What Is FICA?

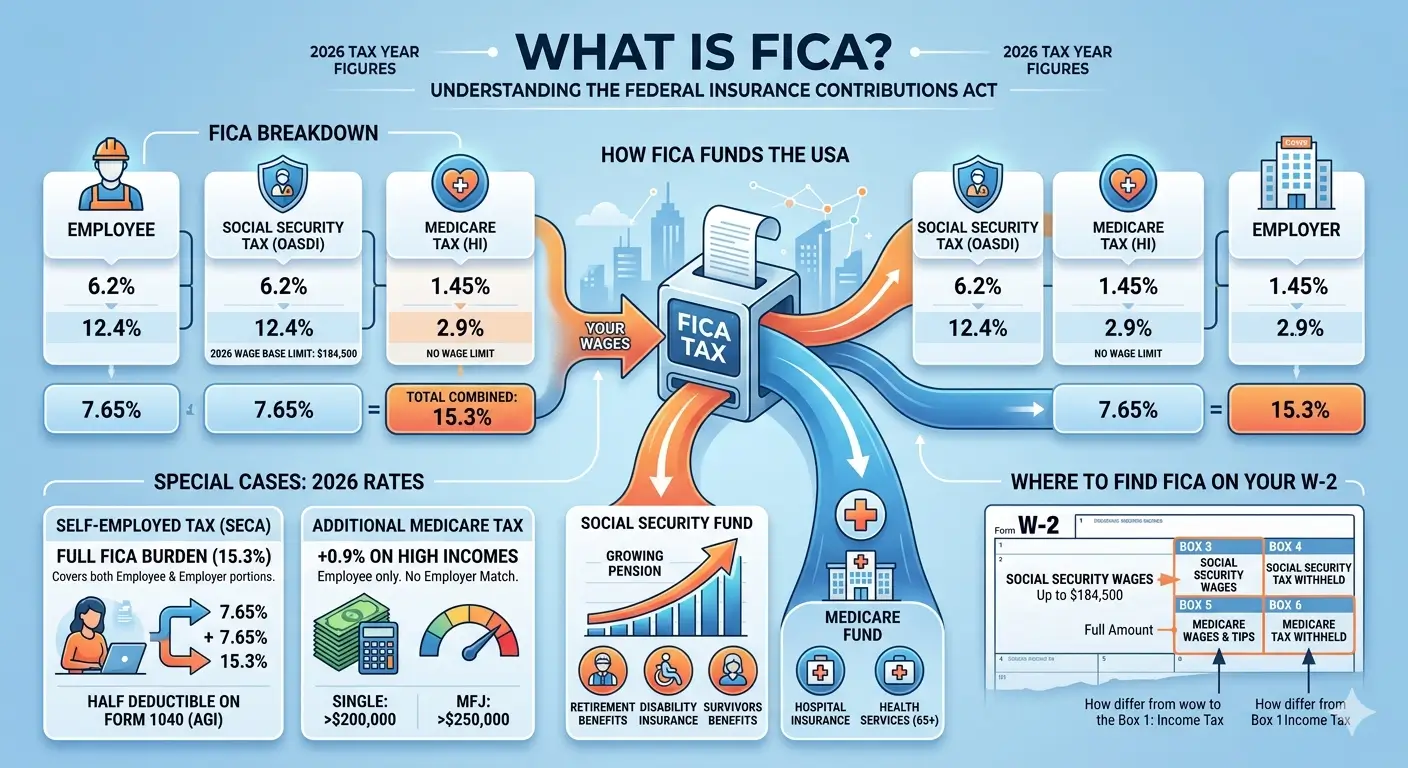

FICA stands for the Federal Insurance Contributions Act — the federal law that requires Social Security and Medicare taxes to be withheld from every worker’s paycheck. Whether you receive a W-2 as an employee or a 1099 as a freelancer, if you earn income from work, you almost certainly pay FICA.

Key Takeaways

- FICA consists of Social Security tax (6.2%) and Medicare tax (1.45%). For employees, the combined rate is 7.65%, withheld from each paycheck.

- Employers match the same 7.65%, making the total FICA tax rate 15.3% on every dollar of covered wages.

- Social Security tax has a wage base limit — earnings above the current threshold of $184,500 are not subject to Social Security tax.

- Medicare tax has no wage base limit. The 1.45% rate applies to all earned income, regardless of amount.

- An Additional Medicare Tax of 0.9% applies to earnings above $200,000 (Single). There is no employer match for this portion.

- Self-employed individuals pay the full 15.3% as self-employment tax, but may deduct the employer-equivalent half when calculating adjusted gross income.

Table of Contents

- 1. What Is FICA?

- 2. The Two Components of FICA

- 3. FICA Tax Rates — Employee vs. Employer vs. Self-Employed

- 4. Social Security Wage Base Limit

- 5. Additional Medicare Tax

- 6. How FICA Appears on Your W-2

- 7. Income Not Subject to FICA

- 8. EA Insight

- 9. Frequently Asked Questions

- 10. Related Articles

- 11. Official Resources

1. What Is FICA?

FICA is a federal law enacted in 1935 that funds two of the nation’s largest social programs — Social Security and Medicare — through taxes on earned income. The name stands for Federal Insurance Contributions Act, and it is the line item labeled “FICA” on your pay stub.

If you are an employee, FICA taxes are automatically withheld from your paycheck, and your employer pays an equal amount on your behalf. If you are self-employed, you pay both the employee and employer shares yourself — this is called self-employment tax.

The revenue collected through FICA is split between two federal trust funds:

- Social Security (OASDI) — Old-Age, Survivors, and Disability Insurance, which provides retirement benefits, disability benefits, and survivor benefits.

- Medicare (HI) — Hospital Insurance, which covers hospital care for individuals aged 65 and older or those who meet certain disability requirements.

One important distinction: FICA is separate from federal income tax. On your W-2, Social Security tax withheld appears in Box 4 and Medicare tax withheld appears in Box 6 — both distinct from the federal income tax withheld shown in Box 2.

2. The Two Components of FICA

Social Security Tax (OASDI)

Social Security tax funds retirement, disability, and survivor benefits. Its official name is Old-Age, Survivors, and Disability Insurance (OASDI). Employees and employers each pay 6.2% of covered wages.

This tax has a wage base limit — an annual ceiling set by the Social Security Administration. Once your earnings reach that ceiling, no further Social Security tax is withheld for the rest of the year.

Medicare Tax (HI)

Medicare tax funds hospital insurance for individuals aged 65 and older, as well as those with qualifying disabilities. Employees and employers each pay 1.45% of covered wages.

Unlike Social Security tax, Medicare tax has no wage base limit. It applies to every dollar of earned income, no matter how high. High earners also face an additional 0.9% Medicare surtax, which is explained in Section 5.

3. FICA Tax Rates — Employee vs. Employer vs. Self-Employed

| Category | Social Security | Medicare | Total |

|---|---|---|---|

| Employee | 6.2% | 1.45% | 7.65% |

| Employer | 6.2% | 1.45% | 7.65% |

| Combined | 12.4% | 2.9% | 15.3% |

| Self-Employed | 12.4% | 2.9% | 15.3% |

Employees see 7.65% withheld from each paycheck, while their employer separately pays another 7.65%. From the employee’s perspective, only half leaves their paycheck — but in total, 15.3% of every covered dollar goes toward FICA.

Self-employed individuals have no employer to split the cost with, so they pay the full 15.3% as self-employment tax. However, they may deduct the employer-equivalent half (7.65%) from their adjusted gross income (AGI) when filing their tax return. This deduction is available regardless of whether the taxpayer itemizes.

Note for self-employed taxpayers: Self-employment tax is not calculated on 100% of net earnings. The IRS applies the 15.3% rate to 92.35% of net self-employment income. This adjustment mirrors the fact that employees pay FICA on wages that have not been reduced by the employer’s share of FICA — leveling the playing field between employees and self-employed individuals.

Example — Employee Earning $80,000

| Tax | Employee Share | Employer Share | Total |

|---|---|---|---|

| Social Security (6.2%) | $4,960 | $4,960 | $9,920 |

| Medicare (1.45%) | $1,160 | $1,160 | $2,320 |

| FICA Total | $6,120 | $6,120 | $12,240 |

4. Social Security Wage Base Limit

Social Security tax does not apply to unlimited earnings. Each year, the Social Security Administration (SSA) sets a wage base limit — the maximum amount of earnings subject to the 6.2% tax. Once your earnings reach that ceiling for the year, no additional Social Security tax is withheld.

The current wage base limit is $184,500.

This threshold is adjusted annually based on the National Average Wage Index.

Maximum Social Security Tax

| Category | Calculation | Maximum Tax |

|---|---|---|

| Employee | $184,500 × 6.2% | $11,439 |

| Employer | $184,500 × 6.2% | $11,439 |

| Self-Employed | $184,500 × 12.4% | $22,878 |

Once your wages exceed $184,500 for the year, Social Security withholding stops for the remainder of the year. Higher-earning employees may notice a slight increase in take-home pay after crossing this threshold mid-year.

Working two or more jobs? Each employer withholds Social Security tax independently, based only on the wages it pays. If your combined earnings exceed $184,500, you may have more Social Security tax withheld than required. You can claim the excess as a credit on your Form 1040 when you file your tax return.

5. Additional Medicare Tax

In addition to the standard 1.45% Medicare tax, an Additional Medicare Tax of 0.9% applies to earned income above certain thresholds. This surtax was introduced under the Affordable Care Act and is reported on Form 8959.

| Filing Status | Threshold |

|---|---|

| Single / Head of Household | $200,000 |

| Married Filing Jointly | $250,000 |

| Married Filing Separately | $125,000 |

Key characteristics of the Additional Medicare Tax:

- No employer match — the 0.9% is paid entirely by the employee or self-employed individual.

- Employer withholding rule — employers must begin withholding the additional 0.9% once wages exceed $200,000 in a calendar year, regardless of the employee’s filing status. Any over- or under-withholding is reconciled on Form 8959 when the employee files their tax return.

Example — Single Filer, $250,000 in Wages

| Component | Amount |

|---|---|

| Regular Medicare (1.45% × $250,000) | $3,625 |

| Additional Medicare (0.9% × $50,000) | $450 |

| Employee’s Total Medicare Tax | $4,075 |

The employer pays only the standard 1.45% on the full $250,000 ($3,625). The additional 0.9% surtax is not matched.

6. How FICA Appears on Your W-2

At year-end, your employer reports FICA information on your W-2 in the following boxes:

| W-2 Box | What It Shows |

|---|---|

| Box 3 | Social Security wages — the amount of earnings subject to Social Security tax |

| Box 4 | Social Security tax withheld |

| Box 5 | Medicare wages and tips — the amount of earnings subject to Medicare tax |

| Box 6 | Medicare tax withheld |

Box 3 cannot exceed the wage base limit ($184,500). Box 5, on the other hand, has no ceiling — it reflects your total Medicare-taxable earnings.

When you receive your W-2, verify that Box 4 equals 6.2% of Box 3 and that Box 6 equals 1.45% of Box 5. If the numbers do not match, contact your employer and request a corrected W-2 (Form W-2c).

If you contribute to a 401(k) or other pre-tax retirement plan, you may notice that Box 1 (Wages, tips, other compensation) is lower than Box 3 or Box 5. This is because most pre-tax retirement contributions reduce income tax but do not reduce FICA. Your full wages before the 401(k) deduction are still subject to Social Security and Medicare taxes.

7. Income Not Subject to FICA

FICA applies to earned income — wages, salaries, tips, and self-employment earnings. The following types of income are not subject to FICA:

- Investment income — interest, dividends, and capital gains

- Rental income — real estate rental proceeds

- Retirement benefits — Social Security benefits and pension distributions

- Section 125 (Cafeteria Plan) benefits — employer-sponsored health insurance premiums, FSA contributions, and other qualifying benefits paid through a Section 125 plan are excluded from both income tax and FICA

- Certain employment exceptions — some religious order members, election workers below specified thresholds, and state or local government employees covered by qualifying separate pension systems

- Nonresident alien students and scholars — F-1 and J-1 visa holders may qualify for the Student FICA Exemption during their initial years in the U.S., provided they maintain valid student status

One common point of confusion: self-employment income is not exempt from FICA. Independent contractors and freelancers who receive a 1099-NEC pay the equivalent of FICA through self-employment tax at the same combined 15.3% rate.

EA Insight

The most common question I hear about FICA is “Can I reduce it?” The honest answer is: in almost all cases, no. FICA is not structured like income tax — there are no deductions or credits that lower your FICA obligation. If you have earned income, the tax is applied at fixed rates automatically.

There is one notable exception. Amounts paid through a Section 125 Cafeteria Plan — such as employer-sponsored health insurance premiums or FSA contributions — are excluded from FICA wages. Beyond that, the rate is essentially fixed.

That is why, in practice, it matters more to understand how FICA interacts with other parts of your tax picture than to try to minimize it. For example, the self-employment tax deduction reduces your AGI, which in turn affects MAGI-based credits, deductions, and phase-outs. If you work two jobs, your employers withhold Social Security tax independently — and if your combined wages exceed the wage base, you could be leaving money on the table by not claiming the excess withholding credit on your return.

Every time you receive a W-2, check Box 3, 4, 5, and 6. If the math does not add up, it may be a payroll processing error on your employer’s end. No one will catch it for you.

Frequently Asked Questions

Is FICA the same as income tax?

No. FICA funds Social Security and Medicare, while income tax funds general federal government operations. Both are withheld from your paycheck, but they have different rates, calculations, and purposes. On your W-2, Box 2 is income tax; Boxes 4 and 6 are FICA.

Do self-employed individuals pay FICA?

Yes. Self-employed individuals pay the full 15.3% as self-employment tax, covering both the employee and employer shares. They may deduct the employer-equivalent half when calculating AGI on their tax return.

Does the Social Security wage base limit change every year?

Yes. The SSA adjusts the wage base annually based on the National Average Wage Index. The current limit is $184,500. The new figure is typically announced in October for the following year.

Does the employer match the Additional Medicare Tax?

No. The 0.9% Additional Medicare Tax is paid entirely by the employee or self-employed individual. There is no employer match for this portion.

What happens if I overpay Social Security tax from two jobs?

Each employer withholds independently, so excess Social Security tax may be collected if your combined wages exceed the wage base limit. You can claim the overpayment as a credit on your Form 1040 when filing your tax return.

Are 401(k) contributions subject to FICA?

Yes. Pre-tax 401(k) contributions reduce your income tax (Box 1 on your W-2 decreases), but they do not reduce FICA. Your full wages before the 401(k) deduction remain subject to Social Security and Medicare taxes (Box 3 and Box 5 are unchanged).

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.