What Is an Enrolled Agent (EA)?

The Enrolled Agent is the only tax credential awarded directly by the U.S. Department of the Treasury — a federal credential rather than a state one. That federal scope is what lets an EA represent taxpayers before the IRS in all 50 states.

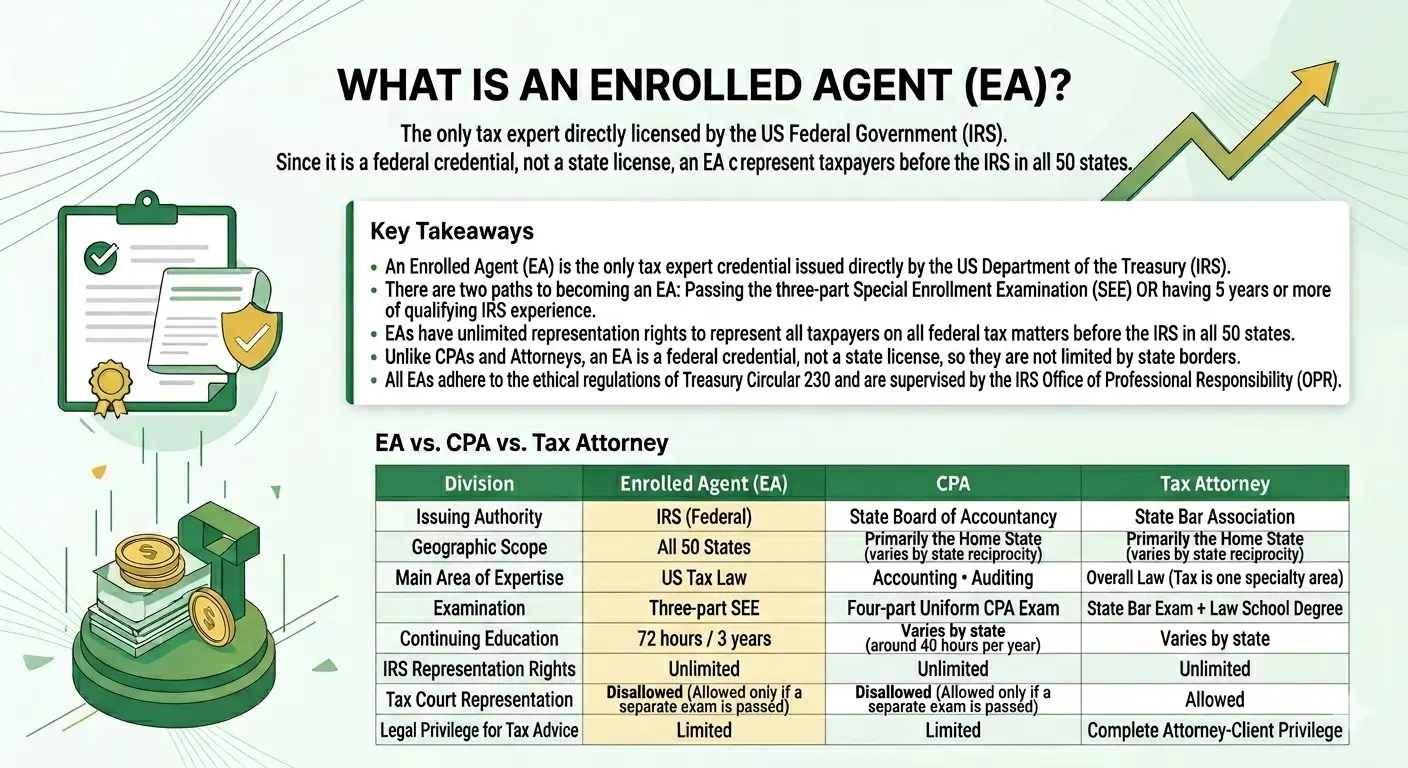

Key Takeaways

- An Enrolled Agent (EA) is the only tax credential awarded directly by the IRS itself — at the federal level, rather than by a state board.

- There are two paths to the credential: passing the three-part Special Enrollment Examination (SEE), or five-plus years of qualifying IRS employment.

- EAs have unlimited representation rights — any taxpayer, any federal tax matter, any IRS office, any state.

- Because the EA is a federal credential, it is not limited by state borders the way CPA and attorney licenses can be.

- Every EA is bound by Treasury Circular 230 and overseen by the IRS Office of Professional Responsibility (OPR).

Table of Contents

- What Is an Enrolled Agent?

- A Brief History of the EA Credential

- How Someone Becomes an Enrolled Agent

- Inside the Three-Part SEE Exam

- What an EA Can Do for Taxpayers

- EA vs. CPA vs. Tax Attorney

- Continuing Education (CE) Requirements

- Circular 230 and Professional Conduct

- How to Verify an Enrolled Agent

1. What Is an Enrolled Agent?

An Enrolled Agent — commonly shortened to EA — is a federally authorized tax practitioner empowered by the U.S. Department of the Treasury to represent taxpayers before the Internal Revenue Service. The EA is the highest credential the IRS itself awards.

An EA’s focus is narrow but deep: U.S. federal tax law and IRS procedure. CPAs also work in accounting, auditing, and attestation; attorneys cover the full breadth of law. EAs work almost exclusively with taxes — individual and business returns, trusts and estates, payroll matters, audits, appeals, and collection cases.

Three features define the credential:

- It is issued at the federal level, not by a state board.

- It grants unlimited representation rights before the IRS.

- It is maintained under Treasury Circular 230.

As an Enrolled Agent myself, I see every week how the federal scope of this credential matters to taxpayers who relocate across state lines, own property in multiple states, or receive IRS notices from service centers far from where they live.

2. A Brief History of the EA Credential

The EA designation traces back to the aftermath of the American Civil War. Claims for property lost or damaged during the war — especially horses seized by the Union Army — flooded the Treasury Department, and many claims were fraudulent or mishandled by unqualified representatives. Congress responded with the Enabling Act of 1884, often called the “Horse Act,” which authorized the Secretary of the Treasury to regulate who could represent citizens with claims before the government.

Once the federal income tax became permanent in 1913, the EA role narrowed from general claim representation toward tax representation specifically. The modern credential carries forward that original principle: anyone who represents a taxpayer before the IRS must meet a federal standard of competency and ethics.

3. How Someone Becomes an Enrolled Agent

There are two recognized paths to EA status.

Path 1 — The Special Enrollment Examination (SEE)

Most EAs earn the credential by passing a three-part exam administered by an IRS-authorized testing vendor. Before scheduling, the candidate must obtain a Preparer Tax Identification Number (PTIN). Each part may be attempted up to four times per testing window, and all three parts must be passed within three years of passing the first part.

Path 2 — Qualifying IRS Experience

A person who has worked at least five years in a qualifying IRS position — interpreting and applying the Internal Revenue Code — may apply for enrollment based on that experience, subject to IRS review. This path explains why a notable share of experienced EAs are former IRS examination, collection, or appeals officers who bring that internal perspective directly to private practice.

After satisfying either path, the candidate submits Form 23, Application for Enrollment to Practice Before the Internal Revenue Service. The IRS then conducts a suitability check reviewing the applicant’s personal tax compliance and criminal background before granting the credential.

4. Inside the Three-Part SEE Exam

The Special Enrollment Examination is divided into three independent parts, each focused on a distinct area of tax practice.

Part 1 — Individuals

Covers preliminary work with taxpayer data, income and assets, deductions and credits, taxation, advising individual taxpayers, and specialized individual returns.

Part 2 — Businesses

Covers business entities — partnerships, corporations, S-corporations, LLCs, trusts, estates, and tax-exempt organizations — along with business financial information and specialized business returns.

Part 3 — Representation, Practices and Procedures

Covers practice before the IRS, representation of taxpayers, specific areas of representation, and filing processes. This part ties most directly to Circular 230.

Each part is a 100-question multiple-choice exam. Of those, 85 questions are scored and 15 are experimental questions the IRS is testing for future use — and you won’t know which is which. Scores are reported on a scaled range from 200 to 800, and a score of 500 is required to pass. Candidates who pass see only the word “Pass,” with no number; only a failing report shows a score.

Registration and testing fees are periodically adjusted; candidates should confirm current figures and the active testing vendor on IRS.gov before scheduling.

Thinking about sitting for Part 1 yourself? My EA Exam Part 1 Made Simple series breaks the Individuals portion into short, plain-English study guides — one domain at a time, written for people who don’t think in tax jargon.

Browse the EA Tax Wise book series →5. What an Enrolled Agent Can Do for Taxpayers

The single word that defines the EA credential is unlimited. An EA can represent any taxpayer, on any federal tax matter, before any IRS office, in any state.

In concrete terms, an EA can:

- Prepare federal and state tax returns for individuals, businesses, estates, and trusts.

- Represent a client during an IRS audit, including in-person examinations.

- Handle appeals before the IRS Office of Appeals.

- Negotiate installment agreements, offers in compromise, and penalty abatements.

- Respond to IRS notices and correspondence on the taxpayer’s behalf.

- Appear at IRS collection proceedings.

Representation rights stop at the courthouse door. EAs cannot argue cases in U.S. Tax Court unless they separately pass the Tax Court’s non-attorney practitioner exam, and they cannot represent clients in U.S. District Court, the Court of Federal Claims, or bankruptcy matters — those require an attorney.

6. EA vs. CPA vs. Tax Attorney

All three credentials offer unlimited representation rights before the IRS, but they differ in training, scope, and jurisdiction.

| Feature | Enrolled Agent (EA) | CPA | Tax Attorney |

|---|---|---|---|

| Authorizing body | IRS (federal) | State Board of Accountancy | State Bar |

| Geographic scope | All 50 states | Home state (reciprocity varies) | Home state (reciprocity varies) |

| Primary focus | U.S. tax law | Accounting & auditing | Law (tax is one specialty) |

| Exam | 3-part SEE | 4-part Uniform CPA Exam | Bar exam + law degree |

| Continuing education | 72 hours / 3 years | Varies by state (~40 hrs/yr) | Varies by state |

| IRS representation | Unlimited | Unlimited | Unlimited |

| U.S. Tax Court | No (unless separate exam) | No (unless separate exam) | Yes |

| Legal privilege | Limited | Limited | Full attorney-client |

The practical takeaway: for pure tax work — return preparation, audit representation, collection cases — an EA and a CPA are functionally equivalent in representation authority. For broader accounting services such as financial statements and audit attestation, a CPA is required. For tax litigation, criminal tax defense, or complex estate planning, a tax attorney is the right choice.

7. Continuing Education (CE) Requirements

An EA’s credential is not permanent. To maintain active status, an EA must meet the following ongoing requirements:

- Complete 72 hours of CE every three years (the enrollment cycle).

- Meet an annual minimum of 16 hours.

- Include at least 2 hours of ethics or professional conduct each year.

- Take CE only from IRS-approved sponsors, who report credits directly to the IRS.

An EA who fails to meet these requirements is placed on inactive status and cannot practice or hold out as an EA until the deficiency is cured.

8. Circular 230 and Professional Conduct

Circular 230 is the Treasury Department publication that governs practice before the IRS. It binds every EA, CPA, attorney, and other recognized practitioner. Its scope reaches due diligence, conflicts of interest, fees, advertising, confidentiality, and the handling of client records.

Enforcement is the responsibility of the IRS Office of Professional Responsibility (OPR). OPR investigates misconduct and can impose sanctions ranging from censure to suspension or disbarment from practice.

The rules in Circular 230 are the ethical backbone of the profession. A companion article in the Related Articles section below covers these rules in detail.

9. How to Verify an Enrolled Agent

Anyone claiming to be an EA should appear in the IRS Directory of Federal Tax Return Preparers with Credentials and Select Qualifications, which is publicly searchable on IRS.gov.

To verify:

- Visit the IRS directory search page.

- Enter the preparer’s last name and ZIP code.

- Confirm that “Enrolled Agent” appears as the credential.

A taxpayer can also request to see the practitioner’s enrollment card or contact the IRS Return Preparer Office to confirm active status.

💡 EA Insight: The Cost of a Missing Credential

A self-employed client came to my office with a CP2000 notice proposing about $18,400 in additional tax. The preparer who filed her return was an unenrolled preparer — and once the IRS notice arrived, he told her plainly that he had no authority to accompany her to an examination or represent her in any way. She ended up paying twice: once for the original return, and again to retain me to handle the response.

That episode captures exactly why the EA credential exists. Preparing a return and being allowed to stand in front of the IRS on your behalf are two entirely different things. One question at the hiring stage — “Are you an Enrolled Agent, CPA, or attorney?” — prevents this situation entirely.

Frequently Asked Questions

Q1. Is an Enrolled Agent equivalent to a CPA?

For IRS representation, yes — both have unlimited practice rights before the IRS. Outside federal tax matters, the credentials differ: CPAs also perform audits, compilations, and financial statement attestation, which EAs do not.

Q2. Can an EA practice in any state?

Yes. Because the EA is a federal credential, an EA authorized in New York can represent a client in California, Texas, or any other state without additional licensing.

Q3. How long does it take to become an EA?

Most candidates complete the three SEE parts within six months to a year of study, followed by IRS processing of Form 23 that typically takes 60 days or more. Total time from start to credential is generally 8 to 14 months.

Q4. Does an EA have to renew the credential?

Yes. Enrollment runs on a three-year cycle, with renewal required through Form 8554 and a renewal fee. CE hours must be completed before renewal.

Q5. Can an EA represent me in U.S. Tax Court?

Not automatically. An EA may represent clients in U.S. Tax Court only after separately passing the Tax Court’s non-attorney practitioner examination.

Q6. What happens if an EA violates Circular 230?

The IRS Office of Professional Responsibility can impose sanctions including censure, suspension, or disbarment. Serious violations may lead to civil penalties or referral for criminal investigation.

Related Articles

Official Resources

Disclaimer: This article is for general educational purposes only and does not constitute tax, legal, or financial advice. Tax rules and IRS procedures change over time. Consult a qualified tax professional regarding your specific situation.