What Are Tax Brackets? Rates, Thresholds & How They Work

The IRS doesn’t tax all your income at one rate. The U.S. uses seven federal income tax brackets — each applied only to the portion of your income that falls within that range. Your “tax bracket” is not what you actually pay.

Key Takeaways

- The U.S. has seven federal income tax rates: 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

- Tax brackets are marginal — only the income within each range is taxed at that bracket’s rate, not your entire income.

- Your marginal tax rate (highest bracket) is always higher than your effective tax rate (actual average rate paid).

- Filing status (Single, Married Filing Jointly, Head of Household, etc.) determines which set of income thresholds applies to you.

- The IRS adjusts bracket thresholds annually for inflation to prevent “bracket creep.”

- Strategies like retirement contributions and deductions can keep more of your income in lower brackets.

- Tax brackets apply only to taxable income — your gross income minus deductions, not your total paycheck.

Table of Contents

- 1. What Are Tax Brackets?

- 2. How the Progressive (Marginal) Tax System Works

- 3. Federal Income Tax Brackets by Filing Status

- 4. Step-by-Step Example: How Tax Is Calculated Across Brackets

- 5. Marginal vs. Effective Tax Rate

- 6. How Filing Status Changes Your Brackets

- 7. Common Misconceptions About Tax Brackets

- 8. How to Keep More Income in Lower Brackets

- 9. EA Insight

- 10. People Also Ask

1. What Are Tax Brackets?

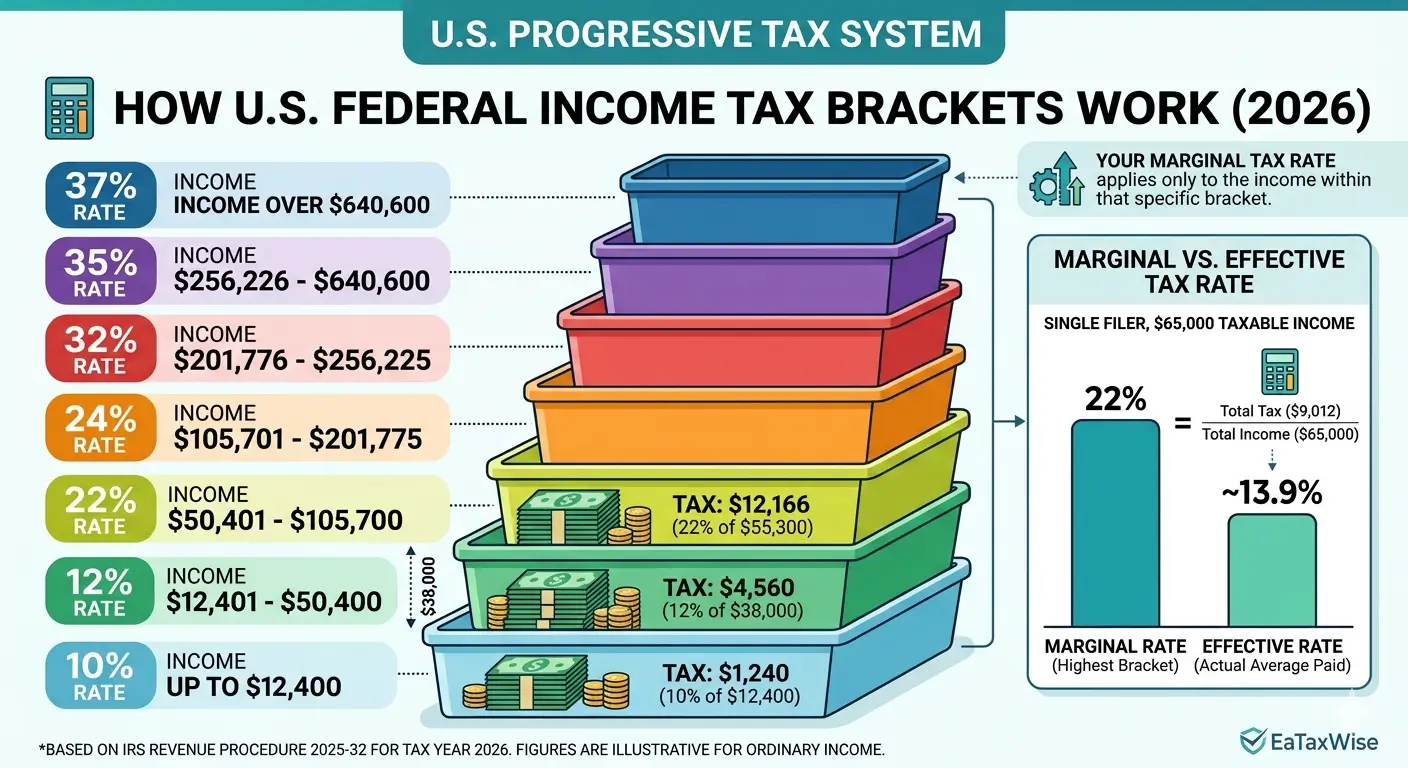

Tax brackets are ranges of taxable income, each assigned a specific federal income tax rate. The United States uses seven brackets with rates of 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

Think of tax brackets like a staircase. As your taxable income climbs each step, only the income on that particular step is taxed at the corresponding rate. The income on the steps below continues to be taxed at the lower rates.

This is the core idea behind the U.S. progressive tax system: higher income is taxed at higher rates, but lower portions of income are always protected at lower rates. No matter how much you earn, your first dollars of taxable income are taxed at just 10%.

The income thresholds — the exact dollar amounts where each bracket starts and ends — vary depending on your filing status (Single, Married Filing Jointly, Head of Household, or Married Filing Separately). The IRS adjusts these thresholds each year for inflation through an index called the Chained Consumer Price Index (C-CPI-U).

Tax Brackets — Quick Definition

Ranges of taxable income taxed at progressively higher rates.

Only the income within each range is taxed at that bracket’s rate — not your entire income.

2. How the Progressive (Marginal) Tax System Works

The word “marginal” is key to understanding how U.S. income taxes actually work. When someone says, “I’m in the 22% tax bracket,” they do not mean all their income is taxed at 22%. It means only the portion of their income that falls within the 22% bracket is taxed at that rate.

Here’s how it works in practice: your taxable income gets divided into layers, like slices of a cake. The bottom slice is taxed at 10%, the next slice at 12%, the next at 22%, and so on. Only the very top slice — the income that pushes into your highest bracket — is taxed at your marginal rate.

This is why moving into a higher tax bracket never causes you to take home less money overall. A raise that pushes you into the next bracket only means the additional income above the previous bracket’s threshold is taxed at the higher rate. Every dollar below that threshold continues to be taxed at the same, lower rates as before.

3. Federal Income Tax Brackets by Filing Status

The tables below show the current federal income tax brackets for each filing status. These amounts reflect the most recent IRS inflation adjustments published in Revenue Procedure 2025-32. Bracket thresholds are updated annually — always confirm the latest figures at IRS.gov before making tax decisions.

Single Filers

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | Up to $12,400 |

| 12% | $12,401 – $50,400 |

| 22% | $50,401 – $105,700 |

| 24% | $105,701 – $201,775 |

| 32% | $201,776 – $256,225 |

| 35% | $256,226 – $640,600 |

| 37% | Over $640,600 |

Married Filing Jointly

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | Up to $24,800 |

| 12% | $24,801 – $100,800 |

| 22% | $100,801 – $211,400 |

| 24% | $211,401 – $403,550 |

| 32% | $403,551 – $512,450 |

| 35% | $512,451 – $768,700 |

| 37% | Over $768,700 |

Head of Household

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | Up to $17,700 |

| 12% | $17,701 – $67,450 |

| 22% | $67,451 – $105,700 |

| 24% | $105,701 – $201,750 |

| 32% | $201,751 – $250,500 |

| 35% | $250,501 – $626,350 |

| 37% | Over $626,350 |

Married Filing Separately

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | Up to $12,400 |

| 12% | $12,401 – $50,400 |

| 22% | $50,401 – $105,700 |

| 24% | $105,701 – $201,775 |

| 32% | $201,776 – $256,225 |

| 35% | $256,226 – $384,350 |

| 37% | Over $384,350 |

Source: IRS Revenue Procedure 2025-32 (tax year 2026 inflation adjustments, filed in 2027). These figures apply to taxable income — your income after subtracting the standard deduction or itemized deductions.

4. Step-by-Step Example: How Tax Is Calculated Across Brackets

Let’s walk through a concrete example to see how tax brackets work in practice. Suppose you’re a single filer with a taxable income of $65,000 (that’s your gross income minus the standard deduction of $16,100).

Your federal income tax is calculated layer by layer:

| Bracket | Income in This Bracket | Tax Owed |

|---|---|---|

| 10% on first $12,400 | $12,400 | $1,240 |

| 12% on $12,401 – $50,400 | $38,000 | $4,560 |

| 22% on $50,401 – $65,000 | $14,600 | $3,212 |

| Total Federal Income Tax | $9,012 | |

Even though this person is “in the 22% bracket,” they don’t pay 22% on all $65,000. Their actual federal income tax of $9,012 represents an effective tax rate of about 13.9% — significantly lower than the 22% marginal rate.

5. Marginal vs. Effective Tax Rate

These two terms describe very different things, and confusing them is one of the most common mistakes taxpayers make.

Your marginal tax rate is the rate applied to your last dollar of taxable income — your highest bracket. In the example above, the marginal rate is 22%.

Your effective tax rate is your total tax divided by your total taxable income. It reflects the blended, average rate you actually pay across all brackets. In the example above, the effective rate is approximately 13.9%.

Why This Matters

Marginal rate → Use this when deciding whether to earn or defer additional income. If you receive a $5,000 bonus and your marginal rate is 22%, that bonus will be taxed at 22%. This rate also determines the real value of deductions and retirement contributions.

Effective rate → Use this to understand your overall tax burden. It’s the better measure for comparing your tax situation year over year or calculating what percentage of your total income goes to federal taxes.

6. How Filing Status Changes Your Brackets

The same income can result in different tax amounts depending on your filing status. This is because each status has its own set of bracket thresholds.

Married Filing Jointly (MFJ) generally offers the widest brackets. For most bracket levels, the MFJ thresholds are exactly double the Single thresholds. This means a married couple can earn twice as much as a single filer before hitting the same marginal rate. However, at the very top (37%), the MFJ threshold is not quite double the single threshold — which can create what’s known as a “marriage penalty” for some high-income couples.

Head of Household (HoH) offers wider brackets than Single status, especially in the lower and middle ranges. This is a meaningful benefit for unmarried taxpayers who are supporting dependents. For example, the 12% bracket for Head of Household extends to $67,450 in taxable income, compared to just $50,400 for a Single filer — a difference of $17,050 taxed at 12% instead of 22%.

Married Filing Separately (MFS) generally uses the same thresholds as Single filers and may also disqualify you from certain credits and deductions. Most married couples save money by filing jointly, though there are situations where separate filing makes sense (such as when one spouse has significant medical expenses or student loan repayment considerations).

Your filing status also determines your standard deduction amount, which directly affects how much of your income is taxable before brackets are applied.

7. Common Misconceptions About Tax Brackets

“If I get a raise into a higher bracket, I’ll take home less money.”

This is the most widespread tax myth in America — and it’s completely false. Only the income above the new bracket threshold is taxed at the higher rate. The rest of your income stays taxed at the same lower rates. A raise always increases your after-tax income.

“My tax bracket is the rate I pay on all my income.”

Your tax bracket refers to your marginal rate — the rate on your last dollar of income. Your actual overall rate (effective rate) is always lower because the lower portions of your income are taxed at lower rates. If you’re in the 22% bracket, you do not pay 22% on all your income.

“Tax brackets only apply to wages and salary.”

Federal tax brackets apply to your total taxable income, which includes wages, salary, self-employment income, interest, ordinary dividends, rental income, and many other types of income. Long-term capital gains and qualified dividends, however, are taxed under a separate rate schedule with their own brackets (0%, 15%, and 20%).

“Tax brackets are the same every year.”

The seven tax rates have remained the same since the Tax Cuts and Jobs Act (TCJA), and the One Big Beautiful Bill Act (OBBBA) made these rates permanent. However, the income thresholds — the dollar amounts that define each bracket — are adjusted annually for inflation. This means the bracket ranges change each year, even though the rates themselves stay the same.

8. How to Keep More Income in Lower Brackets

You don’t lower your bracket itself — you lower your taxable income so that less of it reaches the higher brackets. Here are the most common strategies:

Maximize retirement contributions. Pre-tax contributions to a 401(k), 403(b), or traditional IRA reduce your taxable income directly. For example, if your taxable income is $55,000 and you contribute $5,000 to a traditional IRA, your taxable income drops to $50,000 — potentially keeping all of your income out of the 22% bracket.

Use the standard deduction or itemize — whichever is higher. The standard deduction reduces your taxable income by a fixed amount based on your filing status. If your qualifying expenses (mortgage interest, state taxes, charitable donations) exceed the standard deduction, itemizing saves you more.

Contribute to a Health Savings Account (HSA). If you have a qualifying high-deductible health plan, HSA contributions are tax-deductible and reduce your adjusted gross income.

Time your income strategically. If you’re near the edge of a bracket, deferring a year-end bonus or accelerating deductions into the current year can keep more of your income in a lower bracket.

EA Insight

In my experience, the biggest cost to taxpayers isn’t being in a high bracket — it’s not knowing which bracket they’re in. I’ve seen W-2 employees leave thousands of dollars on the table simply because they didn’t realize they were right at the edge of a bracket, where a relatively small retirement contribution or deduction could have kept a portion of their income taxed at a lower rate.

Understanding your marginal rate isn’t just a textbook concept — it’s the starting point for every smart tax decision you make during the year. Before you file, check which bracket your last dollar of income falls into. That number should guide your 401(k) contributions, your HSA decisions, and whether to bunch deductions.

If you remember one thing from this post: your tax bracket is not what you pay — it’s where you start planning.

People Also Ask

How do I find my tax bracket?

Start by calculating your taxable income: take your total gross income, subtract any adjustments (like retirement contributions), and then subtract either the standard deduction or your itemized deductions. Compare the resulting number to the bracket table for your filing status. The bracket your top dollar falls into is your marginal tax bracket.

Do tax brackets apply to Social Security benefits?

Tax brackets apply to all taxable income, which may include a portion of your Social Security benefits. Whether your benefits are taxable depends on your “combined income” (AGI + nontaxable interest + half of Social Security benefits). Up to 85% of benefits may be taxable for higher-income recipients.

Are state taxes based on the same brackets?

No. State income taxes have their own separate rates and brackets, which vary widely. Some states (like Florida and Texas) have no state income tax at all. Others (like New York and California) have their own progressive bracket systems that apply in addition to federal taxes.

What’s the difference between tax brackets and tax tables?

Tax brackets show the marginal rates and income ranges. Tax tables (found in the Form 1040 instructions) are pre-calculated lookup charts that show the exact tax owed for specific income amounts, eliminating the need to calculate each bracket manually. They produce the same result.

Do capital gains use the same brackets?

Long-term capital gains (from assets held over one year) and qualified dividends are taxed at preferential rates of 0%, 15%, or 20%, depending on your taxable income. Short-term capital gains (assets held one year or less) are taxed as ordinary income using the regular brackets shown above.

Related Articles

Official Resources

Updated: April 2026

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual situations vary. Always verify current figures at IRS.gov and consult a qualified tax professional (EA, CPA, or attorney) for advice specific to your situation.