“My Old Accountant Did It This Way” — How a Dry Cleaner Couple Almost Walked Into an IRS Audit

Just because you swiped the business card doesn’t mean it’s a business expense. Tens of thousands of dollars in personal spending had been hiding inside this couple’s “business” credit card statement — a ticking time bomb pointed straight at the IRS.

Key Takeaways

- A business credit card doesn’t automatically make a purchase a business expense. The purpose of the spending is what counts — not the name on the card.

- Groceries, kids’ martial arts lessons, family vacations, golf — no matter how they’re labeled, the IRS will not accept these as business expenses.

- Misclassified expenses can trigger a 20% accuracy-related penalty (IRC §6662). If the IRS finds intent, it becomes a 75% civil fraud penalty (IRC §6663).

- If fraud is established, the statute of limitations disappears. Returns from 7, 10, or even 15 years ago can be reopened.

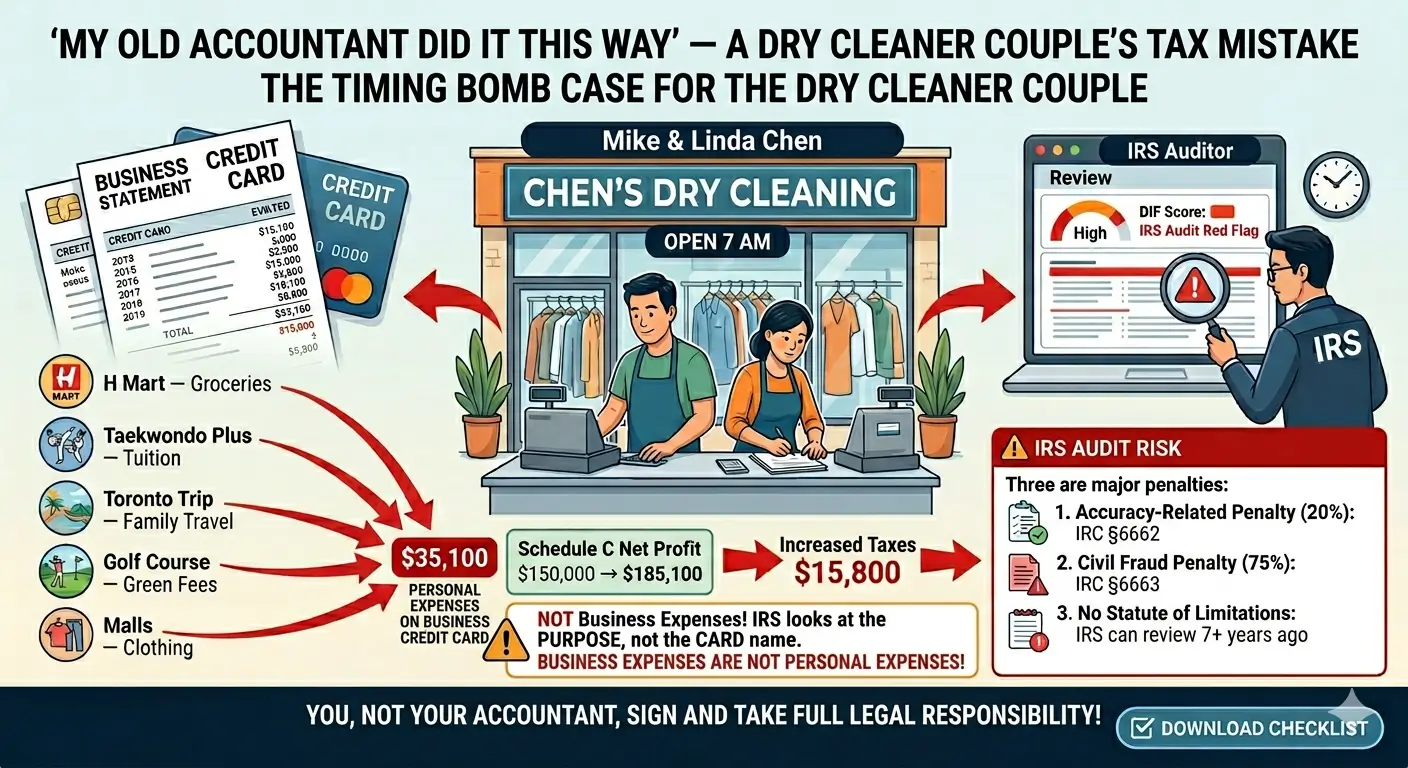

- “My old accountant did it this way” is not a defense the IRS accepts. The person who signs the return is the taxpayer — not the preparer.

Table of Contents

- 1. Meet Mike and Linda

- 2. What I Found on Their Credit Card

- 3. The IRS Rule — What Counts as a Business Expense

- 4. “My Old Accountant Did It This Way” — The Most Dangerous Words

- 5. The Real Risk Isn’t the Extra Tax

- 6. What to Do Right Now

- 7. EA Insight

- 8. Frequently Asked Questions

- 9. Related Articles

- 10. Official Resources

1. Meet Mike and Linda

Mike and Linda Chen ran a small dry cleaner in their neighborhood. Married twenty years, immigrants who had never taken a single day off — open every morning at 7 a.m., rain or shine.

They came to me after years with another accounting firm. At our first meeting, both of them looked relaxed. Comfortable, even.

I did what I always do at a first intake. I pulled up twelve months of their business credit card statement.

And then I stopped scrolling.

H Mart — $147.32

The next line.

Taekwondo Plus — $185.00

Page after page: a Toronto hotel, golf greens fees, family-style restaurant tabs, summer camp registration. Spending tied to the actual dry cleaning business? Harder to find than the personal stuff.

2. What I Found on Their Credit Card

Here’s what the major categories looked like on a single year of statements. Identifying details have been removed; the figures reflect the actual case.

| Category | Annual Total (approx.) | Business Connection? |

|---|---|---|

| Korean grocery / general groceries | $8,200 | None |

| Kids’ martial arts & summer camp | $4,800 | None |

| Family-style restaurant tabs | $6,400 | Mostly none |

| Family vacation to Canada | $5,100 | None |

| Out-of-area shopping malls | $3,900 | None |

| Golf & other leisure | $4,200 | None |

| Clothing & personal items | $2,500 | None |

| Personal spending — total | ≈ $35,100 | Fully nondeductible |

Given the dry cleaner’s revenue scale, more than 60% of the card’s annual spending was personal. Through the eyes of an IRS examiner, this isn’t a business credit card anymore. It’s the owner’s personal wallet — with the company’s name printed on it.

— Mike, when I first raised the issue

That’s where the trouble starts. A business card and a business expense are not the same thing. The IRS doesn’t care about the name on the card. It cares about why the money was spent.

3. The IRS Rule — What Counts as a Business Expense

Internal Revenue Code Section 162 defines deductible business expenses as those that are ordinary and necessary in carrying on a trade or business.

Plainly: it has to be the kind of expense another business owner in the same field would reasonably incur, and it has to actually help operate that business.

On the other side of the line is IRC Section 262, which is just as direct. Personal, living, and family expenses are not deductible.

Bottom line

Family groceries, kids’ lessons, family trips, family meals — no matter what card paid for them or how the bookkeeper labeled them — they are not business expenses.

What ordinary and necessary purpose does a Korean grocery run serve for a dry cleaning operation? How does a child’s taekwondo class connect to running the business? What about a Toronto hotel?

The answer is the same in every case. No connection.

4. “My Old Accountant Did It This Way” — The Most Dangerous Words

I told them the truth. These charges could not be deducted as business expenses. Every single one of them needed to be reclassified as an owner’s draw or a distribution.

The mood in the room shifted. Linda spoke first.

They genuinely didn’t know. A professional had told them this was the way, so they trusted it. Their tax bill came back small every year, so they assumed the accountant was good at his job.

Here’s the part that almost no one explains clearly until it’s too late.

The person who signs Form 1040 and Schedule C is not the accountant. It’s the taxpayer.

The bottom of every return reads:

The preparer signs separately, but the legal responsibility lives with the taxpayer. A bad accountant can sometimes support a “reasonable cause” defense to reduce penalties — but it does not transfer the underlying liability. The tax, the interest, the audit risk — all of that stays with the person whose name is on the return.

5. The Real Risk Isn’t the Extra Tax

I rebuilt their return with the personal spending pulled out. Once $35,100 was removed from the expense column, Schedule C net profit jumped by exactly that amount. Their taxes followed.

| Category | Additional Tax (approx.) |

|---|---|

| Federal income tax (24% bracket) | $8,400 |

| Self-employment tax (15.3%) | $4,960 |

| State income tax (≈ 6.85%) | $2,400 |

| Annual additional tax | ≈ $15,800 |

Mike was stunned.

I told him the answer plainly.

“Your taxes weren’t actually low before. They were under-reported. This number is what you should have been paying all along.”

And here’s the difficult part. What I just described is the best-case scenario.

If the IRS had audited their prior returns first, the conversation would have looked very different.

The dry cleaning industry has a known expense profile. The IRS uses an algorithmic system called the DIF score (Discriminant Inventory Function System) to flag returns whose expense ratios diverge from industry norms. A small business showing 60% personal spending dressed up as business expenses is the kind of pattern that profile catches. Once flagged, here’s what the math could have looked like over three audited years:

- Back taxes across three years: ≈ $47,000

- Interest on unpaid taxes (federal short-term rate + 3%, compounded)

- Accuracy-related penalty under IRC §6662 — 20%: ≈ $9,400

- If the IRS finds intent, civil fraud penalty under IRC §6663 — 75%: ≈ $35,000

- Once fraud is established, the statute of limitations is gone. The IRS can reopen returns from 7, 10, even 15 years back.

- In extreme cases, criminal tax evasion under IRC §7201 enters the conversation.

Paying $15,800 more in current-year tax is one outcome. The audit scenario above is a different universe.

6. What to Do Right Now

If you run a small business and use a business credit card, pull twelve months of statements today and walk through this list.

- Mark each transaction with one of three labels: B (business) / P (personal) / ? (needs review).

- For every “?” — confirm you can document a clear business purpose: receipt, email, calendar entry, or meeting notes.

- Reclassify everything personal as owner’s draw or distribution — not as a business expense.

- Make sure your expense categories map cleanly to Schedule C lines (or your business return). If your bookkeeping doesn’t roll up to the right return, the trouble starts in January, not in April.

- For meals, entertainment, travel, and vehicle expenses, IRC §274(d) requires contemporaneous records — created at the time of the transaction. Reconstructing them after the fact is a losing battle in an audit.

- Look back at prior-year returns. If something was misclassified, consider filing Form 1040-X to correct it voluntarily — before the IRS finds it first.

- Keep receipts and supporting documentation for at least seven years. Digital scans and phone photos are fully accepted under Rev. Proc. 97-22 — cloud storage is often safer than paper.

That last item — voluntary correction — matters more than people realize. When the taxpayer fixes the return before the IRS notices, the fraud penalty almost never enters the picture. When the IRS finds it first, that conversation goes a different direction entirely.

EA Insight

Every year, new business-owner clients come to me from another firm. The most nerve-wracking moment in those first meetings is opening their business credit card statement. Clean books are the exception. The fingerprints of an “extra-helpful” prior accountant are the rule.

The pattern is almost always the same. The owner says, “Just put this through the business,” and the accountant types it in. That goes on for one year, then five, then ten. Nobody pauses to ask the only question that matters: is this actually ordinary and necessary?

Here’s the part that gets missed. The time bomb isn’t in the accountant’s hands. It’s in the owner’s. A preparer who gets it wrong faces a §6694 preparer penalty at most. The owner faces back taxes, interest, accuracy or fraud penalties, and — in the worst cases — a criminal referral.

A good tax professional doesn’t tell you what you want to hear. They tell you what you need to hear. Even when it’s uncomfortable in a first meeting, that conversation is what protects you from the IRS years later. And honestly? The decision that matters most isn’t who prepares your return in April — it’s who classifies each transaction in your books every month. Same expense, different bookkeeper, completely different outcome.

EA Summary

A business credit card is just a payment method. It does not transform every charge into a deductible business expense. Korean grocery runs, kids’ lessons, family vacations, golf — however they’re labeled, they’re personal expenses to the IRS. And the responsibility for what’s on the return belongs to the person who signed it, not the preparer. Catching mistakes at the monthly bookkeeping stage is far cheaper, and far easier, than defending them in front of an IRS examiner a year later.

Worried your books look like Mike and Linda’s?

If a previous accountant put personal expenses through your business — and you’re not sure what’s been classified correctly — the time to find out is now, not during an IRS examination. Monthly bookkeeping by an Enrolled Agent means every transaction is reviewed against §162 the moment it’s recorded. No surprises in April. No surprises three years later when an audit letter arrives.

Send one month of bank and credit card statements with your latest P&L. I’ll review them and tell you, in writing, what’s classified correctly and what isn’t. Free, no obligation.

An Enrolled Agent who keeps your books — built the way the IRS reads them.

Frequently Asked Questions

If I paid with a business credit card, isn’t that automatically a business expense?

No. The IRS looks at the purpose of the spending, not the name on the card. A charge made on a business card for personal use must be treated as an owner’s draw or distribution — not as a deductible expense.

Can I deduct meals with my family as business meals?

Generally, no. A deductible business meal requires a clear business purpose, the presence of business contacts (clients, partners, employees), and contemporaneous records of who attended and what was discussed (IRC §274(d)). Family dinners almost never satisfy these requirements.

Does it help that my old accountant told me to do it this way?

Partially. A prior preparer’s bad advice can sometimes support a “reasonable cause” defense under IRC §6664(c) to reduce penalties. It does not transfer the underlying tax liability. The taxpayer signed the return, and the taxpayer carries the responsibility.

How do I correct prior-year returns that were filed incorrectly?

File Form 1040-X (Amended Return). Additional tax and interest will be owed, but voluntary correction before the IRS opens an examination dramatically reduces the chance of a fraud penalty. Form 8275 (Disclosure Statement) can add further protection. The scope and timing of any correction should be reviewed with an EA or qualified tax professional first.

Are small businesses really audited by the IRS?

Yes. The IRS runs every return through the DIF score system (Discriminant Inventory Function), which automatically flags businesses whose expense ratios deviate sharply from industry norms. Industries like dry cleaning, where revenue scale is well-established, have very predictable expense profiles — which makes outliers easier, not harder, to spot. “We’re too small to notice” is one of the most common — and most dangerous — assumptions a small business owner can make.

Official Resources

- IRS Publication 334 — Tax Guide for Small Business

- IRS Publication 463 — Travel, Gift, and Car Expenses

- IRS — About Form 1040-X (Amended Return)

- IRC §162 — Trade or Business Expenses

- IRC §262 — Personal, Living, and Family Expenses

- IRC §6662 — Accuracy-Related Penalty

- IRC §6663 — Civil Fraud Penalty

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.