What Filing Status Should You Use the Year Your Spouse Dies?

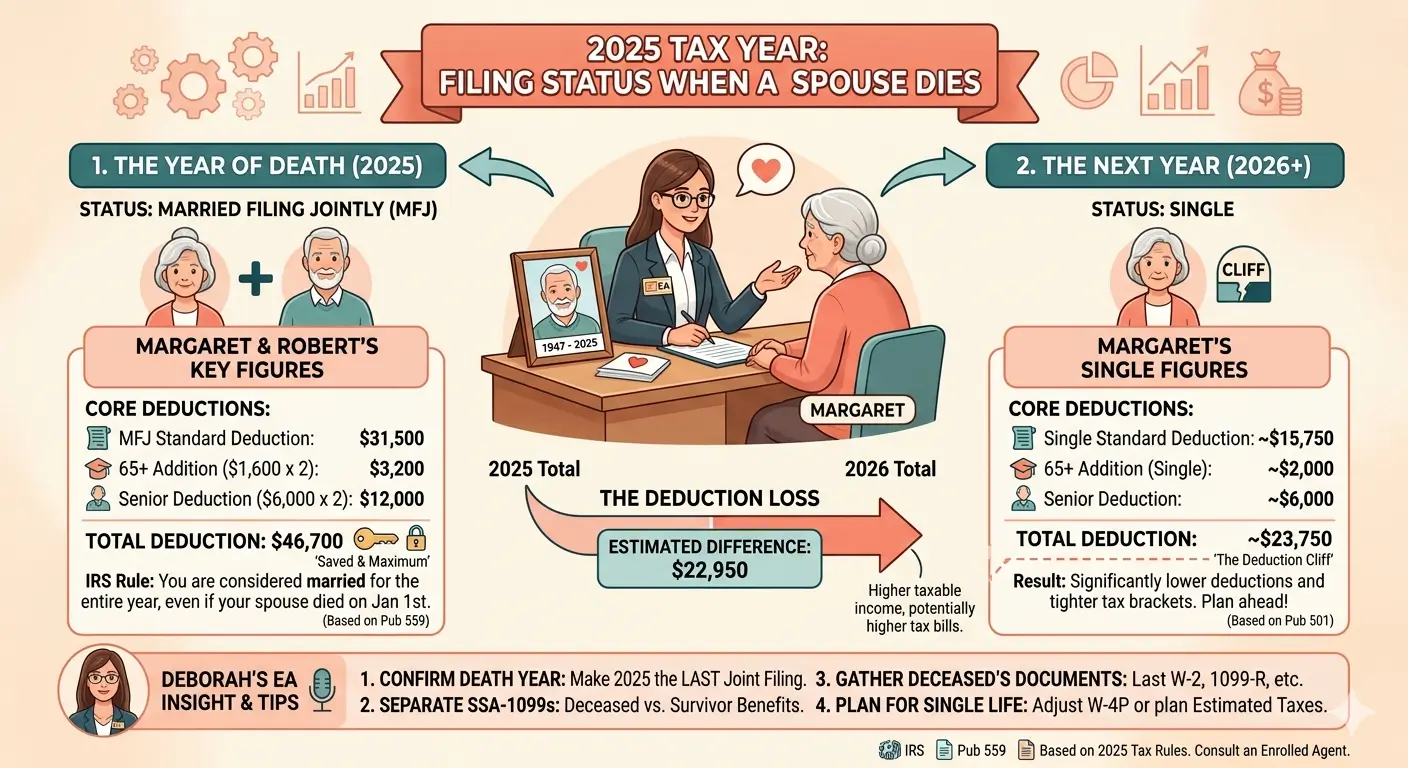

Last fall, after 47 years of marriage, Margaret lost Robert. She walked into our office with a small stack of tax documents and one question: “I’m alone now—so I file as Single, right?” The answer caught her off guard. The year your spouse dies, you can still file jointly. For Margaret, that one fact was worth about $22,950 in deductions.

Key Takeaways

- The year of your spouse’s death is the last year you can file Married Filing Jointly.

- Qualifying Surviving Spouse status applies only if you have a dependent child. Older widows without one move straight to Single the next year.

- For a couple where both spouses are 65 or older, 2025 MFJ deductions stack to $46,700 — base standard deduction plus the age-65 add-on plus the new Senior Deduction.

- Filing as Single instead drops that figure to $23,750 — a roughly $23,000 swing on the same household income.

- IRS Publication 559 is the primary guide for surviving spouses. Read it once, and you’ll save yourself a year of confusion.

Table of Contents

1. Meet Margaret

Robert was 78. Margaret is 75. They had been married 47 years and raised two children, both grown now, both with families of their own. Robert passed in October 2025 from age-related illness.

When Margaret came in, she wasn’t visibly grieving. She had her papers in order. She had handled the funeral arrangements, called Social Security, and gotten Robert’s pension switched over to her own name. One thing remained on her list: this year’s taxes.

She wasn’t wrong to ask. She was just a year early. The IRS treats a surviving spouse as still married for the entire year their spouse died — even if the death happened in January, even if it happened on December 31st. That single rule changed Margaret’s whole return.

2. The Year of Death Rule

The rule itself is short, and it lives in IRS Publication 559, the survivor’s tax guide. If your spouse died during the tax year and you haven’t remarried before December 31st, you can file Married Filing Jointly for that year. The year of death is the last year you can do this.

Bottom line

The year your spouse died, you file jointly. Starting the year after, you don’t.

That second sentence is where most surviving spouses stumble. They assume one of two things — either that they switch to Single immediately when their spouse dies, or that they get to keep filing jointly for two more years as a “Qualifying Surviving Spouse.” Both assumptions miss the real rule.

QSS is a real status, and it does extend MFJ tax treatment for two years. It also requires a dependent child living with you. No child, no QSS. For Margaret, whose children have been independent for decades, the path is straightforward: MFJ for 2025, Single for 2026 onward.

3. Margaret’s Numbers

Margaret’s stack of papers came down to five documents. Here’s what each one represented (numbers anonymized and rounded):

| Document | Source | Amount |

|---|---|---|

| W-2 | Robert (final wages before death) | $9,200 |

| 1099-R | Robert’s pension (distributions before death) | $14,400 |

| SSA-1099 | Robert (Social Security through date of death) | $22,800 |

| 1099-R | Margaret’s own pension | $18,600 |

| SSA-1099 | Margaret (includes survivor benefit) | $26,400 |

After running the Social Security taxability worksheet (only part of SS is ever taxable), Margaret’s combined AGI landed around $67,580. That’s the income side.

The deduction side is where filing status starts to matter. Both Margaret and Robert turned 65 years ago, so under MFJ they both qualified for the senior add-ons:

| Deduction (2025 MFJ) | Amount |

|---|---|

| Base standard deduction | $31,500 |

| Age-65 add-on ($1,600 × 2) | $3,200 |

| OBBBA Senior Deduction ($6,000 × 2) | $12,000 |

| Total deductions | $46,700 |

Taxable income: $67,580 minus $46,700 leaves $20,880. That sits inside the 10% bracket for MFJ, putting Margaret’s federal tax around $2,090 before withholding. Once we credited the federal withholding already taken from her pensions and Social Security, Margaret was looking at a small refund.

4. What If She Had Filed Single?

Same income, same household, same year. Just a different box checked on Form 1040.

| Deduction (2025 Single) | Amount |

|---|---|

| Base standard deduction | $15,750 |

| Age-65 add-on (Single) | $2,000 |

| OBBBA Senior Deduction | $6,000 |

| Total deductions | $23,750 |

The gap between MFJ and Single comes out to $22,950 in lost deductions. And that’s only the deduction side. Single uses narrower tax brackets too, so the same taxable income gets taxed harder. For Margaret’s situation, the additional tax landed somewhere between $2,500 and $3,000.

Important: Filing Single in the year of death isn’t just suboptimal — it’s the wrong answer for almost every surviving spouse who was eligible to file jointly with their late partner. The IRS treats the surviving spouse as married for the full year. Single isn’t on the menu yet.

5. When the Situation Looks Different

If There’s a Dependent Child — Qualifying Surviving Spouse

This is the case where QSS comes in. A surviving spouse who keeps up a home for a qualifying dependent child can use MFJ tax rates for the two years following the year of death. Year of death is still MFJ. Then two years of QSS. After that, Head of Household if the dependent is still in the home.

Practical point

QSS doesn’t let you file a joint return. It just gives you the joint tax brackets and the highest standard deduction. The deceased spouse’s name is no longer on the return.

If the Death Was Early in the Year

Doesn’t matter. A spouse who died in January gets the same treatment as one who died in December. The year of death is the year of death.

If the Surviving Spouse Remarries the Same Year

Rare, but it happens. The surviving spouse files MFJ with the new spouse, and the deceased spouse’s final return goes through as Married Filing Separately.

The Year After — Where the Cliff Lives

For Margaret, 2026 means filing Single. Her standard deduction will be roughly $24,100 (using 2026 figures: $16,100 base + $2,000 age-65 + $6,000 Senior Deduction). That’s almost exactly half of what she got in 2025. Her tax bill will jump even though her income probably won’t change much. This is the cliff that catches widowed retirees off guard, and it’s worth planning for the moment the first return is filed.

6. What to Check Right Now

- Confirm the year your spouse died — that’s your last MFJ year.

- Gather W-2, 1099-R, and SSA-1099 forms covering income up to the date of death.

- Separate the survivor benefit portion of your own SSA-1099 from your spouse’s pre-death Social Security.

- Check that both age-65 add-ons and both Senior Deductions are applied if both spouses qualified.

- Look at next year’s filing status now — Single, HOH, or QSS — and run a rough tax estimate so you’re not surprised.

- Mark the deceased spouse’s final return with “Deceased” and the date of death across the top of Form 1040.

EA Insight

After several seasons in this work, the first question from a newly widowed client is almost always the same. “I’m Single now, right?” The answer is almost always “Not this year.” That single distinction can swing several thousand dollars on the first return after a death.

Two things tend to trip people up. First is the survivor benefit on Social Security. When a spouse dies, SSA pays out the deceased spouse’s benefit through the date of death, and from that point forward the surviving spouse generally receives whichever benefit is higher under their own number. Two SSA-1099s come in the year of death, and they go on the joint return together. Starting the next year, only one SSA-1099 arrives — the surviving spouse’s. People look at the lower total and assume something went wrong. Nothing did. Second is the pension. The portion paid out before death belongs on the joint return as the deceased spouse’s. The portion paid after death, once the pension was retitled into the surviving spouse’s name, belongs to the surviving spouse going forward. Two 1099-Rs, and they need to stay sorted.

The third thing — and this is the part I always say out loud before a widow walks out the door — is what happens next April. A surviving spouse without a dependent child loses MFJ status the year after the death. Her standard deduction roughly halves. Her tax brackets narrow. If nothing else changes, her tax bill goes up. The way to avoid the second shock is to act now, while we’re still finishing the first return. I’ll usually recommend filing a fresh Form W-4P with the pension administrator to bump up federal withholding by a notch, or starting quarterly Estimated Tax payments using Form 1040-ES. A few hundred dollars more taken out monthly is much easier to absorb than a $2,500 surprise next April.

One more piece sits outside the return itself — what happens to the cost basis on assets the surviving spouse inherits. That’s a story of its own, and we’ll cover it separately.

EA Summary

The year a spouse dies, the surviving spouse can still file jointly. That status is on the table for one year only. Without a dependent child, Single is the path the year after — and a much smaller standard deduction comes with it. The work isn’t only filing the first return correctly. It’s getting ready for the second one.

Frequently Asked Questions

My spouse died in December. Can I really still file jointly for that year?

Yes. The date of death within the year doesn’t change anything. As long as you were married at the time of death and haven’t remarried before December 31st, MFJ is available for the year of death.

Do I need to file a separate “final return” for my deceased spouse?

No. The MFJ return for the year of death serves as the final return for the deceased spouse. One Form 1040 covers both. You’ll write “Deceased” along with the date of death across the top of the return, and you sign as the surviving spouse.

My adult children aren’t dependents. Can I still claim Qualifying Surviving Spouse?

Not unless they meet the dependent qualifying child tests, which usually require age, residency, and support conditions. Adult children with their own households generally won’t qualify. Without a qualifying dependent, QSS doesn’t apply.

Where does the survivor pension go on my taxes?

The portion paid before death belongs on the joint return under the deceased spouse’s name. The portion paid after death, once retitled to the surviving spouse, belongs to the surviving spouse on the joint return for the year of death and on their own return going forward.

My tax bill is going to jump next year. What should I do now?

Two practical options. File a new Form W-4P with each pension administrator to increase federal withholding. Or start quarterly Estimated Tax payments using Form 1040-ES. Either way, the goal is to spread the increase across the year instead of facing it as one bill in April.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.