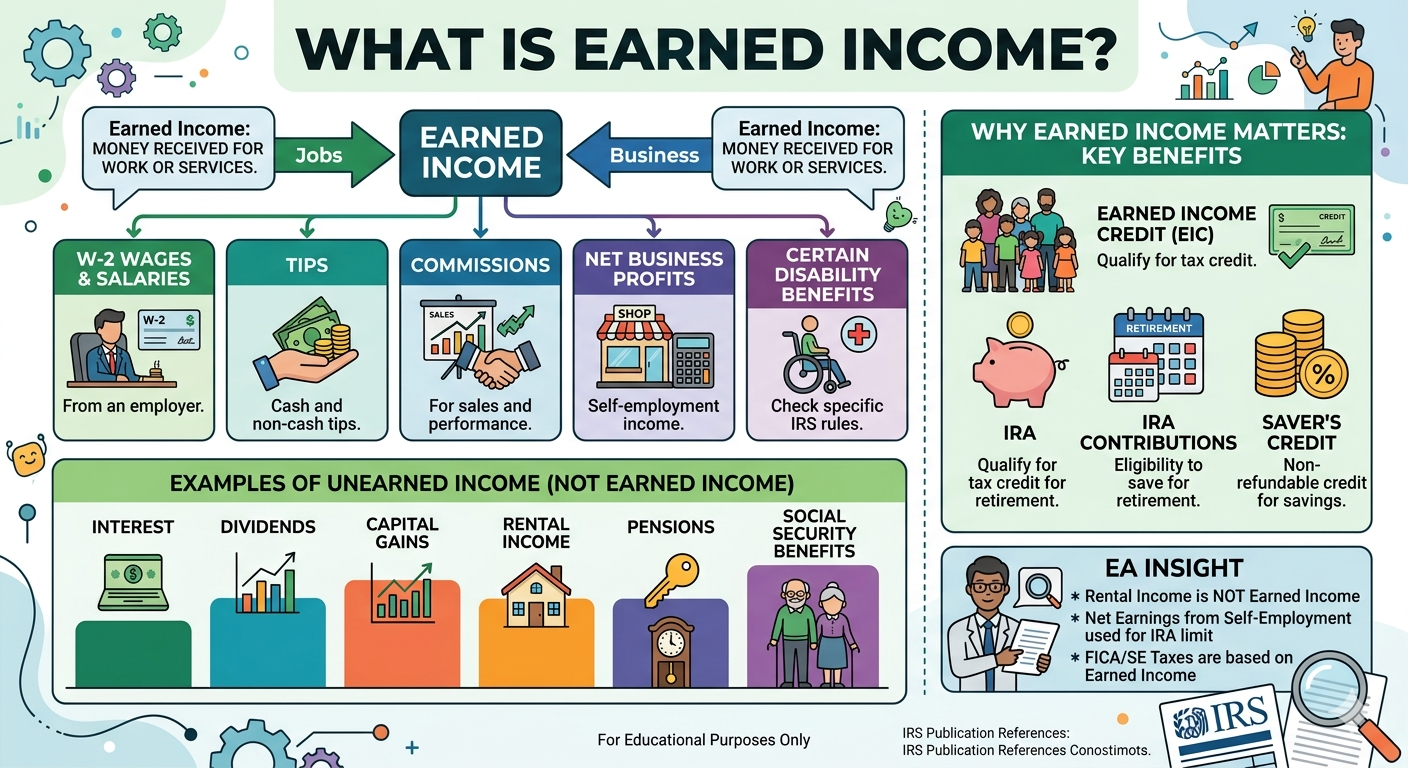

What Is Earned Income?

Earned income is what you make by working — wages, salaries, tips, and self-employment profit. Without it, you cannot claim the Earned Income Credit, contribute to an IRA, or qualify for the Saver’s Credit. Investment income, rental income, and Social Security benefits do not count — no matter how much you receive.

Key Takeaways

- Earned income comes from work or active business activity — wages, tips, commissions, and net self-employment profit.

- Interest, dividends, capital gains, rental income, pensions, and Social Security benefits do not qualify.

- The Earned Income Credit (EIC), Saver’s Credit, and IRA contributions all require this type of income.

- To qualify for the EIC, investment income must also be $12,200 or less for the tax year.

- IRA contributions are limited to the lesser of qualifying income or the annual limit ($7,500; $8,600 if age 50 or older).

- Wages and self-employment profit are subject to FICA; investment and passive income are not.

Table of Contents

1. What Is Earned Income?

Earned income is income you receive as a direct result of work or active business participation. Whether you receive a paycheck from an employer, run your own business, or perform services for pay, the money you earn through that effort falls into this category.

The IRS defines it explicitly in Publication 596 (Earned Income Credit) because three significant tax benefits — the Earned Income Credit, the Saver’s Credit, and IRA contribution eligibility — each depend on whether a taxpayer has this type of income and how much.

The distinction matters because not all income is treated equally. Money that comes from investments, retirement accounts, or government benefits is classified as unearned income and does not satisfy the requirement for these benefits.

2. Income That Qualifies

The following types of income qualify under IRS rules:

- Wages and salaries — all pay received from an employer, reported on Form W-2

- Tips — cash tips, charged tips, and any other gratuities received for services

- Commissions — performance-based compensation for sales or services

- Net profit from self-employment — Schedule C net profit after business deductions

- Active partnership income — income earned by a general partner who provides services to the partnership

- Certain long-term disability benefits — benefits received before reaching minimum retirement age, under specific employer-paid plans

- Nontaxable combat pay — military members may elect to include nontaxable combat pay when calculating the EIC

Note: For self-employed taxpayers, the qualifying amount for IRA contribution purposes is calculated as net self-employment profit minus the deductible portion of Self-Employment Tax (one-half of SE Tax).

3. Income That Does Not Qualify

The following types of income do not count as earned income, regardless of how much effort or time may be involved in managing them:

| Income Type | Classification |

|---|---|

| Interest income | Unearned Income |

| Dividends | Unearned Income |

| Capital gains | Unearned Income |

| Rental income | Passive / Unearned Income |

| Pensions and annuities | Retirement / Unearned Income |

| Social Security benefits | Unearned Income |

| Unemployment compensation | Unearned Income |

| Child support | Not income |

| Alimony (divorce finalized after Dec. 31, 2018) | Not taxable / Does not qualify |

| Welfare benefits | Not income |

Alimony exception: For divorces finalized on or before December 31, 2018, alimony received is still taxable and qualifies as compensation for IRA contribution purposes. Divorces finalized after that date are not eligible.

4. Three Tax Benefits That Depend on It

The Earned Income Credit (EIC / EITC)

The Earned Income Credit is a refundable tax credit for low- to moderate-income workers. Without qualifying wages or business income, the EIC is not available at all. Eligibility depends on the amount of qualifying income, filing status, and number of qualifying children.

In addition, taxpayers must have investment income of $12,200 or less for the tax year to qualify. Investment income includes interest, dividends, and capital gains. Exceeding this threshold disqualifies the taxpayer from the credit even if all other requirements are met.

The Saver’s Credit

The Saver’s Credit is a nonrefundable tax credit available to low- and middle-income taxpayers who contribute to a retirement account such as an IRA or 401(k). Work-based income is required to qualify. The credit rate ranges from 10% to 50% of contributions, depending on adjusted gross income and filing status.

IRA Contribution Eligibility

To contribute to a Traditional IRA or Roth IRA, you must have qualifying income in that tax year. The contribution limit is the lesser of your qualifying wages or business income or the annual cap. For the current tax year, the limit is $7,500. Taxpayers age 50 or older may contribute up to $8,600, which includes a $1,100 catch-up contribution.

Taxpayers with only investment income — dividends, interest, or capital gains — cannot contribute to an IRA, regardless of how large that income may be.

5. FICA and Payroll Taxes

Wages and business profits are subject to FICA (Federal Insurance Contributions Act) taxes, which fund Social Security and Medicare. Unearned income — interest, dividends, and rental income — is not. How FICA applies depends on your employment type:

| Employment Type | How FICA Is Paid |

|---|---|

| W-2 Employee | Employee and employer each pay half (7.65% each; total 15.3%) |

| Self-Employed | Pays full 15.3% as Self-Employment Tax (SE Tax); one-half is deductible from AGI |

6. How It Connects to AGI and MAGI

Earned income, AGI, and MAGI are related but represent different stages of the tax calculation:

- Earned income is a specific category defined by source — it is determined before AGI is calculated.

- AGI (Adjusted Gross Income) includes all income — both earned and unearned — minus above-the-line deductions such as student loan interest, IRA deductions, and the deductible portion of SE Tax.

- MAGI (Modified Adjusted Gross Income) is AGI with certain deductions added back. It is used to determine eligibility for Roth IRA contributions, education credits, and other benefits.

Example: Roth IRA contribution eligibility is based on MAGI, but the maximum contribution amount is still limited to qualifying wages or business income. Both thresholds must be checked independently.

EA Insight

The definition looks straightforward, but in practice I see confusion at the edges — and those misunderstandings lead to real errors on tax returns.

The most common mistake is treating rental income as qualifying wages or business profit. A taxpayer who actively manages rental properties may feel like they are working for that money — and they are — but rental income is passive income by default under the tax code. It cannot be used to support an IRA contribution and cannot help establish EIC eligibility.

For self-employed taxpayers, the IRA calculation is not simply the Schedule C net profit. The correct figure is net profit multiplied by 0.9235 (which equals net profit minus the deductible half of SE Tax). Using the gross Schedule C figure instead results in an overstated contribution limit — a compliance issue the IRS can identify.

On the EIC side, the investment income limit is frequently overlooked. For the current tax year, investment income must not exceed $12,200. A taxpayer with modest wages but large dividends or capital gains may be disqualified from the EIC even when their work income alone would have qualified them. Always run both tests before claiming the credit.

Frequently Asked Questions

Can a non-working spouse contribute to an IRA?

Yes. Married couples filing jointly may use the working spouse’s qualifying income to fund a Spousal IRA for the non-working spouse. The total combined contribution for both spouses cannot exceed the couple’s combined qualifying income, and each account remains subject to the individual annual limit.

Is unemployment compensation earned income?

No. Unemployment compensation is taxable, but it does not qualify as earned income. A taxpayer who receives only unemployment benefits in a given year cannot contribute to an IRA and cannot claim the EIC based on those benefits.

Does military combat pay qualify for EIC purposes?

Nontaxable combat pay is not required to be included, but military members may elect to include it when calculating the EIC. Doing so can increase the credit amount in some cases. The election applies to the entire amount — it cannot be partially included.

Is Social Security Disability (SSDI) earned income?

No. SSDI is unearned income. However, certain long-term disability benefits received before reaching minimum retirement age — under specific employer-funded plans — may be treated as qualifying income. Regular SSDI payments from the Social Security Administration do not qualify.

Is all partnership income earned income?

No. Only income earned by a general partner who actively provides services to the partnership qualifies. A limited partner who receives a passive share of profits without performing services does not receive qualifying income from that distribution.

Does alimony count for IRA contribution purposes?

It depends on the divorce date. Alimony received under an agreement finalized on or before December 31, 2018 is taxable and qualifies as compensation for IRA purposes. Alimony under agreements finalized after that date is not taxable and does not count.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.