What Is an Amended Return (Form 1040-X)?

Form 1040-X is the IRS form used to correct a tax return you already filed. Whether you forgot a deduction, received a corrected W-2, or chose the wrong filing status, amending your return is how you fix it — and how you claim a refund you may have missed.

Key Takeaways

- Form 1040-X amends a previously filed Form 1040, 1040-SR, or 1040-NR.

- To claim a refund, you generally have 3 years from the original filing date, or 2 years from the date the tax was paid — whichever is later.

- Returns from the current year and the two prior years can be e-filed; older years must be filed on paper.

- You can e-file up to 3 amended returns per tax year.

- Math errors and missing forms found by the IRS usually don’t require an amendment — the IRS corrects those automatically.

- Processing typically takes 8 to 12 weeks, but commonly runs longer in practice.

Table of Contents

- 1. What Is Form 1040-X?

- 2. When You Should File an Amended Return

- 3. When You Don’t Need to Amend

- 4. The 3-Year Deadline — With Examples

- 5. How to File Form 1040-X

- 6. Understanding Columns A, B, and C

- 7. Processing Time and Tracking Your Amendment

- 8. Don’t Forget Your State Return

- 9. EA Insight

- 10. Frequently Asked Questions

- 11. Related Articles

- 12. Official Resources

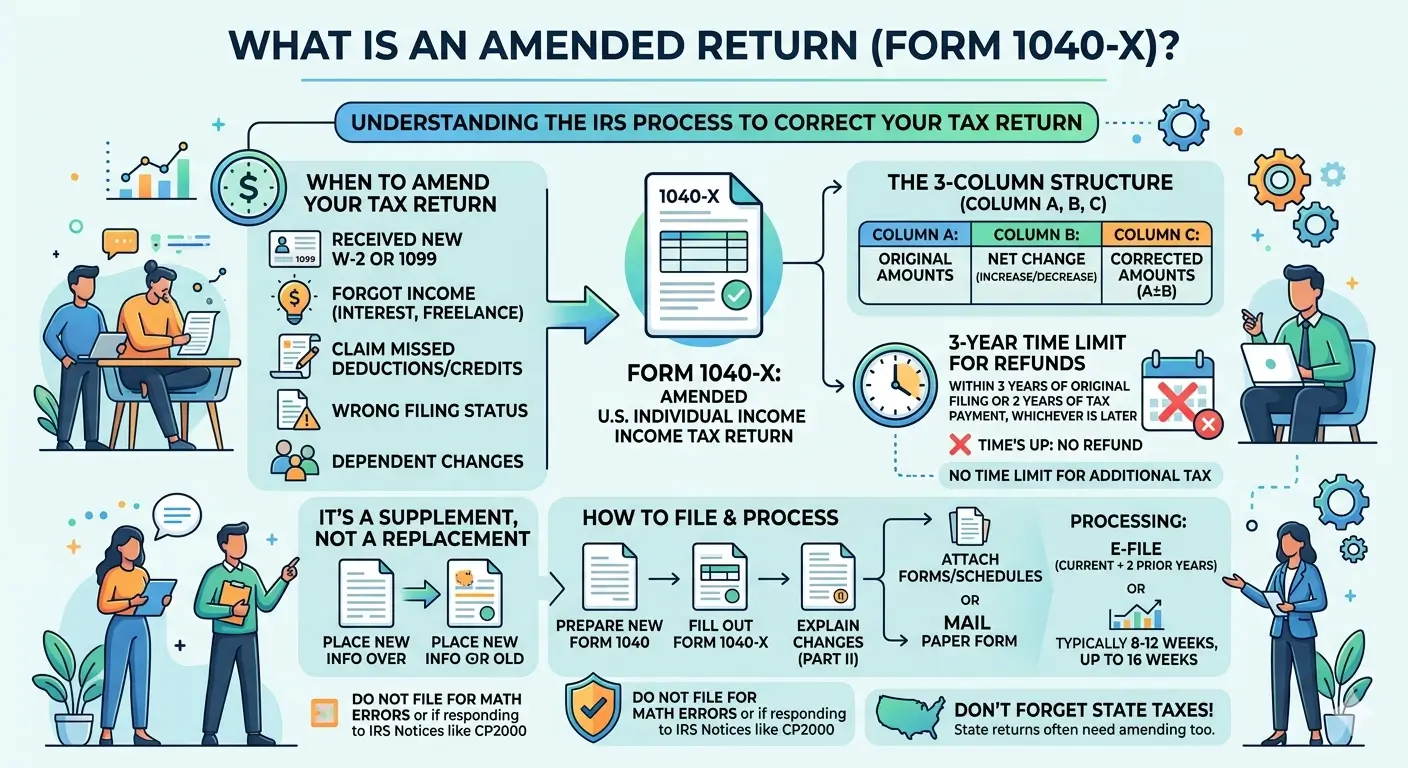

1. What Is Form 1040-X?

Form 1040-X, Amended U.S. Individual Income Tax Return, is the IRS form individual taxpayers use to correct a return they already filed. It does not replace your original return — it sits on top of it as an adjustment, showing what you originally reported, what changed, and the corrected figures.

You can use Form 1040-X to:

- Correct a previously filed Form 1040, 1040-SR, or 1040-NR

- Change amounts that the IRS previously adjusted

- Make a claim for a carryback due to a loss or unused credit

- Make certain elections after the original deadline has passed

2. When You Should File an Amended Return

File Form 1040-X when you discover one of the following after your original return has been accepted:

- You received a corrected or late W-2, 1099, or K-1

- You discovered income you forgot to report (interest, freelance work, crypto sales)

- You realized you missed a deduction or credit you were eligible for

- You used the wrong filing status (for example, filing Single when you qualified for Head of Household)

- You claimed a dependent incorrectly, or forgot to claim one

- You need to change the number of dependents

3. When You Don’t Need to Amend

Not every error requires an amended return. The IRS automatically handles:

- Math errors on your return

- Missing standard forms like a forgotten W-2 (the IRS will request it)

Important: If you receive an IRS notice (such as a CP2000) proposing changes, that is not an automatic amendment situation. Respond to the notice as instructed. Only file Form 1040-X separately if the notice specifically directs you to — otherwise you create a parallel record that delays resolution.

4. The 3-Year Deadline — With Examples

To claim a refund through an amended return, the deadline is the later of these two dates:

- (A) 3 years from the date you filed your original return, or

- (B) 2 years from the date you paid the tax

For most taxpayers, the 3-year rule (A) is what matters. The 2-year rule (B) only becomes relevant in unusual situations where additional tax was paid long after the original return was filed. Here’s how it works in practice:

Example 1 — Standard case (3-year rule applies)

Sarah filed her 2024 return on April 15, 2025. In 2027, she discovered a deduction she had missed.

- (A) Filing date + 3 years = April 15, 2028

- (B) Tax payment date + 2 years = April 15, 2027

- Later of the two = April 15, 2028 → Sarah has until then to file Form 1040-X.

Example 2 — Filed early (treated as April 15)

Michael filed his 2024 return on February 1, 2025.

- Returns filed before the due date are treated as filed on April 15

- Refund claim deadline = April 15, 2028

Filing early does not start the clock early.

Example 3 — Filed under extension (actual filing date counts)

Jessica extended her 2024 return with Form 4868 and filed it on September 10, 2025.

- Clock starts on the actual filing date = September 10, 2025

- Refund claim deadline = September 10, 2028

Example 4 — Rare case where the 2-year rule matters

David filed his 2021 return on April 15, 2022. After an IRS audit, he paid $5,000 in additional tax on June 1, 2026.

- (A) Filing date + 3 years = April 15, 2025 → already expired

- (B) Payment date + 2 years = June 1, 2028

- Later of the two = June 1, 2028, but the refund is limited to the $5,000 paid in the last 2 years.

| Situation | Filing Date Used | Refund Claim Deadline |

|---|---|---|

| Filed by April 15 | April 15, 2025 | April 15, 2028 |

| Filed early (Feb 1, 2025) | Treated as April 15 | April 15, 2028 |

| Filed under extension (Sep 10, 2025) | September 10, 2025 | September 10, 2028 |

| Additional tax paid years later | — | Payment date + 2 years (refund limited) |

Bottom line: Miss the deadline and the refund is permanently lost — even if the underlying claim is valid. There is no extension and no exception. On the other hand, if your amendment increases the tax you owe, there is no statute of limitations protecting you. File and pay as soon as possible to limit interest and penalties.

5. How to File Form 1040-X

You can e-file Form 1040-X for the current tax year and the two prior tax years using commercial tax software, provided your original return was filed electronically. Older returns, or returns originally filed on paper, must be amended on paper.

Steps:

- Gather the original return and any new documents (corrected W-2, missing 1099, etc.)

- Prepare a corrected version of Form 1040 with the new figures

- Complete Form 1040-X showing original amounts, the changes, and corrected amounts

- In Part II, write a clear explanation of what changed and why

- Attach any new or changed forms and schedules

- E-file (if eligible) or mail to the address listed in the Form 1040-X instructions

You can electronically file up to 3 amended returns per tax year.

6. Understanding Columns A, B, and C

The core of Form 1040-X is its three-column structure:

| Column | What You Enter |

|---|---|

| Column A | Original amount (or amount as previously adjusted by the IRS) |

| Column B | Net change — increase or decrease |

| Column C | Corrected amount (Column A ± Column B) |

Part II is where you explain — in plain language — exactly what changed and why. A clear explanation reduces the chance of follow-up questions from the IRS.

7. Processing Time and Tracking Your Amendment

The IRS generally allows 8 to 12 weeks for processing, with some cases taking up to 16 weeks. In practice, processing often runs longer than the official estimates — patience is essential.

You can track your amendment using the IRS “Where’s My Amended Return?” tool on IRS.gov, which updates once a day. Status moves through three stages: Received → Adjusted → Completed.

If your amended return results in an additional refund, you will receive it separately from any original refund. For amendments to tax year 2021 and later, refunds can be sent by direct deposit when you e-file.

8. Don’t Forget Your State Return

Changing your federal return often changes your state tax liability — federal AGI flows into most state returns. After filing Form 1040-X, check whether your state requires a corresponding amended state return. Each state has its own form and deadline. Filing the federal amendment but skipping the state is one of the most common mistakes I see in practice.

EA Insight

The single biggest mistake I see with amended returns is waiting too long. Taxpayers discover a missed deduction in year four or five and call asking how to claim it — but the 3-year window has already closed, and the refund is permanently lost. If you suspect there’s something wrong with a recent return, look at it now, not next year.

A second common trap involves IRS notices. If you receive a CP2000 or similar letter proposing changes, respond to that notice as instructed. Do not file a separate Form 1040-X unless the notice specifically tells you to — an unsolicited amendment on top of an active notice creates a parallel record that often delays resolution by months.

Finally, always remember the state side. A federal amendment that increases your AGI almost always increases your state tax too. If you only fix the federal return, you may receive a state notice — with penalties and interest — a year or two later.

Frequently Asked Questions

How many years back can I amend a return?

To claim a refund, you generally have 3 years from the original filing date or 2 years from the date the tax was paid, whichever is later. There is no time limit if you owe additional tax.

Can I e-file Form 1040-X?

Yes, for the current and two prior tax years if your original return was filed electronically. Older years and paper-filed originals must be amended on paper.

Should I wait for my original refund before filing an amendment?

In most cases, yes. The IRS recommends waiting until you receive your original refund before filing Form 1040-X. Filing the amendment first does not stop the original refund, but it can create processing confusion if both are in the system at the same time.

Will amending my return trigger an audit?

Filing an amendment does not automatically trigger an audit. The IRS reviews 1040-X submissions like any return, and a clear, well-documented amendment typically processes routinely.

I already received a CP2000 notice — do I also need to file an amended return?

Usually not. Respond to the CP2000 directly using the response form provided. Only file Form 1040-X separately if the notice specifically instructs you to, or if you are correcting items unrelated to the notice.

What if I owe more tax after amending?

Pay the additional tax as soon as possible to minimize interest and penalties. Don’t include penalty or interest calculations on the form — the IRS will calculate and bill those separately.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.