What Is Self-Employment Tax?

When you work for yourself, there is no employer to split your Social Security and Medicare taxes. Self-employment tax means you pay both sides — the full 15.3% — out of your own pocket. Understanding how it works is the first step to avoiding an unexpected tax bill.

Key Takeaways

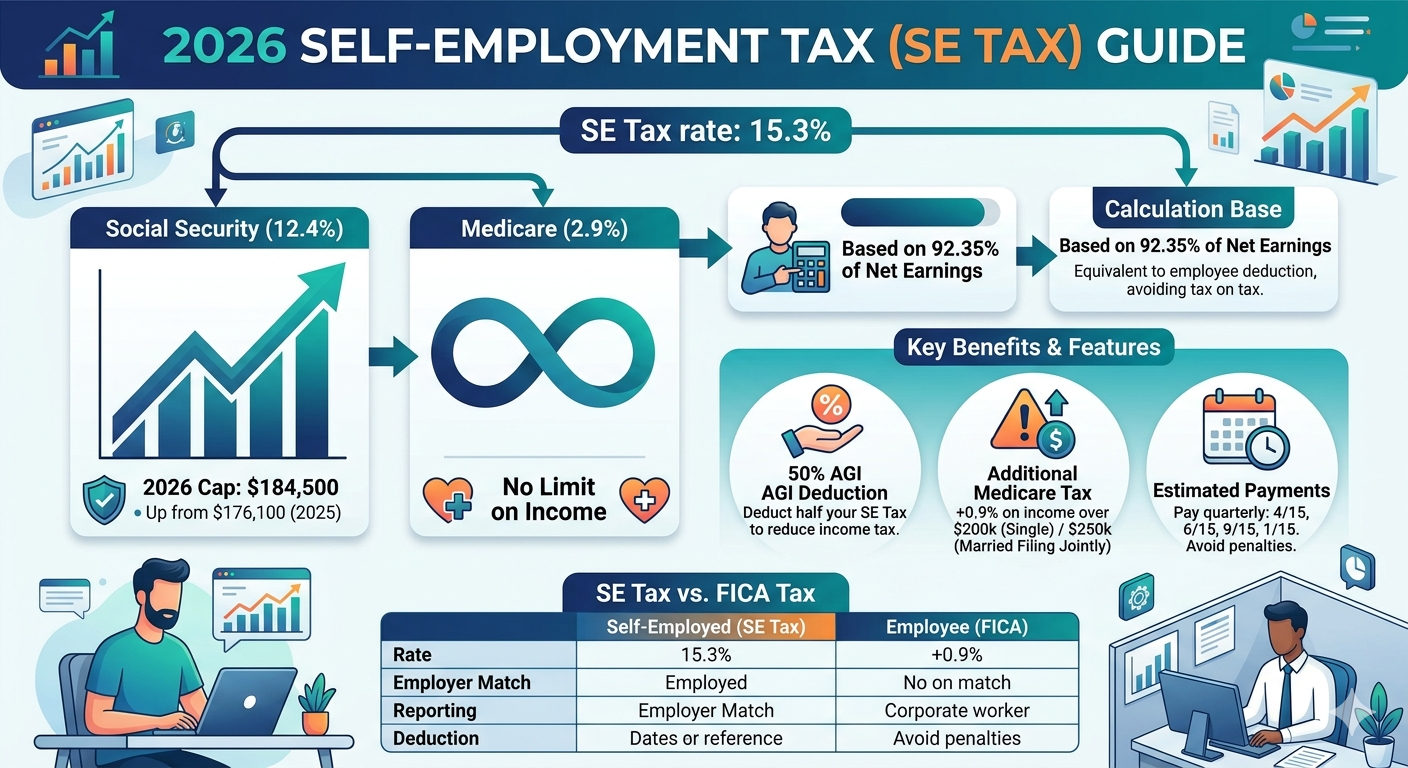

- Self-employment tax (SE tax) consists of Social Security (12.4%) and Medicare (2.9%), for a combined rate of 15.3%.

- SE tax applies to 92.35% of net self-employment income — not the full amount.

- The Social Security portion applies only up to $184,500 in net earnings (2026). Medicare has no cap.

- You can deduct 50% of SE tax from your gross income, which reduces your adjusted gross income (AGI).

- Any net self-employment income of $400 or more triggers the SE tax filing requirement.

- If you also have W-2 wages, your W-2 Social Security withholding counts toward the $184,500 wage base limit.

- SE tax is calculated on Schedule SE and reported on Form 1040.

Table of Contents

- 1. What Is Self-Employment Tax?

- 2. Who Pays Self-Employment Tax?

- 3. SE Tax Rate and Wage Base (2026)

- 4. How to Calculate Self-Employment Tax: The 92.35% Rule

- 5. The 50% SE Tax Deduction

- 6. Additional Medicare Tax

- 7. Schedule SE: How to File

- 8. Quarterly Estimated Tax Payments

- 9. When You Have Both W-2 Wages and Self-Employment Income

- 10. SE Tax vs. FICA: Side-by-Side Comparison

- 11. EA Insight

- 12. Frequently Asked Questions

- 13. Related Articles

- 14. Official Resources

1. What Is Self-Employment Tax?

Self-employment tax (SE tax) is the tax that self-employed individuals pay to fund Social Security and Medicare — the same programs that FICA taxes fund for traditional employees.

When you work as a W-2 employee, your employer withholds half of the FICA tax from your paycheck and pays the other half on your behalf. As a self-employed person, there is no employer to split the cost. Under the Self-Employment Contributions Act (SECA), you are responsible for both the employee and employer portions — the entire 15.3%.

SE tax is separate from federal income tax. You pay both. Forgetting to account for SE tax when estimating your annual tax bill is one of the most common and costly mistakes freelancers make.

2. Who Pays Self-Employment Tax?

You are subject to SE tax if you have net self-employment income of $400 or more in a tax year. This includes:

- Freelancers and independent contractors — those who receive Form 1099-NEC

- Sole proprietors — individuals operating a business under their own name

- Single-member LLC owners — taxed as sole proprietors by default

- Partners in a partnership — on their distributive share of partnership income

- Gig workers — rideshare drivers, delivery couriers, and similar on-demand workers

The $400 threshold is low by design. Even occasional or part-time self-employment income triggers the SE tax obligation once it clears that amount.

Note: Church employees follow a different threshold. If you are an employee of a church and received wages of $108.28 or more, SE tax rules may apply to you under a separate provision.

3. SE Tax Rate and Wage Base (2026)

Self-employment tax consists of two components:

| Component | Rate | 2026 Wage Base | Maximum Tax |

|---|---|---|---|

| Social Security | 12.4% | $184,500 | $22,878 |

| Medicare | 2.9% | No limit | No maximum |

| SE Tax Total | 15.3% | — | — |

| Additional Medicare Tax | +0.9% | Above $200K / $250K | — |

The Social Security wage base — the maximum amount of earnings subject to the 12.4% Social Security tax — is $184,500 for 2026, up from $176,100 in 2025. The Social Security Administration adjusts this figure annually based on changes in the national average wage index. Medicare tax, by contrast, applies to all net self-employment income with no cap.

4. How to Calculate Self-Employment Tax: The 92.35% Rule

SE tax is not applied to your full net self-employment income. Instead, it is applied to 92.35% of that amount.

Here is why: when a W-2 employee pays FICA taxes, the employer’s matching share (7.65%) is not included in the employee’s taxable income — the employer pays it separately. To create the same treatment for self-employed individuals, the IRS allows you to subtract the employer-equivalent portion before calculating SE tax. That subtraction is exactly 7.65%, which means:

100% − 7.65% = 92.35%

This is not a deduction — it is built into the SE tax calculation formula itself.

Calculation Example

Suppose your net self-employment income is $80,000:

| Step | Calculation | Result |

|---|---|---|

| 1. Apply 92.35% | $80,000 × 92.35% | $73,880 |

| 2. Apply 15.3% | $73,880 × 15.3% | $11,304 SE Tax |

Why this matters: If you skipped the 92.35% step and applied 15.3% directly to $80,000, your SE tax would come to $12,240 — overstating your liability by $936. The 92.35% rule is not optional; it is the correct calculation method under IRS rules.

5. The 50% SE Tax Deduction

After calculating your SE tax, you may deduct 50% of that amount from your gross income when calculating your adjusted gross income (AGI). This deduction appears on Schedule 1 (Form 1040), Line 15.

Continuing the example above:

- SE Tax calculated: $11,304

- 50% deduction: $5,652

- This $5,652 reduces your AGI — and therefore your federal income tax

The logic mirrors how W-2 employees are treated: employer FICA contributions are not included in employee income. The 50% deduction gives self-employed individuals an equivalent benefit.

Important: The 50% deduction reduces your income tax — it does not reduce SE tax itself. Both taxes are still calculated and paid separately. W-2 employees cannot claim this deduction; it is available only to those who pay SE tax.

6. Additional Medicare Tax

Higher-income self-employed individuals owe an extra 0.9% Additional Medicare Tax on net self-employment income above the following thresholds:

| Filing Status | Income Threshold |

|---|---|

| Single / Head of Household / Qualifying Surviving Spouse | $200,000 |

| Married Filing Jointly | $250,000 |

| Married Filing Separately | $125,000 |

The Additional Medicare Tax applies to the combined total of wages, tips, and net self-employment income. It is calculated on Form 8959 and reported on Form 1040.

One important distinction: only the regular 2.9% Medicare portion of SE tax qualifies for the 50% AGI deduction. The additional 0.9% is not deductible.

7. Schedule SE: How to File

SE tax is calculated using Schedule SE (Form 1040), which you attach to your annual tax return. The schedule walks you through the 92.35% adjustment, applies the 15.3% rate, and determines any Social Security wage base limitation.

The result from Schedule SE flows into two places on your Form 1040:

- The full SE tax amount is added to your total tax liability

- 50% of SE tax is entered on Schedule 1, Line 15, as a deduction from gross income

Most tax software handles this automatically once you enter your self-employment income. If you file manually, completing Schedule SE before calculating your total tax is essential.

8. Quarterly Estimated Tax Payments

Because self-employed individuals have no employer withholding from a paycheck, the IRS requires most to pay taxes quarterly throughout the year using Form 1040-ES.

Each estimated payment should cover both your projected income tax and SE tax for that quarter. A common mistake is estimating only income tax — omitting the 15.3% SE tax — and discovering a large underpayment balance when filing the annual return.

Standard quarterly due dates are:

- April 15 (Q1)

- June 15 (Q2)

- September 15 (Q3)

- January 15 of the following year (Q4)

Note: When a due date falls on a weekend or federal holiday, the deadline automatically shifts to the next business day. Always confirm the exact date for the current year before submitting your payment.

9. When You Have Both W-2 Wages and Self-Employment Income

If you hold a salaried job and also earn self-employment income, the Social Security wage base applies to your combined earnings from both sources.

The $184,500 Social Security wage base (2026) is a combined annual cap. Social Security taxes withheld from your W-2 wages count toward that limit first. This creates two practical scenarios:

Scenario A: W-2 Wages Below $184,500

You owe Social Security tax on your self-employment income up to the remaining portion of the $184,500 cap. Both the W-2 withholding and Schedule SE work together to reach — but not exceed — the annual maximum.

Scenario B: W-2 Wages Already Reach or Exceed $184,500

If your W-2 employer has already withheld Social Security tax on $184,500 or more in wages, you owe no Social Security tax on your self-employment income — only the 2.9% Medicare portion applies. This is a meaningful tax reduction for high earners with a mix of W-2 and self-employment income.

Watch for overpayment: If you work for multiple employers and your combined W-2 wages exceed $184,500, each employer withholds Social Security tax independently — unaware of the other. This can result in excess Social Security withholding. The overpayment is recovered as a credit on Schedule 3 when you file your return.

10. SE Tax vs. FICA: Side-by-Side Comparison

| Feature | W-2 Employee (FICA) | Self-Employed (SE Tax) |

|---|---|---|

| Total Rate | 15.3% (split equally) | 15.3% (paid in full) |

| Employee Pays | 7.65% | 15.3% |

| Employer Match | Yes — 7.65% | No match |

| How It’s Paid | Withheld from paycheck | Quarterly estimated payments + Schedule SE |

| AGI Deduction | None | 50% of SE tax |

| Governing Law | FICA (IRC §3101–§3128) | SECA (IRC §1401–§1403) |

| SS Wage Base (2026) | $184,500 | $184,500 |

EA Insight

The most common mistake I see in the first year of self-employment is calculating estimated payments based on income tax alone. SE tax adds 15.3% on top of your regular income tax rate — and it applies from the first dollar of net self-employment income over $400. If you forget to include it in your quarterly estimates, the shortfall accumulates quietly and shows up as a large balance due at filing time.

The 92.35% rule is frequently skipped when people calculate SE tax on their own. Applying 15.3% to your full net income instead of 92.35% of it overstates your SE tax. While the difference may seem small, it compounds over time — and it affects your AGI, which in turn can affect your eligibility for credits and deductions that phase out at certain income levels.

If you also receive W-2 wages, always check whether your employer withholding has already reached the Social Security wage base. High earners who cross the $184,500 threshold through their W-2 alone owe only Medicare tax — not the Social Security portion — on their self-employment income. This is a point many taxpayers miss, and it results in unnecessary overpayment that has to be recovered at filing.

Frequently Asked Questions

Do I owe SE tax if I only made $350 from freelance work?

No. The SE tax filing threshold is $400 in net self-employment income. If your net earnings fall below that amount for the year, you are not required to pay SE tax or file Schedule SE. However, you may still need to report the income on your tax return.

Is SE tax the same as income tax?

No. They are two separate taxes. Income tax is based on your taxable income after deductions and credits, and it funds the federal government’s general operations. SE tax is a fixed-rate tax on net self-employment earnings that funds Social Security and Medicare specifically. Both are reported on Form 1040, but they are calculated independently.

Does a single-member LLC pay self-employment tax?

Yes, by default. A single-member LLC is taxed as a sole proprietorship unless it elects to be treated as a corporation. The owner reports net business income on Schedule C, and that income is subject to SE tax via Schedule SE.

Where exactly does the 50% SE tax deduction go on my return?

It is entered on Schedule 1 (Form 1040), Line 15, as an adjustment to income. This reduces your AGI — which can affect your eligibility for various credits and deductions that phase out at higher income levels, including the MAGI-based limits on IRA contributions and certain education credits.

What if I don’t pay quarterly estimated taxes?

If your total tax liability for the year exceeds $1,000 and you did not pay enough through withholding or estimated payments, the IRS may assess an underpayment penalty. The penalty is calculated based on how much was underpaid and for how long. Filing your return and paying in full by the annual deadline does not eliminate this penalty if quarterly payments were missed.

Can I reduce my SE tax by contributing to a retirement account?

Retirement contributions — such as those to a SEP IRA or Solo 401(k) — reduce your federal income tax but do not reduce SE tax. SE tax is calculated on net self-employment income before retirement deductions are applied. However, the 50% SE tax deduction does reduce your AGI, which may lower your income tax and improve eligibility for certain tax benefits.

Official Resources

- IRS — Self-Employment Tax (Social Security and Medicare Taxes)

- IRS — About Schedule SE (Form 1040)

- IRS — About Form 1040-ES, Estimated Tax for Individuals

- IRS Publication 334 — Tax Guide for Small Business

- IRS Tax Topic 554 — Self-Employment Tax

- SSA — Contribution and Benefit Base (Wage Base History)

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.