What Is Tax-Exempt Income?

Tax-exempt income is money you receive that the federal government does not count as taxable — meaning you owe no federal income tax on it. But “exempt” does not mean invisible to the IRS, and it does not always mean free from state tax or free from every calculation that shapes your tax bill. Knowing exactly what qualifies — and why — matters more than most taxpayers realize.

Key Takeaways

- Tax-exempt income is excluded from federal gross income — you pay no federal income tax on it.

- Common examples include municipal bond interest, qualified Roth IRA distributions, life insurance death benefits, gifts and inheritances received, workers’ compensation, and child support.

- Tax-exempt and tax-deferred are not the same. Traditional 401(k) and IRA withdrawals are taxed in full at distribution — they are deferred, not exempt.

- Even if income is federally tax-exempt, your state may still tax it.

- Some tax-exempt income — particularly municipal bond interest — is added back when calculating MAGI, which can reduce eligibility for credits, deductions, and retirement account contributions.

- IRS Publication 525 is the primary reference for what counts as taxable or nontaxable income.

Table of Contents

1. What Is Tax-Exempt Income?

Tax-exempt income is income that federal law specifically excludes from gross income under the Internal Revenue Code. Because it is excluded from gross income, it does not appear on the taxable income line of your Form 1040, and no federal income tax is owed on it.

The IRS covers this topic in detail in Publication 525, Taxable and Nontaxable Income, and Publication 17, Your Federal Income Tax. These publications distinguish between income that must be included in gross income and income that may legally be excluded.

Two important caveats apply to almost every type of tax-exempt income:

- State taxation may still apply. Federal tax exemption does not automatically extend to your state’s income tax. States set their own rules, and many tax income that the federal government exempts.

- Exempt income is not necessarily invisible to the IRS. Some types must be reported on your return even though they are not taxed — and others factor into calculations that determine how much tax you owe on other income.

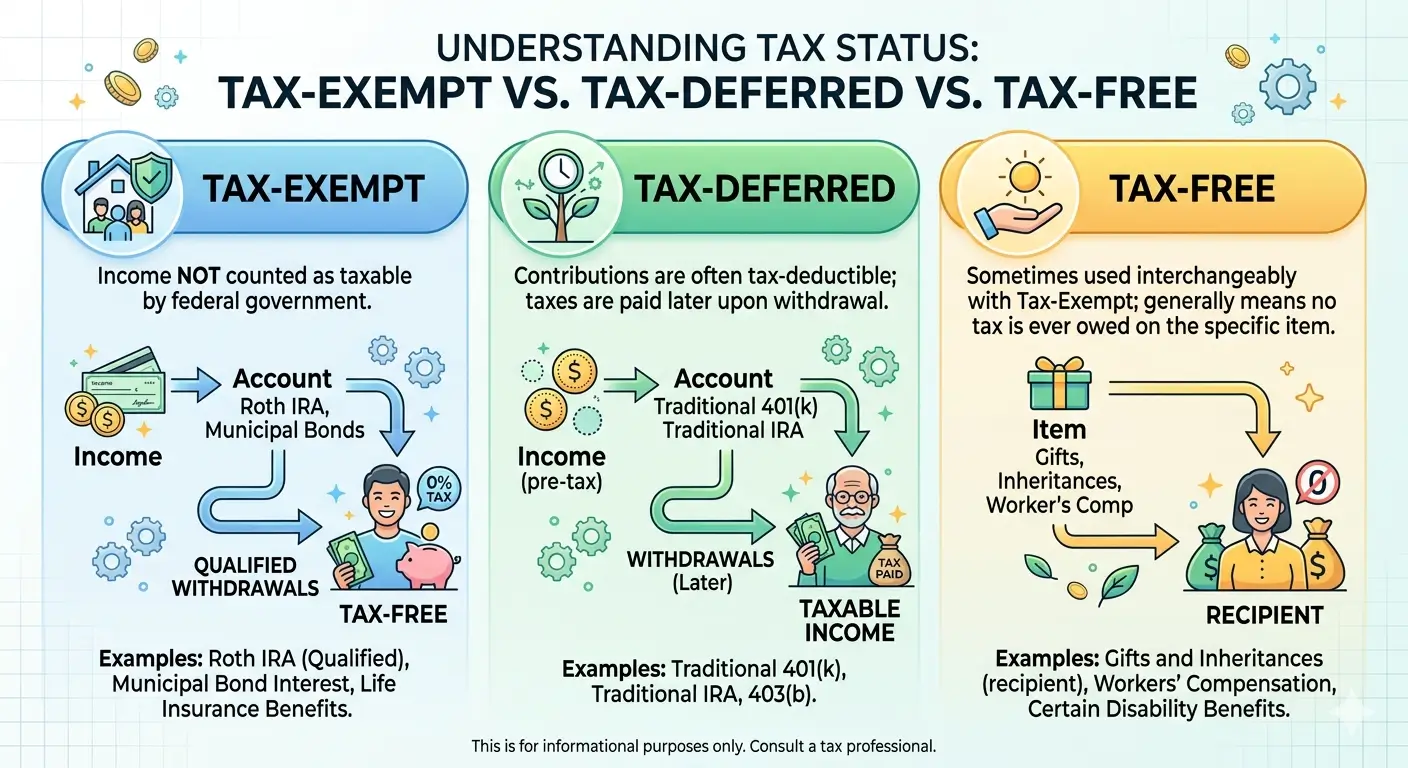

2. Tax-Exempt vs. Tax-Deferred vs. Tax-Free

These three terms are often used interchangeably, but they describe meaningfully different outcomes.

| Term | What It Means | Examples |

|---|---|---|

| Tax-Exempt | Never subject to federal income tax — excluded from gross income entirely | Municipal bond interest, qualified Roth IRA distributions |

| Tax-Deferred | Not taxed now, but fully taxable when withdrawn | Traditional 401(k) and Traditional IRA distributions |

| Tax-Free | Often used as a synonym for tax-exempt in everyday language | Roth IRA qualified distributions, HSA withdrawals for qualified medical expenses |

The most important distinction in practice is between tax-exempt and tax-deferred. Traditional 401(k) and Traditional IRA contributions reduce your taxable income today — but every dollar you withdraw in retirement is taxed as ordinary income. These accounts are not tax-exempt; the tax is simply postponed. Confusing the two leads to significant planning errors.

3. Common Types of Tax-Exempt Income

Municipal Bond Interest

Interest earned on bonds issued by state and local governments — known as municipal bonds or “munis” — is excluded from federal gross income under IRC §103. This interest is reported in Box 8 (Tax-Exempt Interest) on Form 1099-INT, and it must be listed on Schedule B even though no federal tax is owed on it.

Important: Municipal bond interest from another state’s bonds may be taxable in your home state. Additionally, this interest is added back into MAGI for several key calculations — including Roth IRA eligibility and Medicare premium surcharges (IRMAA). A large muni bond portfolio can quietly phase out benefits you expected to keep.

Qualified Roth IRA Distributions

Because Roth IRA contributions are made with after-tax dollars, qualified distributions — both contributions and earnings — are excluded from federal income. A distribution is “qualified” when the account has been open for at least five years and the account holder is age 59½ or older (or meets another qualifying exception such as death or disability). Roth 401(k) accounts follow similar rules.

Life Insurance Death Benefits

When a policyholder dies, the lump-sum death benefit paid to the beneficiary is generally excluded from federal income under IRC §101(a). One exception: employer-provided group term life insurance coverage above $50,000. The imputed cost of coverage exceeding that threshold is included in the employee’s taxable income and reported in Box 12, Code C on Form W-2.

Gifts and Inheritances Received

From the recipient’s perspective, money or property received as a gift or inheritance is not federal taxable income. Any gift tax obligation belongs to the donor, not the recipient. However, if you later sell inherited property, capital gains tax may apply — calculated from the property’s fair market value at the time of inheritance (the stepped-up basis), not the original purchase price.

Workers’ Compensation

Amounts received under a state workers’ compensation law for a job-related injury or illness are excluded from federal income. This exclusion also applies to payments to survivors of a worker who died from a work-related cause.

Child Support Received

Child support payments received are not included in the recipient’s gross income. The paying parent also receives no deduction for child support. This is the opposite of the treatment that applied to alimony under prior law, and the distinction matters at tax time.

Alimony Received (Post-2018 Agreements)

For divorce or separation agreements executed after December 31, 2018, alimony received is no longer included in the recipient’s federal gross income. (Under prior law, alimony received was taxable to the recipient and deductible by the payer. That treatment still applies to pre-2019 agreements that have not been modified.)

Employer-Paid Health Insurance Premiums

Premiums your employer pays for your health coverage are excluded from your taxable wages. Amounts you contribute through a Section 125 cafeteria plan — deducted from your paycheck on a pre-tax basis — are also excluded from federal income and, in most cases, from FICA taxes as well.

Disability Benefits

The taxability of disability benefits depends on who paid the premiums. If you paid the premiums entirely with after-tax dollars, benefits you receive are tax-exempt. If your employer paid the premiums — or you paid with pre-tax dollars — the benefits are taxable. When both you and your employer share the cost, only the portion attributable to employer-paid premiums is taxable.

Combat Pay (Military)

Compensation received by active-duty military personnel for service in a designated combat zone is excluded from federal income. This exclusion applies to enlisted members for all combat pay, and to officers up to the highest enlisted pay grade plus any hostile fire or imminent danger pay received.

4. How Tax-Exempt Income Can Still Affect Your Taxes

One of the most misunderstood aspects of tax-exempt income is that “exempt from federal income tax” does not mean “irrelevant to your overall tax situation.” Several types of exempt income are added back into MAGI for specific purposes.

Where tax-exempt income reappears in MAGI calculations

- Roth IRA contribution eligibility: Municipal bond interest is added back to calculate MAGI, which determines whether — and how much — you can contribute to a Roth IRA.

- Social Security taxability: Municipal bond interest is included in the combined income formula that determines what percentage of your Social Security benefit is taxable (up to 85%).

- Medicare Part B and D premiums (IRMAA): Higher MAGI — including muni bond interest — can trigger surcharges on Medicare premiums. This surprises many retirees who hold large muni bond portfolios assuming the income is invisible to the IRS.

- Premium Tax Credit (ACA): Some exempt income is included in household income for marketplace subsidy calculations.

The practical takeaway: tax-exempt income reduces your current federal tax bill, but it can quietly erode other tax advantages if it pushes your MAGI past key thresholds.

5. Taxable vs. Tax-Exempt at a Glance

| Income Type | Federal Income Tax |

|---|---|

| Municipal bond interest | ✅ Exempt |

| Qualified Roth IRA distributions | ✅ Exempt |

| Life insurance death benefit | ✅ Exempt |

| Gifts and inheritances received | ✅ Exempt |

| Workers’ compensation | ✅ Exempt |

| Child support received | ✅ Exempt |

| Alimony received (post-2018 agreements) | ✅ Exempt |

| Employer-paid health insurance premiums | ✅ Exempt |

| Traditional IRA / 401(k) withdrawals | ❌ Fully taxable |

| Unemployment compensation | ❌ Fully taxable |

| Social Security benefits | ⚠️ Up to 85% taxable depending on income |

| Disability benefits | ⚠️ Depends on who paid the premiums |

EA Insight

Tax-exempt income comes up in almost every client meeting I have, and the same two misunderstandings appear repeatedly.

The first is the municipal bond trap. Clients with significant muni bond holdings often assume that because the interest is “tax-free,” it has no effect on their broader tax picture. It does. That interest is added back into MAGI for purposes of Roth IRA contribution limits, Social Security taxability, and Medicare premium surcharges (IRMAA). A retired couple with $80,000 in muni bond interest may find themselves paying significantly higher Medicare Part B premiums the following year — not because they earned more in the conventional sense, but because that interest is factored into the IRMAA calculation. Planning for this in advance, ideally before the income is realized, makes a measurable difference.

The second is the tax-exempt versus tax-deferred confusion. Every year, clients ask me why their Traditional IRA withdrawal is on their tax return if they “already paid taxes on it.” In most cases, they contributed pre-tax dollars — meaning they never paid taxes on those funds. The deduction they took at contribution time is exactly what gets recaptured when they withdraw. A Roth IRA, by contrast, is funded with after-tax dollars, which is why qualified withdrawals are genuinely tax-exempt. Mixing up these two accounts in retirement planning leads to surprise tax bills.

Finally, a reporting reminder: tax-exempt does not mean unreported. Municipal bond interest must appear on Schedule B even though it generates no federal tax. The IRS receives a copy of your 1099-INT and knows the exempt interest was paid. Omitting it from your return creates a mismatch that can trigger a notice — and explains why tax-exempt income is never truly invisible.

Frequently Asked Questions

Is municipal bond interest really tax-free?

Municipal bond interest is exempt from federal income tax under IRC §103. However, it may be taxable at the state level — particularly if the bond was issued by a different state than where you live. It must also be reported on Schedule B of your federal return, and it is added back into MAGI for several important calculations including Medicare premium surcharges (IRMAA) and Roth IRA eligibility.

Do I have to report tax-exempt income on my tax return?

In many cases, yes. Municipal bond interest, for example, must be listed on Schedule B even though no federal tax is owed on it. The IRS receives a copy of your 1099-INT from the paying institution and uses it to verify your return. Omitting exempt income that appears on an information return can trigger a mismatch notice.

Is a Roth IRA withdrawal always tax-exempt?

Only if it is a qualified distribution. A Roth IRA distribution is qualified — and therefore fully tax-exempt — when the account has been open for at least five years and you are age 59½ or older (or meet another qualifying exception such as death or disability). Early withdrawals of earnings that do not meet these conditions may be subject to income tax and a 10% early withdrawal penalty. Contributions — not earnings — can always be withdrawn tax- and penalty-free at any time.

Does tax-exempt income affect my eligibility for credits or deductions?

Yes, for certain credits and thresholds. Municipal bond interest is added back into MAGI when determining Roth IRA contribution limits, Social Security taxability, and Medicare Part B and D premium surcharges (IRMAA). Tax-exempt income that increases MAGI can phase out benefits you expected to receive, even though no direct tax is owed on that income.

Is Social Security income tax-exempt?

Not entirely. Depending on your combined income — adjusted gross income plus nontaxable interest plus half of your Social Security benefits — up to 85% of your Social Security benefit may be subject to federal income tax. If your combined income is below the applicable threshold, none of your benefit is taxable. A detailed breakdown of these thresholds will be covered in a separate post on Social Security income.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.