What Is an ITIN?

An ITIN is a 9-digit tax identification number issued by the IRS to individuals who have a U.S. tax filing obligation but are not eligible for a Social Security number. You can file a federal tax return, claim eligible tax benefits, and stay compliant with U.S. tax law — all without an SSN.

Key Takeaways

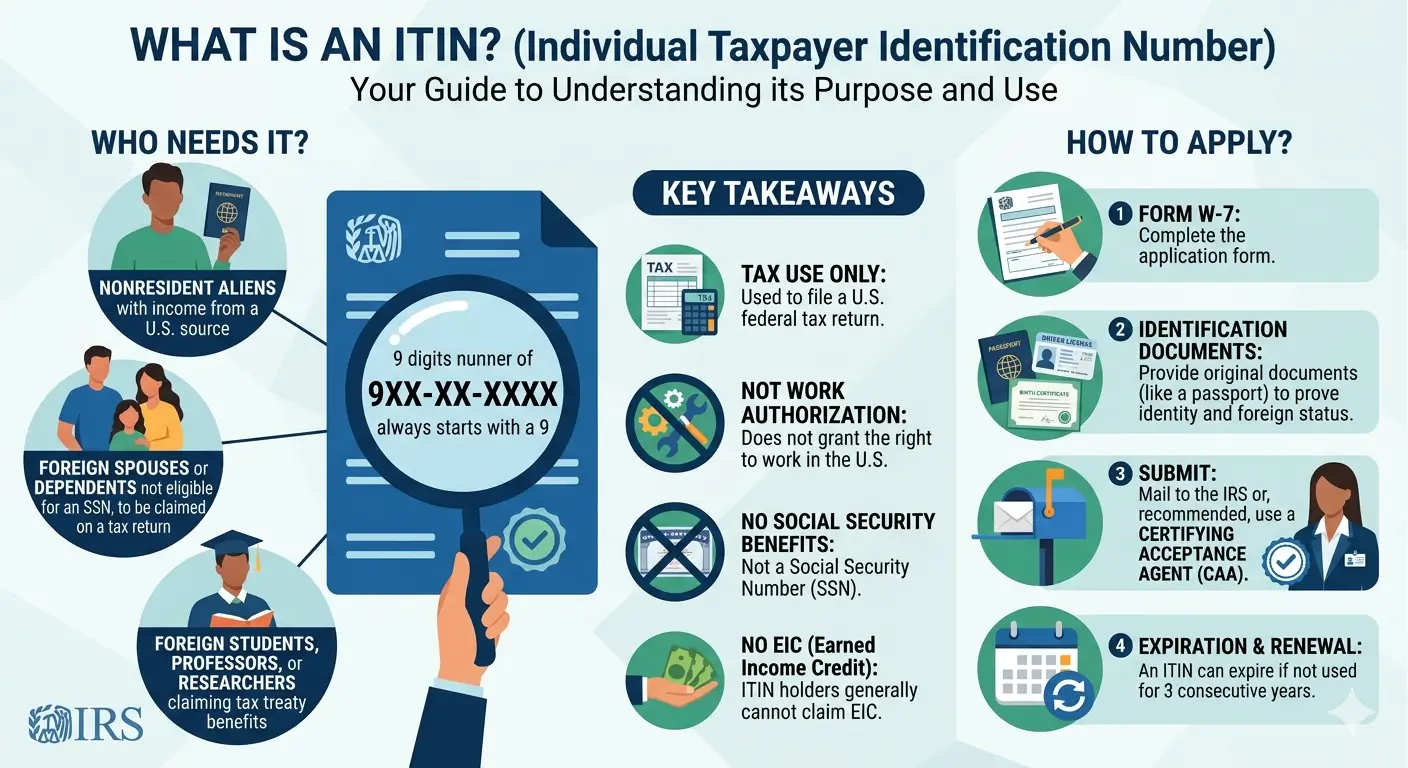

- An ITIN (Individual Taxpayer Identification Number) is issued by the IRS for federal tax purposes only — it does not authorize employment or provide Social Security benefits.

- You apply for an ITIN using Form W-7, which must generally be submitted with a federal tax return.

- A valid passport is the only single document that satisfies both identity and foreign status requirements.

- A CAA (Certifying Acceptance Agent) can authenticate your documents so you don’t have to mail your original passport to the IRS.

- An ITIN expires if it is not used on a federal tax return for three consecutive years.

- ITIN holders cannot claim the Earned Income Credit (EIC), and — under OBBBA — the Child Tax Credit now requires an SSN for both the child and at least one parent.

Table of Contents

1. What Is an ITIN?

An ITIN, or Individual Taxpayer Identification Number, is a nine-digit tax processing number issued by the IRS to individuals who are required to file a U.S. federal tax return but are not eligible to obtain a Social Security number (SSN). ITINs always begin with the digit 9 and follow the format 9XX-XX-XXXX.

The IRS created the ITIN program to ensure that everyone with a U.S. tax obligation — regardless of immigration status — can file a return, receive eligible tax benefits, and remain in compliance with federal tax law. As stated in IRS Publication 1915, an ITIN is issued strictly for federal tax administration purposes and serves no other function.

2. Who Needs an ITIN?

You may need an ITIN if you fall into one of the following categories and are not eligible for an SSN:

- Nonresident aliens with U.S.-source income (rental income, investment income, royalties, etc.) who are required to file a return

- Resident aliens who do not qualify for an SSN under Social Security Administration rules

- Foreign spouses or dependents of U.S. citizens or resident aliens who are claimed for an allowable tax benefit on a U.S. return

- Nonresident alien students, professors, or researchers claiming tax treaty benefits

- Individuals required to be listed on a U.S. federal tax return who cannot obtain an SSN

Important: If you already have — or are eligible to get — an SSN, you should not apply for an ITIN. Spouses and dependents are not eligible for an ITIN unless they are claimed for an allowable tax benefit (such as the Credit for Other Dependents or Married Filing Jointly status) or they file their own tax return.

3. What Is Form W-7?

Form W-7, Application for IRS Individual Taxpayer Identification Number, is the official IRS form used to apply for a new ITIN or to renew an existing one. The current version was revised in December 2024 and includes updated documentation requirements for dependents.

General rule: Form W-7 must be submitted together with a completed U.S. federal tax return (such as Form 1040 or Form 1040-NR). The return is attached to the W-7 and mailed to the IRS ITIN Operation address.

There are limited exceptions that allow you to submit Form W-7 without a tax return — for example, if you are a nonresident alien receiving wages subject to withholding, or if you are a student or researcher claiming a tax treaty benefit. Each exception requires specific supporting documentation as outlined in the Form W-7 instructions.

Note: An ITIN is not required to make estimated tax payments (Form 1040-ES) or to file an extension (Form 4868). You can take those steps without an ITIN in place.

Once the IRS receives a properly completed application with all required documentation, processing typically takes approximately seven weeks. During filing season (January through April) or for applications submitted from outside the United States, processing may take longer.

4. Required Documents

Every ITIN applicant must provide documentation that proves two things: identity and foreign status. The IRS accepts 13 types of documents for this purpose. Each document must be current and include an expiration date.

| Document | Proves Identity | Proves Foreign Status |

|---|---|---|

| Passport | ✅ | ✅ (stand-alone) |

| Foreign National ID Card | ✅ | ✅ |

| U.S. Driver’s License | ✅ | ❌ |

| Civil Birth Certificate | ✅ | Situational |

| Visa Issued by U.S. Dept. of State | ✅ | ✅ |

| Medical Records (dependents under 6 only) | ✅ | ❌ |

A passport is the single most practical choice because it is the only document that simultaneously satisfies both the identity and foreign status requirements. Without a passport, applicants must submit two separate documents. School records are accepted only for dependents under age 24 and must meet IRS content requirements.

5. Three Ways to Submit

There are three methods for submitting a Form W-7 application. Each has different implications for how your original documents are handled.

Option 1 — Mail to the IRS

You can mail your completed Form W-7, the attached tax return, and your original supporting documents directly to the IRS ITIN Operation. The IRS will review your documents and return them by mail once processing is complete. The key drawback: you will be without your passport or other original documents for the duration of processing, which can take several weeks.

Option 2 — IRS Taxpayer Assistance Center (TAC)

Some IRS Taxpayer Assistance Centers offer in-person ITIN document review by appointment. You bring your original documents, an IRS employee reviews them on-site, and you leave with your documents the same day. Not all TAC locations offer this service, so confirm availability before scheduling.

Option 3 — Certifying Acceptance Agent (CAA)

A CAA is an IRS-authorized professional who can review and certify your original documents on behalf of the IRS. Once the CAA certifies your documents, you do not need to send them to the IRS at all. This is particularly valuable for applicants who cannot afford to be without their passport for several weeks. See Section 6 for a full explanation of how CAAs work.

6. What Is a CAA (Certifying Acceptance Agent)?

A Certifying Acceptance Agent (CAA) is an individual or entity authorized by the IRS to assist foreign nationals and other non-U.S. persons in obtaining an ITIN. CAAs verify identity documents, help applicants complete Form W-7, and submit the application directly to the IRS — along with a signed Form W-7 (COA), Certificate of Accuracy, which certifies that the CAA has reviewed the original documentation.

CAA vs. AA — What Is the Difference?

| Feature | AA (Acceptance Agent) | CAA (Certifying Acceptance Agent) |

|---|---|---|

| Document Certification Authority | None | Yes — primary and secondary applicants |

| Must Mail Original Documents to IRS? | Yes | No |

| Forensic Document Training Required | No | Yes (renewed every 4 years) |

| Dependent Document Certification | Not available | Passport and birth certificate only; all others sent directly to IRS |

Who Can Become a CAA?

Tax professionals (including Enrolled Agents, CPAs, and attorneys), financial institutions, and accounting firms can apply to become CAAs through IRS e-Services. To qualify, all responsible parties listed on the application must complete mandatory ITIN Acceptance Agent training and forensic document identification training. The IRS conducts a suitability review — including a background check and tax compliance check — before approving the application.

As of January 19, 2024, the IRS lifted its moratorium on new CAA applications and fully transitioned to an electronic application process. Processing time for a complete application is approximately 60 days, reduced from the previous 120-day timeframe. CAAs must process a minimum of five W-7 applications per year to remain active in the program.

How to find a CAA: The IRS maintains a searchable directory of approved acceptance agents at IRS.gov/tin/itin/itin-acceptance-agents. Fees for service vary by provider.

7. ITIN Expiration and Renewal

An ITIN does not remain valid indefinitely. Under current IRS rules, an ITIN expires on December 31 of the third consecutive tax year in which it has not been used on a filed U.S. federal tax return. Additionally, ITINs assigned before 2013 that have never been renewed are also expired and must be renewed before use.

To renew an expired ITIN, submit Form W-7 with all required documentation. All renewal applications must include a U.S. federal tax return unless you qualify for an exception. If you are only using your ITIN for information return reporting purposes, renewal is not immediately required — but you will need to renew before filing a return in the future.

Important: Filing a tax return with an expired ITIN can result in delayed processing and delayed refunds. The IRS may also disallow credits claimed on a return filed with an expired ITIN.

8. What an ITIN Cannot Do

Because an ITIN is issued solely for federal tax purposes, it carries significant limitations. Understanding these upfront prevents costly mistakes on your return.

| What You Cannot Do With an ITIN | Details |

|---|---|

| Authorize Employment | An ITIN does not grant work authorization. Employers are required to verify work eligibility through Form I-9, which requires an SSN or other qualifying documentation. |

| Receive Social Security Benefits | Work performed under an ITIN does not earn Social Security credits. ITIN holders are not eligible for Social Security retirement, disability, or survivor benefits. |

| Claim the Earned Income Credit (EIC) | The EIC requires a valid SSN for the taxpayer, spouse (if filing jointly), and all qualifying children. If any one of these individuals has only an ITIN, the entire EIC is disallowed. |

| Claim the Child Tax Credit (CTC) for an ITIN Child | The $2,200 CTC requires the child to have a valid SSN. Under OBBBA, at least one parent must also have an SSN (for married couples filing jointly). However, a dependent with an ITIN who meets residency and support tests may still qualify for the $500 Credit for Other Dependents (ODC). |

OBBBA Update: The One Big Beautiful Bill Act (signed July 2025) permanently extended the SSN requirement for the Child Tax Credit and added a new requirement: for married couples filing jointly, at least one parent must also have a valid SSN to claim the $2,200 CTC. This is a change from prior law, which only required the child to have an SSN.

EA Insight

The single most common ITIN mistake I see is a name mismatch. A hyphen, a missing middle name, or one transposed letter between Form W-7 and the applicant’s passport is enough for the IRS to reject the entire application. Before submitting anything, compare every field on the W-7 to the passport character by character.

The second most common mistake is mailing an original passport to the IRS during filing season without understanding the risk. Processing can stretch well beyond seven weeks during busy periods, and people get stranded without their passport when travel plans come up. If you have any international travel on the horizon, use a CAA or visit a Taxpayer Assistance Center in person — both options let you keep your original documents.

On the credit side: many ITIN filers are surprised to learn that a dependent with an ITIN can still qualify for the $500 Credit for Other Dependents (ODC), even though the $2,200 Child Tax Credit is off the table. The ODC is nonrefundable, but it is real money that should not be left on the table.

Finally, watch the spousal ITIN carefully. Under current rules, a spouse is only eligible to apply for an ITIN if there is an actual allowable tax benefit at stake — such as a lower tax bill from filing jointly or a qualifying credit. With the standard deduction for married filing jointly at $32,200 and the personal exemption permanently eliminated, “we just want to file together” alone will not satisfy the IRS’s allowable tax benefit requirement. Make sure the benefit is real and documentable before you submit the application.

Frequently Asked Questions

Does having an ITIN let me work legally in the United States?

No. An ITIN is a tax identification number only. It does not grant work authorization, change your immigration status, or entitle you to any Social Security or government benefits. Employment eligibility is determined by your immigration status and documented through Form I-9, not through your ITIN.

Can I get an ITIN if I am undocumented?

Yes. The IRS issues ITINs regardless of immigration status. The ITIN program exists specifically so that everyone with a U.S. tax obligation can comply with federal tax law. Applying for an ITIN does not affect your immigration status in any way.

What is the difference between a CAA and an Acceptance Agent (AA)?

Both are IRS-authorized to assist with ITIN applications, but a CAA has additional authority to certify original documents on behalf of the IRS — meaning the applicant does not have to mail their passport or other original identification to the IRS. An AA does not have this certification authority, so original documents must still be submitted directly to the IRS. CAAs are also required to complete forensic document training, which AAs are not.

My child has an ITIN. Can I claim the Child Tax Credit?

No. The Child Tax Credit ($2,200 per qualifying child) requires the child to have a valid SSN issued for employment. Under the One Big Beautiful Bill Act, at least one parent must also have an SSN for married couples filing jointly. However, if your child with an ITIN meets the residency and support tests, you may be eligible for the $500 Credit for Other Dependents (ODC), which does not require an SSN.

How do I know if my ITIN has expired?

An ITIN expires on December 31 of the third consecutive year it was not used on a filed tax return. You can check your filing history to determine the last year your ITIN appeared on a submitted return. The IRS may also send a notice if your ITIN is expiring. If you are unsure, contact the IRS directly or consult a tax professional before filing.

Can a spouse who lives outside the United States get an ITIN?

Yes, but only if there is an allowable tax benefit that requires the ITIN — for example, you want to file a joint return to take advantage of the $32,200 married filing jointly standard deduction, or to claim an eligible credit. Simply wanting to include a spouse on a return is not sufficient. The benefit must be real and documentable.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.