What Is Filing Status? The 5 Types Explained

Filing status is one of the first boxes you check on Form 1040 — and it affects your standard deduction, tax brackets, and eligibility for credits. Choosing the right one can mean a significantly lower tax bill.

Key Takeaways

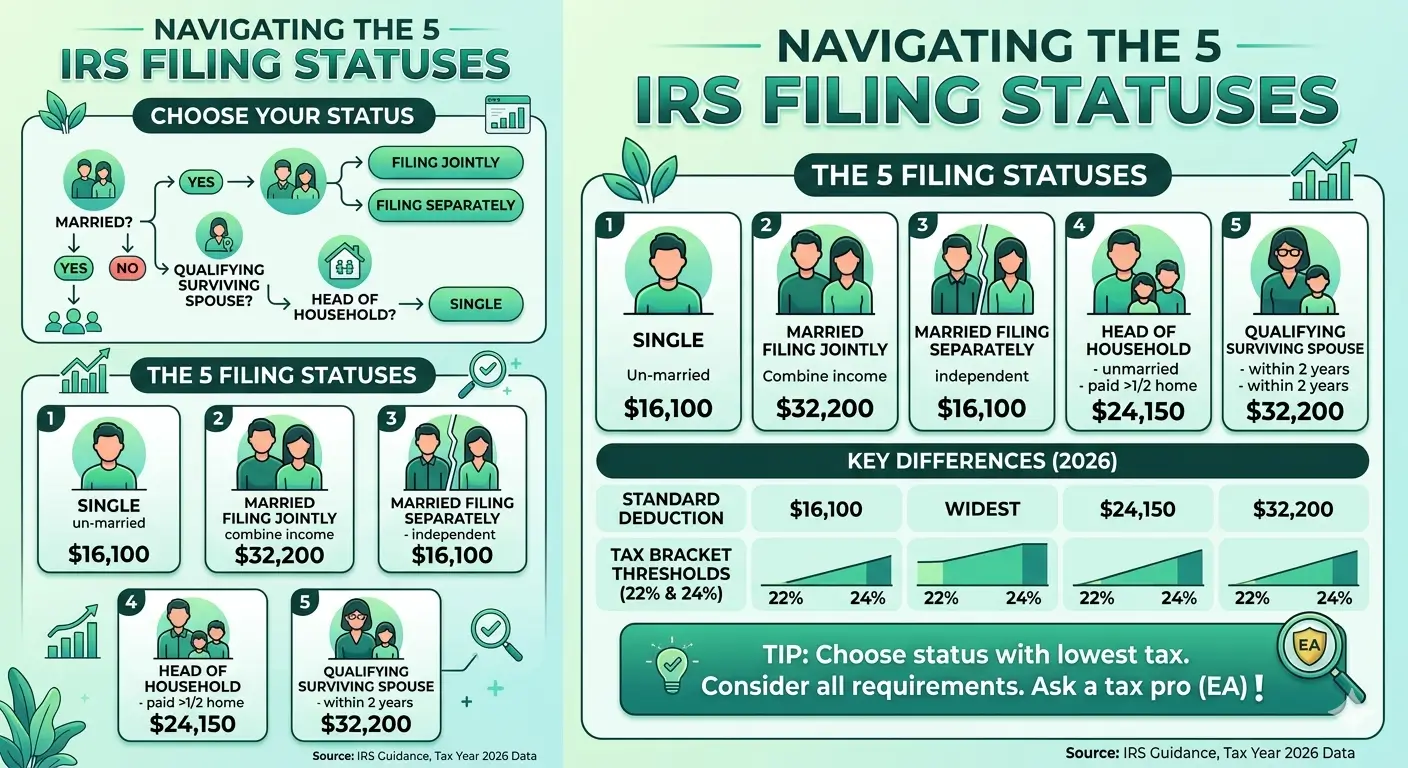

- There are five filing statuses: Single, Married Filing Jointly, Married Filing Separately, Head of Household, and Qualifying Surviving Spouse.

- Your filing status is determined by your marital and family situation as of December 31 of the tax year.

- Filing status directly affects your standard deduction amount, tax bracket thresholds, and credit eligibility.

- If more than one status applies to you, the IRS says to choose the one that results in the lowest tax.

- Head of Household is one of the most commonly misunderstood — and misused — statuses on Form 1040.

Table of Contents

1. What Is Filing Status and Why Does It Matter?

Every federal tax return starts with one question: what is your filing status? It’s not just a label — it’s the foundation that determines three critical things about your tax return.

- Your standard deduction amount — which directly reduces your taxable income

- Your tax bracket thresholds — where each rate begins and ends

- Your eligibility for credits and deductions — many phase out at different income levels depending on your status

Your filing status is based on your situation on the last day of the tax year — December 31. Even if your circumstances changed mid-year (you got married, divorced, or lost a spouse), what matters is where things stand on December 31.

If more than one status applies, the IRS instructs you to use the one that results in the lowest tax liability. This is an important point — choosing the wrong status means paying more than you legally owe.

🔍 Find Your Filing Status

Answer each question to find your correct filing status.

Were you legally married as of December 31?

2. The 5 Filing Statuses at a Glance

| Filing Status | Standard Deduction | Basic Requirement |

|---|---|---|

| Single | $16,100 | Unmarried or legally separated as of Dec 31 |

| Married Filing Jointly | $32,200 | Married as of Dec 31, filing one joint return |

| Married Filing Separately | $16,100 | Married but choosing to file separate returns |

| Head of Household | $24,150 | Unmarried, paid over half of home costs, qualifying person |

| Qualifying Surviving Spouse | $32,200 | Widowed within 2 years, dependent child at home |

Source: IRS Revenue Procedure 2025-32 (tax year 2026 standard deduction amounts).

3. Single

The Single filing status applies if you are unmarried, legally separated, or divorced as of December 31 of the tax year, and you do not qualify for any other filing status.

It’s also the default status for anyone who simply doesn’t meet the requirements for Head of Household or another more favorable status. Single filers receive the lowest standard deduction and face the narrowest tax brackets, meaning income hits higher rates sooner compared to other statuses.

Who files as Single?

- Never married individuals

- Divorced or legally separated individuals (as of Dec 31)

- Widowed individuals who don’t qualify for Qualifying Surviving Spouse or Head of Household

4. Married Filing Jointly (MFJ)

Married Filing Jointly is available to couples who are legally married as of December 31. Both spouses combine all income, deductions, and credits on a single return. This is the most common filing choice for married couples — and for good reason.

MFJ offers the highest standard deduction ($32,200), the widest tax brackets, and access to credits that are reduced or eliminated under Married Filing Separately. In most cases, it results in a lower combined tax bill than filing separate returns.

Key MFJ Benefits

- Highest standard deduction of all five statuses

- Wider tax brackets — more income taxed at lower rates

- Access to Earned Income Credit, Child and Dependent Care Credit, and education credits at higher income thresholds

- Both spouses are jointly and individually responsible for the tax owed (joint and several liability)

Note: If your spouse passed away during the tax year, you are generally still considered married for that year and can file jointly — provided you did not remarry before December 31.

5. Married Filing Separately (MFS)

Married Filing Separately allows legally married spouses to file independent returns, each reporting only their own income, deductions, and credits. While it sounds like a simple option, MFS comes with significant trade-offs.

When MFS Can Make Sense

- One spouse has significant medical expenses that exceed the 7.5% AGI threshold — filing separately lowers that spouse’s AGI, making more expenses deductible

- Spouses want to keep finances legally separate (e.g., during separation proceedings)

- One spouse has outstanding federal debt (e.g., back taxes, student loans) that could trigger a tax refund offset on a joint return

MFS Disadvantages

- Cannot claim the Earned Income Credit, most education credits, or the Child and Dependent Care Credit

- Cannot claim the student loan interest deduction

- If one spouse itemizes, the other must also itemize — even if their itemized deductions are minimal

- Lower IRA contribution phase-out thresholds apply

- IRMAA surcharges on Medicare premiums apply at lower income levels

Important: MFS is rarely the better option from a pure tax standpoint. Always calculate your tax both ways before choosing this status.

6. Head of Household (HoH)

Head of Household is designed for unmarried taxpayers who support a qualifying person. It offers a higher standard deduction than Single ($24,150 vs. $16,100) and more favorable tax brackets — making it a meaningful benefit for single parents and caregivers.

To qualify, you must meet all three of the following requirements:

- Unmarried (or “considered unmarried”) as of December 31 — this includes legally separated individuals and, in some cases, married individuals who lived apart from their spouse for the last 6 months of the year

- Paid more than half the cost of keeping up your home for the year — rent/mortgage, utilities, food, repairs, and similar household expenses count

- A qualifying person lived with you for more than half the year — this is typically a dependent child, but can also be a dependent parent (who does not need to live with you)

What Counts as “Keeping Up a Home”?

Paying more than 50% of household costs is a hard requirement — and the IRS defines qualifying expenses specifically. Use this checklist to see what counts:

✅ Expenses That Count Toward the 50% Threshold

| Expense | Counts? |

|---|---|

| Rent or mortgage interest | ✔ Yes |

| Real estate taxes | ✔ Yes |

| Utilities (electricity, gas, water) | ✔ Yes |

| Repairs and maintenance | ✔ Yes |

| Food eaten in the home | ✔ Yes |

| Home insurance | ✔ Yes |

| Clothing | ✖ No |

| Medical or dental expenses | ✖ No |

| Education or transportation costs | ✖ No |

Source: IRS Publication 501. Total all qualifying costs for the year, then verify you paid more than half.

Who Is a “Qualifying Person”?

- Your child, stepchild, or foster child under age 19 (or under 24 if a full-time student)

- A permanently and totally disabled child of any age

- Your parent, if you can claim them as a dependent (they don’t need to live with you)

- Certain other relatives who lived with you and qualify as your dependent

Common mistake: Head of Household is one of the most frequently misused statuses. You cannot claim HoH simply because you live with your child — you must also be unmarried (or considered unmarried) and pay more than half the household costs. The IRS actively flags incorrect HoH claims.

7. Qualifying Surviving Spouse

Qualifying Surviving Spouse (formerly called “Qualifying Widow(er)”) is a transitional status available to widowed taxpayers for up to two tax years after the year of their spouse’s death. It provides the same standard deduction ($32,200) and tax bracket structure as Married Filing Jointly — helping to soften the financial impact of losing a spouse.

Requirements

- Your spouse died within the prior two tax years and you have not remarried

- You have a qualifying dependent child living in your home

- You paid more than half the cost of maintaining the home for the year

The Timeline

| Year | Available Filing Status | Standard Deduction |

|---|---|---|

| Year spouse dies | Married Filing Jointly | $32,200 |

| Year 1 after death | Qualifying Surviving Spouse | $32,200 |

| Year 2 after death | Qualifying Surviving Spouse | $32,200 |

| Year 3 and beyond | Head of Household or Single | $24,150 or $16,100 |

Remarriage in any year immediately ends eligibility for Qualifying Surviving Spouse status for that year.

8. How Filing Status Affects Your Tax

Filing status doesn’t just change your standard deduction — it reshapes your entire tax picture. Here’s a side-by-side look at the 2026 tax bracket thresholds for each status, using the 22% and 24% brackets as a reference point.

| Filing Status | 22% Bracket Starts At | 24% Bracket Starts At |

|---|---|---|

| Single | $50,400 | $105,700 |

| Married Filing Jointly | $100,800 | $211,400 |

| Married Filing Separately | $50,400 | $105,700 |

| Head of Household | $66,750 | $177,900 |

| Qualifying Surviving Spouse | $100,800 | $211,400 |

Source: IRS Revenue Procedure 2025-32. Tax year 2026 bracket thresholds apply to taxable income (AGI minus deductions).

As the table shows, a single parent who qualifies for Head of Household keeps the 22% rate up to $66,750 of taxable income — compared to only $50,400 under Single. That’s an additional $16,350 of income taxed at the lower 22% rate rather than 24%. The difference adds up quickly.

EA Insight

Head of Household is the status I see misused most often — especially in New York, where I work with a lot of multi-generational households and immigrant families. The most common scenario: a married couple is having problems, one spouse moves out for several months, and the one who stays files as Head of Household claiming the kids. But unless they meet the IRS definition of “considered unmarried” — which requires living apart for the entire last six months of the year, among other conditions — they don’t qualify. The IRS catches this regularly through matching programs.

The second thing I see often: clients who become widowed and don’t realize Qualifying Surviving Spouse exists. They default to Single, and immediately lose the higher standard deduction and broader brackets. If they have a dependent child at home, they may qualify for two full years of MFJ-equivalent tax treatment. That’s real money — potentially thousands of dollars — left on the table simply because no one told them about this status.

My first question with any new client going through a life change — marriage, divorce, separation, death of a spouse, a child moving out — is always: has your filing status changed? People tend to think about this once a year at tax time, but the right answer starts on January 1.

People Also Ask

What if I’m not sure which filing status to use?

The IRS provides an interactive tool — the “What Is My Filing Status?” tool at IRS.gov — that walks you through a series of questions to determine which status applies to your situation. When more than one status applies, choose the one that results in the lowest tax liability.

Can I change my filing status after I’ve already filed?

Yes. If you filed with the wrong status, you can correct it by filing an amended return using Form 1040-X. There is generally a three-year window from the original filing deadline to file an amendment and claim a refund.

Does my filing status have to match my spouse’s?

Not always — but there’s one key exception. If you are married and one spouse itemizes deductions, the other must also itemize. Beyond that, spouses can independently choose Married Filing Jointly or Married Filing Separately each year.

Can two people in the same household claim Head of Household?

Only if they each have a different qualifying person and each meet all the requirements independently. For example, two unmarried siblings living together, each supporting their own child, could potentially each file as Head of Household. The qualifying persons cannot be the same individual.

Does New York State use the same filing status as federal?

Generally, yes — New York State requires you to use the same filing status on your state return as your federal return. However, NYS has its own standard deduction amounts, which are significantly lower than the federal figures:

| Filing Status | Federal (2026) | New York State |

|---|---|---|

| Single | $16,100 | $8,000 |

| Married Filing Jointly | $32,200 | $16,050 |

| Married Filing Separately | $16,100 | $8,000 |

| Head of Household | $24,150 | $11,200 |

Because NYS amounts are roughly half the federal figures, New York residents who take the federal standard deduction should still evaluate whether itemizing at the state level — using Schedule A (NYS) — saves more. Always confirm current NYS figures at tax.ny.gov.

What happens if I use the wrong filing status?

Using an incorrect filing status can result in underpaying or overpaying tax. If you underpay, the IRS will assess the additional tax owed, plus interest and potentially penalties. If you claimed a status that lowered your tax but you didn’t qualify, it may be treated as a fraudulent filing in serious cases. File an amended return (Form 1040-X) as soon as possible if you discover an error.

Related Articles

Official Resources

Updated: Current tax year

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual situations vary. Always verify current figures at IRS.gov and consult a qualified tax professional (EA, CPA, or attorney) for advice specific to your situation.