What Is a Trump Account?

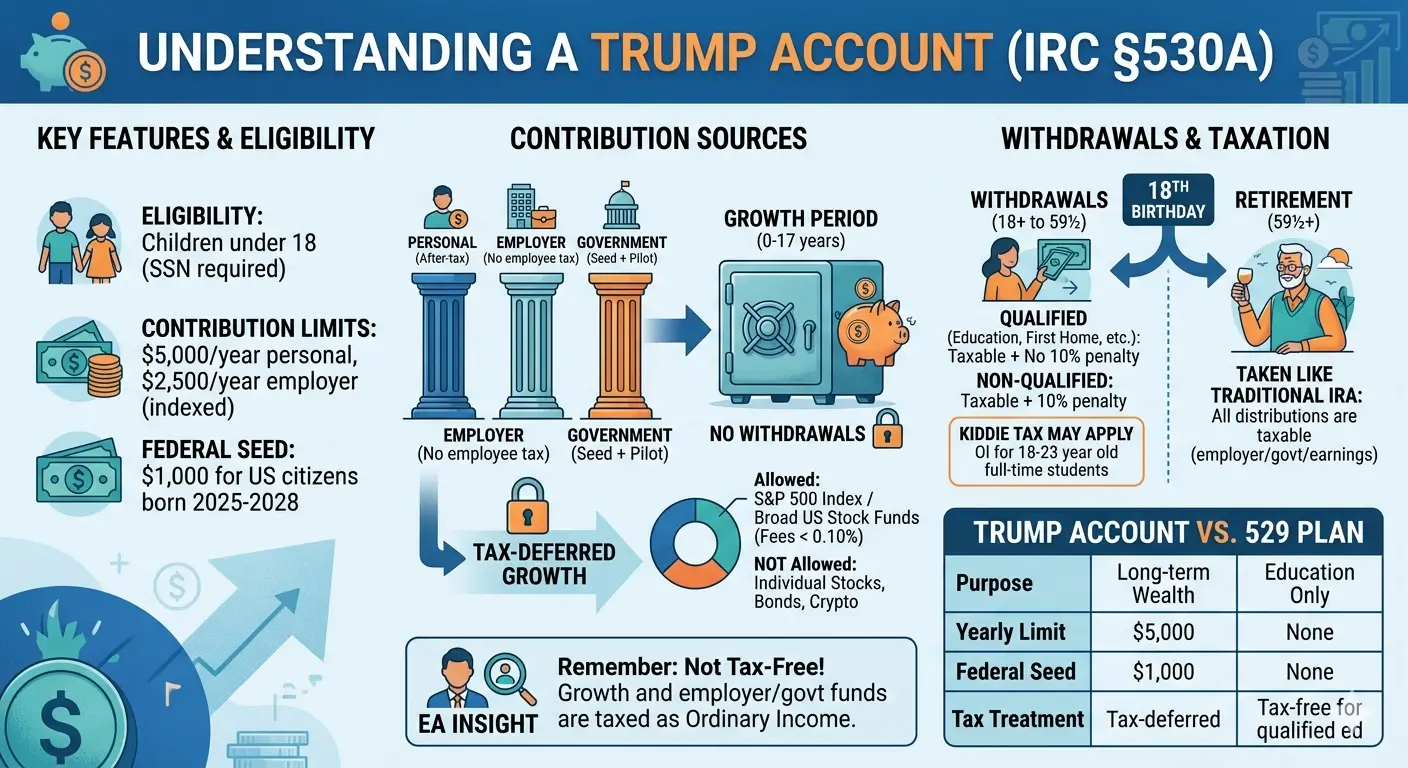

A Trump Account (IRC §530A) is a new type of tax-deferred investment account created under the One Big Beautiful Bill Act (OBBBA) for children under age 18. Starting July 4, 2026, families can open and fund these accounts — and eligible children born between 2025 and 2028 receive a $1,000 federal seed contribution.

Key Takeaways

- A Trump Account is a new type of IRA under IRC §530A, designed as a long-term investment account for children under 18 with a valid Social Security number.

- U.S. citizen children born between 2025 and 2028 are eligible for a one-time $1,000 pilot program contribution from the federal government.

- Individuals (parents, grandparents, others) may contribute up to $5,000 per year (indexed for inflation after 2027). Employers may contribute up to $2,500 per employee, counting toward the $5,000 annual limit.

- Investments are restricted to low-cost index funds or ETFs tracking the S&P 500 or other broad U.S. equity indices, with expense ratios capped at 0.10%.

- Withdrawals are prohibited during the growth period (from account opening through December 31 of the year the child turns 17). After the child turns 18, traditional IRA rules apply.

- Distributions of employer contributions, the government seed, earnings, and charitable contributions are taxed as ordinary income — not at capital gains rates. A 10% early withdrawal penalty may also apply before age 59½.

- Taxable withdrawals from a Trump Account are classified as unearned income, which may trigger the Kiddie Tax at the parent’s marginal rate.

Table of Contents

- 1. What Is a Trump Account?

- 2. Who Can Open a Trump Account?

- 3. How Contributions Work

- 4. What Can You Invest In?

- 5. The Growth Period and Withdrawal Rules

- 6. How Trump Accounts Are Taxed

- 7. Trump Account vs. 529 Plan

- 8. Connection to the Kiddie Tax

- 9. EA Insight

- 10. Frequently Asked Questions

- 11. Related Articles

- 12. Official Resources

1. What Is a Trump Account?

A Trump Account — formally known as a Section 530A Account — is a tax-deferred investment account for children under age 18, created by the One Big Beautiful Bill Act (OBBBA), which was signed into law on July 4, 2025. The IRS classifies it as a new type of Individual Retirement Account (IRA) under Internal Revenue Code §530A.

Several savings vehicles already exist for children, including 529 Plans, UGMA/UTMA custodial accounts, and Coverdell Education Savings Accounts. What sets the Trump Account apart is that it is not limited to education expenses. It is designed for long-term wealth building, functioning more like a retirement account than a college savings plan.

The account is opened in the child’s name, with a parent or legal guardian serving as the responsible party until the child turns 18. Once the child reaches age 18, the account converts to a traditional IRA, and the child assumes full control.

2. Who Can Open a Trump Account?

To open a Trump Account, all of the following requirements must be met:

Child eligibility: The child must not have reached age 18 before the end of the calendar year in which the election is made, and must have a valid Social Security number (SSN) issued before the election date.

Who can open it: Only a parent or legal guardian may open the account. Grandparents, other relatives, and friends cannot open an account — but they can contribute to one.

No income requirement: Unlike a traditional or Roth IRA, the child does not need earned income to receive contributions. This is one of the key differences between a Trump Account and other IRAs.

Citizenship requirement (for the $1,000 seed only): To receive the federal pilot program contribution, the child must be a U.S. citizen born between January 1, 2025, and December 31, 2028. However, opening a Trump Account itself only requires an SSN — U.S. citizenship is not required for the account.

One account per child: Only one Trump Account may exist per child at any time.

To open an account, a parent or guardian files IRS Form 4547 (Trump Account Election). This form can be submitted with the federal income tax return or filed separately. An online tool at trumpaccounts.gov is also expected to become available.

3. How Contributions Work

Trump Accounts can receive contributions from multiple sources. No contributions of any kind are permitted before July 4, 2026.

| Contribution Source | Annual Limit | Creates Basis? | Notes |

|---|---|---|---|

| Federal pilot contribution | $1,000 (one-time) | No | U.S. citizens born 2025–2028 only |

| Individuals (parents, grandparents, others) | Combined $5,000 | Yes | After-tax; not tax-deductible |

| Employer | Up to $2,500 per employee | No | Counts toward the $5,000 limit |

| Qualified charities / state governments | Separate | No | Does not count toward the $5,000 limit |

| Rollover (from another Trump Account) | Entire balance | Carries over | Trustee-to-trustee transfer only |

Employer contribution limit: The $2,500 limit applies per employee, not per child. If an employee has three children with Trump Accounts, the total employer contribution across all three accounts cannot exceed $2,500 for that employee. However, if both parents work for the same employer, each parent has a separate $2,500 limit, for a combined maximum of $5,000 from that employer.

Inflation adjustment: The $5,000 annual contribution limit remains fixed through 2027. Starting in 2028, it will be indexed for inflation.

Excess contributions: If contributions exceed the annual limit, the IRS may assess a 6% penalty each year until the excess is corrected.

Dell Family Contribution

In late 2025, Michael and Susan Dell announced a $6.25 billion donation to fund $250 contributions to the Trump Accounts of approximately 25 million children born between 2016 and 2024 who live in ZIP codes where the median household income is below $150,000. This charitable contribution does not count toward the $5,000 annual limit and does not create basis — meaning it will be fully taxable when withdrawn.

4. What Can You Invest In?

Investment options inside a Trump Account are strictly limited by law during the growth period:

- Allowed: Mutual funds or ETFs that track the S&P 500 or another broad-based index composed primarily of U.S. equities

- Expense ratio cap: Annual fund expenses must not exceed 0.10% (10 basis points)

- Not allowed: Sector-specific or industry-specific index funds, leveraged funds, individual stocks, bonds, cryptocurrency, real estate, or alternative investments

These restrictions are intentional. Because the account is designed for minors who have no control over investment decisions during the growth period, the law limits holdings to diversified, low-cost equity index funds — reducing both management costs and the risk of concentrated losses over a long time horizon.

After the child turns 18 and the account converts to a traditional IRA, standard IRA investment rules apply. At that point, the full range of IRA-eligible investments becomes available.

5. The Growth Period and Withdrawal Rules

The growth period begins on the date the Trump Account is established and ends on December 31 of the calendar year in which the child turns 17.

For example, a child born on October 1, 2026, would turn 17 on October 1, 2043. The growth period for that child’s account would end on December 31, 2043.

During the Growth Period: No Withdrawals

Distributions are generally prohibited during the growth period. There are only four exceptions:

- Rollover to another Trump Account — The entire balance may be transferred via a trustee-to-trustee rollover to a new Trump Account for the same child.

- ABLE Account rollover — The entire balance may be rolled over to an ABLE account for the child, but only during the calendar year in which the child turns 17.

- Return of excess contributions — Contributions that exceed the annual limit may be returned.

- Death of the account beneficiary — If the child passes away during the growth period, the account balance (minus basis) is included in the inheriting beneficiary’s gross income.

Hardship withdrawals are not permitted during the growth period under any circumstance.

After the Growth Period: Traditional IRA Rules Apply

Starting January 1 of the calendar year in which the child turns 18, the Trump Account is treated as a traditional IRA. This means:

- Withdrawals before age 59½ are generally subject to income tax plus a 10% early withdrawal penalty.

- Exceptions to the 10% penalty include distributions for qualified higher education expenses, first-time home purchases (up to $10,000), certain disaster relief, and costs related to birth or adoption.

- The account may be converted to a Roth IRA — but the taxable portion of the conversion is subject to income tax in the year of conversion.

- Required Minimum Distribution (RMD) rules apply at the appropriate age.

- The child has full control over the account once they turn 18.

6. How Trump Accounts Are Taxed

The tax treatment of a Trump Account depends entirely on who contributed the money. This is one of the most commonly misunderstood aspects of the account.

The key concept here is basis. When an individual (such as a parent or grandparent) contributes to a Trump Account, that money has already been taxed as part of the contributor’s income. This after-tax amount is called the basis — and because it was already taxed once, it is not taxed again when withdrawn. However, not all contribution sources create basis.

| Source | At Contribution | During Growth Period | At Withdrawal |

|---|---|---|---|

| Individual contributions (parents, grandparents, etc.) | Not deductible (after-tax) | Tax-deferred | Basis: tax-free; earnings: taxed |

| Employer contributions | Not included in employee income | Tax-deferred | Fully taxable (no basis) |

| Federal $1,000 seed | — | Tax-deferred | Fully taxable (no basis) |

| Charitable / state contributions | — | Tax-deferred | Fully taxable (no basis) |

| Earnings (investment growth) | — | Tax-deferred | Fully taxable |

In short, only individual after-tax contributions create basis. Everything else — employer contributions, the government seed, charitable contributions, and all investment earnings — is taxed as ordinary income when withdrawn.

When a distribution is taken, the taxable and nontaxable portions are calculated using the pro rata rule. You cannot withdraw only the basis first and leave the taxable portion for later — each distribution is a proportional mix of both.

Important: Distributions from a Trump Account are taxed at ordinary income tax rates — not the lower long-term capital gains rates (0%, 15%, or 20%). After decades of compound growth, withdrawing a large lump sum can result in a significant tax bill.

7. Trump Account vs. 529 Plan

Both accounts offer tax advantages for saving on behalf of a child, but they serve different purposes and follow different rules.

| Feature | Trump Account | 529 Plan |

|---|---|---|

| Legal Basis | IRC §530A (OBBBA 2025) | IRC §529 |

| Purpose | Long-term wealth building (not limited to education) | Education savings |

| Annual Contribution Limit | $5,000 (federal) | No federal limit (state limits vary) |

| Government Seed | $1,000 (born 2025–2028) | None |

| Investment Options | Low-cost U.S. equity index funds only | Varies by plan; typically broader selection |

| Tax on Withdrawals | Earnings taxed as ordinary income | Tax-free for qualified education expenses |

| State Tax Benefits | None | Many states offer contribution deductions |

| Withdrawal Restrictions | No withdrawals before age 18 | Available anytime for qualified expenses |

| Control After Age 18 | Child takes full control | Account owner (parent) retains control |

| Roth IRA Rollover | Roth conversion available (taxable) | Up to $35,000 tax-free rollover after 15 years |

If saving for education is the primary goal, a 529 Plan generally offers stronger tax benefits. Qualified withdrawals from a 529 are completely tax-free at the federal level — and often at the state level as well. Trump Account withdrawals, by contrast, are taxed as ordinary income on the earnings portion.

A Trump Account is best understood as a complement to a 529 Plan — not a replacement. For families that have already maximized their 529 contributions or want a savings vehicle that is not restricted to education expenses, the Trump Account adds another option.

8. Connection to the Kiddie Tax

This is where Trump Accounts and tax planning intersect in a way that many families overlook. Taxable withdrawals from a Trump Account — including Roth IRA conversions — are classified as unearned income. And unearned income above a certain threshold can trigger the Kiddie Tax.

The Kiddie Tax applies when a child’s unearned income exceeds a set amount. Instead of being taxed at the child’s presumably lower rate, the excess is taxed at the parent’s marginal tax rate. The Kiddie Tax applies to:

- Children under age 19

- Full-time students ages 19 through 23 who do not provide more than half of their own financial support

This means that if a child turns 18 and immediately withdraws from a Trump Account or converts it to a Roth IRA, the taxable amount could be taxed at the parent’s rate — potentially as high as 37% — rather than the child’s own rate.

Planning Consideration

To minimize the Kiddie Tax impact, consider timing a Roth conversion after the child is no longer a full-time student and is age 24 or older — or in a year when the child’s own taxable income is low. Converting in smaller amounts over multiple years, rather than all at once, can also reduce the overall tax burden.

EA Insight

The Trump Account introduces a genuinely new savings option for children, but I am already seeing misconceptions that could lead to costly mistakes.

The most common misunderstanding is treating the account as tax-free. It is not. A Trump Account is tax-deferred, not tax-free. Investment earnings, employer contributions, and the government seed are all taxed as ordinary income when withdrawn. After decades of compound growth, that tax bill can be substantial — and it is taxed at ordinary income rates, not the more favorable capital gains rates.

The second mistake is choosing a Trump Account instead of a 529 Plan for education savings. If your goal is to fund college tuition, a 529 Plan almost always offers better tax treatment. Qualified 529 withdrawals are completely tax-free, while Trump Account withdrawals are not. The two accounts serve different purposes, and for most families the right approach is to use both — not to pick one over the other.

Third, rushing into a Roth conversion the moment the child turns 18 can trigger the Kiddie Tax. If the child is a full-time student, the Kiddie Tax may apply through age 23, meaning the taxable portion of the conversion could be taxed at the parent’s marginal rate. Waiting until the child is no longer a dependent student — or until a year when their own income is low — can significantly reduce the tax cost.

Finally, remember that the child takes full control of the account at age 18. Unlike a 529 Plan where the parent remains the account owner and controls distributions, a Trump Account belongs entirely to the child once the growth period ends. They can withdraw everything — penalties and taxes included. This is worth discussing with your family before funding the account.

One additional note: if you plan to make large personal contributions, gift tax reporting can come into play. The rules in this area have been shifting, so confirm the current treatment with a tax professional before funding a large amount.

Frequently Asked Questions

When can I open a Trump Account?

Accounts can be opened and contributions can begin starting July 4, 2026. You can file IRS Form 4547 with your tax return or separately, or use the online tool at trumpaccounts.gov once it becomes available.

Who is eligible for the $1,000 seed contribution?

Children who are U.S. citizens born between January 1, 2025, and December 31, 2028, are eligible for the one-time $1,000 pilot program contribution. A separate election must be made on Form 4547 to receive it.

Can I contribute if my child has no earned income?

Yes. Unlike traditional and Roth IRAs, Trump Accounts do not require the child to have earned income. Parents, grandparents, or anyone else can contribute up to $5,000 per year regardless of whether the child has any income.

Does a Trump Account affect my child’s Roth IRA contributions?

No. Contributions to a Trump Account during the growth period do not count toward any other IRA contribution limit. If your child has earned income, they can contribute to a Roth IRA separately.

What happens if my child passes away before age 18?

The account balance minus basis is included in the inheriting beneficiary’s gross income. If the beneficiary is the child’s estate, the amount is included in the child’s final tax return.

Can I move my child’s Trump Account to a different financial institution?

Yes. During the growth period, the entire balance may be transferred to a new Trump Account through a trustee-to-trustee rollover. Partial transfers are not permitted.

How can my child avoid the Kiddie Tax on a Roth conversion?

The Kiddie Tax applies to children under 19 and full-time students through age 23. Waiting to convert until the child is no longer a full-time student — or until age 24 or later — avoids the risk of being taxed at the parent’s rate. Converting in smaller amounts over several low-income years can also help reduce the tax impact.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. The IRS has not yet finalized all rules governing Trump Accounts, and additional guidance is expected. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.