What Is a Tax Refund?

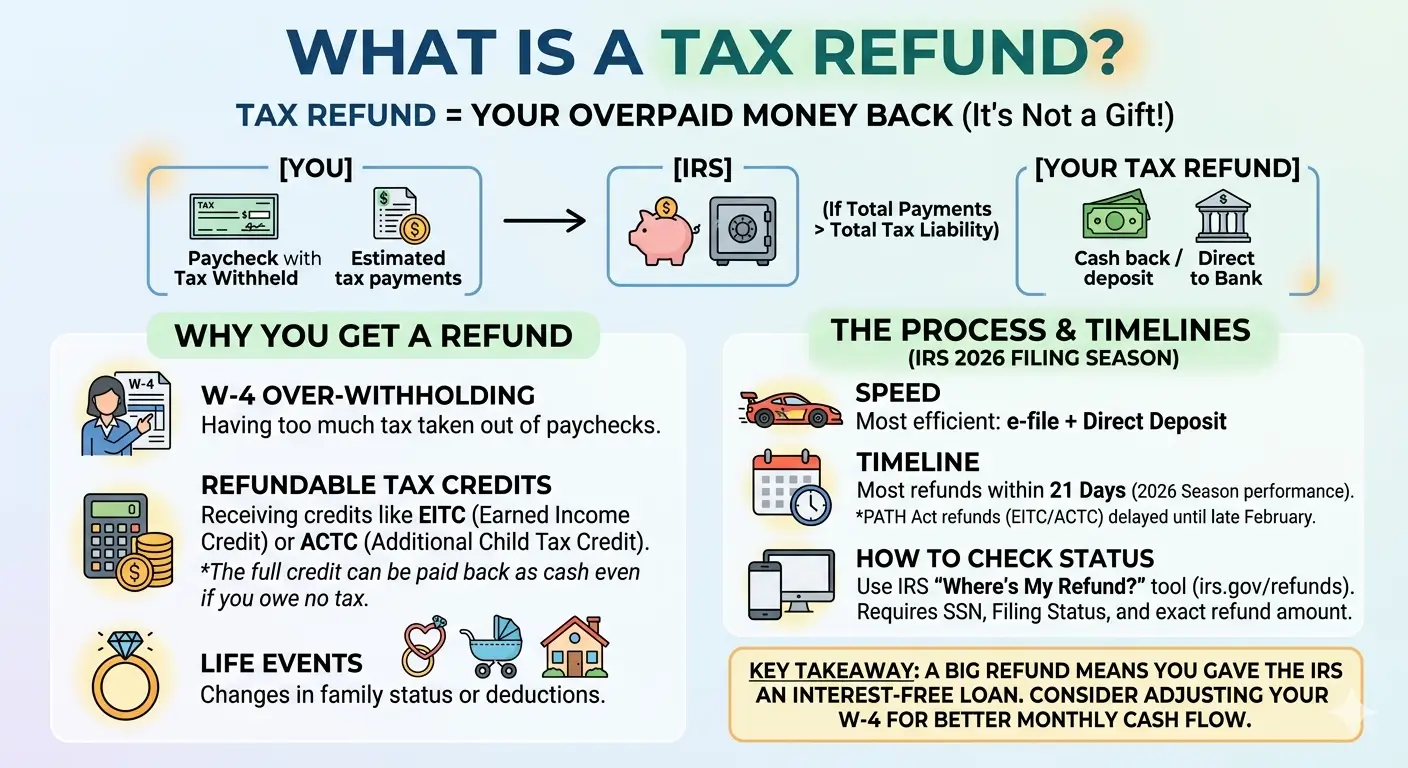

A tax refund is money the IRS returns to you when you’ve paid more tax than you actually owe. It’s not a bonus or a gift from the government — it’s your own money coming back. Understanding how refunds work helps you take control of your withholding, your cash flow, and your overall tax strategy.

Key Takeaways

- A tax refund is the amount the IRS returns when your total tax payments exceed your actual tax liability — it is not extra income.

- The most common cause of a refund is excess withholding from your paycheck through your W-2.

- Refundable credits — such as the Earned Income Credit and the Additional Child Tax Credit — can generate a refund even when your tax liability is zero.

- E-filing with direct deposit is the fastest combination — the IRS processes most refunds within 21 days.

- As of March 20, 2026, the average refund for the current filing season was approximately $3,571, up roughly 10.9% from the same point in the prior season (per IRS filing season statistics).

- A large refund is not always a sign of good tax planning — it may mean too much was withheld from your paycheck throughout the year.

Table of Contents

- 1. How a Tax Refund Works

- 2. What Causes a Tax Refund?

- 3. Refundable Credits vs. Nonrefundable Credits

- 4. How to Check Your Refund Status

- 5. How Long Does It Take?

- 6. What Can Reduce or Delay Your Refund?

- 7. Is a Big Refund Always a Good Thing?

- 8. EA Insight

- 9. Frequently Asked Questions

- 10. Related Articles

- 11. Official Resources

1. How a Tax Refund Works

A tax refund occurs when the total amount you paid in federal income tax during the year — through paycheck withholding, estimated tax payments, or refundable credits — exceeds your actual tax liability. The IRS returns the difference to you. In IRS terms (Publication 17), this difference is called an overpayment.

The formula is straightforward:

Refund = Total Payments − Tax Liability

If this number is positive, you receive a refund. If it is negative, you owe the IRS a balance due.

Here is how the process works step by step:

Step 1 — Tax is collected throughout the year. If you are a W-2 employee, federal income tax is withheld from every paycheck based on the information you provided on your Form W-4. If you are self-employed, you make quarterly estimated tax payments using Form 1040-ES.

Step 2 — You file your tax return. After the year ends, you calculate your actual income, apply deductions and credits, and determine your true tax liability on Form 1040.

Step 3 — The IRS compares. If your total payments (withholding plus estimated payments plus any refundable credits) are greater than your tax liability, the IRS issues the excess as a refund.

Here is a simple example:

| Item | Amount |

|---|---|

| Total federal income tax withheld (W-2, Box 2) | $8,500 |

| Actual federal income tax liability | $6,200 |

| Refund | $2,300 |

In this example, $8,500 was withheld from the taxpayer’s paychecks over the course of the year. After filing, the actual tax owed turned out to be $6,200. The IRS returns the $2,300 difference as a refund.

2. What Causes a Tax Refund?

Several factors can lead to a tax refund. The most common include:

Excess withholding through your W-4. If your W-4 is set conservatively — for example, if you did not claim dependents or additional deductions — more tax is withheld from each paycheck than necessary. The surplus comes back as a refund.

Refundable tax credits. Credits like the Earned Income Credit (EIC) and the Additional Child Tax Credit (ACTC) can reduce your tax below zero. The IRS pays the excess to you in cash, even if you had no tax liability at all.

Life changes that increase deductions. Getting married, having a child, buying a home, or paying tuition can all create new deductions or credits that lower your tax liability below what was withheld.

Income changes during the year. If you lost a job, switched to part-time work, or had lower income than expected, withholding based on your earlier earnings may have been too high relative to your actual annual income.

Nonrefundable tax credits. Credits like the base Child Tax Credit and the Lifetime Learning Credit can reduce your tax liability to zero — but not below zero. They won’t generate a cash refund on their own, but they can create or increase a refund by lowering the amount you owe below what was already withheld.

3. Refundable Credits vs. Nonrefundable Credits

The distinction between refundable and nonrefundable credits directly affects whether — and how much — you can receive as a refund. This is one of the most commonly misunderstood areas of the tax code.

| Feature | Refundable Credit | Nonrefundable Credit |

|---|---|---|

| Can reduce tax below $0? | Yes — excess is paid as cash | No — stops at $0 |

| If tax liability is $0? | Full credit paid as refund | No benefit |

| Examples | Earned Income Credit (EIC), Additional Child Tax Credit (ACTC) | Child Tax Credit (base), Lifetime Learning Credit, Saver’s Credit |

For example, if your tax liability is $500 and you qualify for a $2,000 refundable credit, the first $500 eliminates your tax and the remaining $1,500 is paid to you as a refund. With a nonrefundable credit, that same $500 would be reduced to $0, but the remaining $1,500 would simply be lost — it cannot be refunded.

4. How to Check Your Refund Status

The IRS provides the “Where’s My Refund?” tool as the official way to track your refund. It is available on the IRS website at irs.gov/refunds and through the IRS2Go mobile app (iOS and Android).

To use the tool, you need three pieces of information: your Social Security number (or ITIN), your filing status, and the exact whole-dollar refund amount shown on your return.

The tool displays one of three statuses:

- Return Received — The IRS has your return and is processing it.

- Refund Approved — The IRS has finished processing and approved your refund.

- Refund Sent — The refund has been sent to your bank or mailed.

You can check the status 24 hours after e-filing or four weeks after mailing a paper return. The tool updates once per day, typically overnight.

2026 update: The IRS has been phasing out paper refund checks and now prioritizes direct deposit as the default refund method. If your direct deposit information is missing or invalid, you may receive a CP53E notice asking you to update your banking details through your IRS Individual Online Account within 30 days. This does not mean your refund is denied — it means the refund is on hold until you provide valid account information.

5. How Long Does It Take?

| Filing Method | Estimated Processing Time |

|---|---|

| E-file + Direct Deposit | Within 21 days (most cases) |

| E-file + Paper Check | 21 days + additional 1–3 weeks |

| Paper Return | 6–8 weeks or longer |

| Amended Return (Form 1040-X) | Up to 16 weeks or longer |

| EITC / ACTC Claims | Held until after February 15 (PATH Act); actual deposits typically begin in late February |

The 21-day clock starts when the IRS accepts your return — not when you submit it. E-filed returns are typically accepted within 24 to 48 hours of submission.

If you claimed the Earned Income Tax Credit (EITC) or the Additional Child Tax Credit (ACTC), the PATH Act requires the IRS to hold your entire refund — not just the portion from those credits — until after February 15. In practice, most EITC/ACTC refunds reach bank accounts in late February or early March, not the day after the hold is lifted.

According to IRS data through March 20, 2026, over 80% of refunds were issued in fewer than 21 days, and over 98% of refunds were delivered via direct deposit.

6. What Can Reduce or Delay Your Refund?

Even if your return is accurate and complete, several factors can reduce or delay your refund:

Outstanding tax debt. If you owe back taxes from a prior year, the IRS will automatically apply part or all of your refund to that balance before issuing the remainder.

Other government debts. Through the Treasury Offset Program (TOP), your refund can be reduced to cover past-due child support, defaulted federal student loans, or certain state debts. If an offset occurs, the Bureau of the Fiscal Service (BFS) will send you a notice explaining the amount and the agency that received it.

Errors on your return. Mismatched Social Security numbers, incorrect income amounts, or math errors trigger manual review, which can add weeks to processing time.

Identity verification. If the IRS suspects identity theft or an unusual filing pattern, it may send a letter (such as Letter 5071C) requesting identity verification before releasing your refund.

Incomplete direct deposit information. If your banking information is missing or rejected, the IRS issues a CP53E notice and holds your refund until you update your account details online.

7. Is a Big Refund Always a Good Thing?

A large refund check might feel like a windfall, but from a financial planning perspective, it usually means too much tax was withheld from your paychecks throughout the year. That money sat with the IRS for up to 12 months — earning no interest for you.

Consider this: a $3,600 refund means approximately $300 per month was withheld beyond what you actually owed. That $300 could have gone toward savings, investments, debt repayment, or everyday expenses each month instead of waiting until the following spring to come back.

| Scenario | Monthly Impact | Annual Refund |

|---|---|---|

| Current (over-withheld) | −$300/month from paycheck | $3,600 refund |

| After W-4 adjustment | +$300/month in paycheck | ~$0 refund |

You can adjust your withholding by submitting an updated Form W-4 to your employer. The IRS Tax Withholding Estimator at irs.gov/W4App walks you through the calculation and tells you whether your current withholding is too high, too low, or about right.

That said, some people intentionally over-withhold as a form of forced savings. While this is not the most efficient strategy from an investment standpoint, it can work for those who find it difficult to save on their own. The key is to make the choice deliberately rather than by default.

EA Insight

One of the most common misconceptions I encounter is the belief that a large refund means you filed your taxes well. In reality, it means the opposite — you overpaid throughout the year, and the IRS held your money interest-free for up to 12 months.

If you received a refund of $3,000 or more, that translates to roughly $250 per month that could have been in your paycheck instead. Imagine putting that into a high-yield savings account or an index fund each month — by year’s end, you’d have both the principal and the growth.

On the other hand, the taxpayer whose refund is close to zero — or who owes a small balance — is typically the one whose withholding was set most accurately. Of course, you want to avoid the underpayment penalty. The safe harbor rule is straightforward: pay at least 100% of last year’s tax liability through withholding and estimated payments (110% if your AGI exceeded $150,000), or at least 90% of the current year’s tax. Meeting either threshold keeps you penalty-free.

If you received a large refund this year, take a few minutes to run the IRS Tax Withholding Estimator at irs.gov/W4App. Adjusting your W-4 now puts that money back in your pocket every month — where it belongs.

Frequently Asked Questions

What is the difference between a tax refund and a tax return?

A tax return is the form you file with the IRS (Form 1040). A tax refund is the money you receive back when you’ve overpaid your taxes. They are commonly confused, but they refer to completely different things.

Can I apply my refund to next year’s taxes instead of receiving it?

Yes. On your tax return, you can choose to apply all or part of your refund as an estimated tax payment for the following year. Once applied, this choice cannot be reversed, so make sure it aligns with your financial plan before selecting this option.

Is my federal tax refund taxable?

No. A federal tax refund is not taxable income because it is simply a return of your own overpayment. However, a state tax refund may be taxable on your federal return if you itemized deductions in the prior year and claimed a state tax deduction. The state will report this on Form 1099-G.

Why is my refund smaller than expected?

The IRS may have corrected a calculation error on your return, or your refund may have been reduced through the Treasury Offset Program to cover outstanding debts such as past-due child support, defaulted student loans, or prior-year tax balances. The IRS will send a notice explaining any adjustment.

Can I split my refund into multiple accounts?

Yes. By filing Form 8888, you can direct your refund into up to three different accounts — such as checking, savings, and investment accounts. This can be a useful tool for automatically allocating part of your refund toward savings goals.

Is there a deadline to claim a refund?

Yes. You generally have three years from the original filing deadline (without extensions) to claim a refund. After that window closes, the IRS is not required to issue the refund, and the money is forfeited to the U.S. Treasury.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.