What Is MAGI? Modified Adjusted Gross Income Explained

MAGI sounds like a technical afterthought — but it’s the number the IRS actually uses to decide whether you can contribute to a Roth IRA, how much your ACA health insurance costs, and whether you qualify for a long list of credits and deductions. Understanding how MAGI is calculated (and how it differs from AGI) is foundational tax knowledge.

Key Takeaways

- MAGI starts with your AGI and adds back specific deductions — which ones get added back depends on the rule being applied.

- There is no single universal MAGI formula. The IRS defines MAGI differently for Roth IRAs, ACA subsidies, and other programs.

- For most taxpayers, MAGI equals AGI because the add-backs don’t apply to their situation.

- For 2026, Roth IRA contributions phase out between $153,000–$168,000 (single) and $242,000–$252,000 (MFJ) based on MAGI.

- In 2026, the ACA subsidy cliff returned: households with MAGI above 400% of FPL are no longer eligible for Premium Tax Credits.

Table of Contents

- 1. What Is MAGI?

- 2. How MAGI Differs from AGI

- 3. The MAGI Formula: AGI + Add-Backs

- 4. Why MAGI Has No Single Definition

- 5. MAGI and Roth IRA Eligibility (2026)

- 6. MAGI and the ACA Premium Tax Credit (2026)

- 7. Other Places MAGI Appears on Your Return

- 8. How to Find Your MAGI

- 9. EA Insight

- 10. People Also Ask

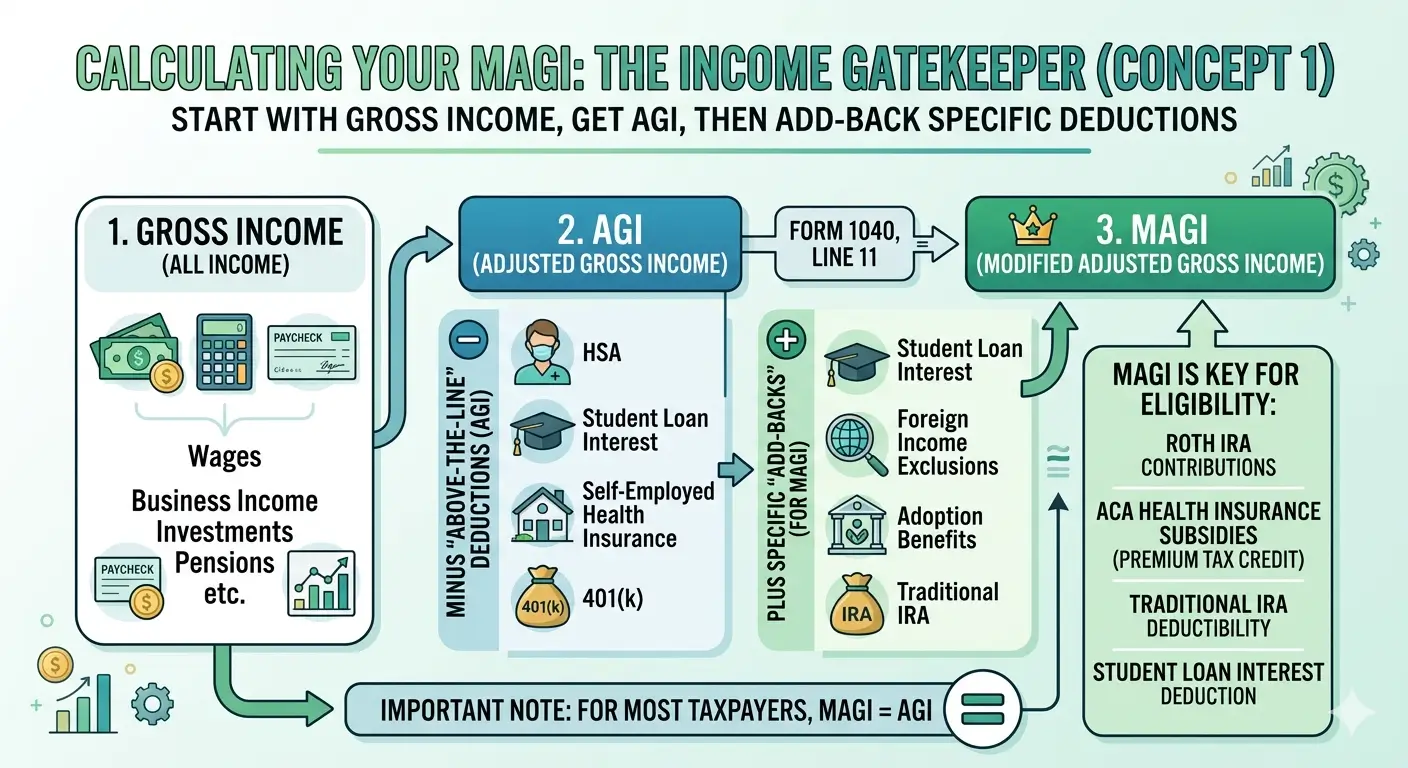

1. What Is MAGI?

Modified Adjusted Gross Income — MAGI — is a version of your income that the IRS uses as a gatekeeper. It determines whether you qualify for certain tax benefits, how much of a benefit you receive, and at what point that benefit phases out or disappears entirely.

The word “modified” is the key. MAGI takes your Adjusted Gross Income (AGI) — the number on line 11 of Form 1040 — and adds back certain deductions that were subtracted to arrive at AGI. The result is a slightly higher income figure that the IRS uses for specific eligibility calculations.

MAGI does not appear as a labeled line on your Form 1040. It is a calculated number you must derive yourself, or have your tax software calculate, based on the specific rule that applies to your situation.

2. How MAGI Differs from AGI

To understand MAGI, you first need a clear picture of where AGI comes from.

| Term | Definition | Where to Find It |

|---|---|---|

| Gross Income | All taxable income before any deductions — wages, interest, dividends, business income, rental income, etc. | Calculated across multiple lines of Form 1040 |

| AGI | Gross income minus “above-the-line” deductions (401(k) contributions, student loan interest, HSA contributions, self-employed health insurance, etc.) | Form 1040, Line 11 |

| MAGI | AGI plus certain deductions added back — the specific add-backs depend on which rule is being applied | Calculated separately; no dedicated line on Form 1040 |

For most people without foreign income, tax-exempt Social Security, or student loan interest deductions, MAGI = AGI. The distinction only matters when the add-backs actually apply.

3. The MAGI Formula: AGI + Add-Backs

The general structure of MAGI is straightforward:

MAGI = AGI + Specific Add-Backs

Which add-backs apply depends entirely on the specific tax rule or benefit being calculated.

The most commonly encountered add-backs include the following items — though which ones are added back varies by context:

| Deduction Taken in AGI | Added Back for MAGI? | Context |

|---|---|---|

| Student loan interest deduction | Yes — often | Roth IRA, Traditional IRA, passive income rules |

| IRA deduction (traditional) | Yes — often | Roth IRA eligibility calculation |

| Foreign earned income exclusion | Yes — often | IRA eligibility, passive loss rules |

| Tax-exempt Social Security benefits | Yes — for ACA | ACA Premium Tax Credit only |

| Tax-exempt interest income | Yes — for ACA | ACA Premium Tax Credit only |

| 401(k) / 403(b) pre-tax contributions | No | Not added back — they reduce both AGI and MAGI |

Practical note: Pre-tax 401(k) contributions, HSA contributions, and self-employed health insurance premiums do reduce your AGI — and since they are not among the items added back, they also reduce your MAGI. This is why these contributions can be powerful tools for managing MAGI when eligibility thresholds matter.

4. Why MAGI Has No Single Definition

One of the most confusing things about MAGI is that the IRS defines it differently depending on which provision of the tax code is being applied. The add-backs for Roth IRA eligibility are not identical to the add-backs for ACA Premium Tax Credit eligibility, which are not identical to the add-backs for the student loan interest deduction phase-out.

Here’s a simplified view of how the definition shifts across common contexts:

| Tax Provision | Key Add-Backs | IRS Reference |

|---|---|---|

| Roth IRA eligibility | Traditional IRA deduction, student loan interest, foreign earned income exclusion, employer adoption assistance | Publication 590-A, Worksheet 2-1 |

| ACA Premium Tax Credit | Tax-exempt Social Security, tax-exempt interest, foreign income exclusions | Publication 974, Form 8962 |

| Traditional IRA deductibility | Traditional IRA deduction itself, student loan interest, foreign income exclusions | Publication 590-A |

| Medicare IRMAA surcharges | Tax-exempt interest income | SSA.gov, Form SSA-44 |

Because MAGI calculations vary by provision, always confirm which definition applies to the specific credit, deduction, or eligibility rule you’re working with.

5. MAGI and Roth IRA Eligibility (2026)

Roth IRA eligibility is one of the most common places taxpayers encounter MAGI — and one of the most consequential. Your ability to contribute to a Roth IRA depends entirely on your MAGI and filing status.

2026 Roth IRA Contribution Limits

- Under age 50: Up to $7,500 per year

- Age 50 or older: Up to $8,600 per year (includes $1,100 catch-up contribution)

- Combined limit: Applies across all IRA accounts (Traditional + Roth combined)

Source: IRS Notice 2025-67 (tax year 2026 limits). Contribution limit increased from $7,000 (2025) to $7,500 (2026).

2026 Phase-Out Ranges

| Filing Status | Full Contribution | Phase-Out Range | No Contribution Allowed |

|---|---|---|---|

| Single / HoH | Below $153,000 | $153,000 – $168,000 | Above $168,000 |

| Married Filing Jointly | Below $242,000 | $242,000 – $252,000 | Above $252,000 |

| Married Filing Separately | $0 (no full contribution) | $0 – $10,000 | Above $10,000 |

Source: IRS Notice 2025-67. Phase-out ranges increased from 2025 levels by $3,000 (single) and $6,000 (MFJ).

How the Phase-Out Works

If your MAGI falls within the phase-out range, your maximum contribution is reduced proportionally using a worksheet in IRS Publication 590-A. The general formula:

Phase-Out Calculation Example — Single Filer, MAGI $160,000 (2026)

- Phase-out range: $153,000 – $168,000 (range width: $15,000)

- Amount over floor: $160,000 − $153,000 = $7,000

- Reduction ratio: $7,000 ÷ $15,000 = 46.7%

- Reduction: $7,500 × 46.7% = $3,503 (rounded to nearest $10 = $3,500)

- Allowable contribution: $7,500 − $3,500 = $4,000

Use IRS Publication 590-A Worksheet 2-1 for the official calculation. Minimum contribution is $200 if the calculated amount would otherwise fall below that threshold.

What if Your MAGI Is Too High?

Exceeding the Roth IRA MAGI ceiling doesn’t mean losing access to Roth benefits entirely. High earners can use the backdoor Roth IRA strategy: contribute to a non-deductible Traditional IRA (no income limit applies) and then convert it to a Roth IRA. Tax consequences depend on whether you have existing pre-tax IRA balances — the IRS pro-rata rule applies. Consult a tax professional before executing this strategy.

6. MAGI and the ACA Premium Tax Credit (2026)

If you purchase health insurance through the ACA Marketplace (Healthcare.gov or a state exchange), your ACA-specific MAGI determines whether you qualify for a Premium Tax Credit (PTC) — the subsidy that reduces your monthly health insurance premiums.

Important Change for 2026: The Subsidy Cliff Has Returned

From 2021 through 2025, enhanced subsidies allowed households with incomes above 400% of the Federal Poverty Level (FPL) to still qualify for a Premium Tax Credit. That provision expired at the end of 2025. Starting in 2026, the original ACA rules are back: households with MAGI above 400% of FPL do not qualify for any federal PTC. This is a significant change that affects millions of Marketplace enrollees.

2026 ACA MAGI Eligibility — 400% FPL Thresholds

| Household Size | 100% FPL | 400% FPL (PTC Cutoff) |

|---|---|---|

| 1 person | $15,650 | $62,600 |

| 2 people | $21,150 | $84,600 |

| 3 people | $26,650 | $106,600 |

| 4 people | $32,150 | $128,600 |

2026 PTC eligibility is based on 2025 HHS poverty guidelines (continental U.S.). Alaska and Hawaii use higher figures. Eligibility begins above 100% FPL (or above the Medicaid expansion threshold in states that have expanded Medicaid, typically 138% FPL).

ACA-Specific MAGI: What’s Different

For ACA purposes, MAGI is calculated differently than for IRA purposes. The ACA add-backs include items that are not added back in the IRA context:

- Tax-exempt Social Security benefits — added back even though they aren’t taxable income

- Tax-exempt interest — from municipal bonds and similar instruments

- Foreign income exclusions — amounts excluded under IRC Section 911

For many taxpayers — particularly those without tax-exempt Social Security or significant tax-free interest — ACA MAGI will equal AGI. The add-backs matter most for retirees receiving Social Security who also purchase Marketplace coverage.

Why MAGI Management Matters for ACA Enrollees

Because the subsidy cliff has returned in 2026, being even $1 over the 400% FPL threshold means losing the entire Premium Tax Credit. For a single person in most of the country, crossing $62,600 in MAGI can mean suddenly owing thousands of dollars for health insurance. This makes MAGI management — through pre-tax retirement contributions, HSA contributions, and careful income timing — particularly important for self-employed individuals, early retirees, and anyone else who relies on Marketplace coverage.

7. Other Places MAGI Appears on Your Return

Beyond Roth IRAs and ACA subsidies, MAGI (under its context-specific definition) determines eligibility for a range of other tax benefits:

| Tax Benefit | MAGI Threshold (2026, Single) | MAGI Threshold (2026, MFJ) |

|---|---|---|

| Traditional IRA deductibility (if covered by workplace plan) | Phase-out: $81,000–$91,000 | Phase-out: $129,000–$149,000 |

| Student loan interest deduction | Phase-out begins — check current year limits | Phase-out begins — check current year limits |

| Child Tax Credit (phase-out) | Reduces above $200,000 | Reduces above $400,000 |

| Medicare IRMAA surcharges | Surcharges apply above $106,000 | Surcharges apply above $212,000 |

| Net Investment Income Tax (NIIT) | 3.8% surtax above $200,000 | 3.8% surtax above $250,000 |

Thresholds reflect 2026 tax year. Always verify the specific MAGI definition that applies to each provision using the relevant IRS Publication.

8. How to Find Your MAGI

Since MAGI isn’t a labeled line on your tax return, you’ll need to calculate it yourself — or confirm your tax software has done so correctly. Here’s the general process:

Step-by-Step: Calculating Your MAGI

- Start with your AGI — Form 1040, Line 11

- Identify which MAGI you need — Roth IRA? ACA? Traditional IRA deductibility? Each has a different add-back list

- Locate the relevant worksheet — Publication 590-A for IRAs; Publication 974 / Form 8962 for ACA; IRS.gov for others

- Add back applicable deductions — Only those specified for that particular rule

- Compare your MAGI to the threshold — Full benefit, partial benefit, or no benefit?

If you use tax software such as TurboTax or H&R Block, MAGI calculations are typically handled automatically once you enter your income and deductions. However, for complex situations — dual incomes near phase-out thresholds, ACA Marketplace coverage, or Social Security combined with Marketplace plans — working through the calculation manually (or with a tax professional) is advisable to avoid errors.

EA Insight

The two places I see MAGI misunderstood most often are the Roth IRA phase-out and the ACA subsidy calculation — and the mistakes tend to go in opposite directions. With Roth IRAs, clients often assume they can’t contribute at all once their income climbs, and they give up without running the worksheet. Many of them are still in the phase-out range and could make a partial contribution — or use the backdoor strategy. Leaving that on the table year after year is a real cost.

With ACA subsidies, the problem in 2026 is the opposite: clients underestimate how much damage a single dollar over the 400% FPL threshold can do. The subsidy cliff is back — and it’s steeper than most people realize.

Why the 2026 Subsidy Cliff Is Especially Dangerous

① The premiums themselves are higher.

2026 Marketplace premiums are projected to rise roughly 18% year-over-year. The full unsubsidized amount a household must absorb if they fall off the cliff is meaningfully larger than it was in 2025. Losing the subsidy doesn’t just mean losing last year’s subsidy — it means absorbing a larger bill with no help at all.

② Early retirees are particularly exposed.

Taxpayers who retire before 65 and purchase Marketplace coverage often have controllable income — but “controllable” cuts both ways. A Roth conversion, a stock sale, or an IRA distribution taken without checking the MAGI impact can push a household over 400% FPL and trigger full repayment of advance credits already received. I’ve seen a single year-end distribution decision cost a client over $10,000.

③ Self-employed taxpayers face unpredictable exposure.

A good month in December — a large client payment, a contract close — can push net income above the line after all advance credits have been paid out. The repayment isn’t capped at the subsidy amount received; it’s the full credit. Income that triggers a $5,000 tax repayment on top of the income tax itself is a scenario I see more often than it should happen.

My standard practice with any client who has Marketplace coverage or is near a Roth phase-out: I calculate projected MAGI in November — not in April. By the time you’re filing, there’s nothing left to do. Tools like pre-tax retirement contributions, HSA contributions, and careful income timing exist precisely to address this. IRS Publication 590-A (for IRAs) and Publication 974 (for ACA) are both worth reading if you’re managing these numbers yourself. For a deeper look at the specific strategies for managing MAGI before year-end, see our Tax Savings guide on MAGI reduction strategies.

People Also Ask

Is MAGI the same as AGI?

For most taxpayers, yes — MAGI equals AGI because the items that would be added back (such as student loan interest, foreign income exclusions, or tax-exempt Social Security) don’t apply to their situation. The distinction matters when you have foreign income, are repaying student loans, or receive tax-exempt Social Security while also on a Marketplace health plan.

Where can I find my MAGI on my tax return?

MAGI is not a labeled line on Form 1040. It is a derived figure. Your AGI appears on Line 11 of Form 1040. From there, you calculate MAGI by adding back whichever items are specified for the tax rule you’re applying. For Roth IRA purposes, use Worksheet 2-1 in IRS Publication 590-A.

Does a 401(k) contribution reduce MAGI?

Yes — pre-tax (Traditional) 401(k) contributions reduce your gross income before AGI is calculated. Since 401(k) contributions are not among the items added back to calculate MAGI, they reduce both AGI and MAGI. A $10,000 Traditional 401(k) contribution generally lowers your MAGI by $10,000 — which can be strategically useful when approaching Roth IRA phase-out thresholds or ACA eligibility limits.

Does HSA contributions reduce MAGI?

Yes. Contributions to an HSA through payroll deductions reduce your W-2 wages before AGI is computed. Contributions made directly (outside of payroll) are deductible above the line on Schedule 1 and reduce AGI directly. Since HSA deductions are not added back in most MAGI calculations, they reduce MAGI as well. For 2026, the HSA contribution limit is $4,400 for self-only coverage and $8,750 for family coverage.

My MAGI is over the Roth IRA limit. Can I still contribute?

Not directly — once your MAGI exceeds the upper phase-out threshold ($168,000 single / $252,000 MFJ in 2026), direct Roth IRA contributions are prohibited. However, the backdoor Roth IRA strategy allows high earners to effectively access Roth treatment by contributing to a non-deductible Traditional IRA and then converting those funds to a Roth IRA. Tax consequences depend on your existing IRA balances due to the IRS pro-rata rule.

How does Social Security affect MAGI for ACA purposes?

For ACA Premium Tax Credit purposes, tax-exempt Social Security benefits are added back to AGI as part of the MAGI calculation. This means that even the non-taxable portion of your Social Security benefit counts toward the 400% FPL eligibility threshold. Retirees under 65 who receive Social Security and purchase Marketplace coverage need to account for this when projecting their ACA MAGI.

Related Articles

Official Resources

Updated: Tax Year 2026

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and thresholds change annually. MAGI definitions vary by tax provision — always verify using the relevant IRS Publication or consult a qualified tax professional (EA, CPA, or tax attorney) for advice specific to your situation.