Traditional IRA vs. Roth IRA — What’s the Difference?

Both are retirement accounts. The split comes down to one thing — when you get the tax break. A traditional IRA is tax-deferred: you deduct now and pay later. A Roth IRA is tax-free in retirement: you pay now and skip the tax later. That timing decides how much actually lands in your pocket decades from now.

Key Takeaways

- The tax benefits run in opposite directions. A traditional IRA is tax-deferred — deduct now, pay tax on withdrawal. A Roth IRA is tax-free on qualified distributions — pay now, withdraw later tax-free.

- The annual contribution limit is combined across both accounts: $7,500, or $8,600 if you’re 50 or older. That’s not $7,500 into each.

- Earn too much and a Roth blocks you from contributing at all (MAGI phase-out). A traditional IRA has no income limit on contributing — but your deduction can phase out if you or your spouse has a workplace plan.

- A traditional IRA forces required minimum distributions (RMDs) starting at 73 or 75, depending on your birth year. A Roth has no RMDs during the original owner’s lifetime.

- Money you contribute to a Roth (your principal) can come out anytime, tax-free and penalty-free. The tax-free treatment on earnings is what comes with conditions.

Table of Contents

1. What Is an IRA?

An IRA — short for Individual Retirement Arrangement — is a retirement account you open on your own, directly with a bank, brokerage, or other financial institution. No employer involved, which is what sets it apart from a 401(k). As long as you have qualifying income (usually earned income from work), you can open one and invest the money inside it.

Two main types exist: traditional and Roth. They share the same yearly contribution limit. The way the IRS taxes them, though, runs in opposite directions — and that single difference shapes almost every decision around them. (A third type, the SEP IRA, is built for the self-employed and works differently from the two covered here.)

You can contribute to an IRA even while you participate in a 401(k) at work. What that workplace plan affects is whether your traditional IRA contribution is deductible — and, alongside your income, whether you can put money in a Roth at all.

2. Traditional IRA: How It Works

A traditional IRA runs on one idea — tax-deferred growth. You get a break now and settle up with the IRS later.

Going in. If you meet the rules, your contribution is deductible. It lowers your taxable income for the year, so your tax bill drops right away.

Growing. Inside the account, your money compounds with no yearly tax on interest, dividends, or gains.

Coming out. When you withdraw in retirement, the full amount counts as ordinary income, taxed at your rate that year.

Pull money out before age 59½ and the taxable portion usually gets hit with a 10% additional tax. Some exceptions apply — a first home up to $10,000, qualified education costs, and a handful of others.

When the Deduction Is Actually Allowed

Whether your contribution is deductible comes down to two things: your income, and whether you or your spouse is covered by a workplace retirement plan.

| Situation | Deductibility |

|---|---|

| Neither you nor your spouse has a workplace plan | Fully deductible, regardless of income |

| You are covered by a workplace plan | Deduction phases out based on your income |

| You aren’t covered, but your spouse is | Phases out at a higher, separate income range |

If your contribution isn’t deductible, you can still make a nondeductible contribution. The money goes in after-tax, and you track it on Form 8606. This matters later — that after-tax basis isn’t taxed again when you withdraw, but the earnings are.

Required Minimum Distributions (RMDs)

There’s a deadline on the back end. The year you reach the RMD age, you have to start taking required minimum distributions — a set amount the IRS makes you withdraw each year. Under current federal tax law (the SECURE 2.0 Act), that age is 73 for people born between 1951 and 1959, and 75 for those born in 1960 or later. Miss a required distribution and an excise tax applies to the shortfall.

3. Roth IRA: How It Works

A Roth IRA flips the order. You pay the tax first.

Going in. You contribute with money you’ve already paid tax on. No deduction — what you put in is after-tax.

Growing. Same tax-deferred compounding inside the account, with no yearly tax on what it earns.

Coming out. Here’s the payoff. A qualified distribution comes out completely tax-free — your contributions and every dollar of growth.

To count as qualified, a withdrawal has to clear two hurdles: the account must be at least five years old, and you must be 59½ or older (death, disability, and a first-home purchase also open the door).

How the five-year clock works: It starts on January 1 of the first tax year you contributed to any Roth IRA — not from the date of each deposit. Open a Roth in December, and the five-year period still begins January 1 of that same year.

One feature trips people up in a good way — your contributions, the principal you put in, can come out anytime, tax-free and penalty-free, no matter the five-year rule or your age. The tax-free treatment everyone talks about applies to the earnings. Contributions come out first, then earnings, which is why early access to your own principal is so clean.

Roth IRAs carry one more advantage worth its own line. No RMDs during the original owner’s lifetime. Nothing forces a withdrawal, so the money can keep growing or pass to your heirs — which makes the Roth a strong tool for long-term and estate planning.

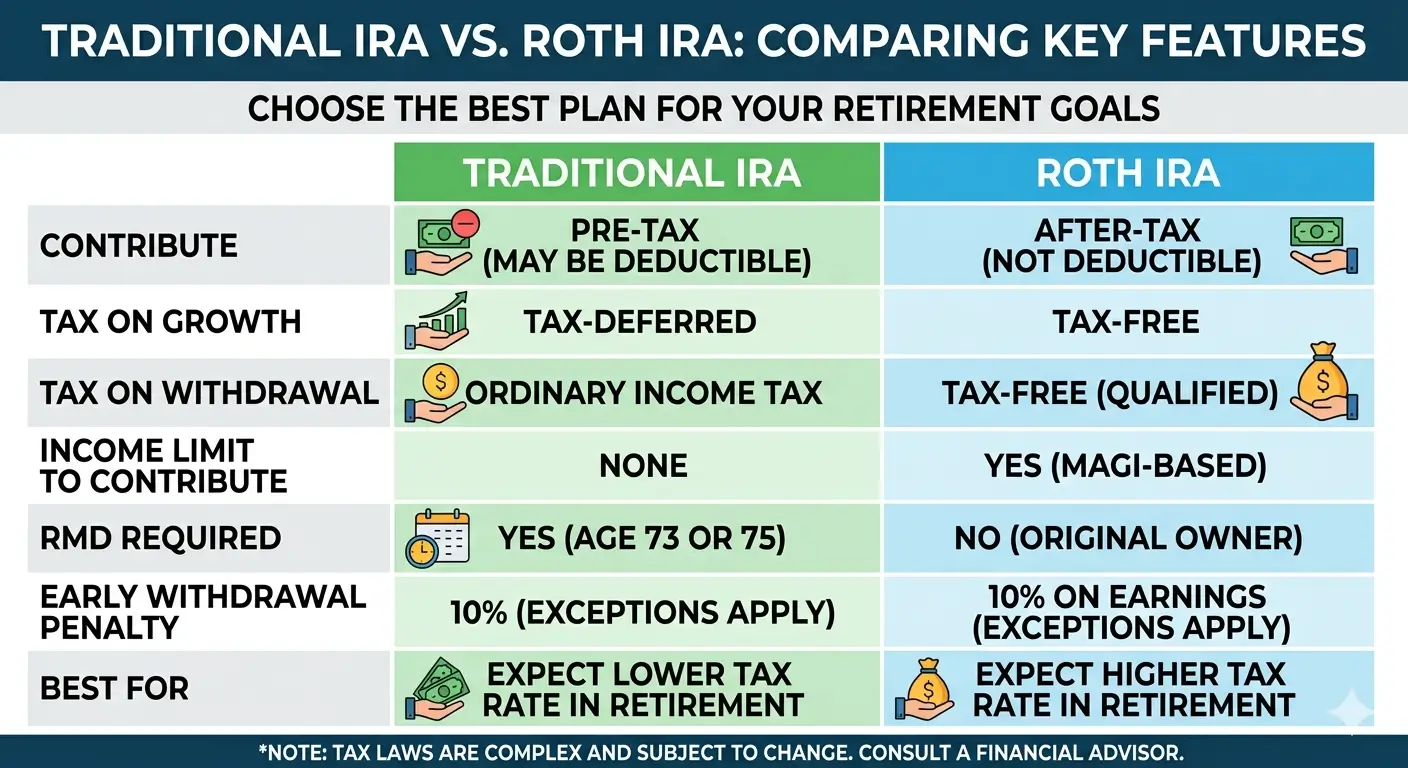

4. Traditional vs. Roth: Side by Side

Here’s how the two stack up across the features that matter most.

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Tax benefit timing | Tax-deferred | Tax-free (qualified distributions) |

| Contribution deductible? | Yes, if conditions are met | No |

| Growth inside the account | Tax-deferred | Tax-free |

| Income limit to contribute | None | Yes (MAGI phase-out) |

| Income limit on the deduction | Yes, if covered by a workplace plan | Not applicable |

| Early withdrawal of principal | 10% additional tax (exceptions apply) | Anytime, tax-free and penalty-free |

| Early withdrawal of earnings | Ordinary income + 10% additional tax | Taxable + 10% if not qualified |

| Qualified withdrawal condition | After age 59½ | 5-year rule + age 59½ (or death, disability, first home) |

| RMDs during owner’s lifetime | Required starting at 73 or 75 | None |

5. Contribution Limits and Income Rules

Three separate sets of numbers decide what you can actually do. Miss the distinction between them and you can walk straight into a penalty.

The combined annual limit

Across both accounts together, you can contribute up to $7,500 a year. Add a $1,100 catch-up at age 50 or older, and the total reaches $8,600. The word together does a lot of work here. Hold both a traditional and a Roth? The cap still covers the pair — not $7,500 into each. Your contribution also can’t exceed your taxable compensation for the year. These amounts adjust for inflation from time to time, so check IRS.gov for the current figure before you contribute.

| Age | Combined Annual Limit |

|---|---|

| Under 50 | $7,500 |

| Age 50 and older (with catch-up) | $8,600 |

Roth — who’s allowed to contribute

Earn too much and your Roth contribution shrinks, then disappears entirely. Above the top of the range, direct contributions aren’t allowed at all.

| Filing Status | MAGI Phase-Out Range |

|---|---|

| Single or Head of Household | $153,000 – $168,000 |

| Married Filing Jointly | $242,000 – $252,000 |

| Married Filing Separately | $0 – $10,000 |

Traditional — who gets the deduction

There’s no income limit on contributing to a traditional IRA. The limit is on the deduction. When you or your spouse is covered by a workplace plan, the deduction phases out based on income. When neither spouse has a workplace plan, the full deduction is available no matter how much you earn.

| Filing Status / Situation | MAGI Phase-Out Range |

|---|---|

| Single or HOH — covered by workplace plan | $81,000 – $91,000 |

| MFJ — contributing spouse covered | $129,000 – $149,000 |

| MFJ — contributor not covered, spouse is | $242,000 – $252,000 |

| MFS — covered by workplace plan | $0 – $10,000 |

Above the top of a phase-out range, no deduction is allowed — but you can still make a nondeductible contribution and track it on Form 8606.

Don’t confuse the two limits: a Roth limits whether you can contribute. A traditional IRA limits whether your contribution is deductible. These are different rules with different thresholds — and mixing them up is one of the most common mistakes I see.

6. Which One Should You Choose?

There’s no universal answer. It comes down to a single question: is your tax rate higher now, or will it be higher in retirement?

Early in your career, with a low rate, a Roth often wins. You lock in tax at a cheap rate today and pull out decades of growth tax-free. Flip the picture — a high earner now who expects less income later — and the traditional IRA’s upfront deduction can be the stronger move. When the future is genuinely uncertain, splitting contributions between both spreads your tax exposure.

One caution worth keeping in mind: your “retirement tax rate” isn’t simply today’s bracket. Social Security (often partly taxable), pension income, rental income, and RMDs from other accounts all stack up. Plenty of retirees end up with more taxable income than they expected — which is why this deserves a real projection, not a rule of thumb.

Earn above the Roth limit? Some high earners use a backdoor Roth: contribute to a traditional IRA without taking the deduction, then convert it to a Roth. The strategy works. The catch is the pro-rata rule, which can hand you a surprise tax bill if you already hold pre-tax IRA money. It’s worth understanding carefully before you make the move — the Related Articles section below covers exactly how that trap works.

EA Insight

Two traps cross my desk more than any others.

The first is blowing past the Roth income limit without noticing. A client in her early thirties got a raise, then contributed $7,000 to her Roth the same way she had every year before. Her MAGI had crossed the limit. That turned the whole contribution into an excess contribution, which carries a 6% excise tax for every year it sits in the account. We caught it before she filed and pulled the excess plus its earnings out in time. It’s a clean reminder that “can I even contribute?” has to come first with a Roth.

The second is assuming a traditional IRA contribution is deductible when it isn’t. Another client was an active 401(k) participant whose income sat above the deduction phase-out. He contributed and expected the write-off. His deduction was zero.

Here’s the part most articles skip: a nondeductible contribution doesn’t just disappear. You have to track that basis on Form 8606 every single year.

Miss that filing and you’ll eventually pay tax twice on the same dollars when you withdraw. Before you fund either account, confirm two things — whether you’re eligible to contribute (Roth) and whether the contribution is actually deductible (traditional). Confuse them, and a move meant to save tax can cost you a penalty instead.

One last word on Roth flexibility: yes, your contributions can come out anytime. But I steer clients away from treating a Roth as a backup emergency fund. Every dollar pulled early loses decades of tax-free compounding. The flexibility is real — use it as a last resort, not a plan.

Frequently Asked Questions

Can I have both a traditional IRA and a Roth IRA?

Yes. You can hold both. Just remember the annual contribution limit applies to the two accounts combined, not to each one separately.

What happens if I contribute to a Roth but my income is over the limit?

Excess Roth contributions carry a 6% excise tax for each year the excess stays in the account. To avoid it, withdraw the excess — and any earnings on it — by your filing deadline, including extensions. You can also recharacterize it as a nondeductible traditional IRA contribution.

How does the Roth IRA five-year rule actually work?

The five-year clock starts on January 1 of the first tax year for which you made any Roth IRA contribution — not from the date of each individual deposit. Contribute for the first time in November, and the clock starts January 1 of that same year. You don’t restart the five-year period with each new contribution. A Roth conversion, though, has its own separate five-year clock for penalty-free withdrawal of the converted amount before age 59½.

What if I need to pull money out of my Roth IRA early?

Your contributions (the principal) can come out anytime, tax-free and penalty-free. Withdraw the earnings before you meet the qualified-distribution conditions, though, and that portion can be taxed and hit with a 10% additional tax.

Can a non-working spouse contribute to an IRA?

Yes. Under the spousal IRA rules, a non-working spouse can contribute based on the working spouse’s earned income, as long as the couple files jointly and has enough combined earned income. The same contribution limit applies — and Roth income limits still apply if contributing to a Roth.

Can I convert a traditional IRA to a Roth IRA?

Yes. A Roth conversion moves funds from a traditional IRA into a Roth. The converted amount is added to your taxable income for that year. There’s no income limit on conversions — anyone can convert regardless of MAGI. If you hold large pre-tax IRA balances, weigh the full tax impact (and the pro-rata rule) before proceeding.

I have a 401(k) at work. Can I still contribute to an IRA?

Yes. A workplace plan doesn’t stop you from contributing to a traditional or Roth IRA. It can limit whether your traditional IRA contribution is deductible, based on your MAGI. Roth eligibility is subject to its own MAGI limits regardless of workplace plan participation.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.