Four W-2s, One Surprise Tax Bill

Daniel worked four jobs last year and picked up side work on top of that. He expected a refund. What he got was a bill. Here’s why that happens — and what actually brought the number down.

Key Takeaways

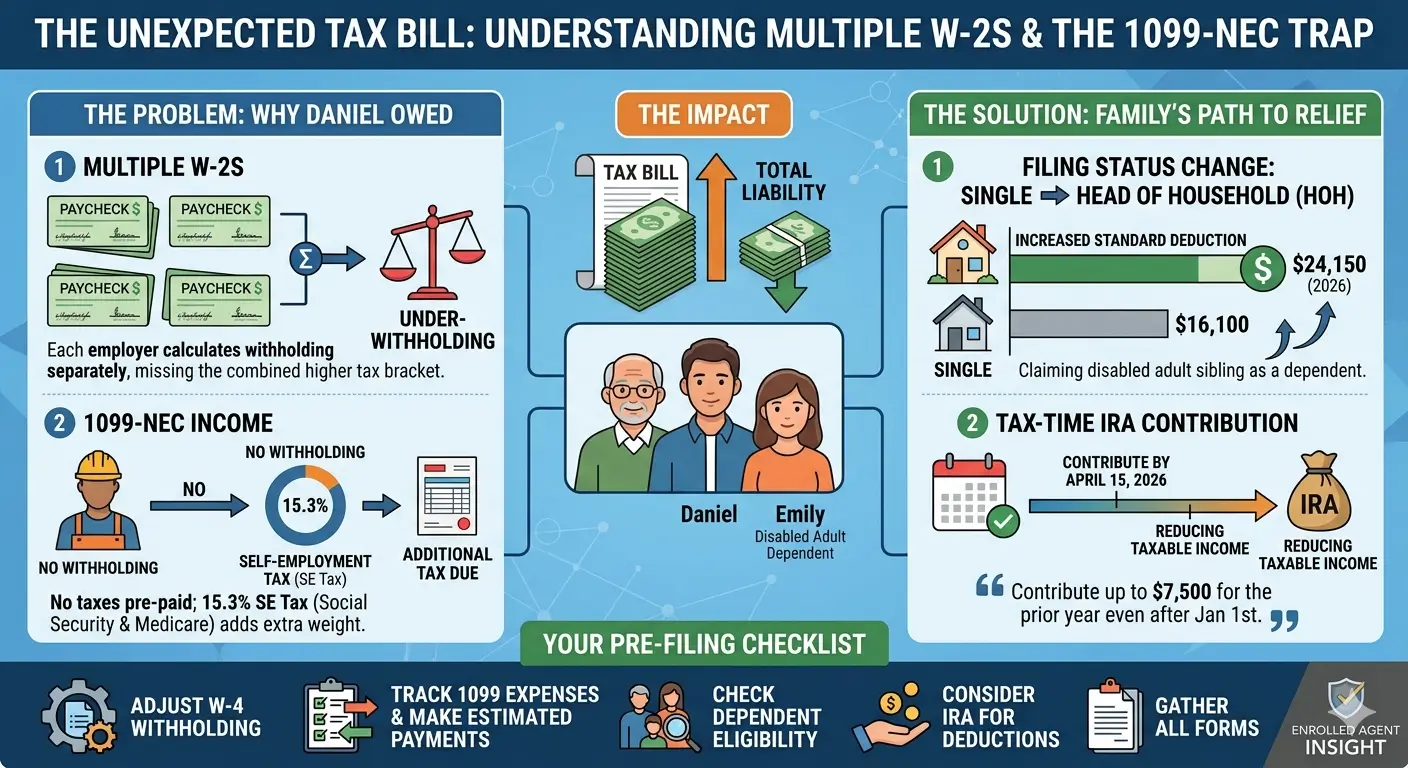

- When you hold several W-2 jobs, each employer withholds as if that job is your only income. Nobody accounts for the combined total — so withholding usually falls short.

- 1099-NEC income has no withholding at all. If net earnings reach $400, self-employment tax of 15.3% applies on top of regular income tax.

- A sibling with a permanent and total disability can be a qualifying child regardless of age, as long as the residency and support tests are met.

- One dependent can move a filer from Single to Head of Household — lifting the 2026 standard deduction from $16,100 to $24,150.

- A traditional IRA contribution can still reduce last year’s taxable income, because the deadline runs to the filing date.

Table of Contents

1. Meet Daniel

Daniel’s mother came in to file on his behalf. He was at work — he usually is. He’s in his early thirties, single, and the reason the household stays afloat.

Four people live under one roof. Daniel’s parents are both retired, and neither is in good health. His younger sister, Emily, has an intellectual disability and needs the kind of daily care a young child needs. Daniel carries almost all of it. That’s why, over the course of the year, he worked four different jobs and took side work whenever it came up.

His mother wasn’t wrong to expect a refund. Most people in her shoes would. The return told a different story, and the reason sits in how withholding works when income comes from more than one place.

2. Why Four W-2s Can Leave You Short

Every employer runs withholding off the W-4 you hand them. That form tells them one thing: roughly how much tax to hold back, based on what they pay you. They have no view into your other jobs.

So picture Daniel’s year. Four employers, four separate calculations. Each one looked at its slice of his income and withheld at the rate that slice suggested. None of them saw the full $55,000. And the federal income tax system is progressive — later dollars are taxed at higher rates than the first ones. When four employers each withhold as though their paycheck is the only paycheck, the combined amount held back lands below the tax actually owed on the stacked total.

Bottom line

More jobs is a good problem to have. But unless the W-4s are adjusted to reflect the other income, the total withholding almost always comes up short.

This isn’t a mistake anyone made. Daniel filled out each W-4 honestly. The shortfall is built into the design — and it shows up at filing time, when the four W-2s finally sit on the same return.

3. The 1099 Added Its Own Weight

Daniel also had one 1099-NEC. Side work, paid as an independent contractor. That income carries two features the W-2 jobs don’t.

First, no withholding. Not a dollar. A 1099-NEC payer sends the full amount and reports it — the tax is entirely Daniel’s to settle later.

Second, self-employment tax. Once net earnings from self-employment reach $400, the income owes SE tax of 15.3% — 12.4% for Social Security and 2.9% for Medicare. It applies to 92.35% of net earnings, and it sits on top of regular income tax, not instead of it.

Here’s where Daniel’s situation got tighter. SE tax is figured on net earnings — gross income minus business expenses. Daniel had almost nothing to deduct. No equipment, no mileage worth tracking, no real costs. So nearly the entire 1099 amount ran straight into the SE tax calculation.

| Income Source | Tax Withheld During the Year | Extra Tax at Filing |

|---|---|---|

| Four W-2 jobs | Some — but under-withheld | Income tax shortfall |

| One 1099-NEC | None | Income tax + 15.3% SE tax |

One bit of good news: half of the self-employment tax comes back as an above-the-line deduction. It doesn’t erase the SE tax, but it does lower the income that regular tax is figured on.

Put the two pieces together — under-withheld W-2s and an untaxed 1099 — and the result was the bill that surprised Daniel’s mother.

4. Who Could Claim Emily?

Now the part that worked in Daniel’s favor. Emily.

A disabled sibling has no age limit

Normally a qualifying child has to be under 19, or under 24 if a full-time student. Emily is past both. But the age test drops away entirely for someone who is permanently and totally disabled — and Emily meets that definition. A brother or sister counts as a qualifying child, so on that basis Emily can be claimed at any age.

Two more tests still have to hold. The residency test: she must live with the person claiming her for more than half the year. The support test: she must not provide more than half of her own support. Emily lives with the family year-round and has no income of her own, so both are clearly met.

Why Daniel, and not the parents?

The parents live in the same house. So why does Daniel claim Emily? Because a dependent is claimed by the person who can actually support that claim. Daniel’s parents are retired with almost no income. Daniel provides the household. Among the people in that home, he’s the one the dependent rules point to.

Practical point

Claiming Emily moved Daniel from Single to Head of Household. For 2026 that lifts the standard deduction from $16,100 to $24,150 — roughly $8,000 of additional income shielded from tax, from one filing-status change.

It’s a $500 credit, not the Child Tax Credit

Here’s a point that trips people up. Emily is an adult. Because she’s past 17, she doesn’t bring the Child Tax Credit. She brings the Credit for Other Dependents — $500, nonrefundable. Many families assume a disabled dependent means a large credit. The dependent still matters a great deal, mostly through the filing-status change, but the credit itself is the $500 ODC.

5. The Move That Brought the Number Down

By this point the return still showed a balance due. The filing status was set, the dependent was claimed, the income was all in. So what was left?

One thing. Daniel had no retirement plan at work — none of the four jobs offered one. That opened the door to a traditional IRA. When neither you nor a spouse is covered by a workplace plan, the contribution is fully deductible no matter the income.

So Daniel contributed to a traditional IRA, up to the 2026 limit of $7,500. And here’s the part that makes an IRA unusual: the contribution deadline isn’t December 31. It runs to the filing deadline. A contribution made in the spring can still count for the prior tax year — which means it can still reduce a tax bill for a year that has already ended.

The deductible contribution lowered Daniel’s taxable income. The balance due came down. Not erased — under-withholding and SE tax don’t simply vanish — but a return that had felt like a dead end turned into a smaller, manageable number. And Daniel finished the year with $7,500 of his own money saved for retirement, instead of a larger check to the IRS.

6. What to Check Right Now

- Holding more than one W-2 job? Run the IRS Tax Withholding Estimator and adjust each W-4 so the combined withholding reflects your total income.

- Have 1099 work? Set money aside as you go, and consider quarterly estimated payments instead of facing it all at filing time.

- Supporting a family member who lives with you — especially one with a disability? Check whether they qualify as a dependent, and whether that changes your filing status.

- No retirement plan at work? Look at whether a traditional IRA contribution fits before you file.

- Gather every W-2 and 1099 in one place before you start. A missing form is its own surprise.

EA Insight

The multiple-W-2 surprise is one I see every season. People come in bracing for a refund and leave with a balance due, and they assume they did something wrong. They didn’t. Four honest W-4s still produce under-withholding, because no single employer can see the whole picture. If you work several jobs, the fix is the withholding estimator — not a better accountant.

The second trap is the disabled-dependent assumption. Families hear “disabled dependent” and picture a large credit. For an adult, it’s the $500 Credit for Other Dependents. The real value usually comes somewhere else — the move to Head of Household, and the larger standard deduction that comes with it. Naming where the benefit actually sits keeps expectations honest.

One more thing on the IRA. A deduction isn’t the only way a contribution can help. Lowering adjusted gross income can also affect eligibility for credits that phase out by income — the Saver’s Credit is one worth checking at this income level. That’s why I look at IRA room as part of the return, not as an afterthought. The contribution can do more than one job, and it’s worth confirming whether it does in any given case.

EA Summary

Several jobs and a 1099 stacked together can produce a balance due — under-withheld W-2s plus self-employment tax. But a disabled sibling living at home opened the door to Head of Household, and a traditional IRA contribution made at filing time lowered the bill. Daniel’s return ended in a far better place than it started.

Frequently Asked Questions

I had several W-2 jobs. Why do I owe instead of getting a refund?

Each employer withholds based only on what it pays you, with no view of your other jobs. Because tax rates rise as income stacks up, the combined withholding from several jobs often falls short of the tax owed on the total. Adjusting each W-4 — or using the IRS Tax Withholding Estimator — closes that gap.

Can I claim an adult sibling with a disability as a dependent?

Often, yes. A brother or sister who is permanently and totally disabled can be a qualifying child with no age limit, as long as they live with you more than half the year and don’t provide more than half of their own support. They generally bring the $500 Credit for Other Dependents rather than the Child Tax Credit.

Can an IRA contribution lower last year’s taxes?

It can. The deadline to contribute for a tax year runs to the filing deadline, not December 31. A traditional IRA contribution made in the spring can be applied to the prior year and, if deductible, reduce that year’s taxable income. Just be sure the contribution is designated for the correct year.

Is there an extra credit for contributing to an IRA?

There can be. The Saver’s Credit (Retirement Savings Contributions Credit, Form 8880) rewards retirement contributions for taxpayers under certain income limits. Whether it applies depends on filing status, income, and other factors, so it’s worth checking with your tax professional rather than assuming either way.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.