What Are Tax Deductions for Content Creators?

Earn money from a blog, YouTube channel, podcast, or any platform where you create content, and the IRS sees a self-employed business owner — from the very first dollar, whether or not you receive a 1099. The good news is that legitimate business expenses are deductible. The bad news is that no deduction survives without records.

Key Takeaways

- Creator income is self-employment income from the first dollar — Schedule C reporting applies whether you receive a 1099 or not.

- If your activity is classified as a hobby under IRC §183, expense deductions drop to zero. Proving business intent is the first hurdle.

- Cameras, computers, microphones, and similar equipment can be expensed in year one through Section 179 or 100% Bonus Depreciation.

- Clothing, personal grooming, and items you’d wear in everyday life are almost always denied — even if you wear them on camera.

- Vehicle, meal, and travel expenses fall under IRC §274(d). Without contemporaneous records, the IRS rejects them entirely on audit.

- Free products (PR boxes) count as income at fair market value — receiving them isn’t free in tax terms.

Table of Contents

- 1. Who Counts as a “Content Creator” for Tax Purposes?

- 2. Hobby vs. Business — The First Test (IRC §183)

- 3. Major Deduction Categories

- 4. Equipment Deductions: Section 179 vs. Bonus Depreciation

- 5. Common Gray Areas — What Gets Denied

- 6. Recordkeeping Requirements (IRC §274(d))

- 7. How to Report on Schedule C

- 8. EA Insight

- 9. Frequently Asked Questions

- 10. Related Articles

- 11. Official Resources

1. Who Counts as a “Content Creator” for Tax Purposes?

Bloggers, YouTubers, Instagram and TikTok influencers, podcasters, Twitch streamers, Substack writers — the IRS treats them all the same way. Self-employed.

The income channels look different. AdSense, YouTube Partner Program, sponsorships, affiliate commissions, digital products, Patreon and Substack memberships, tips, merchandise. Channel type doesn’t matter for tax purposes. Two things do: are you trying to make money, and are you doing this regularly?

Most creators start as Sole Proprietors and report on Schedule C. LLC and S-Corp structures only start making sense at higher revenue levels and sit outside the scope of this article.

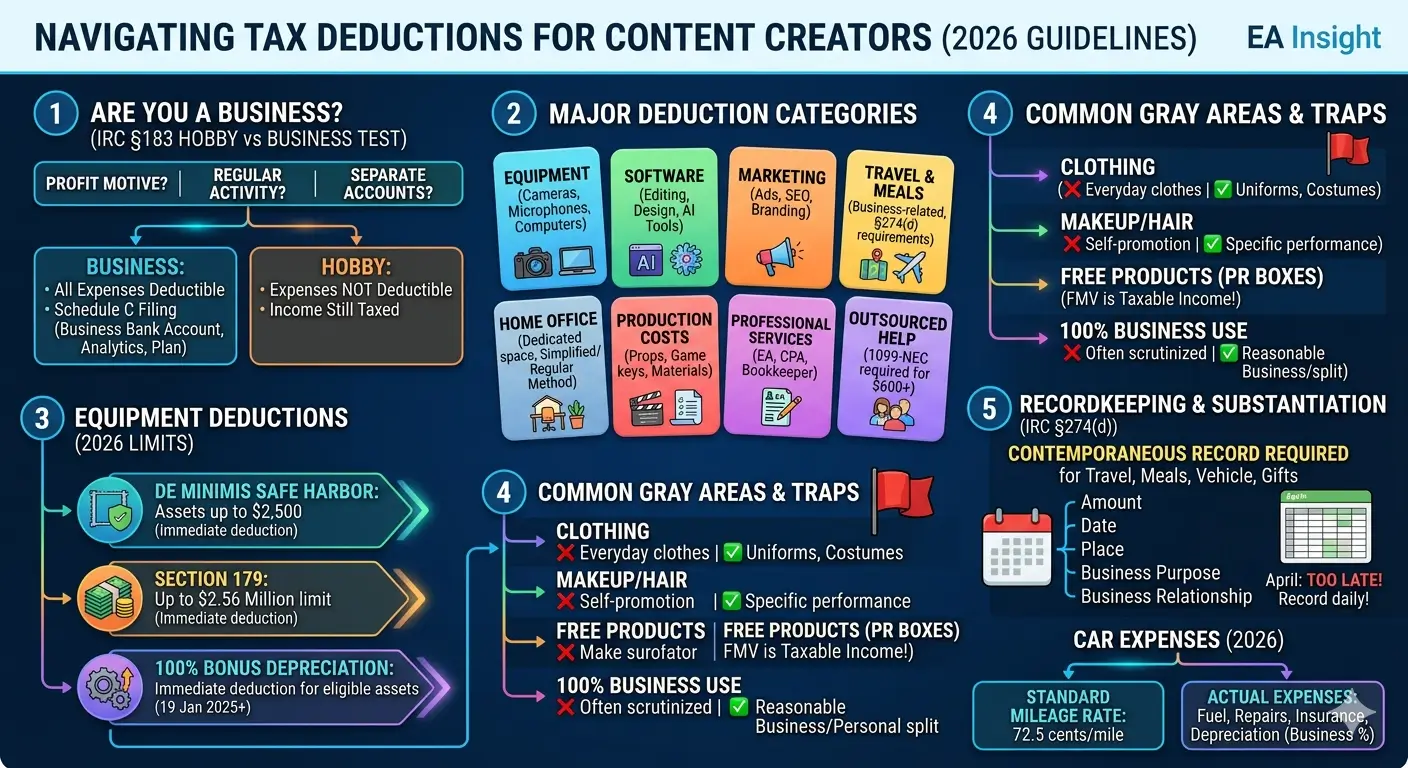

2. Hobby vs. Business — The First Test (IRC §183)

This is the test you have to pass before any other deduction matters. Fail it, and everything else in this article becomes irrelevant.

IRC §183 is known as the Hobby Loss Rule. Under current law, if your activity is classified as a hobby, expense deductions drop to zero. Income still gets taxed. Expenses can’t offset it. Worst-case scenario, all in one ruling.

The IRS uses nine factors from Treas. Reg. §1.183-2 to make the call. The simplified version:

- Do you operate it like a business — separate accounts, books, and records?

- Are you putting in real time and effort?

- Do you have the expertise, or are you actively learning?

- Are you making genuine attempts to monetize?

- Are losses a normal startup phase, or a long-running pattern?

Show a profit in three out of five years and the IRS presumes you’re running a business — the “presumption of profit.” You don’t need profit in year one. What you do need is documentation: a written plan, a separate business bank account, marketing records, traffic and revenue analytics.

Bottom line: Open a separate business bank account the day you start the channel. It’s the single most powerful action you can take to defeat a hobby classification in year one.

3. Major Deduction Categories

Most creator deductions fall into ten categories. Each one maps to a specific Schedule C line.

| Category | Examples |

|---|---|

| Equipment | Cameras, lenses, microphones, lighting, tripods, computers, monitors, drives |

| Software & Subscriptions | Adobe Creative Cloud, Canva, hosting, domains, SEO tools, AI tools, email marketing |

| Home Office | Simplified ($5/sq ft, 300 sq ft cap) or actual-expense method |

| Internet & Phone | Business-use percentage only |

| Education & Research | Online courses, conferences, business books, industry subscriptions |

| Marketing & Advertising | Paid ads, SEO platforms, designers, sponsored content production |

| Travel & Meals | Business travel (full), meals (50% limit applies) |

| Professional Services | EA, CPA, attorney, bookkeeper fees |

| Direct Production | Ingredients (food creators), props, games (review channels), entry fees |

| Outsourced Help | Editors, VAs, thumbnail designers — Form 1099-NEC required at $600+ per recipient |

The next three sections drill into the categories where creators most often go wrong: equipment treatment, gray-area expenses, and recordkeeping.

4. Equipment Deductions: Section 179 vs. Bonus Depreciation

Equipment is usually the largest single deduction in a creator’s first year. The default rule says you depreciate items used for more than a year over a multi-year recovery period. Current law gives you three faster paths.

De Minimis Safe Harbor

Items costing $2,500 or less can be expensed immediately when you elect the de minimis safe harbor on your return. Most microphones, small lights, gimbals, and accessories fit here.

Section 179

Lets you deduct the full cost of qualifying equipment in the year placed in service. The current limit ($2.56 million) sits far above what any individual creator will reach. One catch — Section 179 can’t create a business loss. Your deduction is capped at your business income.

Bonus Depreciation

Currently 100% under existing law. Unlike Section 179, Bonus Depreciation can create a loss, which makes it useful for new creators with large first-year purchases and limited revenue.

Practical point: A $4,000 camera bought in year one? You can deduct the full amount that year through Bonus Depreciation, instead of spreading it over five. Two conditions apply — business use must exceed 50%, and you have to document that percentage.

Computers and phones used to fall under “listed property” with stricter recordkeeping rules. They’ve since been reclassified, but business-use percentage records are still required. A 100% business-use claim on a personal computer or phone draws audit attention every time.

5. Common Gray Areas — What Gets Denied

Clothing — The Pevsner Rule

The most famous trap. Pevsner v. Commissioner set the standard: if you can wear it in everyday life, you can’t deduct it — regardless of whether you actually wear it outside work. Required for the job and unsuitable for ordinary use is the test.

- A fashion blogger’s “review” designer clothing — wearable in daily life. Denied.

- Suits worn for on-camera work — wearable in daily life. Denied.

- Branded uniforms, costumes, theatrical wardrobe — qualifies.

Personal Grooming for the Camera

Makeup, hair styling, and manicures done before filming — denied almost every time. The IRS sees no clean line between professional appearance and personal grooming.

Free Products and PR Boxes

The deduction trap creators miss most often. Receiving a free product isn’t free for tax purposes — you owe income tax on its fair market value (IRS Pub 525). Unreported PR-box value adds up fast, and an IRS examiner reading your channel can see the haul videos. That gap becomes a hobby-classification flag.

Important: Free isn’t free. Track every PR box, branded gift, and complimentary service at fair market value, and report the total as income on Schedule C.

100% Business-Use Claims

Possible? Technically. Defensible on audit? Rarely. A reasonable percentage — 70 to 80 percent on a primary editing computer, 60 to 70 on a personal-business phone — holds up far better than a 100% claim that requires you to prove you never once used the device for personal email.

6. Recordkeeping Requirements (IRC §274(d))

This is the section that decides whether your deductions actually survive on paper.

General business expenses need to meet two tests — ordinary and necessary, plus reasonable substantiation. Four expense categories face a higher bar: vehicle, meals, travel, and gifts. IRC §274(d) requires what tax law calls a contemporaneous record — written at or near the time of the expense, not reconstructed from memory in April.

For each entry, you need five elements:

| Required Element | Example |

|---|---|

| Amount | $47.32 |

| Date | March 14 |

| Place | Restaurant name and city |

| Business Purpose | Sponsorship discussion with brand contact |

| Business Relationship | Brand partner / advertiser |

Estimating mileage in April? The IRS rejects it on audit. Every time.

Vehicle Expenses — Two Methods

You can use the IRS standard mileage rate (currently 72.5 cents per mile for business use) or actual expenses — fuel, insurance, repairs, depreciation, all multiplied by your business-use percentage. One important catch: if you don’t choose the standard mileage rate in the first year a vehicle is in service for the business, you can never use it for that vehicle. Only actual expenses, for the life of that car.

Practical point: Turn on a mileage-tracking app on day one. Move all business spending to a separate business card so receipts auto-categorize. The systems you build when revenue is small are the only systems that scale to year three.

7. How to Report on Schedule C

All creator income lands on the same line — Schedule C, Gross Receipts. That includes:

- Form 1099-NEC (sponsorships, direct payments)

- Form 1099-K (PayPal, Stripe, Patreon — gross figure, before fees)

- Form 1099-MISC (royalties, prizes)

- Form 1099-DA (digital asset payments)

- Cash, foreign payments, and any income that didn’t generate a form

Each expense category maps to a specific Schedule C line — Advertising (Line 8), Car and Truck (Line 9), Office Expense (Line 18), Supplies (Line 22), Travel (Line 24a), Meals at 50% (Line 24b), Utilities (Line 25). Home office runs through Form 8829 and lands on Line 30.

Net profit then carries Self-Employment Tax of 15.3% on top of regular income tax. That calculation runs through Schedule SE. This is where most W-2 employees moving into creator work get blindsided.

The 25–30% Rule Every New Creator Needs

Set aside 25 to 30 percent of every payment the moment it arrives. Federal income tax plus 15.3% SE tax plus state tax adds up to that range fast, even in modest brackets. Open a second account labeled “tax savings” alongside your business operating account. Move the percentage over the same day a deposit hits. The creators who run into trouble in April are the ones who skipped this step. Every year.

Quarterly Estimated Tax payments start the year you have self-employment income. Miss them and the IRS adds underpayment penalties on top of the tax owed.

EA Insight

I run eataxwise.com myself, alongside a YouTube channel at @EATaxWise. So when I write about creator deductions, I’m describing my own books too — hosting fees, Yoast Premium for SEO, Pictory for video production, Vrew for shorts, Canva Pro for graphics, AI tools I use for research, CE materials I read for both EA continuing education and source content, and the home office where all of this happens. Each item runs through a separate business card and gets categorized the same week. Not because the IRS forced me to. Because the documentation rules I teach in this article are the rules I follow in my own bookkeeping.

Three mistakes I see new creators make again and again. First, they skip the hobby-vs-business question entirely — no separate account, no marketing records, no business plan. When year-one losses hit and the IRS classifies the activity as a hobby, every deduction disappears. Second, the “exclusive use” requirement on the home office gets violated. People work from a kitchen table and claim the simplified method. The IRS asks whether anyone else used that space. If the family eats dinner there, the deduction fails. Third, vehicle expenses get reconstructed in April. “I drove maybe 5,000 miles for the business last year.” That answer violates §274(d), and on audit it gets denied at 100%.

One platform, one revenue stream — bookkeeping is easy. Year three is different. AdSense, affiliate programs, sponsorships, digital products, memberships. Five revenue channels, with 1099-NEC, 1099-K, and 1099-MISC arriving simultaneously. The most common error at that stage is reporting the gross 1099-K figure without subtracting the platform fees PayPal or Stripe took out before payout. Misreport that, and your income looks higher than it was, your SE tax goes up with it, and you’ve overpaid for no reason. The systems you don’t build in year one are nearly impossible to retrofit in year three.

Frequently Asked Questions

I didn’t receive a 1099. Do I still have to report the income?

Yes. The 1099 is a reporting tool for the payer, not a trigger for your obligation. All self-employment income is taxable from the first dollar, whether or not a form arrives.

My channel had a loss in year one. Will the IRS automatically classify it as a hobby?

No. A first-year loss is normal for any startup. The IRS only raises hobby concerns when losses persist for three to five years without clear business activity. What matters is documentation — separate accounts, marketing records, a written plan, and visible attempts at monetization.

Should I use the simplified or actual home office method?

Simplified is faster and audit-friendlier — $5 per square foot, capped at 300 square feet ($1,500 max). The actual-expense method can produce a larger deduction if you have substantial home costs and a higher business-use percentage, but it requires detailed records on utilities, insurance, depreciation, and home value. Run both calculations the first year, then pick the better one.

Do I have to report free products I receive from brands?

Yes. Per IRS Pub 525, free products received in exchange for content count as taxable income at fair market value. Track them with the same care you track cash payments.

Can I deduct my computer at 100% if I tell the IRS it’s only for the business?

Possible, but rarely defensible on audit. The IRS expects a reasonable business-use percentage backed by records. Most creators land between 70% and 90%. A flat 100% claim invites questions you’d rather not answer.

Is clothing really never deductible for content creators?

Almost never. Under Pevsner v. Commissioner, clothing must be both required for the work and unsuitable for ordinary wear. Branded uniforms, costumes, and theatrical wardrobe qualify. Designer outfits worn on camera, even when bought specifically for content, do not.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.