How David Earned Social Security Credits Before Retirement

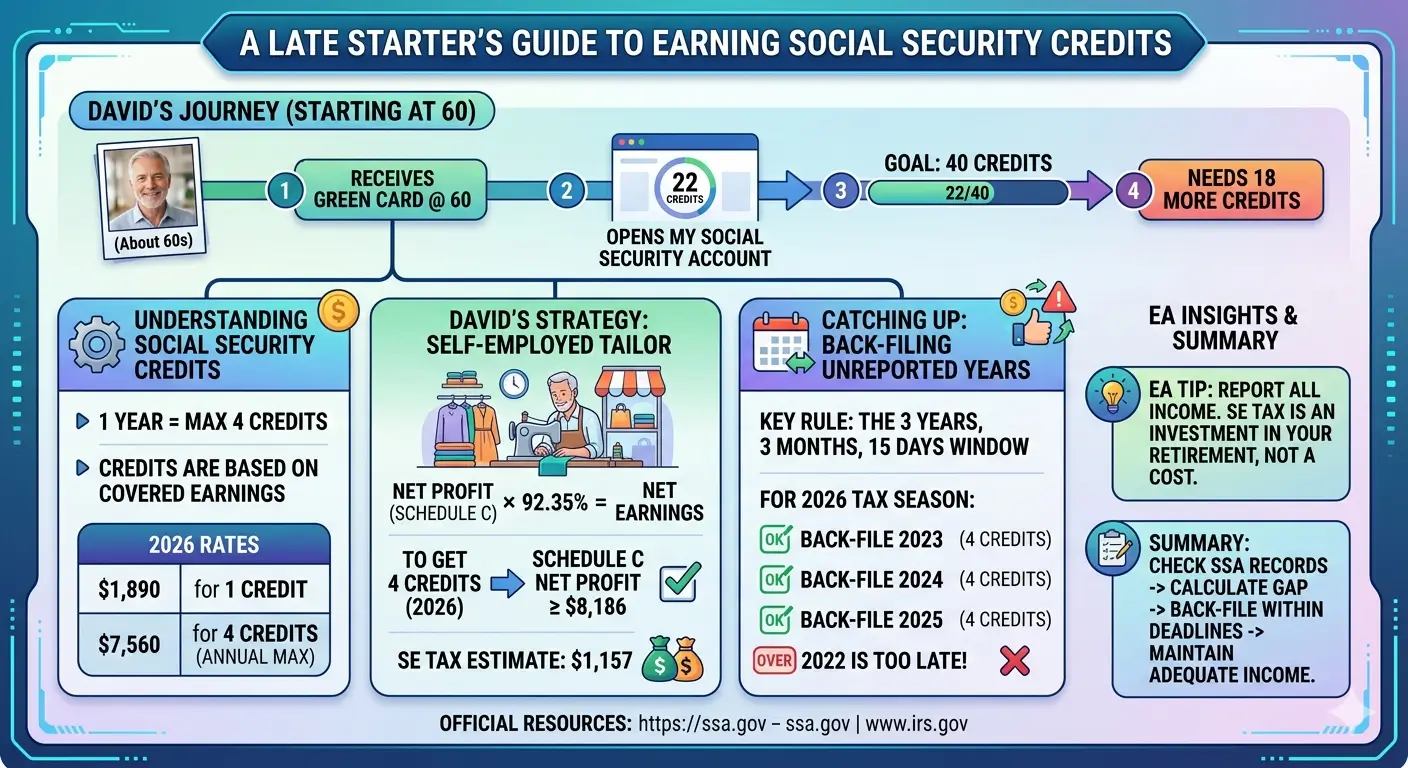

David got his green card at 60. When he opened his my Social Security account for the first time, the screen showed just 22 credits — eighteen short of what he needed to qualify for retirement benefits. The maximum a worker can earn in a year is four. The math looked impossible.

Key Takeaways

- Social Security retirement benefits generally require 40 credits — about ten years of covered work.

- In 2026, $1,890 of covered earnings buys one credit. $7,560 buys the maximum four for the year.

- For the self-employed, net profit on Schedule C — not gross sales — drives the credit count. About $8,186 in net profit produces $7,560 in covered earnings and 4 credits.

- Self-employment income has its own SSA reporting deadline: 3 years, 3 months, and 15 days after year-end.

- Miss that window and SSA generally won’t credit the earnings, even if you later file with the IRS.

- W-2 wages are easier to fix — employers report them quarterly to SSA. Self-employed workers are on their own clock.

Table of Contents

- 1. Meet David

- 2. How Social Security Credits Work

- 3. David’s Numbers: The 4-Credit Threshold

- 4. The Self-Employment Trap: The 3-Year Rule

- 5. When Net Earnings Fall Short: The Optional Method

- 6. What to Check Right Now

- 7. EA Insight

- 8. Frequently Asked Questions

- 9. Related Articles

- 10. Official Resources

1. Meet David

David is 62. He received his green card 18 months ago, after decades of waiting. The work he did during those long years — informal, paid in cash — was never recorded with the Social Security Administration.

Once his status came through, David registered as a sole proprietor and opened a small alterations shop near his home. About a year and a half later, his grandson sat with him at the kitchen table and helped him create a my Social Security account at ssa.gov. The screen loaded a single summary of his entire working life in the United States.

Twenty-two credits. Most of them earned during a short period of legal work as a student decades earlier. About six credits had been added since his green card. He needed eighteen more to qualify for retirement benefits — and the law caps credit accumulation at four per year.

David’s situation isn’t unusual. Anyone whose work authorization came late in life — through a long-delayed green card, an asylum approval, or a status change — can end up looking at a Social Security record that doesn’t match the years they’ve actually worked.

2. How Social Security Credits Work

To qualify for Social Security retirement benefits on your own record, you need 40 credits over your lifetime. The maximum is four credits in any single calendar year, no matter how high your earnings. Forty credits roughly translates to ten years of covered work, though it doesn’t have to be ten consecutive years.

What earns a credit isn’t time worked — it’s covered earnings, meaning income subject to Social Security tax. The dollar threshold rises each year as average wages rise.

| Year | 1 Credit Requires | 4 Credits (Max) |

|---|---|---|

| 2024 | $1,730 | $6,920 |

| 2025 | $1,810 | $7,240 |

| 2026 | $1,890 | $7,560 |

For W-2 employees, covered earnings appear in Box 3 of the W-2. For self-employed workers, covered earnings are net earnings from self-employment, calculated on Schedule SE as 92.35% of Schedule C net profit. Per SSA Publication 05-10072, the self-employed earn credits the same way employees do — one credit per $1,890 in 2026, capped at four per year.

3. David’s Numbers: The 4-Credit Threshold

To earn the maximum 4 credits in 2026, David needs net SE earnings of at least $7,560. Dividing by 92.35% gives a Schedule C net profit of $8,186.

Bottom line

$8,186 isn’t sales. It’s what’s left after fabric costs, rent, utilities, supplies, and every other allowable business expense. A shop bringing in $25,000 in revenue with $20,000 in expenses produces only $5,000 in net profit — not enough for 4 credits.

For David, the alterations shop comfortably clears that threshold in a normal year. Here’s what he owes in self-employment tax on $7,560 of net SE earnings:

| Calculation | Amount |

|---|---|

| Net SE earnings × 15.3% | $1,157 SE tax |

| Half deductible on Schedule 1 | $578.50 reduces AGI |

| Federal income tax at this earnings level | Largely absorbed by standard deduction |

At David’s modest income level, federal income tax is mostly absorbed by the standard deduction. The $1,157 of SE tax is essentially his full out-of-pocket cost for the year — and it isn’t a tax in the ordinary sense. It’s a contribution toward his own future Social Security and Medicare eligibility, recorded under his name and SSN.

Four or five years of this kind of contribution — roughly $5,000 total — would purchase David lifetime monthly retirement benefits plus premium-free Medicare Part A starting at age 65.

4. The Self-Employment Trap: The 3-Year Rule

David’s next question was the one almost every late-starter asks first:

Partly yes. Mostly no. And the “no” part catches almost everyone by surprise.

The SSA Deadline Is Different from the IRS Deadline

Self-employment income has its own SSA reporting deadline, separate from the IRS refund statute. Under Social Security Act §205(c)(1)(B) and the regulations at 20 CFR §404.802:

Self-employment income is credited to your SSA earnings record only if the tax return is filed within 3 years, 3 months, and 15 days after the close of the tax year in which the income was earned.

That deadline isn’t the same as the IRS three-year refund statute. You can file late returns with the IRS years after the fact to settle tax owed. But for Social Security credit purposes, once the 3-year-3-month-15-day window closes, the income generally never gets credited (see SSR 65-42c and GAO/GGD-99-18).

W-2 wages don’t have this problem. Employers report wages to SSA quarterly, so late corrections can usually be reconciled through SSA’s earnings record correction process. Self-employment is on you — and once the window closes, it doesn’t reopen.

What David Could Still Claim in 2026

| SE Income Year | SSA Credit Deadline | Status (May 2026) |

|---|---|---|

| 2025 | April 15, 2029 | Open |

| 2024 | April 15, 2028 | Open |

| 2023 | April 15, 2027 | Open |

| 2022 | April 15, 2026 | Closed (IRS-only catch-up possible) |

| 2021 or earlier | Expired | No SSA credit |

Important: The 2026-specific deadlines in this table apply as of May 2026. Each year, the window shifts forward — 2023’s deadline becomes the new “use it or lose it” year in April 2027, and so on.

David’s Recovery Plan

David filed self-employment returns for tax years 2023, 2024, and 2025 — adding 12 credits to his record. Combined with the 22 he already had, his total reached 34. Two more years of timely filing — 2026 and 2027 — bring him to 42 credits by early 2028, comfortably ahead of his full retirement age of 67.

5. When Net Earnings Fall Short: The Optional Method

Some years a small business has revenue but very little net profit. Materials cost more than expected, rent goes up mid-year, or a slow season eats the margin. When net SE earnings fall below $7,560, the worker risks losing credits for the year — even with reasonable gross income.

The Non-farm Optional Method on Schedule SE, Part II, exists for exactly this situation. It lets a self-employed taxpayer report two-thirds of gross self-employment income (up to $7,560 in 2026) as net SE earnings, instead of actual net profit. Done correctly, it can preserve the year’s 4 credits even when the bottom line came in thin.

This isn’t a routine planning tool. A few things to know before electing it:

- Lifetime cap: the Non-farm Optional Method can be used a maximum of five times over a worker’s lifetime.

- Eligibility thresholds apply to both gross and net SE figures — not every low-profit year qualifies.

- SE tax consequence: you pay SE tax on the elected amount, not on actual net earnings. The tradeoff is real money for a future-credit benefit.

Whether to use one of those five lifetime elections in any given year depends on the gap between gross and net, how many credits are still needed, and how close the worker is to retirement. If your net SE earnings are heading below the credit threshold this year, work the numbers with an EA before you file. Once the return is submitted, the election is locked in.

6. What to Check Right Now

- Create a my Social Security account at ssa.gov and view your exact lifetime credit count.

- Calculate your gap: 40 minus your current credits = years of work still needed.

- List every self-employment year you didn’t file. Mark which ones are still within the 3-year-3-month-15-day window.

- If tax year 2022 is on that list, act before April 15, 2026 — it’s the last year on the calendar for SSA credit purposes as of this writing.

- For every year going forward, target Schedule C net profit of at least $8,186 (2026 figure) to lock in the full 4 credits.

- If you’ve worked in a country with a U.S. Totalization Agreement (about 30 nations, including South Korea), find out whether those foreign credits can count toward U.S. eligibility.

- If gross income is solid but net will fall short this year, ask about the Non-farm Optional Method before filing.

EA Insight

The most dangerous assumption I see from late-starters is this one: “I’ll file everything from past years and the credits will all catch up.” For self-employment income, that’s not how the system works.

I’ve sat across the table from clients who’ve worked seven or eight years without filing a single return — diligent people who walked in ready to clean it all up. Explaining that the IRS will accept the late filings, but SSA won’t credit anything older than 3 years, 3 months, and 15 days, is one of the hardest conversations in this profession. The paperwork can be finished. The retirement record can’t.

On the other side, I see clients with newly issued green cards running small businesses who try to push Schedule C net profit down to minimize SE tax. Saving $1,000 a year on SE tax sounds attractive — until you realize it can mean falling short of the credits needed to qualify for benefits worth tens of thousands of dollars over retirement. SE tax isn’t money disappearing into a hole. It’s the only mechanism by which your self-employment work builds a Social Security and Medicare record under your name.

If your work authorization came late, don’t start by calling a tax preparer. Start by opening a my Social Security account and reading your record. Once you can see exactly where the gaps are, the path to 40 credits becomes a planning problem rather than a vague worry.

EA Summary

Earning Social Security credits isn’t hard. The trap is time. Self-employment income only counts toward your record if the return is filed within 3 years, 3 months, and 15 days of year-end. For anyone whose work authorization came late in life: check your SSA record first, file any open years before the windows close, and target adequate Schedule C net profit each year going forward.

Frequently Asked Questions

Does work I did in another country count toward U.S. Social Security?

Usually not on its own. The exception is countries that have a Totalization Agreement with the U.S. — about 30 nations, including South Korea, Canada, the U.K., Germany, and most of Europe. Credits from those countries can be combined with U.S. credits for eligibility purposes. The U.S. benefit amount is still computed from U.S.-side contributions, but the combined record can be the difference between qualifying for any benefit and qualifying for none.

I filed self-employment returns under an ITIN before I got my SSN. Do those count?

Generally no. Social Security credits are tied to SSN-based earnings. Self-employment income filed under an ITIN stays in IRS records but does not transfer to your SSA earnings record. From the date your SSN is issued, future earnings build credit normally.

Can I lower my Schedule C net profit to reduce SE tax?

Net profit must reflect actual income and actual deductible expenses — claiming fewer earnings than you really had isn’t allowed. Beyond that, lowering net profit means fewer Social Security credits. The $1,157 of SE tax on $7,560 of net SE earnings isn’t a cost in the ordinary sense — it’s the entry fee for that year’s four credits and the lifetime benefits attached to them.

Do W-2 wages count differently from self-employment income?

The credits work the same way — Box 3 Social Security wages count toward the same annual maximum of four credits. The big difference is reporting. W-2 employers report wages to SSA quarterly, so errors can usually be reconciled through SSA’s correction process. Self-employed workers report through Schedule SE on the tax return, and the 3-year-3-month-15-day deadline applies.

What happens if I never reach 40 credits?

You won’t qualify for retirement benefits on your own record. If your current spouse — or a former spouse you were married to for at least 10 years — has 40 credits, you may qualify for spousal benefits based on their record. Medicare Part A works similarly: a spouse’s record can sometimes provide premium-free eligibility, or you can buy in by paying the Part A premium yourself once you turn 65.

Official Resources

- SSA — How You Earn Credits (Publication 05-10072)

- SSA — If You Are Self-Employed (Publication 05-10022)

- SSA — Benefits Planner: Social Security Credits and Benefit Eligibility

- SSA — How Do I Earn Social Security Credits?

- SSA — International Totalization Agreements

- IRS — About Schedule SE (Self-Employment Tax)

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and Social Security regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.