What Is a 1099-DA?

Form 1099-DA is the IRS information return designed specifically for digital asset transactions. If you sold, exchanged, or disposed of cryptocurrency, NFTs, or other digital assets through a U.S.-based exchange, the IRS now receives the same transaction data you do.

Key Takeaways

- Form 1099-DA reports sales, exchanges, and dispositions of digital assets — including cryptocurrency, stablecoins, and NFTs.

- Custodial brokers (Coinbase, Kraken, Robinhood, PayPal, etc.) issue 1099-DA to both the taxpayer and the IRS.

- Initial reporting covers gross proceeds only. Cost basis reporting phases in for covered securities acquired through a custodial broker.

- DeFi transactions, staking rewards, and self-custody wallet activity are not reported on 1099-DA — but they are still taxable.

- Whether or not you receive a 1099-DA, you must report all digital asset income on your federal tax return.

- Cost basis tracking is now required on a wallet-by-wallet basis — the old universal method is no longer permitted.

Table of Contents

- 1. What Is Form 1099-DA?

- 2. Why Was a New Form Needed?

- 3. Who Receives a 1099-DA?

- 4. What Information Does It Report?

- 5. Reporting Phases: Gross Proceeds vs. Cost Basis

- 6. What 1099-DA Does Not Cover

- 7. Why You Must Track Your Own Cost Basis

- 8. 1099-DA vs. 1099-B vs. 1099-K

- 9. EA Insight

- 10. Frequently Asked Questions

- 11. Related Articles

- 12. Official Resources

1. What Is Form 1099-DA?

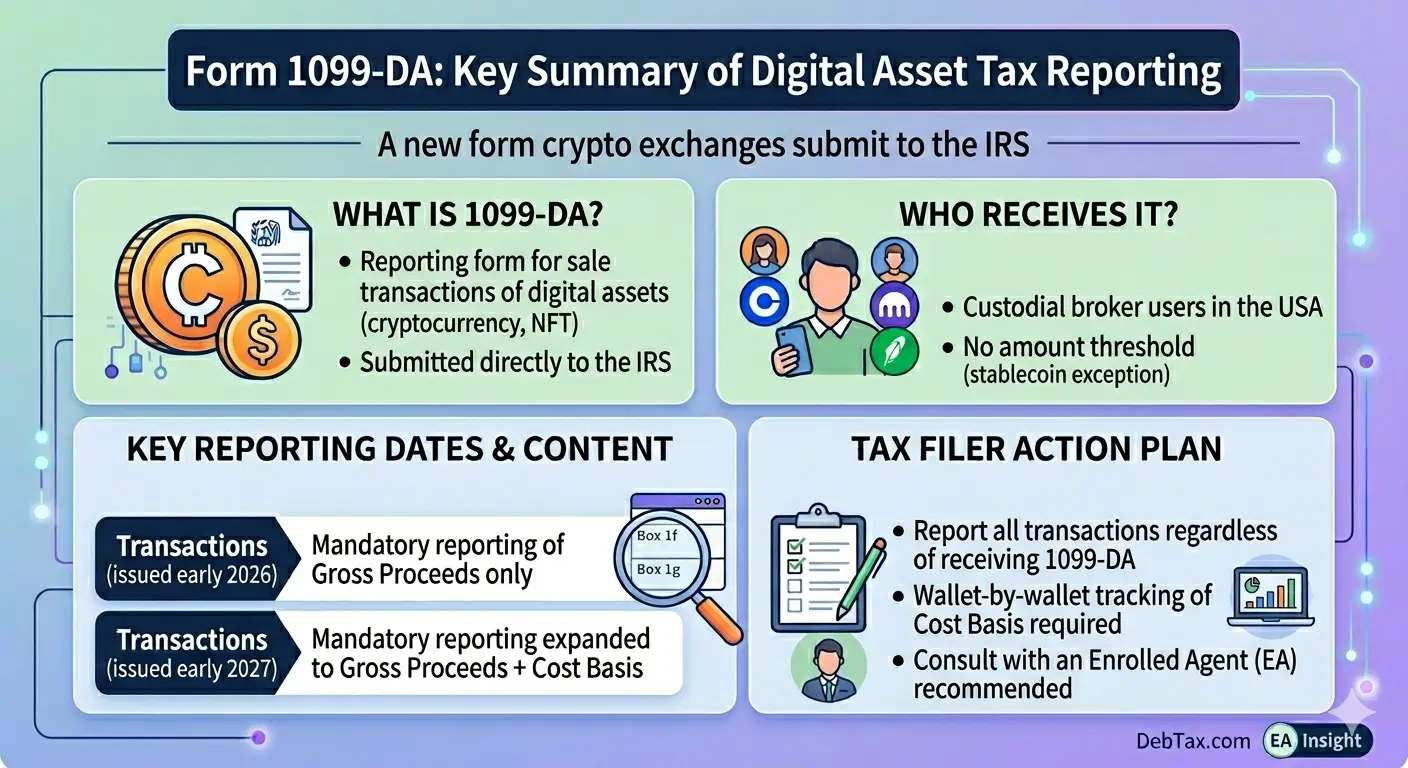

Form 1099-DA, Digital Asset Proceeds From Broker Transactions, is an IRS information return that reports sales, exchanges, and other dispositions of digital assets handled by custodial brokers.

Digital assets include cryptocurrency (Bitcoin, Ethereum, etc.), stablecoins, and non-fungible tokens (NFTs). Before this form existed, there was no standardized way for digital asset platforms to report transaction data to the IRS. Some exchanges used Form 1099-B, others used 1099-K or 1099-MISC, and many reported nothing at all.

Form 1099-DA was created to bring consistency to digital asset reporting — much like Form 1099-B has long served for stocks and securities.

2. Why Was a New Form Needed?

For traditional investments like stocks and bonds, brokers have reported transaction data to the IRS through Form 1099-B for decades. This third-party reporting system allows the IRS to cross-reference what brokers report with what taxpayers file on their returns.

Digital assets had no equivalent system. The IRS relied almost entirely on self-reporting by taxpayers, which left a significant gap in compliance.

The legal foundation for 1099-DA comes from the Infrastructure Investment and Jobs Act (signed in late 2021), which expanded the definition of “broker” under Internal Revenue Code §6045 to include custodial digital asset platforms. The IRS finalized the reporting regulations in July 2024 (Treasury Decision 10000).

With 1099-DA in place, the IRS can now automatically match broker-reported data against individual tax returns. When reported proceeds do not align with a taxpayer’s filing, the system can trigger an automated notice.

3. Who Receives a 1099-DA?

You may receive a 1099-DA if you sold, exchanged, or otherwise disposed of digital assets through a U.S.-based custodial broker. This includes:

- Cryptocurrency exchanges — Coinbase, Kraken, Gemini, Binance.US

- Payment apps with crypto features — PayPal, Venmo, Cash App, Robinhood

- Hosted wallet providers — platforms that store your digital assets on your behalf

- Digital asset kiosks — Bitcoin ATMs and similar machines

There is no minimum dollar threshold for Form 1099-DA. A broker may issue it for any covered sale or exchange, regardless of the amount. Qualifying stablecoin transactions below $10,000 in annual gross proceeds are exempt from broker reporting.

Important: Foreign exchanges (those based outside the U.S.) are generally not required to issue 1099-DA. Your tax reporting obligation remains the same regardless of which platform you used.

Brokers must furnish the form by January 31, or by February 15 if the form includes information in Box 8 or Box 10.

4. What Information Does It Report?

Form 1099-DA contains several boxes that detail each digital asset transaction:

| Box | Information Reported |

|---|---|

| 1a | Digital Token Identifier (DTIF) code |

| 1b | Name of the digital asset (e.g., Bitcoin, Ethereum) |

| 1c | Number of units sold or disposed of |

| 1d | Date acquired |

| 1e | Date sold or disposed |

| 1f | Gross proceeds |

| 1g | Cost or other basis |

| 2 | Check if basis was reported to the IRS (covered security) |

| 6 | Short-term or long-term gain/loss |

| 9 | Check if noncovered security |

You use the information from this form — along with your own records — to complete Form 8949 (Sales and Other Dispositions of Capital Assets) and Schedule D on your tax return.

5. Reporting Phases: Gross Proceeds vs. Cost Basis

The IRS is phasing in 1099-DA reporting requirements over time:

| Phase | What Brokers Must Report |

|---|---|

| Phase 1 | Gross proceeds only — cost basis reporting is optional |

| Phase 2 | Gross proceeds and cost basis for covered securities |

A digital asset qualifies as a covered security when it meets all of these conditions: it was acquired on or after January 1, 2026, the broker provided custodial services for it at the time of acquisition, and it was not transferred in from an external wallet.

Assets acquired before that date, or transferred into a broker from a personal wallet, are classified as noncovered securities. Brokers are not required to report cost basis for noncovered securities, though they may choose to do so voluntarily.

What this means for you: During Phase 1, most 1099-DA forms will show gross proceeds but leave cost basis blank. Without basis information, the IRS may treat your entire sale amount as taxable gain unless you report your own basis on Form 8949.

6. What 1099-DA Does Not Cover

Form 1099-DA only covers transactions processed by custodial brokers. The following types of digital asset activity are not reported on this form:

- Transactions in self-custody wallets (hardware wallets, non-custodial software wallets)

- DeFi (decentralized finance) swaps, liquidity pool activity, and lending

- Staking rewards — some may be reported on Form 1099-MISC instead

- Smart contract interactions and AMM (automated market maker) trades

- Cross-chain bridging

- Mining income

The IRS issued Notice 2024-57, which temporarily defers broker reporting obligations for certain “identified transactions” until further guidance is published. This deferral applies only to the broker’s reporting duty — not to the taxpayer’s obligation to report.

Even if you do not receive a 1099-DA for these activities, any income, gain, or loss must be reported on your tax return using Form 8949 and Schedule D.

7. Why You Must Track Your Own Cost Basis

During Phase 1, most 1099-DA forms will not include cost basis. When the broker reports only gross proceeds, the IRS sees the full sale amount — with no purchase price to offset it.

This is especially problematic for transferred-in assets. If you bought crypto on one platform and moved it to another exchange before selling, the receiving exchange does not know your original purchase price. The 1099-DA may show cost basis as $0 or blank. If you copy that figure onto your tax return, you will overstate your taxable gain.

Wallet-by-Wallet Basis Tracking

Under current IRS rules (Rev. Proc. 2024-28), cost basis must be tracked at the individual wallet or account level. The previous approach — pooling all holdings of the same asset across every wallet into one calculation — is no longer permitted.

The default method is FIFO (first in, first out), applied separately within each wallet. Taxpayers may instead use Specific Identification, which allows selecting particular lots for sale, but the choice must be documented at the time of the transaction and cannot be changed retroactively.

Bottom line: Do not prepare your tax return from the 1099-DA alone. Reconcile every form against your own wallet records, exchange transaction histories, and transfer logs. If cost basis appears as $0, replace it with your actual documented purchase price.

8. 1099-DA vs. 1099-B vs. 1099-K

| Feature | 1099-DA | 1099-B | 1099-K |

|---|---|---|---|

| What It Reports | Digital asset sales (crypto, NFTs, stablecoins) | Stocks, bonds, mutual funds, traditional securities | Gross payments via payment cards and third-party networks |

| Issued By | Crypto exchanges, hosted wallets | Brokerage firms | PayPal, Venmo, Etsy, payment processors |

| Includes Cost Basis? | Phase 2 only (covered securities) | Yes (covered securities) | No |

| Filed Using | Form 8949 + Schedule D | Form 8949 + Schedule D | Schedule C, Schedule 1, or other applicable form |

Before 1099-DA existed, some crypto exchanges reported digital asset transactions on Form 1099-B or 1099-K, which created confusion. Form 1099-DA now provides a dedicated reporting path for digital assets. Note that staking rewards and certain other crypto income may still be reported on Form 1099-MISC.

EA Insight

I’ll be honest about what this form changed on my side of the desk. Before 1099-DA existed, clients would walk in having traded on Coinbase or a similar exchange, and there was no clean transaction summary to work from. We had to add up every buy and sell by hand to reconstruct what actually happened during the year. It took hours, it drove up the fee the client paid, and frankly it was a frustrating way to spend a filing season. A standardized form that lays out proceeds by transaction is a real improvement — so if you receive one, bring it in.

That said, the form is a starting point, not the finish line. The most dangerous mistake I see now is copying the 1099-DA straight onto a return without checking cost basis. During Phase 1, most forms leave basis blank, and for anything you transferred in from an outside wallet, the broker has no record of what you originally paid — so it may show $0. Report that as-is and your taxable gain balloons. That is how an unexpected tax bill gets created out of nothing.

It also cuts the other way. Transactions that never show up on a 1099-DA — DeFi swaps, staking rewards, mining income, sales from a self-custody wallet — are still fully taxable. “I didn’t get a form” is not a position the IRS accepts.

So treat the 1099-DA as the best paperwork we have ever had for crypto, and still reconcile it against your own wallet and exchange records before anything goes on the return. If you use several platforms, gather all of it in one place ahead of filing season. Now that the IRS receives the same data, the gaps are far easier for them to spot.

Frequently Asked Questions

Do I have to report crypto if I didn’t receive a 1099-DA?

Yes. Whether or not you receive a form, you must report all income, gains, and losses from digital asset transactions on your federal income tax return. The IRS makes this clear in its guidance on Form 1099-DA.

Will I get a 1099-DA if I only bought crypto and didn’t sell?

No. Form 1099-DA is only issued when there is a sale, exchange, or other disposition. Simply purchasing and holding digital assets does not trigger the form.

What if the amounts on my 1099-DA don’t match my records?

Contact the issuing broker directly — the “Filer” information is shown in the top-left corner of the form. The IRS cannot correct your 1099-DA. Do not delay filing your return while waiting for a correction; file on time using your own accurate records, and amend later if needed.

Are DeFi transactions taxable even without a 1099-DA?

Yes. DeFi swaps, liquidity pool activity, staking rewards, and other on-chain transactions may generate taxable income or capital gains. Report them on Form 8949 and Schedule D regardless of whether a 1099-DA was issued.

What is the relationship between 1099-DA and Form 8949?

Form 1099-DA is the information return sent by the broker to you and the IRS. Form 8949 is the form you complete on your tax return to report each capital asset sale. You use the data from your 1099-DA(s) — verified against your own records — to fill out Form 8949, which then flows into Schedule D.

Can I receive more than one 1099-DA?

Yes. Each broker issues its own 1099-DA for transactions on its platform. If you used multiple exchanges, you will receive a separate form from each. You may also receive multiple forms from the same broker for different transactions. Report all of them on your tax return.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.