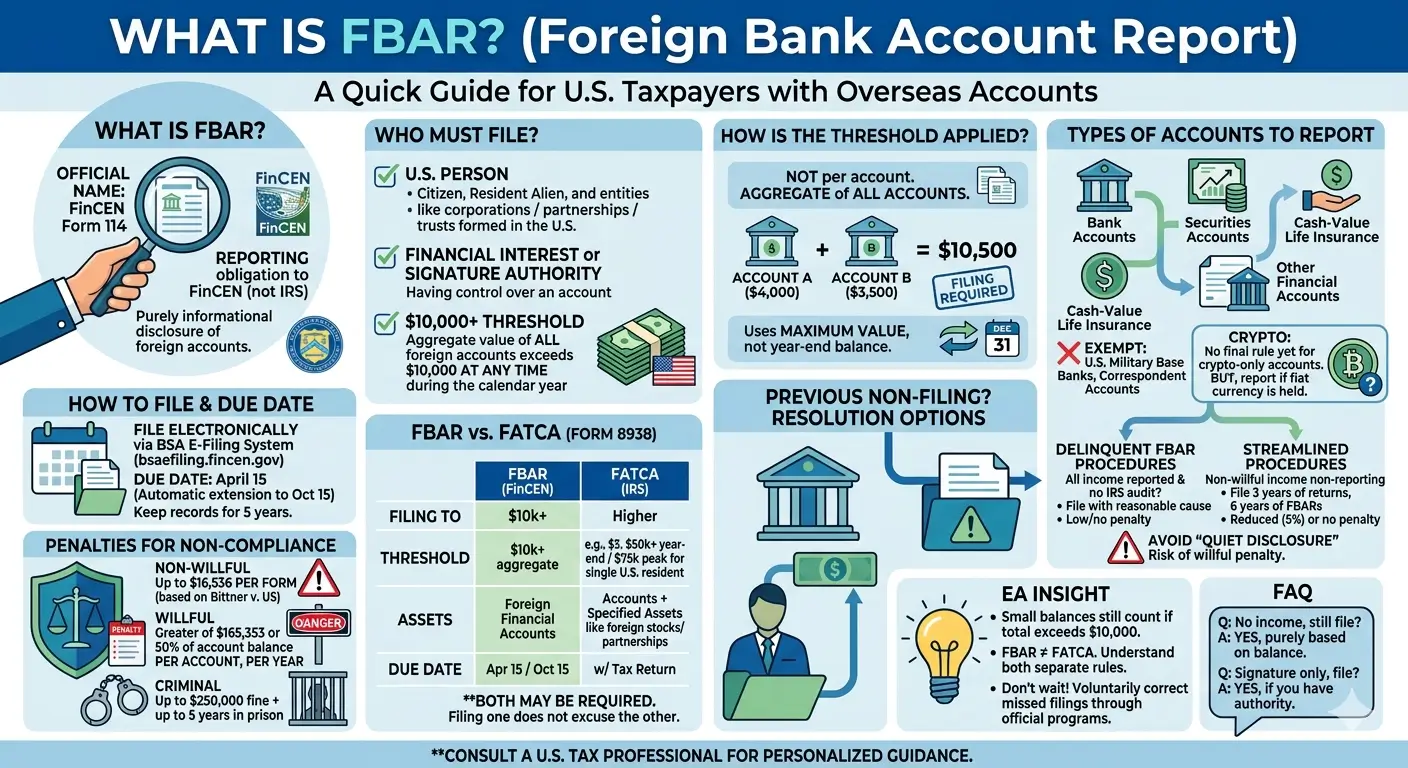

What Is FBAR?

FBAR (Foreign Bank Account Report) is an annual disclosure filed with the U.S. Treasury Department — not the IRS — by U.S. persons who hold foreign financial accounts. If the combined maximum value of all your foreign accounts exceeded $10,000 at any point during the year, you are required to file FinCEN Form 114. FBAR is not a tax form. It does not generate a tax bill. But failing to file it can trigger some of the most severe penalties in all of U.S. law.

Key Takeaways

- FBAR is filed as FinCEN Form 114 through the BSA E-Filing System — it is separate from your income tax return.

- You must file if the aggregate maximum value of all your foreign financial accounts exceeded $10,000 at any time during the calendar year — not per account, but combined.

- U.S. citizens, green card holders, resident aliens, and U.S.-formed entities (corporations, partnerships, LLCs, trusts, estates) are all subject to FBAR requirements.

- The filing deadline is April 15, with an automatic extension to October 15 — no request needed.

- Non-willful penalties can reach up to $16,536 per report. Willful penalties can reach $165,353 or 50% of the account balance, whichever is greater. Figures are subject to annual inflation adjustments.

- FBAR and IRS Form 8938 (FATCA) are separate filing obligations. Filing one does not satisfy the other.

Table of Contents

- 1. What Is FBAR?

- 2. Who Must File an FBAR?

- 3. How the $10,000 Threshold Works

- 4. Which Accounts Must Be Reported?

- 5. How to File and When It Is Due

- 6. FBAR Penalty Structure

- 7. FBAR vs. Form 8938 (FATCA)

- 8. Missed Past FBARs — How to Fix It

- 9. EA Insight

- 10. Frequently Asked Questions

- 11. Related Articles

- 12. Official Resources

1. What Is FBAR?

FBAR stands for Foreign Bank Account Report. Its official name is FinCEN Form 114, and it is filed with the Financial Crimes Enforcement Network (FinCEN), a bureau of the U.S. Department of the Treasury.

FBAR is not a tax form. It is a financial disclosure report, filed separately from your federal income tax return (Form 1040). The legal authority for FBAR comes from the Bank Secrecy Act (31 U.S.C. §5314), which was enacted to help the U.S. government detect and prevent tax evasion and money laundering through offshore accounts.

Filing an FBAR does not create a tax liability. The report is purely informational — it tells the Treasury Department that you hold financial accounts outside the United States. However, any income earned in those foreign accounts — such as interest, dividends, or capital gains — must be reported separately on your U.S. income tax return.

2. Who Must File an FBAR?

You are required to file an FBAR if you meet all three of the following conditions:

- You are a U.S. person — This includes U.S. citizens, green card holders (lawful permanent residents), and resident aliens. It also includes entities formed or organized in the United States, such as corporations, partnerships, LLCs, trusts, and estates.

- You have a financial interest in, or signature authority over, at least one foreign financial account.

- The aggregate maximum value of all your foreign financial accounts exceeded $10,000 at any time during the calendar year.

Signature authority matters: Even if the money in the account is not yours, you may still have an FBAR filing obligation. For example, an officer or employee who has signing authority over a company’s foreign bank account must report that account — even if they have no personal financial interest in it.

3. How the $10,000 Threshold Works

The $10,000 threshold is based on the aggregate maximum value of all your foreign financial accounts — not each account individually. And it is based on the highest balance reached at any point during the calendar year, not the year-end balance.

Example: You hold three accounts in South Korea — a checking account that peaked at $4,000, a savings account that peaked at $3,500, and a brokerage account that peaked at $3,000. No single account crossed $10,000. But the combined peak values total $10,500, which triggers the FBAR filing requirement.

Important: Whether or not the account generated any income is irrelevant. Even an account you rarely use — or one that held a balance above the threshold for a single day — can trigger the filing requirement.

Foreign currency balances must be converted to U.S. dollars using the Treasury Reporting Rates of Exchange for December 31 of the year being reported.

4. Which Accounts Must Be Reported?

The following types of accounts held at foreign financial institutions must be reported on an FBAR:

- Bank accounts — checking, savings, certificates of deposit

- Securities accounts — stocks, bonds, mutual funds

- Insurance policies with cash surrender value held at a foreign institution

- Other financial accounts maintained at a foreign financial institution

The following accounts are exempt from FBAR reporting:

- Accounts at financial institutions located on U.S. military bases

- Correspondent or nostro accounts (used for bank-to-bank transactions)

- Accounts at international financial institutions (e.g., the World Bank, IMF)

Cryptocurrency on Foreign Exchanges

FinCEN has proposed rules that would explicitly require FBAR reporting for cryptocurrency held in foreign exchange accounts, but those regulations have not been finalized. Under current guidance, if your foreign exchange account holds both fiat currency and cryptocurrency, the account is likely reportable once it crosses the $10,000 aggregate threshold. For accounts that hold cryptocurrency only, the requirement remains uncertain. The recommended approach is to report conservatively and consult a tax professional if you hold digital assets on foreign platforms.

5. How to File and When It Is Due

FBAR must be filed electronically through the FinCEN BSA E-Filing System at bsaefiling.fincen.gov. Paper filing is not accepted.

For each foreign account, you will need to report:

- Name and address of the foreign financial institution

- Account number

- Type of account (bank, securities, other)

- Maximum value during the year (converted to U.S. dollars)

| Filing Detail | What You Need to Know |

|---|---|

| Filing System | BSA E-Filing System (bsaefiling.fincen.gov) |

| Deadline | April 15 (for the prior calendar year) |

| Automatic Extension | October 15 — no request needed |

| Currency Conversion | Treasury year-end exchange rate (December 31) |

| Record Retention | Minimum 5 years |

Joint filing with a spouse: If all foreign accounts are jointly owned and neither spouse has separate foreign accounts, one spouse may file on behalf of both. Both spouses must sign FinCEN Form 114a (Record of Authorization) and keep it on file.

6. FBAR Penalty Structure

FBAR penalties are not tax penalties. They are civil penalties imposed under the Bank Secrecy Act (31 U.S.C. §5321) and are adjusted annually for inflation. The distinction between non-willful and willful violations is critical — it can mean the difference between a manageable fine and financial ruin.

| Violation Type | Maximum Penalty (2026) | Applied Per |

|---|---|---|

| Non-Willful | Up to $16,536 | Per annual report (form) |

| Willful | $165,353 or 50% of account balance, whichever is greater | Per account, per year |

| Criminal | Up to $250,000 fine + up to 5 years imprisonment | Up to $500,000 + 10 years if linked to other criminal activity |

Penalty figures are subject to annual inflation adjustments by FinCEN.

In Bittner v. United States (2023), the U.S. Supreme Court ruled that non-willful penalties are applied per annual report (per form), not per account. This significantly reduced the penalty exposure for non-willful violations involving multiple accounts.

However, willful penalties still apply per account, per year. For someone with multiple unreported accounts over several years, willful penalties can exceed the total balance of the accounts themselves.

Reasonable cause: If you can demonstrate reasonable cause for failing to file — and that the failure was not due to willful neglect — penalties may be reduced or waived entirely. However, simply being unaware of the FBAR requirement does not automatically qualify as reasonable cause.

7. FBAR vs. Form 8938 (FATCA)

Both FBAR and Form 8938 deal with foreign financial assets, but they are separate filing obligations with different rules, thresholds, and filing channels.

| Feature | FBAR (FinCEN Form 114) | Form 8938 (FATCA) |

|---|---|---|

| Filed With | FinCEN (U.S. Treasury) | IRS (attached to tax return) |

| Legal Authority | Bank Secrecy Act (31 U.S.C. §5314) | Internal Revenue Code §6038D |

| Threshold (Individual, U.S. Resident) | Aggregate $10,000 at any time | Year-end $50,000 or annual peak $75,000 |

| Threshold (Individual, Living Abroad) | Same ($10,000) | Year-end $200,000 or annual peak $300,000 |

| What It Covers | Foreign financial accounts only | Foreign financial accounts + foreign financial assets (stocks, partnership interests, etc.) |

| How to File | BSA E-Filing System (separate electronic filing) | Attached to your income tax return |

| Deadline | April 15 (auto extension to October 15) | Same as your income tax return deadline |

Filing one does not satisfy the other. If you meet both thresholds, you must file both FBAR and Form 8938. The two reports have different definitions of reportable accounts, different threshold amounts, and are filed through entirely different systems.

8. Missed Past FBARs — How to Fix It

If you failed to file FBARs in prior years, the most important step is to take corrective action before the IRS contacts you. The IRS offers formal programs designed to help taxpayers come into compliance with reduced — or zero — penalties.

Delinquent FBAR Submission Procedures

This option is available if you properly reported all foreign account income on your tax returns but simply missed the FBAR filing. You must not be under IRS examination or investigation. Submit the late FBAR(s) through the BSA E-Filing System with a statement explaining why they were not filed on time. In most cases, this results in no penalties.

Streamlined Filing Compliance Procedures

This program applies when foreign income was also unreported on your tax returns. It requires filing three years of amended or delinquent tax returns and six years of delinquent FBARs, along with a certification under penalties of perjury that the failure was non-willful.

- U.S. residents: Subject to a miscellaneous offshore penalty of 5% of the highest aggregate balance of unreported foreign accounts during the six-year period.

- Foreign residents: The 5% penalty is waived.

Warning about “quiet disclosures”: Filing past-due FBARs outside of an official IRS program — sometimes called a “quiet disclosure” — carries significant risk. The IRS may treat such filings as evidence of willful noncompliance, which dramatically increases penalty exposure. Always use a formal program when correcting past filing failures.

EA Insight

The three most common FBAR mistakes I encounter in practice all stem from the same root cause: not realizing how broadly the reporting requirement applies.

First, many taxpayers assume that because no single account exceeds $10,000, they have no filing obligation. FBAR uses an aggregate threshold. If you maintain several accounts in your home country — checking, savings, a small investment account — the combined peak balances often cross $10,000 without you realizing it. This is especially common among immigrants who keep accounts in their country of origin.

Second, I frequently see taxpayers confuse FBAR with Form 8938. They file one and assume it covers the other. It does not. The two reports go to different agencies, have different thresholds, and cover different types of assets. Missing either one can result in separate penalties.

Third, some taxpayers who missed several years of FBARs try to fix the problem by quietly filing the late forms without going through an official IRS program. This is risky. The IRS Delinquent FBAR Submission Procedures and Streamlined Procedures exist specifically for this situation and typically result in minimal or no penalties when the failure was non-willful. Filing outside these programs can be treated as a willful violation — and the penalty gap between non-willful and willful is enormous.

Frequently Asked Questions

Do I need to file an FBAR if my foreign account earned no income?

Yes. The FBAR filing requirement is based solely on account value, not on whether the account generated any income. If the aggregate maximum value of all your foreign accounts exceeded $10,000 at any point during the year, you must file — regardless of whether those accounts earned interest, dividends, or any other income.

I have signature authority on a family member’s foreign account but no financial interest. Do I still need to report it?

Yes. If you have signature authority or other authority over a foreign financial account — even if the money is not yours — that account must be included in your FBAR. This applies to accounts belonging to a parent, employer, or other entity where you can authorize transactions.

Does filing a late FBAR automatically trigger a penalty?

No. Penalties are assessed on a case-by-case basis. If you properly reported all foreign account income on your tax returns and the IRS has not contacted you, filing through the Delinquent FBAR Submission Procedures typically results in no penalties.

Is a Korean National Pension (NPS) account subject to FBAR reporting?

Korea’s National Pension, which functions similarly to U.S. Social Security, is generally not considered a reportable financial account under FBAR. However, Korean employer-sponsored retirement plans (DB or DC type) and individual retirement savings accounts are likely reportable. If you hold any type of pension or retirement account at a foreign financial institution, confirm with a qualified tax professional whether it meets FinCEN’s definition of a financial account.

Does filing an FBAR create additional tax liability?

No. FBAR is a disclosure report — it does not generate any tax on its own. However, income earned in foreign accounts (interest, dividends, capital gains, etc.) must be reported separately on your U.S. income tax return, and that income is subject to tax.

Is cryptocurrency held on a foreign exchange reportable on FBAR?

Final regulations have not been issued. Under current guidance, if a foreign exchange account holds both fiat currency and cryptocurrency, the entire account is likely reportable once it crosses the aggregate $10,000 threshold. For accounts holding only cryptocurrency, the requirement remains uncertain. The recommended approach is to report conservatively and consult a tax professional.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.