What Are Education Credits? AOTC vs. LLC Explained

Two federal tax credits can help offset the cost of higher education — but they work differently, and you can only use one per student per year. Choosing the wrong one, or missing key requirements, can cost you hundreds of dollars.

Key Takeaways

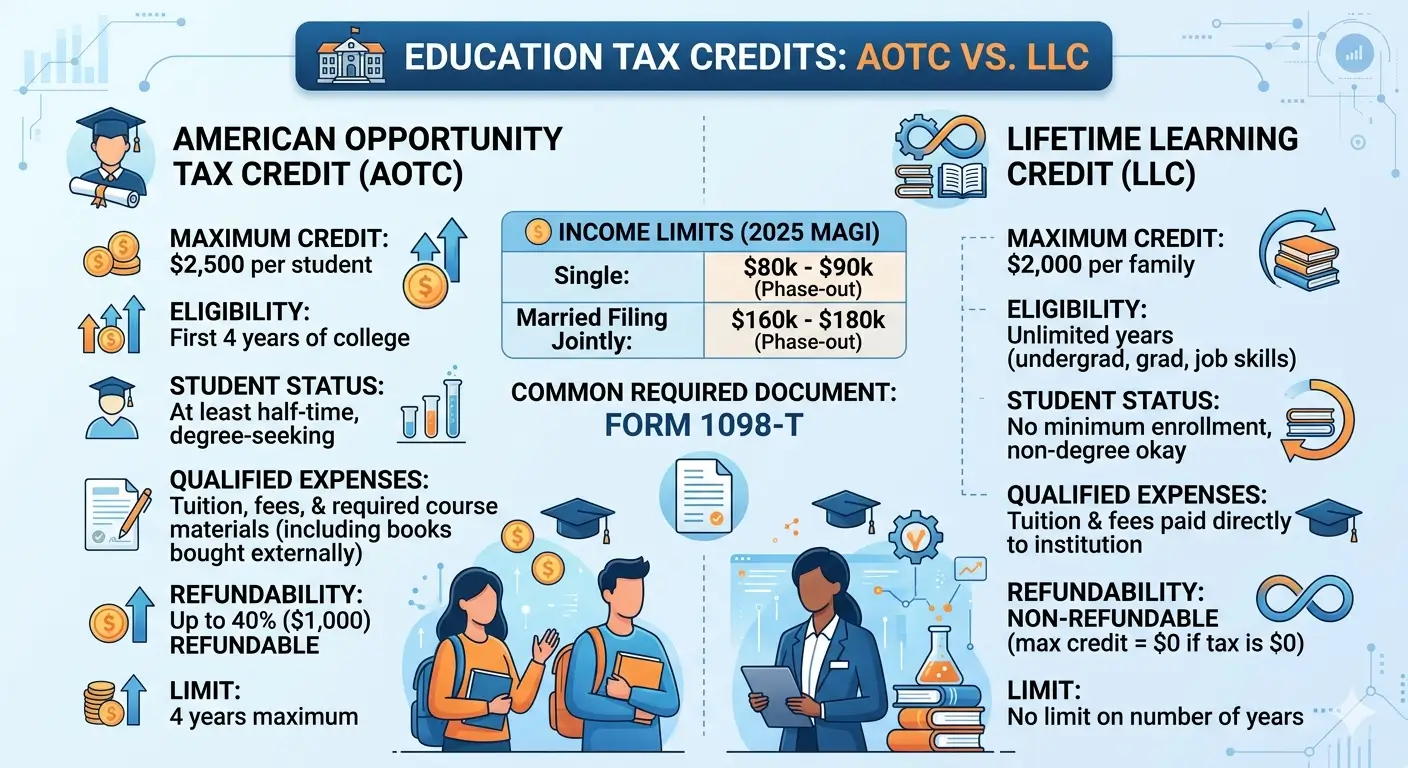

- The American Opportunity Tax Credit (AOTC) offers up to $2,500 per student — but only for the first four years of undergraduate education.

- The Lifetime Learning Credit (LLC) offers up to $2,000 per tax return and has no year or degree-level limit.

- You cannot claim both credits for the same student in the same tax year — you must choose one.

- AOTC is 40% refundable — you can receive up to $1,000 back even if you owe no tax. LLC is nonrefundable.

- Both credits phase out based on MAGI and require Form 1098-T from the school.

- If a student is claimed as a dependent, the parent — not the student — claims the credit.

Table of Contents

- 1. What Are Education Tax Credits?

- 2. American Opportunity Tax Credit (AOTC)

- 3. Lifetime Learning Credit (LLC)

- 4. AOTC vs. LLC — Side-by-Side Comparison

- 5. Who Claims the Credit — Parent or Student?

- 6. How Form 1098-T Affects Your Credit

- 7. EA Insight

- 8. Frequently Asked Questions

- 9. Related Articles

- 10. Official Resources

1. What Are Education Tax Credits?

Education tax credits are federal tax benefits that directly reduce the amount of income tax you owe — dollar for dollar. Unlike a deduction, which reduces the income subject to tax, a credit reduces your actual tax bill. That makes credits a more powerful tool for most taxpayers.

The IRS currently offers two education credits for higher education expenses:

- The American Opportunity Tax Credit (AOTC)

- The Lifetime Learning Credit (LLC)

Both credits are claimed on Form 8863 (Education Credits) and are based on qualified education expenses reported on Form 1098-T, which your school issues each year. Neither credit can be claimed for the same student in the same tax year — you must choose one.

2. American Opportunity Tax Credit (AOTC)

The AOTC is designed specifically for undergraduate students in the first four years of higher education. It is the larger of the two credits and includes a partial refund provision — making it the more valuable option for most families when eligible.

How the Credit Is Calculated

| Qualified Expenses | Credit Rate | Credit Amount |

|---|---|---|

| First $2,000 | 100% | $2,000 |

| Next $2,000 | 25% | $500 |

| Maximum Credit | — | $2,500 |

What Counts as a Qualified Expense?

AOTC covers a broader range of expenses than LLC:

- Tuition and enrollment fees

- Textbooks, supplies, and equipment required for a course — even if purchased outside the school (a bookstore, Amazon, etc.)

The following do not qualify: room and board, transportation, health insurance, and personal living expenses.

Eligibility Requirements

- The student must be enrolled at least half-time for at least one academic period during the tax year

- The student must be in the first four years of undergraduate education

- AOTC must not have been claimed for this student for more than four prior tax years

- The student must not have a felony drug conviction at the end of the tax year

- The student must be pursuing a degree or recognized credential

Income Limits (MAGI-Based)

| Filing Status | Full Credit | Partial Credit (Phase-Out) | No Credit |

|---|---|---|---|

| Single / Head of Household | $80,000 or less | $80,001 – $90,000 | Over $90,000 |

| Married Filing Jointly | $160,000 or less | $160,001 – $180,000 | Over $180,000 |

Note: Married Filing Separately taxpayers cannot claim the AOTC.

The Refundable Portion

AOTC is 40% refundable. This means that even if your tax liability is zero, you can still receive up to $1,000 as a refund. This is a meaningful benefit for students or lower-income households who may not owe much federal tax.

One exception: if a dependent student is subject to the Kiddie Tax (unearned income rules for dependents under age 19, or under 24 if a full-time student), the refundable portion of the AOTC may be reduced or eliminated for that student.

3. Lifetime Learning Credit (LLC)

The Lifetime Learning Credit is designed for flexibility. There is no limit on the number of years you can claim it, no half-time enrollment requirement, and no restriction on degree level. It works for undergraduate students, graduate students, and anyone taking a single course to improve job skills.

How the Credit Is Calculated

The LLC equals 20% of up to $10,000 in qualified education expenses, for a maximum credit of $2,000 per tax return.

Unlike AOTC, the LLC is calculated at the household level — not per student. Even if you have multiple students in college at the same time, the maximum LLC remains $2,000 total for the tax return.

What Counts as a Qualified Expense?

LLC covers tuition and enrollment fees. For course materials (textbooks, supplies, equipment) to qualify, they must be paid directly to the institution as a condition of enrollment or attendance. Textbooks purchased independently from an outside retailer do not qualify for LLC — this is a key difference from AOTC.

Eligibility Requirements

- No year limit — available for any year of postsecondary education

- No half-time enrollment requirement — even one course qualifies

- Available for undergraduate, graduate, and professional degree programs

- Available for courses taken to acquire or improve job skills — a degree is not required

- No felony drug conviction restriction

Income Limits (MAGI-Based)

| Filing Status | Full Credit | Partial Credit (Phase-Out) | No Credit |

|---|---|---|---|

| Single / Head of Household | $80,000 or less | $80,001 – $90,000 | Over $90,000 |

| Married Filing Jointly | $160,000 or less | $160,001 – $180,000 | Over $180,000 |

Note: LLC is nonrefundable. If the credit exceeds your tax liability, the excess is not refunded and cannot be carried forward. Married Filing Separately taxpayers cannot claim LLC.

4. AOTC vs. LLC — Side-by-Side Comparison

| Feature | AOTC | LLC |

|---|---|---|

| Maximum Credit | $2,500 per student | $2,000 per tax return |

| Year Limit | First 4 years of undergraduate only | No limit — any year, any level |

| Degree Requirement | Must be pursuing a degree or credential | Not required — job skills courses qualify |

| Half-Time Enrollment | Required | Not required |

| Textbook Expenses | Any retailer qualifies (Amazon, bookstore, etc.) | Only if paid directly to the school |

| Refundable? | Yes — 40% refundable (up to $1,000) | No — nonrefundable only |

| Drug Conviction Restriction | Yes — felony drug conviction disqualifies | No restriction |

| Income Phase-Out (Single) | $80,000 – $90,000 | $80,000 – $90,000 |

| Income Phase-Out (MFJ) | $160,000 – $180,000 | $160,000 – $180,000 |

| Filed On | Form 8863 (both credits) | |

5. Who Claims the Credit — Parent or Student?

The answer depends on whether the student is claimed as a dependent on someone else’s tax return.

If a parent claims the student as a dependent, the parent must claim the education credit on the parent’s return. The student cannot claim it on their own return. The credit follows the dependent — whoever claims the student claims the credit.

If the student files as an independent taxpayer (not claimed as a dependent by anyone), the student claims the credit on their own return. This can be advantageous when the student has meaningful tax liability, especially with AOTC’s refundable component.

Important: If a parent is eligible to claim the student as a dependent but chooses not to, the student still cannot claim the education credit. The credit is only available to the student if no one is eligible to claim them — not merely if someone chooses not to.

The Academic Period Rule

Qualified education expenses are generally deductible in the year they are paid, not the year the academic period begins. However, there is an important exception: expenses paid in one tax year for an academic period that begins in the first three months of the following tax year also qualify.

For example, tuition paid in December for a spring semester that begins in January or February of the next year can be claimed as a credit for the year in which payment was made. This timing rule gives families flexibility in planning when to make payments.

6. How Form 1098-T Affects Your Credit

Your school issues Form 1098-T (Tuition Statement) each year to report education-related amounts to both you and the IRS. Two boxes matter most for calculating education credits:

- Box 1 — Amounts paid for qualified tuition and related expenses during the tax year

- Box 5 — Scholarships and grants received

The starting point for your qualified education expenses is generally:

Qualified Expenses = Box 1 − Box 5

If scholarships and grants (Box 5) exceed the tuition paid (Box 1), there may be no remaining qualified expenses to support a credit.

Box 1 May Not Reflect What You Actually Paid

One detail that catches many families off guard: the amount in Box 1 on your 1098-T may not match your actual out-of-pocket payments. Schools use different accounting methods, and timing differences between when charges are billed and when payments are processed can cause discrepancies.

Before calculating your credit, cross-reference your 1098-T against your school’s student account (bursar’s) statement for the year. The bursar’s statement is your most accurate record of what was actually paid and when. If the two figures differ, the bursar’s statement typically provides the better basis for your credit calculation.

Taxable Scholarships

If a scholarship or grant exceeds the student’s qualified education expenses — for example, it covers not just tuition but also room and board — the excess amount is generally includible in the student’s gross income as a taxable scholarship. This can create a tax liability for the student even if no W-2 is issued. It also affects the net qualified expenses available for the education credit calculation.

EA Insight

The single most common error I see with education credits is claiming AOTC for a student who has already used it four times. The IRS tracks prior claims, and if you claim it a fifth time, the credit will be disallowed — and you may be required to repay the refunded amount with interest and penalties. Before filing, confirm exactly how many prior tax years AOTC was claimed for that student.

The second issue is failing to subtract scholarships from Box 1 before calculating the credit. I regularly see returns where Box 1 is used as-is, without subtracting Box 5. If the school reported $20,000 in tuition paid but also provided $18,000 in scholarships, the actual qualified expenses for credit purposes may be only $2,000 — not $20,000. The IRS matches Form 1098-T against what you report, and discrepancies get flagged.

Finally, don’t assume AOTC is always the better choice simply because the maximum is higher. For a graduate student, a professional returning to school part-time, or someone with high enough tax liability that the nonrefundable LLC fully offsets their bill, LLC may be the more practical option. Compare both calculations before deciding.

Frequently Asked Questions

Can I claim both AOTC and LLC in the same year?

No. You cannot claim both credits for the same student in the same tax year. If you have multiple students — for example, two children in college simultaneously — you can claim AOTC for one and LLC for the other, but you must choose one per student.

My child’s scholarship covers all tuition. Can I still claim a credit?

If tax-free scholarships fully cover tuition and all qualified expenses, there may be no remaining qualified expenses on which to base a credit. However, if any part of the scholarship is taxable (for example, amounts covering room and board), you may be able to allocate expenses in a way that preserves some credit. This is a nuanced calculation that a tax professional can help with.

Who claims the education credit — parent or student?

If the student is claimed as a dependent on the parent’s return, the parent claims the credit. The student cannot claim it separately. If the student files independently and no one is eligible to claim them as a dependent, the student claims the credit on their own return.

Does room and board count as a qualified education expense?

No. Neither AOTC nor LLC allows room and board, transportation, insurance, or general living expenses. Only tuition, required fees, and — for AOTC — required course materials qualify.

What happens if I have already used AOTC four times?

You are no longer eligible for AOTC for that student. You may still be eligible for the Lifetime Learning Credit, provided you meet the income and enrollment requirements. The IRS tracks prior AOTC claims, so claiming it a fifth time will result in the credit being disallowed.

Can graduate students claim an education credit?

Graduate students are not eligible for AOTC, which is limited to the first four years of undergraduate education. However, they may qualify for the Lifetime Learning Credit, which has no restrictions on degree level or year of study.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.