What Happens If You Don’t Check “Someone Can Claim You as a Dependent”?

One unchecked box on Form 1040 can trigger an IRS e-file rejection — even if your child owes zero tax.

Key Takeaways

- If a parent can claim you as a dependent, you must check “Someone can claim you as a dependent” on your own Form 1040.

- Skipping that checkbox tells the IRS you are filing as an independent taxpayer — and creates a conflict with your parent’s return.

- When the parent e-filed first and the child e-files second without the box, the child’s return is rejected with a duplicate SSN error.

- A dependent’s standard deduction for 2026 is limited to the greater of $1,350 or earned income + $450, up to $16,100.

- Being a dependent does not mean you cannot file your own return — it means you must file it correctly.

Table of Contents

1. A Call I Get Every Tax Season

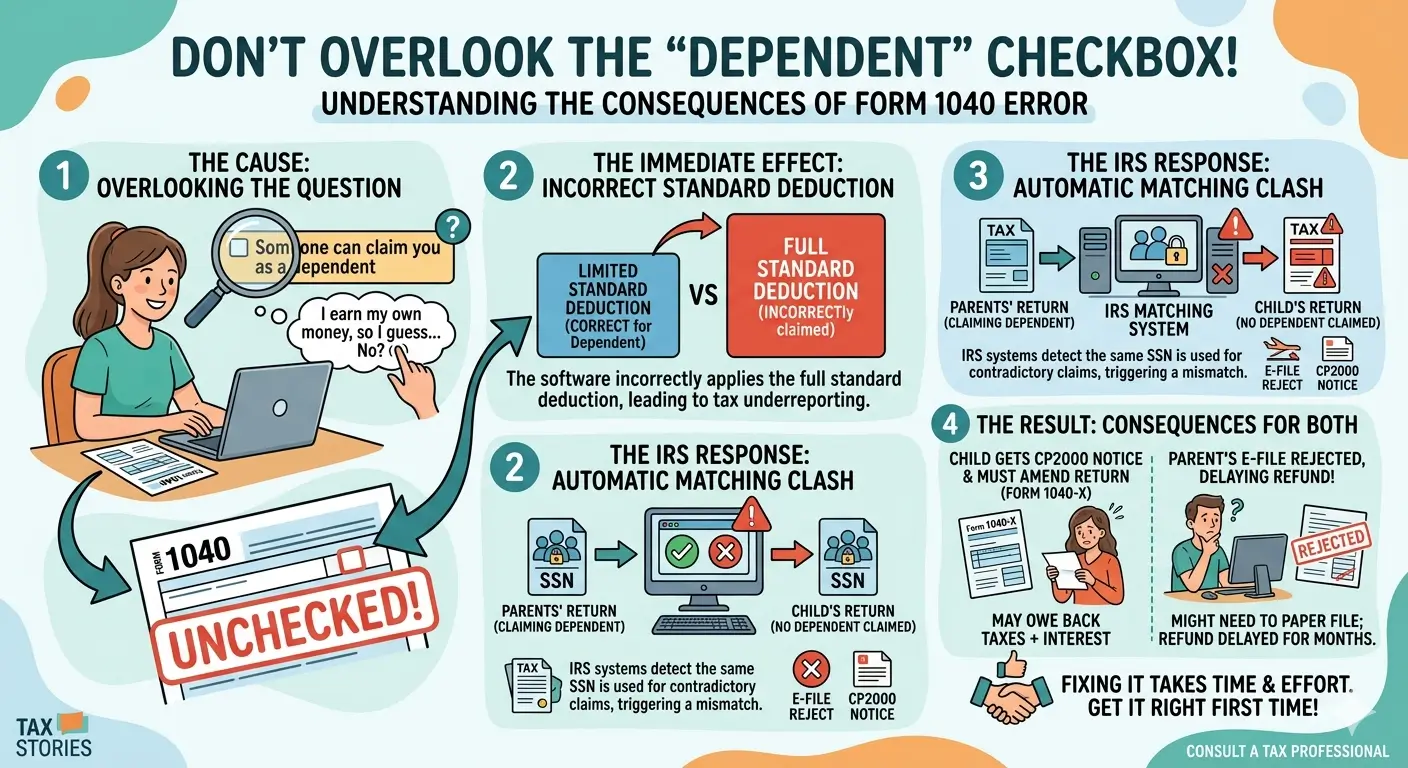

Every tax season, I see the same scenario. A parent e-files without issue. A few days later, their college-age child tries to file their own return — and the IRS rejects it. The parent is confused. The child is panicked. And almost always, the cause is a single checkbox on Form 1040.

Let me walk you through what happens. We’ll call our filers Emily and Lisa.

Emily is a college sophomore working part-time at the campus bookstore. She earned about $8,000 that year — her first real paycheck, her first W-2, and her first time filing a tax return on her own.

She downloaded a free tax software, plugged in her W-2, and started answering questions. Everything was going smoothly until this one popped up:

Emily paused for a moment. She thought: “I earned my own money and I’m filing my own return — nobody’s claiming me.” She selected “No” and moved on.

What Emily didn’t know: her mom Lisa had already e-filed a few days earlier and claimed Emily as a dependent — just like every year. Lisa pays for Emily’s tuition, rent, and health insurance. To Lisa, nothing about Emily’s dependent status had changed.

Three days later, Emily got an email from the tax software: “Your return was rejected by the IRS.”

2. Why That Checkbox Changes Everything

Form 1040 includes a checkbox that reads: “Someone can claim you as a dependent.” This is not just a formality — it does two things at once. It determines your standard deduction amount, and it tells the IRS matching system whether your SSN is allowed to appear on another return as a dependent.

Bottom line

If someone can claim you as a dependent — whether or not they actually do — your standard deduction is limited, and you must indicate it on your return.

How the Dependent Standard Deduction Works

For the 2026 tax year, a dependent’s standard deduction is the greater of:

- $1,350, or

- Earned income + $450

Either way, the total cannot exceed $16,100 (the full standard deduction for a single filer in 2026).

Emily’s Numbers

| Scenario | Standard Deduction Applied |

|---|---|

| Emily checks the box (correct) | $8,450 ($8,000 + $450) |

| Emily does not check the box (incorrect) | $16,100 (full amount) |

In Emily’s case, her $8,000 income falls below either standard deduction amount, so she owes $0 in tax regardless. But here is the problem: the IRS does not just look at the tax owed — it checks whether the information on both returns is consistent. When Emily’s return says she is not a dependent, and Lisa’s return says she is, the system flags a conflict before Emily’s return is even accepted.

3. What Actually Happens When the Box Is Wrong

The IRS processes e-filed returns through an automated matching system. Every SSN on a new return is checked against every return already accepted for that tax year. When a conflict appears, the system responds in real time.

The Sequence

Here is what happened in Emily’s case:

- Lisa e-filed first, claiming Emily as a dependent. Her return was accepted without issue.

- Three days later, Emily e-filed without checking the dependent box. Her return treated her as an independent taxpayer.

- The IRS matching system saw that Emily’s SSN had already been used as a dependent on Lisa’s return. It rejected Emily’s return with a duplicate SSN error (internal reject code IND-517).

The IRS does not reveal who else claimed the SSN — for confidentiality reasons, the rejection email simply says the SSN is in use on another return. It took one phone call home for Emily to understand what had happened.

The Fix

Once the situation is understood, the fix is straightforward. Emily reopened her return in the tax software, changed her answer to “Yes, someone can claim me as a dependent,” let the standard deduction adjust to the limited $8,450 amount, and re-filed. Within a day, her return was accepted.

The limited standard deduction made no difference to Emily’s tax bill. With $8,000 of earned income and an $8,450 dependent SD, her taxable income was $0 — the same result she would have gotten with the full $16,100 SD. The rejection was never really about tax owed. It was about the IRS insisting that both returns tell the same story.

Different Paths, Different Problems

| Filing Situation | What the IRS Does |

|---|---|

| Parent e-files first, child e-files with box checked | Both returns accepted |

| Parent e-files first, child e-files without box | Child’s return rejected — must correct and re-file |

| Child e-files first without box, parent e-files later | Parent’s return rejected — must paper-file |

| Either party paper-files with the wrong box | Processed initially; CP2000 notice may follow months later |

Important: The IRS does not decide who is “right” based on who filed first. Filing first just means the first return gets accepted by the automated system. If both parties believe they have the right to claim the dependent, the IRS applies the qualifying child tiebreaker rules — and can require the wrong claimant to repay any tax benefit received.

One more thing worth knowing: if the federal return has the wrong dependent status, the state tax return almost always inherits the same mistake. Many states follow federal dependent rules, so a federal error can generate a separate state notice as well.

4. What If the Situation Is Different?

What if Emily earned $20,000 or more?

For a qualifying child, there is no income limit test. Even if Emily earned $20,000 from a summer internship, she can still be claimed as a dependent — as long as she did not provide more than half of her own financial support for the year. Under the qualifying child rules, it is not how much the child earns that matters, but who paid the living expenses.

Practical point

If Emily earned $20,000 but saved most of it while Lisa paid tuition, rent, and health insurance, Emily is still a qualifying child. Her dependent standard deduction would be $20,000 + $450 = $20,450 — but capped at $16,100.

For earned income alone, the dependent standard deduction formula is designed to absorb typical student or part-time wages. In many cases, there is no actual tax difference between the correct and incorrect checkbox — both produce a taxable income of zero. The real tax impact shows up when a dependent has unearned income — interest, dividends, or capital gains. The dependent SD formula is based on earned income only, so a dependent with $5,000 in dividends and no job gets just the $1,350 minimum deduction, not the full $16,100. That is where the checkbox error turns into real dollars owed.

What if Emily is 24 or older?

The qualifying child age limit is under 19, or under 24 if the child is a full-time student. Once Emily turns 24, she can no longer be claimed as a qualifying child. At that point, the only path for Lisa to claim Emily would be through the qualifying relative test — which does have a gross income limit ($5,300 for 2026). If Emily is 24 or older and earns more than that threshold, she is not a dependent, and checking “No” on the box would be correct.

What if Emily has health insurance through the Marketplace?

If Emily left her parent’s health plan and enrolled in a Marketplace plan with the Premium Tax Credit, the dependent checkbox affects more than just the standard deduction. Incorrectly filing as an independent taxpayer could inflate the credit amount, creating an additional repayment obligation when the IRS reconciles the return.

5. Common Misconceptions

“I file my own return, so I’m not a dependent.”

Filing your own tax return and being a dependent are two completely separate things. Dependents can — and often must — file their own returns when they have earned income above a certain threshold. The act of filing does not change your dependency status.

“My parent didn’t actually claim me, so the box doesn’t matter.”

The checkbox says “someone can claim you” — not “someone did claim you.” If you meet the qualifying child or qualifying relative tests, you must check the box regardless of whether the other person actually files a return claiming you.

“I’m a dependent, so I can’t get a refund.”

Dependents can absolutely receive a refund. If the federal income tax withheld from your paycheck (shown in Box 2 of your W-2) exceeds your actual tax liability, the IRS will refund the difference. Dependency status limits your standard deduction, but it does not block refunds.

Important: Do not confuse “qualifying child” with “qualifying relative.” The qualifying child test has no income limit — the key factor is who provided financial support. The qualifying relative test does have a strict income ceiling.

6. What to Check Right Now

- Confirm with your parent whether they plan to claim you as a dependent this year.

- Check that you marked “Someone can claim you as a dependent” correctly on your Form 1040.

- Verify that your standard deduction reflects the limited amount — not the full $16,100.

- If your e-file was rejected, read the rejection email carefully before re-filing — the fix is usually just the checkbox.

- If you already filed incorrectly on paper, prepare Form 1040-X (Amended Return) to correct it before the IRS contacts you.

EA Insight

This is one of the most common e-file rejections I see during the college-age filing years. The scenario repeats almost every season: a parent files first, a new-to-filing child files second without checking the dependent box, and the IRS matching system rejects the child’s return with a duplicate SSN error. Same pattern, different families.

When I get this call, my first question is always: “Did you already file, or are you still working on it?” If the child’s e-file was just rejected, the fix is fast — open the return, check “Someone can claim you as a dependent,” let the standard deduction adjust, and e-file again. If the child already paper-filed, or the rejection went unnoticed for weeks, the cleanup gets longer: a Form 1040-X amended return, sometimes state corrections, occasionally a CP2000 notice to reconcile.

The simplest prevention is one conversation before filing season. Parents, tell your college-age child: “I’m claiming you as a dependent this year, so check that box when you file.” Students, ask your parent before you file solo. That one sentence prevents an IRS rejection, weeks of back-and-forth emails, and the sinking feeling of realizing your tax return was wrong.

EA Summary

When a parent claims a child as a dependent and the child then files their own return, the child must check “Someone can claim you as a dependent” on Form 1040. That single checkbox determines the standard deduction amount and keeps the IRS matching system from rejecting the return. A quick conversation between parent and child before filing season is the most reliable way to prevent an e-file rejection, a paper refile, or a CP2000 notice down the road.

Frequently Asked Questions

Do dependents have to file their own tax return?

It depends on income. If a dependent’s earned income exceeds the full single standard deduction ($16,100 for 2026), or if unearned income exceeds $1,350, a separate return is required. Being a dependent does not automatically exempt you from filing.

What if I checked the box wrong and already e-filed?

If the return was rejected, simply correct the checkbox in your tax software and re-file. If the return was accepted (for example, through a paper filing), file Form 1040-X (Amended U.S. Individual Income Tax Return) to correct it. It is better to amend proactively than to wait for an IRS notice.

What happens if both parent and child claim the same exemption?

The IRS applies tiebreaker rules. Generally, the parent with whom the child lived for the longer part of the year has priority. If the child lived with both parents equally, the parent with the higher adjusted gross income (AGI) prevails.

Can a dependent still get a tax refund?

Yes. If the amount of federal income tax withheld from your paycheck exceeds your actual tax liability, you are entitled to a refund. Dependency status limits the standard deduction, but it does not prevent refunds.

Does this checkbox affect state tax returns too?

In most cases, yes. Many states follow federal dependency rules. If your federal return has the wrong dependent status, your state return likely does too — and you may receive a separate notice from your state’s tax agency.

Is there an income limit for a qualifying child?

No. Unlike the qualifying relative test, the qualifying child test does not have a gross income limit. The key factor is whether the child provided more than half of their own financial support — not how much they earned.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.