Standard Deduction vs. Itemized Deductions — Which Saves You More?

One of the most fundamental choices on every tax return: take the flat-dollar Standard Deduction, or list your actual expenses on Schedule A? Most taxpayers come out ahead with the Standard Deduction — but if you carry a mortgage, pay high state and local taxes, or make significant charitable contributions, itemizing could put more money back in your pocket.

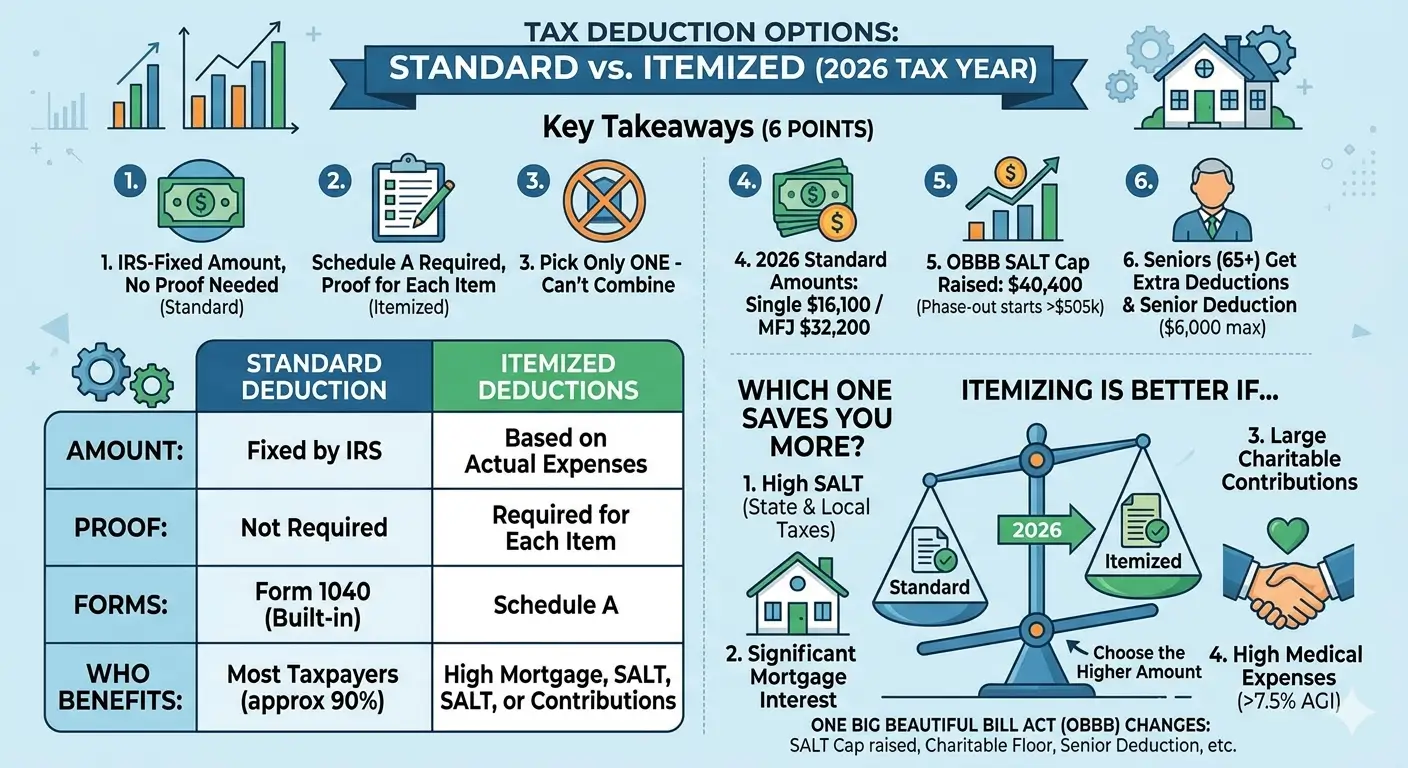

Key Takeaways

- The Standard Deduction is a fixed dollar amount set by the IRS each year — no receipts or documentation required.

- Itemized Deductions let you deduct specific expenses (SALT, mortgage interest, charitable gifts, medical costs) on Schedule A, but you must keep records for every item.

- You must choose one or the other — you cannot claim both on the same return.

- For tax year 2026: Single $16,100 | MFJ $32,200 | HOH $24,150.

- The SALT deduction cap rose to $40,400 for 2026 under the One Big Beautiful Bill Act (OBBB), making itemizing attractive again for some taxpayers in high-tax states.

- Taxpayers age 65 and older may qualify for both the Additional Standard Deduction and the new Senior Deduction (up to $6,000 per person) — regardless of whether they itemize or take the Standard Deduction.

Table of Contents

1. What Is the Standard Deduction?

The Standard Deduction is a fixed dollar amount that the IRS sets each year. It reduces your taxable income automatically — no receipts, no documentation, no Schedule A required. The vast majority of taxpayers (roughly 90%) choose the Standard Deduction because it is simple and, for most filing situations, provides a larger benefit than itemizing.

| Filing Status | Standard Deduction (2026) |

|---|---|

| Single | $16,100 |

| Married Filing Jointly (MFJ) | $32,200 |

| Married Filing Separately (MFS) | $16,100 |

| Head of Household (HOH) | $24,150 |

Extra Deductions for Taxpayers Age 65 and Older

If you are 65 or older (or legally blind), you qualify for an Additional Standard Deduction on top of the base amount. For tax year 2026, this additional amount is $2,050 for Single and Head of Household filers, or $1,650 per person for Married Filing Jointly filers.

On top of that, the One Big Beautiful Bill Act (OBBB) created a separate Senior Deduction worth up to $6,000 per qualifying taxpayer ($12,000 if both spouses on a joint return are 65 or older). Unlike the Additional Standard Deduction, the Senior Deduction is available whether you take the Standard Deduction or itemize — but it begins to phase out at a 6% rate when income exceeds $75,000 (Single) or $150,000 (MFJ). This deduction is available through the 2028 tax year.

Don’t confuse the two: The Additional Standard Deduction is a long-standing provision available only when you take the Standard Deduction. The Senior Deduction is a new OBBB provision available regardless of your deduction method. Eligible taxpayers can claim both.

Who Cannot Take the Standard Deduction?

In certain situations, the Standard Deduction is not available. You cannot claim it if your spouse files separately and itemizes, if you file as a nonresident alien, or if your tax year covers fewer than 12 months due to a change in accounting period.

2. What Are Itemized Deductions?

Itemized Deductions allow you to deduct specific expenses you actually paid during the year. Instead of accepting the IRS’s flat-dollar Standard Deduction, you list each qualifying expense on Schedule A (Form 1040) and deduct the total. This approach requires documentation — receipts, Form 1098 statements, donation acknowledgment letters, and other records.

Schedule A is divided into several categories:

State and Local Taxes (SALT)

You may deduct state and local income taxes (or general sales taxes, whichever is higher), real estate taxes, and qualified personal property taxes. For tax year 2026, the SALT deduction cap is $40,400 ($20,200 for Married Filing Separately). However, this cap phases down for taxpayers with MAGI above $505,000 ($252,500 for MFS) — reducing by 30% of the excess until the cap reaches $10,000.

Mortgage Interest

Interest on a mortgage for your primary residence or a second home is deductible. For loans taken out after December 15, 2017, the deduction is limited to interest on the first $750,000 of qualifying debt ($375,000 for MFS). The OBBB made this cap permanent.

Charitable Contributions

Cash and property donations to qualified organizations are deductible. Cash contributions are generally limited to 60% of AGI. Starting in 2026, a new 0.5% AGI floor applies — the first 0.5% of your AGI in charitable contributions is not deductible. For example, if your AGI is $200,000, the first $1,000 of contributions produces no tax benefit.

Medical and Dental Expenses

Unreimbursed medical and dental expenses are deductible, but only the portion that exceeds 7.5% of your AGI. If your AGI is $80,000, only expenses above $6,000 count toward your deduction.

Casualty and Theft Losses

Personal casualty and theft losses are deductible only if they occur in a federally declared disaster area.

Other Itemized Deductions

This category includes gambling losses (deductible only up to gambling winnings) and investment interest expense. Note that beginning in 2026, the gambling loss deduction is limited to 90% of actual losses — a change from the prior rule that allowed 100% of losses up to the amount of winnings. The 2% miscellaneous itemized deductions (unreimbursed employee expenses, tax preparation fees, etc.) were permanently repealed under OBBB.

3. Side-by-Side Comparison

| Feature | Standard Deduction | Itemized Deductions |

|---|---|---|

| Amount | Fixed by IRS each year | Varies based on actual spending |

| Documentation | None required | Receipts and records for every item |

| Filed On | Form 1040 (automatic) | Schedule A (Form 1040) |

| Who Benefits Most | Most taxpayers (~90%) | Homeowners with large mortgages, high-SALT-state residents, generous donors |

| Can Both Be Claimed? | No — you must choose one or the other each year | |

| MFS Rule | If one spouse itemizes, the other must also itemize | |

4. When Is Itemizing the Better Choice?

The decision rule is straightforward: if your total itemized deductions exceed your Standard Deduction, itemizing saves you more.

You are more likely to benefit from itemizing if you live in a high-tax state (New York, New Jersey, California, Connecticut) where property taxes and state income taxes are substantial, if you are in the early years of a mortgage when interest payments are at their highest, if you make significant charitable contributions each year, or if you had unusually large unreimbursed medical expenses during the year (exceeding 7.5% of your AGI).

On the other hand, if you rent rather than own, live in a state with no income tax and low property taxes, and make modest charitable gifts, the Standard Deduction will almost certainly be the better option.

5. What Changed Under OBBB

The One Big Beautiful Bill Act (signed July 2025) made significant changes to both the Standard Deduction and Itemized Deductions. Here is what is different starting with tax year 2025 and beyond:

Standard Deduction Side

The base Standard Deduction was increased starting in 2025 (Single $15,750 / MFJ $31,500), with inflation adjustments continuing each year — reaching Single $16,100 / MFJ $32,200 for tax year 2026. OBBB also created the new Senior Deduction for taxpayers age 65 and older, worth up to $6,000 per person, available through the 2028 tax year regardless of whether you itemize or take the Standard Deduction.

Itemized Deductions Side

| Change | Before OBBB | After OBBB |

|---|---|---|

| SALT Cap | $10,000 | Raised to $40,000+ with 1% annual increases through 2029; reverts to $10,000 in 2030 (see table below) |

| SALT Phase-Down | None | Begins at MAGI $505,000 (2026); cap reduces to $10,000 for highest earners |

| Charitable Floor | No floor | 0.5% of AGI floor starting 2026 |

| Non-Itemizer Charitable Deduction | Not available | Up to $1,000 (Single) / $2,000 (MFJ) for cash gifts — above-the-line |

| Mortgage Interest Cap | $750,000 (set to expire) | $750,000 — made permanent |

| Gambling Loss Limit | 100% of losses (up to winnings) | 90% of losses (up to winnings) — starting 2026 |

| Pease Limitation | Suspended (TCJA) | Permanently repealed; replaced with a new limit for taxpayers in the 37% bracket |

Important: The 2% miscellaneous itemized deductions — unreimbursed employee expenses, tax preparation fees, investment advisory fees — were permanently repealed by OBBB. These deductions are no longer available.

SALT Cap by Year

| Tax Year | SALT Cap | Phase-Down Starts At (MAGI) |

|---|---|---|

| 2018–2024 | $10,000 | N/A |

| 2025 | $40,000 | $500,000 |

| 2026 | $40,400 | $505,000 |

| 2027 | $40,804 | $510,050 |

| 2028 | $41,212 | $515,151 |

| 2029 | $41,624 | $520,302 |

| 2030+ | $10,000 | N/A (unless Congress acts) |

Note: The SALT cap and phase-down threshold each increase by 1% annually. The 2027–2029 figures shown above are projections based on the statutory 1% formula. Actual amounts will be confirmed by the IRS each year. MFS filers use half of the amounts shown.

6. Real-Life Examples

Example A — Single Renter in New York

| Itemized Expense | Amount |

|---|---|

| State income tax | $4,500 |

| Charitable contributions | $500 |

| Medical expenses above 7.5% AGI | $0 |

| Total Itemized | $5,000 |

Standard Deduction: $16,100. Total itemized deductions: $5,000. The Standard Deduction is $11,100 larger — the clear winner.

Example B — Married Couple, Homeowners in New Jersey

| Itemized Expense | Amount |

|---|---|

| Property taxes | $12,000 |

| State income tax | $9,500 |

| Mortgage interest | $14,000 |

| Charitable contributions | $3,000 |

| Total Itemized | $38,500 |

Standard Deduction (MFJ): $32,200. Total itemized deductions: $38,500. Itemizing produces $6,300 more in deductions — a meaningful tax savings, especially for taxpayers in the 22% or 24% bracket.

Example C — Single, Age 66, Retired in Texas

| Itemized Expense | Amount |

|---|---|

| Property taxes | $5,000 |

| Sales tax | $1,200 |

| Charitable contributions | $2,000 |

| Total Itemized | $8,200 |

This taxpayer’s Standard Deduction stack: $16,100 (base) + $2,050 (Additional, age 65+) + up to $6,000 (Senior Deduction) = up to $24,150. Total itemized: $8,200. The Standard Deduction wins by nearly $16,000.

Note: These examples use simplified figures. Actual tax savings depend on your full tax picture, including filing status, income level, applicable phase-outs, and state tax rules.

7. Common Mistakes

“I have lots of deductible expenses, so itemizing must be better.”

The number of expenses does not matter — only the total dollar amount. Five itemized deductions adding up to $10,000 still lose to a $16,100 Standard Deduction.

“My spouse itemizes, but I’ll take the Standard Deduction.”

If you file as Married Filing Separately and your spouse itemizes, you must also itemize. You cannot mix methods on separate returns.

“I itemized last year, so I have to do it again this year.”

You make this choice fresh every year. As your mortgage balance drops, your interest payments shrink. As the Standard Deduction rises with inflation, the crossover point shifts. Compare both options annually.

“All my charitable donations are fully deductible.”

Starting in 2026, the new 0.5% AGI floor means the first portion of your contributions may not produce any deduction. With an AGI of $200,000, the first $1,000 in charitable gifts is nondeductible.

EA Insight

Two patterns come up repeatedly in my practice.

First, homeowners in the early years of a mortgage often benefit from itemizing because interest makes up the bulk of their payments. But as the loan amortizes, the interest portion shrinks — and at some point, the Standard Deduction becomes larger. Many taxpayers miss this crossover and keep itemizing out of habit, leaving money on the table.

Second, the SALT cap increase to $40,400 under OBBB has brought some high-tax-state taxpayers back to itemizing after years of taking the Standard Deduction. This is real and meaningful relief — but it is temporary. The cap is scheduled to revert to $10,000 in 2030. Building a long-term financial plan around the current cap as though it will last indefinitely is a risk I caution clients against.

Every year before you file, run the numbers both ways. Even if you use tax software, verify which method the software selected — and confirm that it chose correctly for your situation.

Frequently Asked Questions

Can I take the Standard Deduction and still deduct charitable donations?

Yes — starting in 2026, taxpayers who take the Standard Deduction may deduct up to $1,000 (Single) or $2,000 (MFJ) in cash contributions to qualified operating charities as an above-the-line deduction. This benefit does not apply to donations of appreciated property or contributions through donor-advised funds.

Does owning a home automatically make itemizing better?

Not necessarily. If your mortgage balance is small, your interest payments may be low enough that the Standard Deduction still exceeds your total itemized deductions. This is especially common later in a mortgage term when payments shift toward principal rather than interest.

Do state tax returns follow the same choice?

Not always. Federal and state returns are separate. Some states require you to use the same method you chose on your federal return. Others allow a different choice, and some states have their own standard deduction amounts. Check your state’s rules.

What form do I file if I itemize?

You complete Schedule A (Form 1040) and attach it to your tax return. If you take the Standard Deduction, you simply enter the amount on Form 1040 — no additional schedule is needed.

Can I switch from the Standard Deduction to itemizing after I file?

Yes. You can change your deduction method by filing an amended return (Form 1040-X) within the original filing deadline, including extensions. If you discover that itemizing would have saved more, you can switch — and vice versa.

What is the SALT cap, and will it stay at $40,400?

The SALT (State and Local Tax) deduction cap limits how much state and local tax you can deduct on your federal return. Under OBBB, the cap rose from $10,000 to $40,000 for 2025 and increases by 1% each year through 2029 ($40,400 for 2026). Unless Congress acts, the cap reverts to $10,000 in 2030.

Official Resources

- IRS — About Schedule A (Form 1040)

- IRS — Itemized Deductions, Standard Deduction FAQ

- IRS — New and Enhanced Deductions for Individuals

- IRS — Revenue Procedure 2025-32 (2026 Inflation Adjustments)

- IRS Publication 501 — Dependents, Standard Deduction, and Filing Information

- IRS Publication 936 — Home Mortgage Interest Deduction

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.