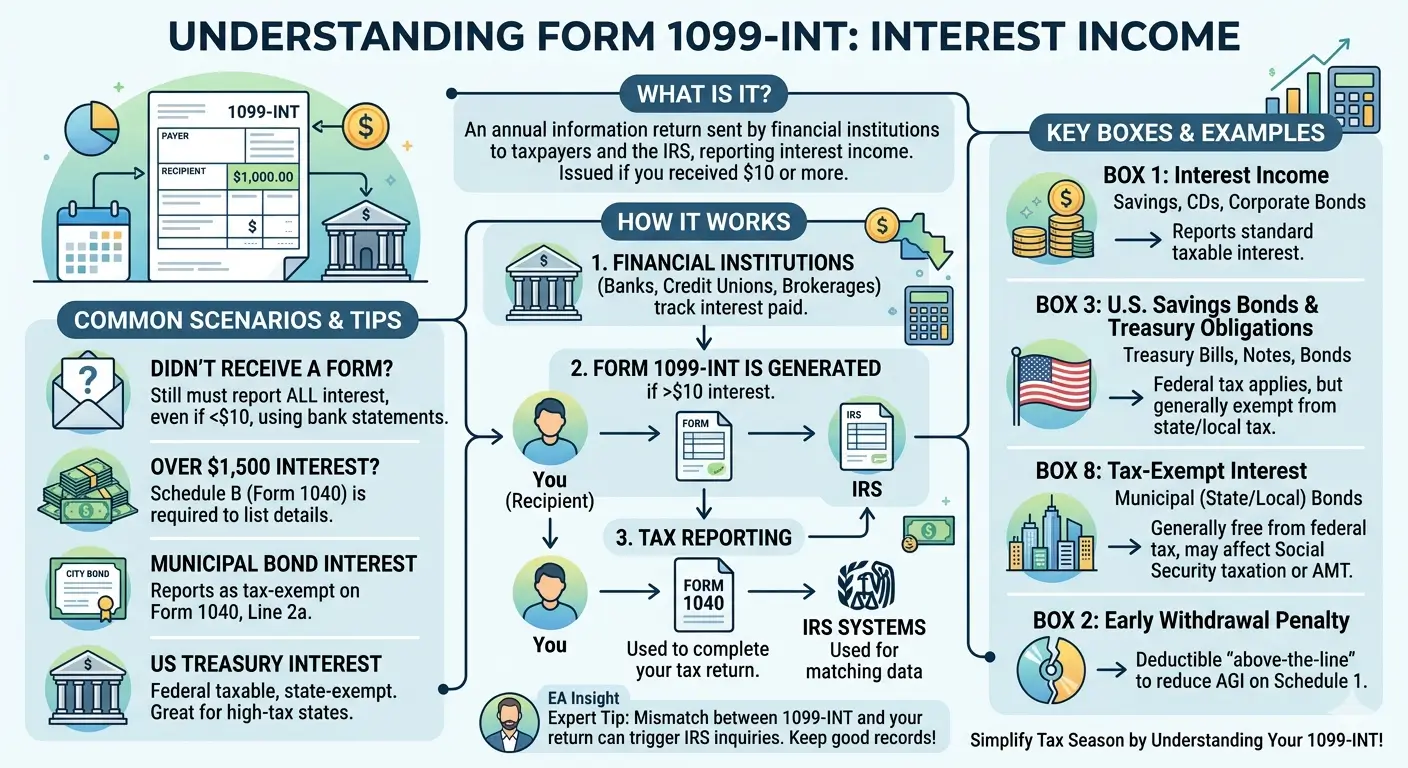

What Is a 1099-INT?

Form 1099-INT is the IRS information return used to report interest income paid by banks, credit unions, brokerage firms, and other financial institutions. If you earned interest from a savings account, certificate of deposit (CD), U.S. Treasury securities, or municipal bonds, this is the form that reports it — to both you and the IRS.

Key Takeaways

- Form 1099-INT is issued when a financial institution pays you $10 or more in interest during the tax year. The same data goes to the IRS.

- The three most important boxes are Box 1 (taxable interest), Box 3 (U.S. savings bonds and Treasury interest), and Box 8 (tax-exempt interest).

- Interest income is taxed as ordinary income — at the same rate as your wages or salary.

- If your total taxable interest exceeds $1,500, you must file Schedule B with your return.

- Even if you do not receive a 1099-INT — because your interest was under $10 — you are still required to report all interest income.

- The early withdrawal penalty in Box 2 can be deducted as an adjustment to income on Schedule 1, reducing your AGI.

Table of Contents

- 1. What Is Form 1099-INT?

- 2. Who Issues It and Who Receives It?

- 3. Key Boxes on Form 1099-INT

- 4. Where Does Interest Income Go on Your Tax Return?

- 5. What If You Did Not Receive a 1099-INT?

- 6. Forms That Are Easy to Confuse With 1099-INT

- 7. EA Insight

- 8. Frequently Asked Questions

- 9. Related Articles

- 10. Official Resources

1. What Is Form 1099-INT?

Form 1099-INT, Interest Income, is an IRS information return that reports interest paid to you by banks, credit unions, brokerage firms, insurance companies, and other financial institutions during the tax year.

The types of interest reported on this form include earnings from savings accounts, certificates of deposit (CDs), money market accounts, U.S. Treasury bills, notes and bonds, Series EE and Series I savings bonds, and municipal bonds.

A financial institution must issue Form 1099-INT if it paid you $10 or more in interest during the year. One copy goes to you and another goes directly to the IRS. The IRS uses this data to cross-reference your tax return and verify that all interest income is properly reported.

2. Who Issues It and Who Receives It?

Who Issues Form 1099-INT (Payers)

The following entities are required to issue Form 1099-INT when they pay $10 or more in interest to a recipient:

- Banks and credit unions — interest on savings accounts, CDs, and money market accounts

- Brokerage firms and investment companies — interest on bonds, fixed-income funds, and margin accounts

- Life insurance companies — interest paid on policy dividends or annuities

- Federal, state, and local government agencies — interest on delayed tax refunds

- Businesses that pay $600 or more in interest as part of their trade or business operations

Who Receives It (Recipients)

You may receive a 1099-INT if you earned interest from any of the sources listed above. This includes interest from savings accounts, bond investments, and even interest the IRS or a state tax agency paid on a delayed refund.

Deadline: Financial institutions must send Form 1099-INT to recipients by January 31 each year. The IRS filing deadline for electronic submissions is March 31.

Certain recipients are exempt from 1099-INT reporting. Payers are generally not required to issue the form to corporations, tax-exempt organizations, IRAs, HSAs, or U.S. government entities (IRS Instructions for Forms 1099-INT and 1099-OID).

3. Key Boxes on Form 1099-INT

Form 1099-INT contains multiple boxes, each reporting a specific type of interest or related amount. Here are the ones that matter most for individual taxpayers:

| Box | Label | What It Reports |

|---|---|---|

| 1 | Interest Income | Taxable interest from savings accounts, CDs, corporate bonds, etc. |

| 2 | Early Withdrawal Penalty | Penalty charged for breaking a CD or other time deposit before maturity |

| 3 | Interest on U.S. Savings Bonds and Treasury Obligations | Interest from Treasury bills, notes, bonds, and Series EE/I savings bonds |

| 4 | Federal Income Tax Withheld | Backup withholding (typically 24%) applied by the payer |

| 6 | Foreign Tax Paid | Tax withheld by a foreign country on interest income |

| 8 | Tax-Exempt Interest | Interest from municipal bonds — exempt from federal income tax |

| 9 | Specified Private Activity Bond Interest | Portion of Box 8 that may be subject to the Alternative Minimum Tax (AMT) |

| 10 | Market Discount | Accrued market discount on a covered security |

| 11 | Bond Premium | Premium amortization on a taxable covered security |

The Three Boxes That Matter Most

Box 1 — Interest Income. This is the most common box. It reports taxable interest from savings accounts, CDs, corporate bonds, and similar sources. This amount goes on Form 1040, Line 2b.

Box 3 — Interest on U.S. Savings Bonds and Treasury Obligations. This box reports interest from U.S. Treasury securities and savings bonds. This interest is subject to federal income tax but exempt from state and local income tax. It is reported separately from Box 1. If you live in a high-tax state like New York or California, this exemption provides a meaningful reduction in your state tax liability.

Box 8 — Tax-Exempt Interest. This box reports interest from municipal bonds issued by state and local governments. Municipal bond interest is generally exempt from federal income tax. However, you must still report it on Form 1040, Line 2a for informational purposes. Although it does not increase your federal tax liability, this amount can affect other calculations — including the taxable portion of Social Security benefits and your MAGI.

4. Where Does Interest Income Go on Your Tax Return?

Interest income is taxed as ordinary income — at the same federal tax rate as your wages or salary. There is no special or reduced rate for interest. If you are in the 22% bracket, you pay 22 cents in federal tax for every dollar of taxable interest you earn.

Basic Reporting Rules

If your total taxable interest is $1,500 or less, report it directly on Form 1040, Line 2b. If it exceeds $1,500, you must complete Schedule B (Interest and Ordinary Dividends), listing each payer and amount, before entering the total on Line 2b.

| Item | Where to Report |

|---|---|

| Box 1 — Taxable Interest | Form 1040, Line 2b (or Schedule B → Line 2b) |

| Box 3 — U.S. Treasury / Savings Bond Interest | Form 1040, Line 2b (federal taxable) + state return exclusion |

| Box 8 — Tax-Exempt Interest | Form 1040, Line 2a (informational only — not taxed) |

| Box 2 — Early Withdrawal Penalty | Schedule 1, Line 18 (adjustment to income — reduces AGI) |

| Box 4 — Federal Income Tax Withheld | Form 1040, Line 25b (credit against tax owed) |

State tax benefit: Box 3 interest (U.S. Treasury and savings bonds) is exempt from state and local income tax. When preparing your state return, exclude this amount from state taxable income. In high-tax states like New York, New Jersey, and California, this exemption can produce a noticeable reduction in your state tax bill.

5. What If You Did Not Receive a 1099-INT?

The $10 threshold determines whether a financial institution must issue Form 1099-INT. If your interest was less than $10, the institution may not send you a form.

However, not receiving a 1099-INT does not eliminate your reporting obligation. The IRS requires you to report all interest income regardless of the amount. The $10 figure is a payer reporting threshold — not a taxpayer filing exemption.

To report interest without a 1099-INT, check your bank statements or year-end account summaries, total all interest earned for the year, and enter the amount on the appropriate line of Form 1040 or Schedule B.

If you expected a 1099-INT but have not received it by mid-February, contact the issuing financial institution directly. If the form still does not arrive before the filing deadline, file your return using your own records. If the form arrives later and shows a different amount, you may need to file an amended return (Form 1040-X).

6. Forms That Are Easy to Confuse With 1099-INT

| Form | What It Reports | Key Difference From 1099-INT |

|---|---|---|

| 1099-INT | Interest income (savings, CDs, bonds) | Interest only |

| 1099-DIV | Dividend income (stocks, mutual funds) | Dividends, not interest. Exempt-interest dividends from muni bond funds go on 1099-DIV, not 1099-INT. |

| 1099-OID | Original Issue Discount | Reports imputed interest on discount bonds — different calculation method from stated interest. |

| 1099-B | Proceeds from broker transactions (stocks, bonds, securities) | Reports capital gains/losses from sales — not interest income. |

Most common mix-up: If you invest in a municipal bond mutual fund, the tax-exempt dividends you receive are reported on Form 1099-DIV — not Form 1099-INT. The fund itself holds the bonds and distributes the interest to shareholders as exempt-interest dividends, which changes the reporting form.

Similarly, if you receive staking rewards or interest-like income from a cryptocurrency exchange, that income is typically reported on Form 1099-MISC, not 1099-INT. Digital asset platforms are not classified as traditional financial institutions for interest reporting purposes.

EA Insight

The three most common mistakes I see with Form 1099-INT all come down to the same thing: confusing what the payer is required to report with what the taxpayer is required to file.

First, taxpayers who do not receive a 1099-INT assume they have nothing to report. If your interest was under $10, the bank may not issue the form — but the income is still taxable. When you have small amounts spread across multiple banks, it is easy to overlook them. Check every account statement before filing.

Second, taxpayers who hold U.S. Treasury securities often fail to exclude Box 3 interest from their state return. Treasury interest is exempt from state and local income tax, but this exclusion does not happen automatically — you must claim it. In states like New York and California, missing this exclusion means paying state tax you do not owe.

Third, taxpayers who receive Box 8 (tax-exempt interest) assume it does not need to appear on their return at all. While it is true that municipal bond interest is not federally taxed, it must be reported on Form 1040, Line 2a. This figure feeds into other calculations, including MAGI and the taxable portion of Social Security benefits. Leaving it off can trigger an IRS notice.

Frequently Asked Questions

Do I have to report interest income if I did not receive a 1099-INT?

Yes. The $10 threshold only determines whether the payer must issue the form. You are required to report all interest income on your federal return, even amounts under $10. Use your bank statements or year-end summaries to calculate the total.

Is U.S. Treasury interest exempt from state taxes?

Yes. Interest reported in Box 3 — from Treasury bills, notes, bonds, and Series EE/I savings bonds — is subject to federal income tax but exempt from state and local income tax. You must claim this exclusion on your state return to receive the benefit.

Do I need to report tax-exempt municipal bond interest?

Yes. Although municipal bond interest (Box 8) is not subject to federal income tax, you must report it on Form 1040, Line 2a for informational purposes. This amount may affect other tax calculations, including whether a portion of your Social Security benefits becomes taxable and whether you are subject to the Alternative Minimum Tax.

When do I need to file Schedule B?

You must file Schedule B if your total taxable interest (or ordinary dividends) exceeds $1,500 during the tax year. You also need Schedule B if you had a financial interest in a foreign financial account, or if you received interest as a nominee for another person.

Can I deduct the early withdrawal penalty from a CD?

Yes. The penalty shown in Box 2 can be deducted as an adjustment to income on Schedule 1, Line 18. This reduces your Adjusted Gross Income (AGI) and is available whether or not you itemize deductions.

What if my 1099-INT has an amount in Box 4 (Federal Income Tax Withheld)?

Box 4 reports backup withholding, which is typically applied at 24% when a recipient provides an incorrect taxpayer identification number (TIN) or does not provide one at all. This amount is treated as tax you have already paid. Report it on Form 1040, Line 25b, where it will be credited against your total tax liability — reducing the amount you owe or increasing your refund.

What should I do if the amounts on my 1099-INT do not match my records?

Contact the issuing financial institution directly to request a corrected form. The IRS cannot correct your 1099-INT. Do not delay filing your return while waiting for the correction — file on time using your own accurate records, and amend later with Form 1040-X if needed.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.