal wages in Box 1 because some deductions are treated differently at the state level.

8. What to Do If Your W-2 Is Wrong or Missing

If your W-2 contains an error: Contact your employer’s payroll or HR department first. Common errors include incorrect Social Security numbers, wrong wage amounts, or missing Box 12 codes. Your employer can issue a corrected Form W-2c.

If you haven’t received your W-2 by mid-February: First, verify your mailing address with your employer and check if an electronic version is available through your company’s payroll portal. If you still can’t get it, call the IRS at 1-800-829-1040 — they can contact your employer on your behalf.

If you need to file before your W-2 arrives: You can use Form 4852, Substitute for Form W-2, Wage and Tax Statement. Use your final pay stub to estimate the amounts. However, if the actual W-2 arrives later with different numbers, you may need to file an amended return (Form 1040-X).

EA Insight

The single most useful habit I recommend to every W-2 employee: compare your final December pay stub to your W-2 when it arrives. Box 1 should closely match your year-to-date taxable wages on that last stub. If there’s a significant discrepancy, flag it immediately — it’s much easier to fix before you file than after.

I also see many employees overlook Box 12, Code DD. While it doesn’t affect your tax calculation, it shows the total cost of your employer-sponsored health coverage. This number matters if you’re evaluating whether marketplace insurance or a spouse’s plan might be a better deal — it gives you the full picture of what your current coverage actually costs.

And for employees who receive tips or work overtime: starting with the 2026 W-2, check Box 12 for codes TP and TT. These are the amounts you’ll use to claim the new deductions on Schedule 1-A. If your employer didn’t report them, you can’t claim the deduction — so verify this before filing season.

People Also Ask

What’s the difference between a W-2 and a 1099?

A W-2 is issued to employees whose employers withhold taxes from their pay. A 1099 (such as 1099-NEC) is issued to independent contractors or freelancers who receive payment without tax withholding. The tax obligations and filing processes are different for each.

Can I file my taxes without a W-2?

Yes, but only as a last resort. You can use Form 4852 as a substitute, estimating your wages and withholding from your final pay stub. If the actual W-2 arrives later with different amounts, you’ll need to file an amended return.

Why is my Box 1 lower than my salary?

Box 1 shows taxable wages after pre-tax deductions are subtracted. If you contribute to a 401(k), HSA, health insurance premiums, or FSA through payroll, those amounts reduce your Box 1 figure. Your gross salary is not the same as your taxable wages.

How long should I keep my W-2?

The IRS generally recommends keeping tax records for at least three years from the date you filed or two years from the date you paid the tax, whichever is later. Many tax professionals recommend keeping W-2s for at least four years, and indefinitely for Social Security verification purposes.

What does the “Retirement Plan” checkbox in Box 13 mean?

If this box is checked, it means your employer offered you a qualified retirement plan (such as a 401(k), 403(b), or pension). This checkbox affects whether your traditional IRA contributions are tax-deductible — if you’re covered by an employer plan, the deductibility of your IRA contributions may be reduced or eliminated based on your income level.

Related Articles

Official Resources

Updated: April 2026

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual situations vary. Always verify current figures at IRS.gov and consult a qualified tax professional (EA, CPA, or attorney) for advice specific to your situation.