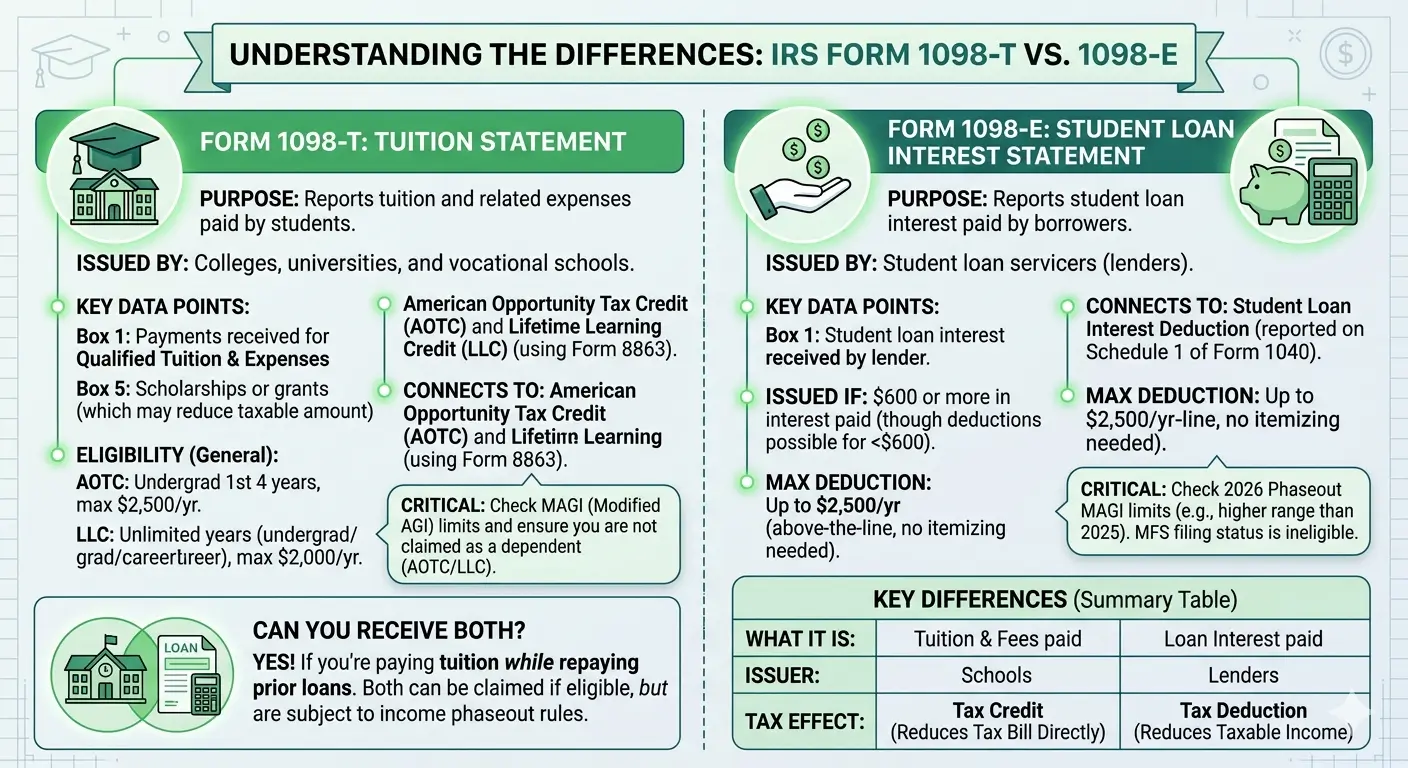

1098-T vs 1098-E: What’s the Difference?

Both forms are related to education — but they report very different things.

College tuition and student loan payments are both connected to IRS forms that can unlock valuable tax benefits. Form 1098-T reports tuition payments, while Form 1098-E reports student loan interest. This guide explains what each form is, who issues it, which tax benefits it connects to, and what mistakes to avoid.

Key Takeaways

- Form 1098-T is a tuition statement issued by your school.

- Form 1098-E is a student loan interest statement issued by your loan servicer.

- 1098-T connects to Education Credits (AOTC and LLC).

- 1098-E connects to the Student Loan Interest Deduction (up to $2,500).

- These two forms are not interchangeable — if you qualify, you may receive both.

- Both tax benefits have MAGI-based income limits that you should verify each year.

Table of Contents

What Is Form 1098-T?

Form 1098-T, officially called the Tuition Statement, is an IRS information form issued by eligible educational institutions — including colleges, universities, and accredited trade schools. It reports the amount of qualified tuition and related expenses a student paid during the calendar year.

Schools are required to provide this form to enrolled students by January 31 each year. Students use the information on the 1098-T to determine whether they qualify for education tax credits when filing their federal tax return.

Key Boxes on the 1098-T

| Box | What It Reports |

|---|---|

| Box 1 | Payments received for qualified tuition and related expenses |

| Box 4 | Adjustments made for a prior year |

| Box 5 | Scholarships or grants received |

| Box 7 | Checked if Box 1 includes amounts for an academic period beginning in January–March of the next year |

| Box 8 | Checked if the student was enrolled at least half-time |

| Box 9 | Checked if the student was a graduate student |

What’s not included: Room and board, transportation, health insurance, and other fees not directly related to course enrollment are not reported on the 1098-T.

⚠ Important: If the amount in Box 5 (scholarships) exceeds the amount in Box 1 (tuition paid), the difference may be considered taxable income. This commonly affects students who receive scholarships that cover more than just tuition and fees.

Note: The amounts shown on Form 1098-T may not exactly match what you can claim on your tax return. Always compare the form against your actual payment records.

What Is Form 1098-E?

Form 1098-E, officially called the Student Loan Interest Statement, is an IRS information form issued by your loan servicer — the company that collects your student loan payments. It reports the total amount of student loan interest you paid during the calendar year.

Loan servicers are required to send a 1098-E if you paid $600 or more in student loan interest during the year. The form must be provided by January 31.

Key Details About the 1098-E

| Box | What It Reports |

|---|---|

| Box 1 | Student loan interest received by the lender |

| Box 2 | Checked if the amount in Box 1 does not include loan origination fees or capitalized interest |

Both federal and private student loans qualify. If you have loans with multiple servicers, you may receive a separate 1098-E from each one.

For loans made on or after September 1, 2004, Box 1 includes loan origination fees and capitalized interest. For older loans, you may be able to deduct those amounts separately — see IRS Publication 970 for details.

Note: Even if you paid less than $600 in interest and did not receive a 1098-E, you may still be eligible for the deduction. Contact your loan servicer to confirm the exact amount of interest you paid.

Side-by-Side Comparison

| Category | Form 1098-T | Form 1098-E |

|---|---|---|

| Official Name | Tuition Statement | Student Loan Interest Statement |

| Issued By | School (Educational Institution) | Loan Servicer |

| Reports | Tuition payments + Scholarships | Student loan interest paid |

| Key Box | Box 1 (Payments), Box 5 (Scholarships) | Box 1 (Interest Paid) |

| Issued When | Student is enrolled | Interest paid ≥ $600 |

| Tax Benefit | Education Credits (AOTC, LLC) | Student Loan Interest Deduction |

| Benefit Type | Tax Credit (reduces tax owed) | Tax Deduction (reduces taxable income) |

| Filed Using | Form 8863 | Schedule 1 (Form 1040) |

| Deadline | January 31 | January 31 |

Which Tax Benefits Do They Unlock?

1098-T → Education Credits

The 1098-T is used to determine eligibility for two education tax credits:

American Opportunity Tax Credit (AOTC)

- Available for the first four years of post-secondary education

- Maximum credit: $2,500 per eligible student per year

- Up to 40% is refundable (up to $1,000 back even if you owe no tax)

- MAGI phaseout: $80,000–$90,000 (Single) / $160,000–$180,000 (MFJ)

- Claimed using Form 8863

Lifetime Learning Credit (LLC)

- No limit on the number of years you can claim it

- Covers undergraduate, graduate, and professional courses

- Maximum credit: $2,000 per tax return (not per student)

- Non-refundable

- MAGI phaseout: Same as AOTC ($80,000 / $160,000)

You cannot claim both the AOTC and LLC for the same student in the same year. However, you can claim different credits for different students on the same return.

1098-E → Student Loan Interest Deduction

- Deduct up to $2,500 in student loan interest per year

- Above-the-line deduction — no need to itemize

- MAGI phaseout applies (the IRS adjusts these limits annually for inflation — verify the current thresholds at IRS Topic No. 456)

- Reported on Schedule 1 (Form 1040)

- Married Filing Separately filers are not eligible

- You cannot be claimed as a dependent on someone else’s return

Can You Receive Both Forms?

Yes. If you are currently enrolled in school and also making payments on a previous student loan, you can receive both a 1098-T and a 1098-E in the same year.

For example, a graduate student attending classes (→ receives 1098-T) while repaying undergraduate student loans (→ receives 1098-E) could potentially claim both an education credit and the student loan interest deduction on the same return — as long as the eligibility requirements for each benefit are met separately.

Since each form connects to a different type of expense (tuition vs. loan interest), claiming both is not double-dipping. However, both benefits have MAGI-based income limits, so check your MAGI before filing.

Common Mistakes to Avoid

Mistake 1: Using the 1098-T amounts directly on your tax return without verification.

The amount in Box 1 may not match your actual eligible expenses. Subtract scholarships (Box 5), and compare against your own payment records before claiming a credit.

Mistake 2: Giving up on the deduction because you didn’t receive a 1098-E.

If you paid less than $600 in student loan interest, your servicer may not send a 1098-E. But you can still claim the deduction. Contact your loan servicer directly to get the exact interest amount.

Mistake 3: Confusing the two forms.

The 1098-T is about tuition. The 1098-E is about loan interest. They connect to different tax benefits and one does not replace the other.

Mistake 4: Filing Married Filing Separately and trying to claim the student loan interest deduction.

The Student Loan Interest Deduction is not available to taxpayers who file with the Married Filing Separately status.

Mistake 5: Claiming the deduction while being listed as a dependent.

If someone else — such as a parent — claims you as a dependent on their tax return, you cannot claim the Student Loan Interest Deduction on your own return, even if you are the one making the payments. This is one of the most commonly overlooked rules.

Mistake 6: Not checking the current income limits.

Both education credits and the student loan interest deduction have MAGI phaseout ranges that the IRS adjusts annually for inflation. Always verify the latest thresholds before filing.

💡 EA Insight

Many taxpayers check only one of these forms and move on. But if you’re attending school while repaying a previous student loan, each form connects to a different tax benefit — and both can be claimed in the same year.

In my experience, one of the most common missed opportunities involves the dependent question. A parent claims the student as a dependent and takes the education credit using the 1098-T — which is perfectly fine. But the student, still making loan payments, assumes they can also deduct the interest on their own return. They can’t. If you’re claimed as a dependent, the Student Loan Interest Deduction is off the table for you.

If you received both forms, take the time to review each one. A few minutes of checking can prevent missed deductions — or incorrect claims.

Frequently Asked Questions

Can I claim an education credit without receiving a 1098-T?

Generally, the IRS requires you to have received a 1098-T from an eligible institution to claim the AOTC. There are limited exceptions — see IRS Publication 970 for details.

If my parents pay my student loan interest, who gets the deduction?

The borrower — the person legally obligated to repay the loan — claims the deduction. The IRS treats the parent’s payment as a gift to the student, and the student is then considered to have paid the interest. However, the student must not be claimed as a dependent on anyone else’s return.

Can I claim both an education credit and the student loan interest deduction in the same year?

Yes. These two benefits apply to different expenses — tuition payments and loan interest — so claiming both is not double-dipping. Each has its own eligibility requirements and MAGI limits.

Do I need to attach the 1098-T or 1098-E to my tax return?

No. Neither form needs to be attached to your return. Keep them in your personal records for at least three years in case of an IRS audit.

What if the scholarship amount (Box 5) on my 1098-T is higher than the tuition amount (Box 1)?

The excess may be considered taxable income, especially if the scholarship was used for non-qualified expenses like room and board. Review IRS Publication 970 or consult a tax professional to determine how this applies to your situation.

Related Articles

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.