One W-4, a Lot of Confusion — What F-1 Couples Need to Know

When both spouses are on F-1 visas, the W-4 isn’t filled out the same way a U.S. citizen would. The rules are different — and getting them wrong sets up a surprise tax bill at the end of the year.

Key Takeaways

- F-1 visa holders are generally classified as Nonresident Aliens (NRAs) for U.S. tax purposes during their first five years in the country.

- NRAs must follow Notice 1392’s special instructions when completing Form W-4 — including checking “Single or MFS” and writing “Nonresident Alien” below Step 4(c).

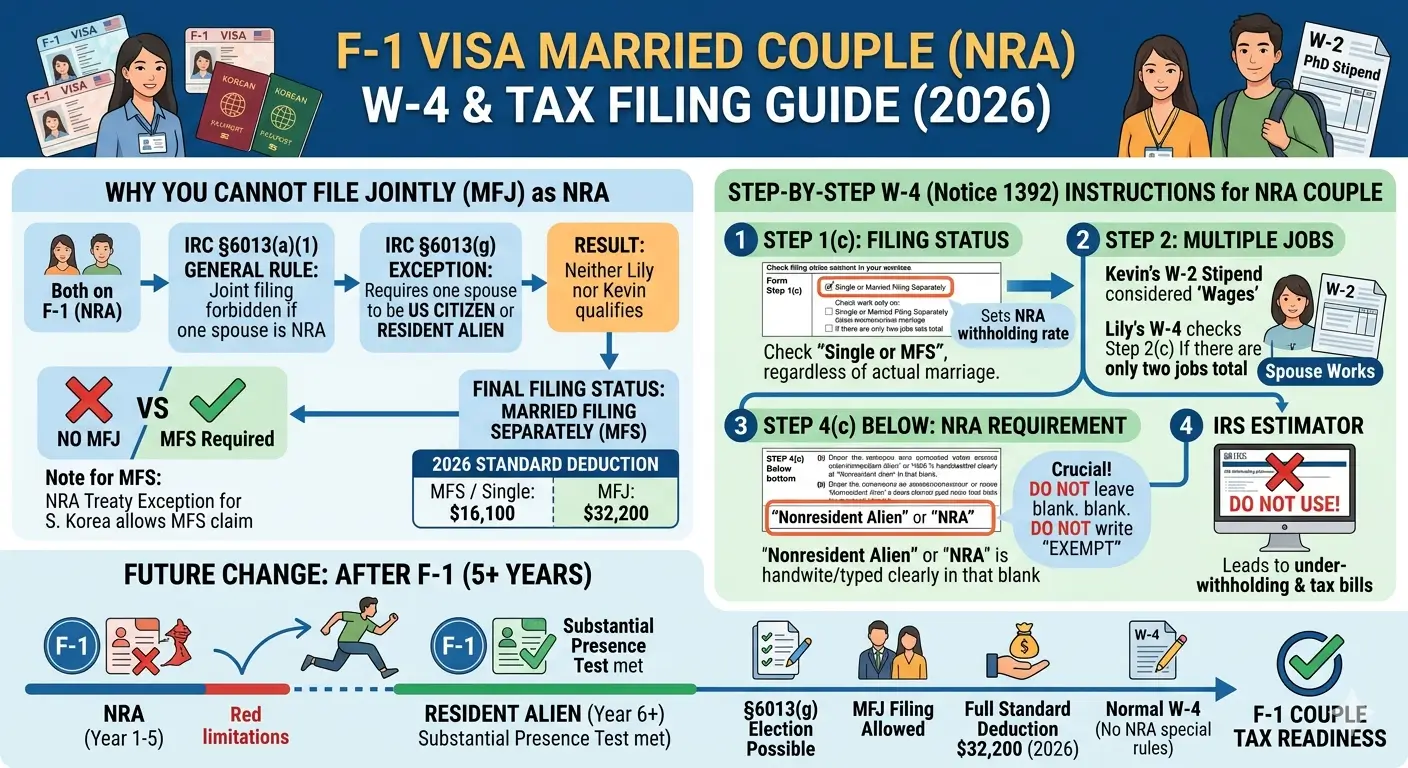

- When both spouses are NRAs, Married Filing Jointly is not available. IRC §6013(g) — the one exception — requires one spouse to be a U.S. citizen or resident alien.

- If a spouse receives a PhD stipend paid as wages (W-2), the “Multiple Jobs / Spouse Works” section of Form W-4 applies.

- Once one spouse clears the five-year mark and meets the Substantial Presence Test, the tax picture changes significantly.

Table of Contents

- 1. Meet Lily — W-4 in Hand, No Idea What to Check

- 2. What “NRA” Means on Your W-4

- 3. Why Both-F-1 Couples Can’t File Jointly

- 4. Kevin’s Stipend and the “Spouse Works” Question

- 5. What Changes After Five Years

- 6. What to Check Right Now

- 7. EA Insight

- 8. Frequently Asked Questions

- 9. Related Articles

- 10. Official Resources

1. Meet Lily — W-4 in Hand, No Idea What to Check

Lily had two days before her first day of work. The job offer was done, the start date was confirmed, and the onboarding paperwork was sitting in her inbox. Most of it was straightforward. Then she got to Form W-4.

She and her husband Kevin had both come from South Korea on F-1 visas. They’d gotten legally married while in the U.S. Kevin was deep into his PhD program, pulling in a stipend from his university. Lily had just wrapped up her degree and was starting her first U.S. job on OPT.

Kevin had been doing some research. He’d found posts in international student forums saying that F-1 couples can’t file jointly — that Married Filing Separately was the only option. But nobody explained why, and nobody said what that actually meant for the W-4 she needed to submit tomorrow.

The confusion is common. The answers are specific. Here’s what Lily needed to know.

2. What “NRA” Means on Your W-4

Form W-4 tells your employer how much federal income tax to withhold from each paycheck. Get it wrong, and the math doesn’t catch up with you until the following spring — when you either owe money you weren’t expecting or realize you overpaid all year.

F-1 visa holders are classified as Nonresident Aliens (NRAs) for U.S. federal tax purposes during the first five calendar years they are present in the country. The clock doesn’t move to Resident Alien status until a person passes the Substantial Presence Test — which generally requires being physically present in the U.S. for at least 183 days over a three-year period, counting the current year in full and prior years at reduced weights. Lily and Kevin are in year three. Both NRAs.

NRAs don’t fill out W-4 the same way a U.S. citizen does. The IRS published Notice 1392 specifically to address this — it modifies the standard W-4 instructions for nonresident alien employees. Three rules matter most:

| W-4 Item | U.S. Citizen / Resident | Nonresident Alien (Notice 1392) |

|---|---|---|

| Step 1(c) — Filing Status | Reflects actual marital status | Always check “Single or MFS” — regardless of marital status |

| Step 4(c) — Space Below | Leave blank or enter extra withholding | Write “Nonresident Alien” or “NRA” — required |

| IRS Withholding Estimator | Available and recommended | Do not use — not designed for NRA calculations |

Important: NRAs cannot write “EXEMPT” in the space below Step 4(c). Writing “Nonresident Alien” or “NRA” is required — these are not interchangeable.

Lily is legally married, but on Step 1(c) of her W-4, she must check “Single or Married filing separately.” This isn’t a statement about her relationship. It’s a technical designation that tells the employer’s payroll system to apply NRA withholding rates — which are calculated differently from standard resident rates.

3. Why Both-F-1 Couples Can’t File Jointly

Kevin’s research was right. When both spouses are nonresident aliens, Married Filing Jointly is off the table.

The general rule is in IRC §6013(a)(1): if either spouse is a nonresident alien at any point during the tax year, a joint return cannot be filed. There is one exception — IRC §6013(g), which allows a nonresident alien spouse to be treated as a U.S. resident for tax purposes so that the couple can file jointly. Couples use it all the time.

The catch

IRC §6013(g) only works when one spouse is already a U.S. citizen or resident alien. It can’t make both spouses into residents — it can only elevate one NRA to resident status when the other person already qualifies as a resident.

Lily and Kevin are both NRAs. Neither of them meets the “U.S. citizen or resident alien” prerequisite. The §6013(g) election isn’t available to them, not because of paperwork, but because the underlying requirement doesn’t exist. Their filing status for the tax year is Married Filing Separately — full stop.

That has real consequences for their standard deduction. For tax year 2026:

| Filing Status | 2026 Standard Deduction |

|---|---|

| Married Filing Jointly | $32,200 |

| Married Filing Separately | $16,100 |

| Single | $16,100 |

Note on the standard deduction for NRAs: Nonresident aliens generally cannot claim the standard deduction. South Korean nationals are an exception under the U.S.–Korea tax treaty, which allows an MFS-equivalent standard deduction of $16,100 for 2026. This applies at the annual tax return stage — on Form 1040-NR — and is separate from the W-4 withholding calculation.

4. Kevin’s Stipend and the “Spouse Works” Question

Lily hit another snag at Step 2 of the W-4. The instructions say to complete that section if you hold more than one job at the same time, or if you’re married filing jointly and your spouse also works. Kevin gets a PhD stipend from the university. Does that count?

Kevin’s stipend comes from his work as a Teaching Assistant — paid as wages and reported on a W-2. That makes it employment income, and it matters for Lily’s withholding.

How it affects Lily’s W-4

Kevin’s W-2 stipend is wages. Two people in the household are earning income, and the withholding calculation should reflect that. Lily should work through Step 2 of her W-4 to avoid under-withholding across the household.

If the stipend is a fellowship, not wages: Some PhD stipends are pure fellowships with no service requirement. These are reported on Form 1042-S or Form 1099, not W-2, and are not classified as wages. In that case, Step 2 of the W-4 does not apply — but the fellowship income is still taxable and may require quarterly estimated tax payments. Check which form Kevin’s university issues before completing Lily’s W-4.

5. What Changes After Five Years

None of these restrictions are permanent. Once a person has been in the U.S. on F-1 status for more than five calendar years and meets the Substantial Presence Test, the IRS reclassifies them as a Resident Alien for tax purposes. At that point, the NRA rules fall away entirely.

What opens up when one spouse becomes a resident

As soon as one of them crosses into resident alien status, the §6013(g) election becomes available. The resident spouse can elect to treat the still-NRA spouse as a resident, and the couple can file jointly. For 2026, that means access to a $32,200 standard deduction instead of $16,100 — a meaningful difference at most income levels.

What changes on the W-4

Once classified as a resident alien, the Notice 1392 rules no longer apply. The W-4 gets filled out the same way any U.S. employee would. No NRA notation, no forced “Single or MFS” selection, no restriction on the withholding estimator.

Practical point

The residency transition year can be complicated. If one spouse shifts from NRA to resident alien during the tax year, dual-status filing rules apply. That’s a separate calculation entirely — worth addressing with a tax professional in the year it happens.

6. What to Check Right Now

- Confirm your F-1 entry year — have you been in the U.S. for five or more calendar years?

- On W-4 Step 1(c), check “Single or Married filing separately” regardless of actual marital status.

- In the blank space below Step 4(c), write “Nonresident Alien” or “NRA.” Don’t leave it blank, and don’t write “EXEMPT.”

- Confirm whether your spouse’s stipend is paid as wages (W-2) or as a fellowship (1042-S / 1099) before completing Step 2.

- Do not use the IRS Tax Withholding Estimator — it doesn’t account for NRA withholding rules.

- Note your residency transition year so you’re prepared for the year the rules change.

EA Insight

The question I hear most often from F-1 couples isn’t about the tax return — it’s about the W-4. They’re legally married, so checking “Single” feels wrong. It isn’t. For an NRA, that checkbox isn’t a marital status question. It’s an instruction to the payroll system about which withholding table to use.

What actually causes problems is the missing NRA notation below Step 4(c). When that line is left blank, the employer’s system treats the employee as a standard resident. The withholding comes out lower than it should. Come spring, there’s a balance due — and sometimes an underpayment penalty on top of it. A single line of text could have prevented the whole thing.

The §6013(g) confusion is also worth addressing directly. Many people find articles about it online and think it’s a solution available to any married couple with a nonresident spouse. It isn’t. The election exists to help mixed-status couples — one resident, one nonresident. When both spouses are NRAs, the election has no legal basis. MFS is the only filing status available, and the tax return for each spouse is filed separately on Form 1040-NR.

EA Summary

When both spouses hold F-1 status, they are nonresident aliens — and that classification controls everything from how the W-4 is filled out to what filing status is available at tax time. MFJ is not an option, §6013(g) doesn’t apply, and the W-4 must follow Notice 1392 rules: “Single or MFS” in Step 1(c) and “Nonresident Alien” written below Step 4(c). Getting those two things right from day one is the simplest way to avoid a withholding shortfall by year-end.

Frequently Asked Questions

Does checking “Single or MFS” on the W-4 affect my actual tax filing status?

No. Your W-4 filing status designation is used only for withholding calculation purposes. Your actual tax return filing status — Married Filing Separately — is determined by your circumstances at year-end and reported on your annual return, not on the W-4.

What form do F-1 nonresident aliens use to file their annual tax return?

Form 1040-NR, U.S. Nonresident Alien Income Tax Return. This is a separate form from Form 1040, which is used by U.S. citizens and resident aliens. Each spouse files their own 1040-NR individually.

Can we file jointly if one of us becomes a resident alien during the year?

Possibly, but the year of transition is complicated. If one spouse shifts from NRA to resident alien status during the tax year, dual-status filing rules apply. In the following year, when that spouse is a resident alien for the full year, the §6013(g) election may become available and joint filing is an option.

Is a PhD stipend always taxable income?

It depends on the nature of the payment. Stipends paid in exchange for services such as teaching or research assistance are wages and are fully taxable. Pure fellowship grants with no service requirement may be partially or fully excludable from income, but the portion used for room, board, or non-qualified expenses is still taxable. Check which form your university issues — W-2 indicates wages, while 1042-S or 1099 indicates a fellowship or other payment type.

Do South Korean nationals on F-1 visas qualify for any U.S. tax treaty benefits?

Yes. Under the U.S.–Korea income tax treaty, South Korean nationals can claim the standard deduction on Form 1040-NR — an exception that most other NRAs don’t have. For tax year 2026, the MFS standard deduction is $16,100. This benefit applies at the tax return stage and must be claimed explicitly on the return.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.