What Is Unearned Income?

Money you receive without currently working for it — interest, dividends, rent, pensions, capital gains — is still subject to federal income tax. The IRS draws a clear line between income you earn through current labor and income you receive passively. Unearned income falls on the passive side of that line, and the tax rules that apply to it are different from those for wages and salaries.

Key Takeaways

- Unearned income is any income received without performing current work — including interest, dividends, capital gains, rental income, pensions, unemployment benefits, and Social Security.

- The IRS distinguishes earned income from unearned income, and each type follows different tax rules, credit eligibility, and reporting requirements.

- Unearned income is exempt from FICA taxes (Social Security and Medicare), but is subject to federal income tax.

- High-income taxpayers may owe an additional 3.8% Net Investment Income Tax (NIIT) on certain unearned income.

- A child’s unearned income above $2,700 may be taxed at the parent’s rate under the Kiddie Tax rules.

- Unearned income alone does not qualify you for IRA contributions, the Earned Income Credit, or Social Security work credits.

Table of Contents

- 1. What Is Unearned Income?

- 2. Earned Income vs. Unearned Income

- 3. Types of Unearned Income

- 4. How Is Unearned Income Taxed?

- 5. NIIT — The 3.8% Surtax on Investment Income

- 6. Kiddie Tax — When a Child’s Unearned Income Is Taxed at the Parent’s Rate

- 7. What You Cannot Get With Unearned Income Alone

- 8. EA Insight

- 9. Frequently Asked Questions

- 10. Related Articles

- 11. Official Resources

1. What Is Unearned Income?

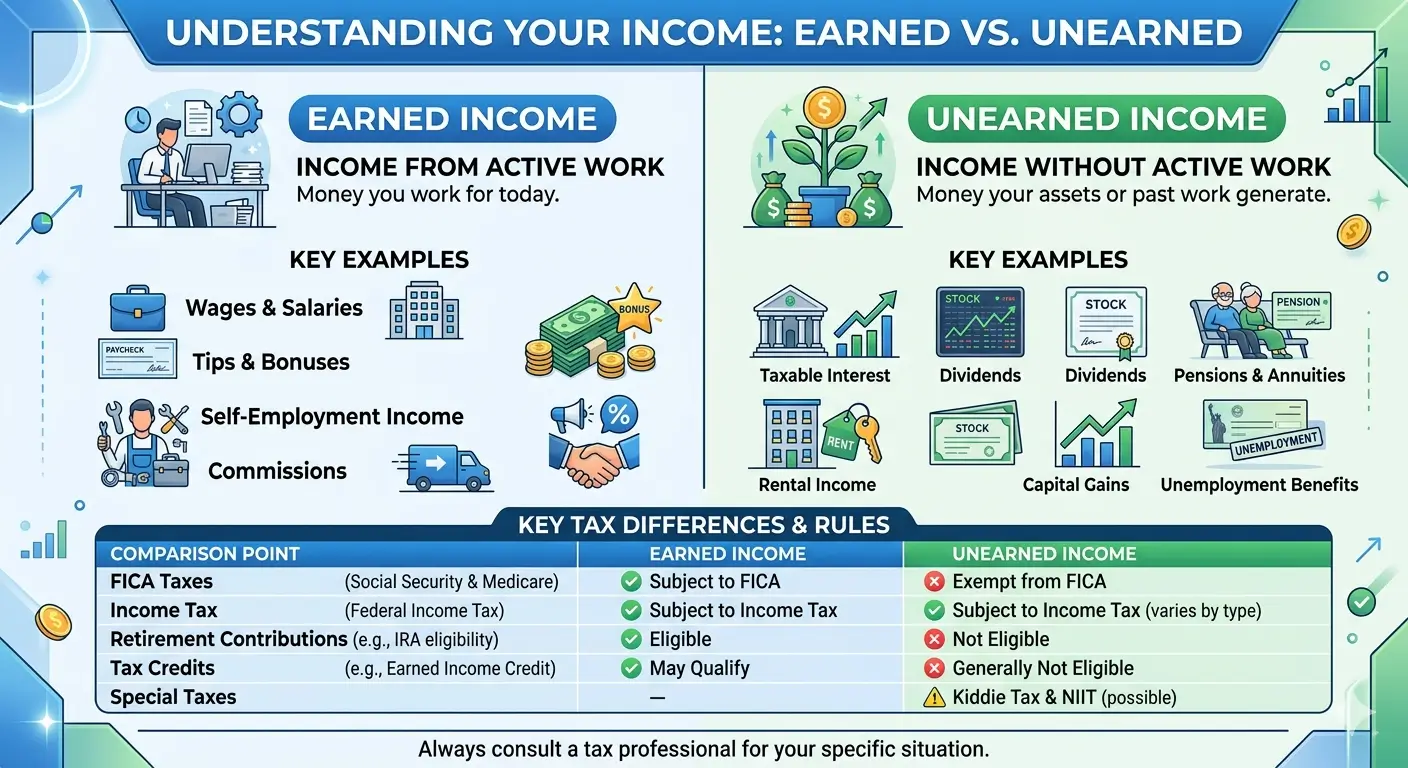

Unearned income is any income you receive without performing current work or services. The IRS defines it as income that is not attributable to wages, salaries, or compensation for personal services.

The test is straightforward: are you currently working for this money? If not, the IRS treats it as unearned income. This includes investment returns, retirement distributions, unemployment benefits, and many other types of passive receipts.

One point that surprises many people: pension payments are unearned income, even though you earned them through years of prior work. The IRS looks at whether you are currently performing services — not whether the income traces back to past employment. Since you are no longer working when you receive pension checks, the IRS classifies them as unearned.

A note on terminology: You may hear unearned income called “passive income” in everyday conversation. While the two overlap significantly, they are not identical under the tax code. Pension income is one case where the difference shows: it’s unearned, but not classified as “passive activity income” under IRC §469. For most taxpayers, the practical distinction matters mainly in rental income and business investment contexts.

2. Earned Income vs. Unearned Income

| Feature | Earned Income | Unearned Income |

|---|---|---|

| Definition | Compensation for current work or services | Income received without performing current work |

| Examples | Wages, tips, salaries, self-employment income, commissions | Interest, dividends, capital gains, rental income, pensions, unemployment |

| FICA Taxes | Yes (Social Security 6.2% + Medicare 1.45%) | No |

| NIIT (3.8%) | Does not apply | May apply for high-income taxpayers |

| EIC Eligibility | Qualifies | Does not qualify |

| IRA Contributions | Eligible | Not eligible |

This distinction matters beyond just tax rates. Earned income determines your eligibility for refundable credits like the Earned Income Credit, your ability to contribute to retirement accounts, and whether you accumulate Social Security work credits. Unearned income does none of these things.

3. Types of Unearned Income

Investment Income

Taxable interest comes from bank accounts, certificates of deposit, bonds, and similar instruments. If you earn $10 or more in interest during the year, the financial institution will issue Form 1099-INT.

Dividends are payments from stocks or mutual funds. Ordinary dividends are taxed at your regular income tax rate. Qualified dividends — those meeting specific holding period requirements — are taxed at the lower long-term capital gains rates of 0%, 15%, or 20%.

Capital gains arise when you sell an asset (stocks, real estate, cryptocurrency) for more than you paid. Short-term gains (assets held one year or less) are taxed at ordinary income rates. Long-term gains (assets held more than one year) receive preferential rates of 0%, 15%, or 20%, depending on your taxable income.

Rental income from investment properties is generally classified as unearned income. For most landlords who are not full-time real estate professionals, rental receipts are passive and unearned.

Retirement and Pension Income

Pension and annuity payments are distributions from employer-sponsored retirement plans or purchased annuity contracts. These are taxed at ordinary income rates.

Social Security benefits may be partially taxable depending on your income level. Based on your “combined income” (AGI + nontaxable interest + half of Social Security), anywhere from 0% to 85% of your benefits may be subject to federal income tax.

Distributions from IRAs and 401(k) plans are unearned income. Traditional account withdrawals are taxed at ordinary rates. Qualified distributions from Roth IRAs are tax-free.

Other Types

Unemployment compensation is fully taxable at the federal level. Many taxpayers are surprised to learn that unemployment benefits are not tax-free.

Cancellation of debt income occurs when a lender forgives part or all of a debt. The forgiven amount is generally taxable and reported on Form 1099-C.

Trust distributions — the taxable portion of income received from a trust — are unearned income to the beneficiary.

Alimony under divorce agreements executed on or before December 31, 2018, is included in the recipient’s income. For agreements executed after that date, alimony is not taxable to the recipient and not deductible by the payer.

Gambling winnings are fully taxable. Losses may be deducted only up to the amount of winnings. Under current federal tax law, the gambling loss deduction is limited to 90% of actual losses.

Items That Are Unearned but Not Taxable

Not all unearned income is subject to tax. The following are generally excluded from taxable income:

- Gifts — The recipient does not report a gift as income. The giver may have gift tax reporting obligations for gifts above $19,000 per recipient per year.

- Inheritances — Not subject to federal income tax (separate estate tax rules may apply).

- Municipal bond interest — Exempt from federal income tax.

- Qualified Roth IRA distributions — Tax-free if the account has been open for at least five years and the owner is 59½ or older.

- Life insurance death benefits — Generally not taxable to the beneficiary.

4. How Is Unearned Income Taxed?

Unearned income is not taxed at a single flat rate. The applicable rate depends on the type of income:

| Income Type | How It Is Taxed |

|---|---|

| Taxable interest | Ordinary income rates (10%–37%) |

| Ordinary dividends | Ordinary income rates (10%–37%) |

| Qualified dividends | Long-term capital gains rates (0% / 15% / 20%) |

| Short-term capital gains | Ordinary income rates (10%–37%) |

| Long-term capital gains | 0% / 15% / 20% |

| Rental income | Ordinary income rates (10%–37%) |

| Pensions / Annuities | Ordinary income rates (10%–37%) |

| Social Security benefits | 0% to 85% taxable, depending on combined income |

| Unemployment compensation | Ordinary income rates (10%–37%) |

One of the most significant tax differences between earned and unearned income is FICA. Earned income is subject to Social Security tax (6.2%) and Medicare tax (1.45%), totaling 7.65% for employees — or 15.3% for self-employed individuals. Unearned income is exempt from these payroll taxes entirely.

High-income taxpayers with significant investment income may also face the Net Investment Income Tax, which adds 3.8% on top of regular income tax.

5. NIIT — The 3.8% Surtax on Investment Income

The Net Investment Income Tax (NIIT) is a 3.8% surtax that applies to certain investment income when a taxpayer’s modified adjusted gross income (MAGI) exceeds specific thresholds. It is imposed on top of regular federal income tax — not instead of it.

| Filing Status | MAGI Threshold |

|---|---|

| Single / Head of Household | $200,000 |

| Married Filing Jointly | $250,000 |

| Married Filing Separately | $125,000 |

The NIIT is calculated as 3.8% of the lesser of your net investment income or the amount by which your MAGI exceeds the threshold for your filing status.

Income subject to NIIT: taxable interest, dividends, capital gains, rental income, royalties, and passive business income.

Income not subject to NIIT: wages, self-employment income, Social Security benefits, retirement account distributions, and tax-exempt municipal bond interest.

Important: These MAGI thresholds are not adjusted for inflation. They have remained unchanged since the NIIT was introduced in 2013. As wages and investment values rise over time, more taxpayers cross these fixed thresholds each year — even without any change in lifestyle or financial strategy. The NIIT is reported on Form 8960.

6. Kiddie Tax — When a Child’s Unearned Income Is Taxed at the Parent’s Rate

When a child receives unearned income above a certain threshold, the excess is taxed at the parent’s marginal tax rate rather than the child’s lower rate. This rule is commonly known as the Kiddie Tax.

For tax year 2026, the Kiddie Tax works as follows:

| Child’s Unearned Income | How It Is Taxed |

|---|---|

| First $1,350 | Tax-free |

| $1,351 – $2,700 | Taxed at the child’s own rate |

| Above $2,700 | Taxed at the parent’s marginal rate |

The Kiddie Tax applies to children who meet all of the following conditions:

- Under age 18 at the end of the tax year, or

- Age 18 with earned income that does not exceed half of their own support, or

- A full-time student aged 19–23 with earned income that does not exceed half of their own support

The Kiddie Tax is calculated on Form 8615. If the child’s income consists only of interest, dividends, and capital gain distributions totaling less than $13,500, the parent may choose to include the child’s income on the parent’s own return using Form 8814 instead of filing a separate return for the child. Note that this election covers interest, dividends, and capital gain distributions only — gains from a child selling individual stocks are reported on the child’s own return and cannot be pulled onto the parent’s return this way.

The flip side for older children: The Kiddie Tax applies only while a child can still be claimed as a dependent. Once a child is 19 or older and not a full-time student, a different rule takes over. If that child’s gross income — including dividends and capital gains — exceeds the qualifying relative limit (currently $5,200, a figure the IRS adjusts annually), the parents cannot claim them as a dependent at all, no matter how much support the parents provided. An adult child with $8,000 of investment income costs their parents the dependency claim — and the $500 Credit for Other Dependents that comes with it.

7. What You Cannot Get With Unearned Income Alone

Several important tax benefits require earned income. If your only income is unearned, you are not eligible for the following:

Earned Income Credit (EIC) — This refundable credit is specifically designed for low-to-moderate-income workers. You must have earned income to qualify. Unearned income such as investment returns or pension payments does not count.

IRA contributions — Both Traditional and Roth IRAs require earned income (compensation) to make contributions. Dividend income, rental receipts, or pension payments cannot be used as the basis for IRA contributions.

Social Security work credits — Eligibility for Social Security retirement benefits is based on work credits accumulated during your working years. Unearned income does not generate work credits.

Foreign Earned Income Exclusion (FEIE) — U.S. citizens living abroad may exclude up to $130,000 of foreign earned income from taxation. This exclusion does not apply to foreign dividends, rental income, or other unearned income earned overseas.

EA Insight

A retired couple once came to me certain they owed nothing — a $48,000 pension, $30,000 in Social Security, no job, no withholding set up anywhere. They walked out with a four-figure balance due. The pension was fully taxable at ordinary rates, and because of their combined income, 85% of the Social Security was taxable too. “Not working” had quietly become “underwithheld.” Unearned does not mean untaxed.

The case that catches families off guard most involves a young adult child. Parents planning to claim their 22-year-old — out of school, job hunting, no wages — assumed the $500 Credit for Other Dependents was theirs. Then we added up the child’s brokerage account: $3,000 in dividends and $5,000 in capital gains. That $8,000 sits above the $5,200 gross income limit for claiming an adult child, so the dependency claim vanished, and the $500 with it. They had paid every dollar of the child’s living costs that year, which felt like it should settle the matter. It doesn’t. The gross income test stands entirely on its own.

Two habits prevent both surprises. Retirees should set up withholding or estimated payments before the unearned income lands, not after the return is done. And any family with an investing adult child should total that child’s dividends and gains before assuming the dependency claim holds. One more thing for the child: if they sell stock and skip filing because the income seems small, the broker still reports the gross sale amount to the IRS — which can produce a notice treating the whole sale as gain. A short return filed on time costs far less than answering that letter later.

Frequently Asked Questions

Is bank interest taxable even if the amount is small?

Yes. All taxable interest is reportable on your federal return regardless of the amount. If you earn $10 or more, the bank will issue Form 1099-INT — but even amounts below $10 must be included in your income.

Does unearned income get hit with FICA taxes?

No. FICA taxes (Social Security and Medicare) apply only to earned income. High-income taxpayers may still owe the 3.8% NIIT on certain investment income, which is a separate tax from FICA.

Are stock dividends earned or unearned income?

Unearned. Holding stock is not considered performing current work or services, so dividend payments are classified as unearned income regardless of how actively you manage your portfolio.

Is rental income always unearned?

For most landlords, yes. If you qualify as a Real Estate Professional under IRS rules — meeting strict time and material participation requirements — rental income may be reclassified. This status requires spending more than 750 hours per year and more than half of your total working hours in real estate activities.

Do I have to file a tax return if I only have unearned income?

It depends on the amount, your age, and your filing status. If your unearned income exceeds the applicable filing threshold, you are required to file. The IRS provides an interactive tool at IRS.gov (“Do I Need to File a Tax Return?”) to help you determine your filing obligation.

My adult child only has investment income — can I still claim them?

Often not. A child who is 19 or older and not a full-time student can only be claimed under the qualifying relative rules, which cap the child’s gross income (currently $5,200, adjusted annually). Dividends and capital gains count toward that limit. If the child’s investment income exceeds it, you cannot claim them — even if you provided all of their support for the year.

Is a gift I received considered unearned income?

No — gifts are not income to the recipient at all. You do not report a gift on your tax return. The person giving the gift may need to file Form 709 if the gift exceeds $19,000 per recipient in a single year, but that is the giver’s obligation, not the recipient’s.

How is Social Security taxability determined?

The IRS uses a formula called “combined income” — your adjusted gross income plus nontaxable interest plus half of your Social Security benefits. If this total exceeds $25,000 (Single) or $32,000 (MFJ), a portion of your benefits becomes taxable. At the highest levels, up to 85% of Social Security may be subject to federal income tax.

Official Resources

- IRS — Topic No. 553: Tax on a Child’s Investment and Other Unearned Income (Kiddie Tax)

- IRS — Topic No. 559: Net Investment Income Tax

- IRS — Questions and Answers on the Net Investment Income Tax

- IRS — Topic No. 409: Capital Gains and Losses

- IRS Publication 501 — Dependents, Standard Deduction, and Filing Information

- IRS Publication 550 — Investment Income and Expenses

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.