What Is a 529 Plan?

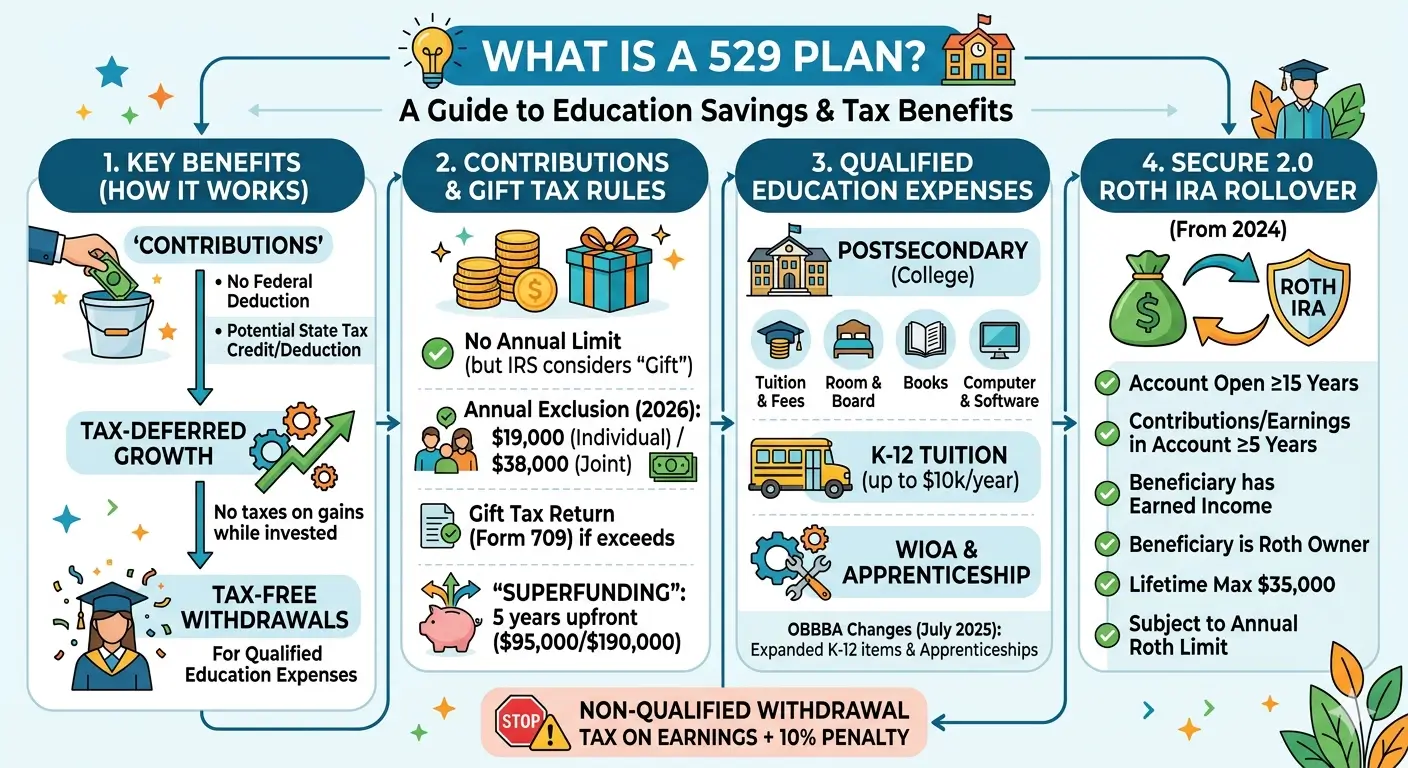

A 529 plan is one of the most powerful tax-advantaged savings tools available for education in the United States. Contributions grow tax-deferred, and withdrawals for qualified education expenses are federally tax-free. With recent legislation expanding its reach to K-12 costs, credential programs, and even Roth IRA rollovers for unused funds, the 529 plan has become far more versatile than a traditional college savings account.

Key Takeaways

- A 529 plan is a tax-advantaged education savings account established under IRC §529. Each state sponsors its own plan, but you are not required to use your home state’s plan.

- There is no federal income tax deduction for contributions, but approximately 40 states offer a state income tax deduction or credit.

- Earnings grow tax-deferred, and withdrawals used for qualified education expenses are free from federal income tax and penalties.

- The IRS does not set an annual contribution limit. However, contributions exceeding $19,000 per person ($38,000 for married couples) require filing a gift tax return (Form 709).

- The One Big Beautiful Bill Act (OBBBA), effective July 2025, expanded the list of qualified K-12 expenses and raised the annual K-12 withdrawal cap from $10,000 to $20,000 per beneficiary.

- Under SECURE 2.0, unused 529 funds can be rolled over tax-free into the beneficiary’s Roth IRA — up to a $35,000 lifetime limit.

- Non-qualified withdrawals trigger income tax plus a 10% federal penalty on the earnings portion.

Table of Contents

- 1. What Is a 529 Plan?

- 2. How the Tax Benefits Work

- 3. Contribution Limits and Gift Tax Rules

- 4. What Are Qualified Education Expenses?

- 5. What Changed Under the OBBBA

- 6. 529-to-Roth IRA Rollover (SECURE 2.0)

- 7. Non-Qualified Withdrawals: Taxes and Penalties

- 8. 529 Plan vs. Coverdell ESA vs. UTMA/UGMA

- 9. EA Insight

- 10. Frequently Asked Questions

- 11. Related Articles

- 12. Official Resources

1. What Is a 529 Plan?

A 529 plan is a tax-advantaged savings account created under Internal Revenue Code §529, designed specifically to help families save for education costs. Each state sponsors its own 529 plan, but anyone — parents, grandparents, relatives, or friends — can open an account and contribute. There are no income restrictions for contributors or beneficiaries, and there is no limit on how many plans you can set up.

There are two types of 529 plans:

Education Savings Plan — the most common type. Contributions are invested in mutual funds, ETFs, or similar investment options, and the account value grows or declines based on market performance. This is what most people mean when they refer to a “529 plan.”

Prepaid Tuition Plan — allows families to prepay future tuition at today’s rates. Only a handful of states offer these, and they typically apply only to in-state public universities. Coverage for room and board is generally excluded.

This guide focuses on the Education Savings Plan, which is what the vast majority of families use.

Good to know: You are not required to use the 529 plan sponsored by your home state. You can enroll in any state’s plan. However, if your state offers a state income tax deduction or credit for contributions to its own plan, using an out-of-state plan may mean giving up that benefit.

2. How the Tax Benefits Work

The tax advantages of a 529 plan operate in three stages:

Stage 1 — Contributions: There is no federal income tax deduction for 529 contributions. However, approximately 40 states offer a state income tax deduction or credit for contributions to their plan. The deductible amount varies widely by state — from as low as $500 per year in Rhode Island to unlimited in states like New Mexico, South Carolina, and West Virginia.

Stage 2 — Growth: Investment earnings inside the account grow tax-deferred. You do not pay federal income tax on interest, dividends, or capital gains each year while the money remains in the plan.

Stage 3 — Withdrawals: When you withdraw funds for qualified education expenses, the earnings portion is free from federal income tax. If you withdraw for non-qualified purposes, the earnings are subject to income tax plus a 10% federal penalty.

In short

You contribute with after-tax dollars, the money grows tax-deferred, and qualified withdrawals come out tax-free. The longer the money stays invested, the greater the tax-free growth.

3. Contribution Limits and Gift Tax Rules

The IRS does not set an annual contribution limit for 529 plans. You can contribute as much as you want in any given year. However, there are three types of limits to be aware of:

Annual Gift Tax Exclusion

The IRS treats 529 contributions as gifts. For the current tax year, contributions up to $19,000 per person per beneficiary ($38,000 for married couples filing jointly) fall within the annual gift tax exclusion — no gift tax return is required. Contributions above this amount must be reported on Form 709 and count against the contributor’s lifetime gift and estate tax exemption, which is $15 million per individual in the current tax year. Most families will never reach this lifetime threshold.

Superfunding (5-Year Gift-Tax Averaging)

529 plans offer a unique feature called superfunding, which allows you to front-load up to five years of annual exclusion gifts at once. This means a single individual can contribute up to $95,000 per beneficiary, and a married couple can contribute up to $190,000 per beneficiary, in a single year — without triggering gift tax. The contribution is spread across five years for gift tax reporting purposes on Form 709. If no additional gifts are made to that beneficiary during the five-year period, no portion counts against the lifetime exemption.

Important: If the contributor passes away before the five-year period is complete, a prorated portion of the contribution is added back into their taxable estate.

State Aggregate Lifetime Limits

Each state sets its own maximum total balance per beneficiary. These range from $235,000 in Georgia to more than $621,000 in New Hampshire. Once the account balance reaches this limit, no additional contributions are accepted — but existing investments continue to grow.

4. What Are Qualified Education Expenses?

To withdraw 529 funds tax-free, the money must be used for expenses the IRS recognizes as qualified education expenses.

Postsecondary (College and Beyond)

- Tuition and fees at eligible colleges, universities, vocational schools, and other postsecondary institutions

- Books, supplies, and equipment required for enrollment

- Computers, software, and internet access used by the student

- Room and board — for students enrolled at least half-time. The qualifying amount is limited to the school’s published Cost of Attendance (COA) figure for room and board. Expenses exceeding the COA amount are not considered qualified, even if the student actually paid more.

- Student loan repayment — up to a $10,000 lifetime limit per beneficiary

K-12 Education (Before the OBBBA)

Prior to the OBBBA, 529 funds could only be used for K-12 tuition at public, private, or religious elementary and secondary schools — up to $10,000 per beneficiary per year. No other K-12 expenses qualified.

5. What Changed Under the OBBBA

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, significantly expanded how families can use 529 plan funds.

Change 1 — Higher K-12 Withdrawal Cap

The annual withdrawal limit for K-12 education expenses increased from $10,000 to $20,000 per beneficiary, effective for tax years beginning after December 31, 2025.

Change 2 — Expanded K-12 Qualified Expenses

Beginning July 5, 2025, the list of qualified K-12 expenses now extends well beyond tuition to include:

- Curriculum materials, textbooks, and online educational materials

- Standardized test fees (SAT, ACT, and similar exams)

- Tutoring costs — the tutor must be unrelated to the student and meet specific qualifications (e.g., state-licensed teacher, subject matter expert, or instructor at an eligible institution)

- Educational therapies for students with disabilities — including occupational, behavioral, physical, and speech-language therapies from a licensed or accredited provider

- Dual-enrollment tuition for college-level courses taken during high school

Change 3 — Postsecondary Credential Programs

529 funds can now cover expenses for recognized credential and certification programs, including tuition, exam fees, books, and continuing education costs. To qualify, the credential program must be authorized by the Workforce Innovation and Opportunity Act (WIOA), approved by a federal or state government, or recognized as a military credential.

Change 4 — Permanent 529-to-ABLE Rollovers

Tax-free rollovers from 529 plans to ABLE accounts (tax-advantaged savings accounts for individuals with disabilities) were previously set to expire on December 31, 2025. The OBBBA made these rollovers permanent.

State conformity warning: These changes apply at the federal level. Not all states have adopted the OBBBA’s expanded definitions and higher K-12 limits. If your state has not conformed, distributions that are federally tax-free may still be subject to state income tax, or prior state tax deductions may be subject to recapture. Always verify your state’s current rules before withdrawing.

6. 529-to-Roth IRA Rollover (SECURE 2.0)

The SECURE 2.0 Act, enacted in late 2022 and effective January 1, 2024, created a new option for unused 529 funds: a tax-free and penalty-free rollover into the beneficiary’s Roth IRA.

Before this provision existed, families with leftover 529 balances had limited choices — either find another qualified use or take a non-qualified withdrawal and pay taxes plus a 10% penalty on earnings. The Roth IRA rollover provides a productive second life for unused education savings.

Rollover Requirements

All of the following conditions must be met:

| Requirement | Details |

|---|---|

| Account Age | The 529 plan must have been open for at least 15 years |

| Contribution Seasoning | Funds being rolled over must have been in the account for at least 5 years |

| Roth IRA Owner | Must be the 529 plan beneficiary (parents cannot roll over to their own Roth IRA) |

| Annual Limit | Cannot exceed the Roth IRA annual contribution limit — $7,500 (under 50) or $8,600 (50+) |

| Lifetime Limit | $35,000 per beneficiary across all 529 plans |

| Earned Income | Beneficiary must have earned income ≥ the rollover amount in the year of transfer |

| Transfer Method | Must be a direct trustee-to-trustee transfer |

Key Points to Understand

The rollover amount counts toward the beneficiary’s total Roth IRA contributions for the year. If the beneficiary contributes $3,000 directly to their Roth IRA, they can only roll over $4,500 from the 529 plan (assuming the $7,500 annual limit applies). Combined contributions cannot exceed the annual limit.

The Roth IRA income limits that normally restrict high earners from contributing directly do not apply to 529-to-Roth IRA rollovers. This makes the strategy particularly valuable for beneficiaries in high-paying careers who would otherwise be ineligible for direct Roth IRA contributions.

Reaching the full $35,000 lifetime limit will take at least five years of maximum annual rollovers.

Beneficiary changes and the 15-year clock: The IRS has not yet issued final guidance, but the conservative interpretation is that changing the 529 beneficiary likely restarts the 15-year holding period. That said, many practitioners believe that changes within the same family (to a sibling, for example) may not trigger a reset. Until the IRS clarifies, the safest approach is to maintain the original beneficiary if you plan to use the Roth IRA rollover option.

7. Non-Qualified Withdrawals: Taxes and Penalties

If you withdraw 529 funds for expenses that do not qualify as qualified education expenses, the tax consequences apply only to the earnings portion of the withdrawal:

Contributions (principal): No tax or penalty. These were made with after-tax dollars, so you get them back tax-free regardless of how the withdrawal is used.

Earnings: Subject to federal income tax at ordinary rates, plus a 10% federal penalty.

Exceptions to the 10% Penalty

In certain situations, the 10% penalty is waived — though the earnings portion is still subject to income tax:

- Scholarship: If the beneficiary receives a tax-free scholarship, you can withdraw an amount equal to the scholarship without the 10% penalty

- Death or disability of the beneficiary

- Attendance at a U.S. military academy

8. 529 Plan vs. Coverdell ESA vs. UTMA/UGMA

| Feature | 529 Plan | Coverdell ESA | UTMA/UGMA |

|---|---|---|---|

| Annual Contribution Limit | None (gift tax rules apply) | $2,000 | None |

| Income Restrictions | None | MAGI above $110,000 (Single) / $220,000 (MFJ) — cannot contribute | None |

| Eligible Expenses | College, K-12, credential programs | College + K-12 | Unrestricted (beneficiary controls funds at age of majority) |

| Tax Treatment | Qualified withdrawals are tax-free | Qualified withdrawals are tax-free | Kiddie Tax may apply |

| Beneficiary Change | Allowed (within family) | Allowed (within family) | Not allowed |

| Roth IRA Rollover | Yes ($35,000 lifetime limit) | No | No |

| Financial Aid Impact | Parent asset (lower impact) | Parent asset (lower impact) | Student asset (higher impact) |

For most families, the 529 plan offers the best combination of flexibility, tax efficiency, and financial aid treatment. Coverdell ESAs are limited by a $2,000 annual cap and income restrictions, while UTMA/UGMA accounts are not restricted to education but give the beneficiary full control of the funds at the age of majority (typically 18 to 21, depending on the state).

EA Insight

Three mistakes come up repeatedly when I work with clients on 529 plans.

First, enrolling in an out-of-state plan without checking whether your home state offers a tax deduction or credit for using its own plan. If your state provides a meaningful deduction, you may be leaving money on the table. On the other hand, if your state has no income tax or does not offer a 529 deduction — California and Hawaii, for example — you should compare fees and investment options across other states and choose the plan that gives you the best overall value.

Second, rushing into a non-qualified withdrawal when plans change — a child receives a scholarship, chooses a less expensive school, or decides not to attend college. Before paying the 10% penalty and income tax on earnings, consider the alternatives: you can change the beneficiary to another family member (a sibling, cousin, or even yourself), hold the funds for graduate school or credential programs, or use the SECURE 2.0 Roth IRA rollover if the account meets the 15-year requirement. There are options — knowing they exist before you withdraw is what matters.

Third, assuming that the OBBBA’s expanded K-12 rules apply in every state. The broader expense categories and the $20,000 annual limit are federal provisions. If your state has not conformed, using 529 funds for these expanded expenses could trigger state income tax or cause a recapture of prior state deductions. Always verify your state’s position before withdrawing.

One more point worth noting: for families applying for federal financial aid, 529 plan assets held by a parent are reported as parental assets on the FAFSA, which has a significantly lower impact on aid eligibility than student-owned assets like UTMA or UGMA accounts. This is a meaningful advantage that often gets overlooked when comparing education savings options.

Frequently Asked Questions

Is there an annual contribution limit for 529 plans?

The IRS does not set an annual contribution limit. However, contributions exceeding $19,000 per person per beneficiary ($38,000 for married couples) require filing a gift tax return (Form 709). Each state also sets its own aggregate lifetime limit per beneficiary.

Are 529 plan contributions tax-deductible?

Not at the federal level. However, approximately 40 states offer a state income tax deduction or credit for contributions, with limits that vary by state.

Can 529 funds be used for K-12 education?

Yes. Under the OBBBA, starting with the current tax year, the annual withdrawal limit for K-12 education expenses increased to $20,000 per beneficiary. Qualified expenses now include textbooks, tutoring, standardized test fees, educational therapies, and dual-enrollment college courses — in addition to tuition.

Can unused 529 funds be rolled over to a Roth IRA?

Yes. Under SECURE 2.0, up to $35,000 in lifetime rollovers can be transferred tax-free to the beneficiary’s Roth IRA. The 529 account must have been open for at least 15 years, the funds must have been in the account for at least 5 years, the beneficiary must have earned income equal to or greater than the rollover amount, and each annual rollover cannot exceed the Roth IRA contribution limit.

Can I use a 529 plan from a different state?

Yes. You are not limited to your home state’s plan. However, your state may offer a tax deduction or credit only for contributions to its own plan. Compare your state’s tax benefit with the fees and investment options of other plans before deciding.

What happens if I withdraw 529 funds for non-education expenses?

The earnings portion of the withdrawal is subject to federal income tax plus a 10% penalty. The principal (contributions) is returned tax-free. The 10% penalty is waived in certain cases, such as when the beneficiary receives a scholarship, passes away, or becomes disabled.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.