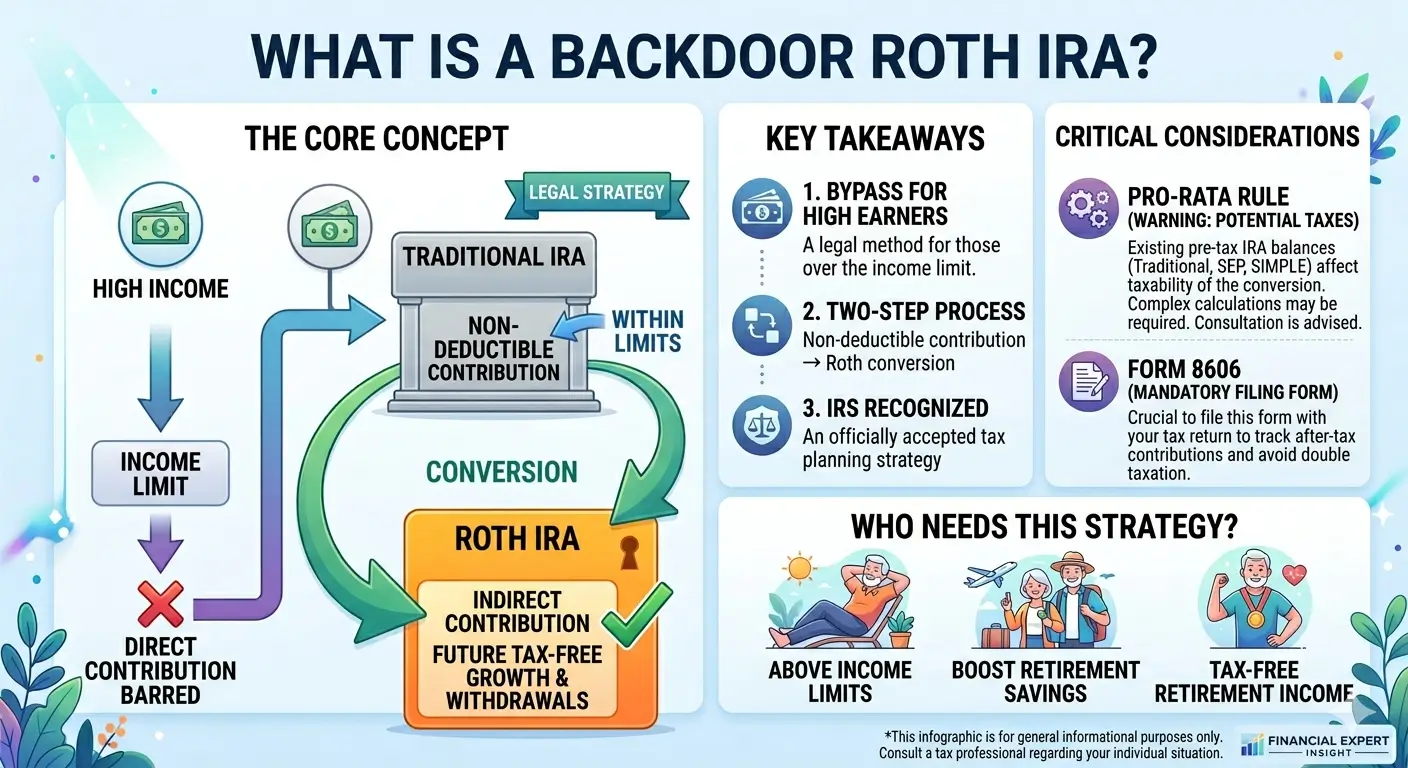

What Is a Backdoor Roth IRA?

Roth IRA contributions are off-limits once your income exceeds a certain threshold — but that does not mean high earners have no path to a Roth. The Backdoor Roth IRA is a legal, IRS-recognized strategy that lets you fund a Roth IRA regardless of your income. Done correctly, it works exactly as intended. Done carelessly, it triggers an unexpected tax bill.

Key Takeaways

- A Backdoor Roth IRA is a two-step strategy: contribute to a nondeductible Traditional IRA, then convert it to a Roth IRA.

- There are no income limits on IRA-to-Roth conversions — anyone can convert regardless of MAGI.

- The Pro-Rata Rule is the critical trap: existing pre-tax balances in any Traditional IRA, SEP IRA, or SIMPLE IRA affect how much of the conversion is taxable. Balances are measured as of December 31 of the conversion year.

- Form 8606 must be filed every year you make a nondeductible contribution or complete a conversion — this is what protects you from being taxed twice.

- The strategy is fully legal and recognized by the IRS. Congress has acknowledged it in legislative history.

- A separate strategy — the Mega Backdoor Roth — uses after-tax 401(k) contributions and can allow significantly larger amounts to reach a Roth account.

Table of Contents

1. What Is a Backdoor Roth IRA?

A Backdoor Roth IRA is not a special type of account — it is a two-step process that allows high-income earners to fund a Roth IRA indirectly when their income exceeds the IRS limit for direct Roth contributions.

The steps are straightforward: first, you make a nondeductible contribution to a Traditional IRA; then, you convert that Traditional IRA to a Roth IRA. Because there is no income limit on IRA-to-Roth conversions, the restriction on direct Roth contributions is effectively bypassed.

“Backdoor Roth” is not an official IRS term — it is a widely used informal name for this strategy. However, the IRS has acknowledged the approach, and Congress referenced it explicitly in legislative history when considering (and ultimately rejecting) proposals to eliminate it. As of now, the strategy is fully legal.

2. Who Needs a Backdoor Roth IRA?

The Backdoor Roth is primarily relevant for taxpayers whose MAGI exceeds the Roth IRA contribution phase-out range:

| Filing Status | Phase-Out Range | Direct Roth Contribution Not Allowed Above |

|---|---|---|

| Single / Head of Household | $153,000 – $168,000 | $168,000 |

| Married Filing Jointly | $242,000 – $252,000 | $252,000 |

| Married Filing Separately | $0 – $10,000 | $10,000 |

If your income falls within the phase-out range, your direct Roth contribution limit is reduced proportionally. Above the upper threshold, direct contributions are not permitted at all. The Backdoor Roth provides an alternative path for both groups.

3. How It Works: Step by Step

The Backdoor Roth IRA involves two distinct transactions, typically completed in the same tax year.

| Step | Action | Notes |

|---|---|---|

| 1 | Make a nondeductible contribution to a Traditional IRA | Up to $7,500 (under 50) or $8,600 (50 and older). No income limit on contributions — only on deductibility. |

| 2 | Report the nondeductible contribution on Form 8606 | This establishes your “basis” — the after-tax dollars you put in. Without this record, you may be taxed again on the same money when you convert or withdraw. |

| 3 | Convert the Traditional IRA to a Roth IRA | Contact your brokerage and request a Roth conversion. No income limit applies to conversions. Converting promptly after contribution minimizes any taxable earnings that accumulate between the two steps. |

| 4 | Report the conversion on Form 8606 | The conversion amount is reported on your tax return. If you converted immediately and had no earnings, the taxable portion is $0. Any earnings accumulated before conversion are taxable as ordinary income. |

Timing tip: Converting promptly after the nondeductible contribution — sometimes called a “clean” conversion — minimizes the chance of taxable earnings building up between the two steps. Any investment gain or interest that accumulates in the Traditional IRA before you convert is taxable ordinary income at the time of conversion.

4. The Pro-Rata Rule — The Most Important Trap

The Pro-Rata Rule is the most commonly misunderstood aspect of the Backdoor Roth. Many taxpayers assume that because they contributed nondeductible (after-tax) dollars, the entire conversion is tax-free. That assumption is wrong if you have any other pre-tax IRA balances.

How the Rule Works

The IRS does not allow you to selectively convert only your nondeductible dollars. When calculating the taxable portion of a Roth conversion, the IRS aggregates all of your IRA balances — including Traditional IRAs, SEP IRAs, and SIMPLE IRAs — and applies a proportional formula:

Tax-free percentage = Total nondeductible (after-tax) basis ÷ Total IRA balance across all accounts

Example

You contribute $7,500 to a nondeductible Traditional IRA. You also have an existing Traditional IRA with a pre-tax balance of $92,500. Your total IRA balance is $100,000. Your nondeductible basis is $7,500.

| Item | Amount |

|---|---|

| New nondeductible contribution | $7,500 |

| Existing pre-tax Traditional IRA balance | $92,500 |

| Total IRA balance | $100,000 |

| Tax-free percentage ($7,500 ÷ $100,000) | 7.5% |

| Tax-free portion of $7,500 conversion | $563 |

| Taxable portion of $7,500 conversion | $6,937 |

Important — Balance Date: The Pro-Rata calculation uses your total IRA balance as of December 31 of the year in which the conversion occurs — not the date of the contribution or the date of the conversion. This means that if you roll funds into an IRA later in the same calendar year, that balance is included in the calculation even if the rollover happened after the conversion.

Accounts Included in the Calculation

The aggregation rule applies to all pre-tax IRA balances you hold under your own name: Traditional IRAs, SEP IRAs, and SIMPLE IRAs. A spouse’s IRA balances are not included — the rule applies to each person separately.

How to Resolve the Pro-Rata Problem

If your existing pre-tax IRA balance makes the Backdoor Roth inefficient, one solution is to roll those pre-tax IRA funds into your employer’s 401(k) plan before year-end. Once those balances are moved out of your IRA, they are no longer part of the Pro-Rata calculation. This approach works only if your employer’s plan accepts incoming IRA rollovers — not all plans do.

5. Form 8606 — Why It Matters

Form 8606, Nondeductible IRAs, is the document that tells the IRS how much after-tax money (basis) you have accumulated in your IRAs. Without this record, the IRS has no way to distinguish your after-tax contributions from pre-tax contributions — and may tax the same dollars twice when you withdraw them.

When You Must File Form 8606

- Any year you make a nondeductible contribution to a Traditional IRA

- Any year you convert a Traditional IRA (or SEP or SIMPLE IRA) to a Roth IRA

- Any year you take a distribution from a Traditional IRA and you have prior nondeductible contributions on record

Think of It as a Running Ledger

Form 8606 functions as a cumulative record of your IRA basis. Each year’s form carries forward the basis from prior years. This is why the form — and accurate recordkeeping — must be maintained for as long as you hold any IRA.

Missed a prior year? If you made nondeductible IRA contributions in past years but never filed Form 8606, it is not too late. You can file a late or amended Form 8606 for those prior years to establish your basis on record. Doing so protects you from double taxation on those after-tax dollars when you eventually convert or withdraw. The penalty for failure to file Form 8606 when required is $50 per occurrence.

6. What About the Mega Backdoor Roth?

The Mega Backdoor Roth is a separate, more complex strategy that also routes after-tax money into a Roth account — but through a 401(k) plan rather than an IRA.

Here is how it works at a high level: some employer 401(k) plans allow after-tax contributions beyond the standard employee deferral limit. If the plan also permits in-service withdrawals or in-plan Roth conversions, those after-tax contributions can be rolled into a Roth IRA or converted to a Roth 401(k).

| Feature | Standard Backdoor Roth | Mega Backdoor Roth |

|---|---|---|

| Vehicle | Traditional IRA → Roth IRA | 401(k) after-tax → Roth IRA or Roth 401(k) |

| Annual Limit | $7,500 / $8,600 (IRA limit) | Up to $72,000 total (Section 415(c) limit, including employer contributions) |

| Availability | Available to anyone with earned income | Only if employer plan allows after-tax contributions and in-service distributions |

| Pro-Rata Rule | Applies if pre-tax IRA balances exist | Generally not an issue for after-tax 401(k) amounts |

The Mega Backdoor Roth is a powerful tool for high earners whose employer plan supports it — but it is not available to everyone. Whether your plan allows the necessary features requires reviewing your Summary Plan Description or asking your plan administrator directly.

EA Insight

The most common mistake I see with Backdoor Roth conversions is the assumption that nondeductible equals tax-free. Clients complete the contribution, convert immediately, and then are surprised when there is a taxable amount on their return. The culprit is almost always a forgotten SEP IRA or an old rollover IRA sitting at a different institution. The Pro-Rata Rule does not care which account you convert from — it looks at everything. And it uses the December 31 balance, which means a rollover you receive late in the year can retroactively change your tax exposure for a conversion you already completed months earlier.

Form 8606 is not a formality — it is the only legal record establishing that your nondeductible contributions have already been taxed. I have seen situations where a taxpayer made nondeductible contributions for years without filing the form, then faced a fully taxable distribution because there was no documented basis. The fix is to file late Forms 8606 for each missed year, which is allowed. If you are in this situation, address it before your next withdrawal or conversion, not after.

On the question of whether the Backdoor Roth will be eliminated: it has survived multiple legislative attempts so far. I do not advise making rushed financial decisions based on what Congress might do. Execute the strategy correctly, document it thoroughly, and let the tax benefits accumulate. The risk of doing it sloppily is far more immediate than the risk of future law changes.

Frequently Asked Questions

Is the Backdoor Roth IRA legal?

Yes. The strategy uses two provisions that are each independently allowed under the tax code: nondeductible Traditional IRA contributions (which have no income limit) and IRA-to-Roth conversions (which also have no income limit). Congress has acknowledged the strategy in legislative history. It is not a loophole in the sense of exploiting an unintended gap — it is a straightforward application of existing law.

Can married couples each do a Backdoor Roth?

Yes. Each spouse can independently execute a Backdoor Roth using their own IRA. The Pro-Rata Rule applies separately to each spouse — one spouse’s IRA balances do not affect the other’s calculation. Both spouses can contribute up to the individual IRA limit, provided they have sufficient combined earned income and file a joint return.

How does the five-year rule apply to Backdoor Roth conversions?

Each Roth conversion has its own separate five-year clock for determining whether the converted amount can be withdrawn penalty-free before age 59½. This is different from the five-year rule that applies to Roth IRA earnings. For taxpayers who are already 59½ or older, the conversion five-year rule generally does not apply to withdrawals. For younger taxpayers, converted amounts withdrawn before five years are subject to a 10% early withdrawal penalty on the converted portion (not the original contribution basis).

I already have a large Traditional IRA balance. Should I still do a Backdoor Roth?

It depends. If your existing pre-tax IRA balance is large relative to your nondeductible contribution, the Pro-Rata Rule will result in most of the conversion being taxable — significantly reducing the strategy’s benefit. In that case, consider whether rolling your pre-tax IRA funds into an employer 401(k) plan is feasible before proceeding. If your employer’s plan does not accept IRA rollovers, the Backdoor Roth may not be worth executing until that balance is reduced through distributions or conversions in lower-income years.

Can I do a Backdoor Roth every year?

Yes. There is no restriction on repeating this strategy annually. Each year, you can make a new nondeductible contribution to a Traditional IRA up to the annual limit and then convert it to a Roth IRA. As long as you file Form 8606 each year and monitor your pre-tax IRA balances for Pro-Rata purposes, the strategy can be repeated indefinitely.

What happens if I forget to file Form 8606?

Failing to file Form 8606 when required carries a $50 penalty per occurrence. More significantly, without the form on record, you have no documented proof of your after-tax basis — which means the IRS may treat the entire amount as taxable when you later convert or withdraw. If you missed filing in prior years, you can submit a late Form 8606 for each affected year. This is the correct way to establish basis retroactively and protect yourself from double taxation.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.