He Made $24K Trading. He Owed $40K in Tax.

David thought he’d cleared a small profit on a year of active trading. Then his 1099-B arrived — and he owed the IRS just over forty thousand dollars. The number that broke his math was hiding in Box 1g.

Key Takeaways

- The wash sale rule (IRC §1091) blocks a loss deduction when you buy the same security — or one substantially identical — within 30 days before or after a loss sale.

- The window is 61 days total: 30 before, the sale day, 30 after. Many traders only count the 30 after.

- In a taxable account the disallowed loss isn’t lost — it shifts into the basis of the replacement shares. In an IRA, it’s destroyed.

- Box 1g on your 1099-B reports the disallowed amount. Don’t file without checking it.

- Brokers track wash sales only inside their own accounts. Cross-broker, IRA, and spouse trades are on you.

- Crypto isn’t currently covered by §1091, but a congressional discussion draft introduced in late 2025 could change that within the year. Spot Bitcoin ETFs are already a different story.

Table of Contents

1. Meet David

David Park is 36. Software engineer at a Seattle tech company. W-2 base of $185,000.

He started buying stocks in 2020, locked at home like everyone else. The first few years it was just index ETFs — set them and forget them. Things shifted in 2024. NVIDIA, Tesla, AMD, Palantir. The same tickers, in and out, week after week. By December he’d run some names through five separate round trips.

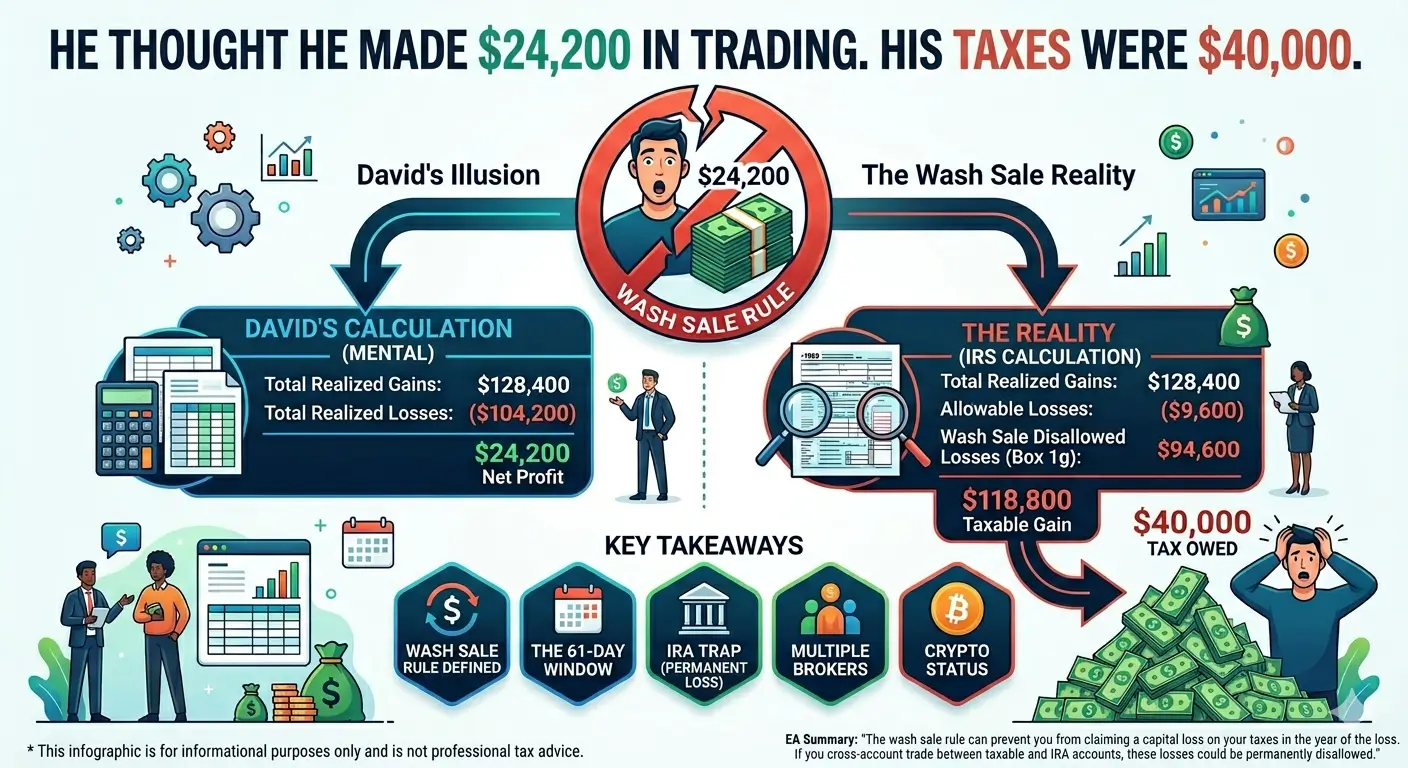

His own math told him he’d booked about $128,400 in gains against $104,200 in losses. Net for the year: roughly $24,000. He plugged his W-2 and his net trading gain into a couple of YouTube tax calculators. Both spit back numbers in the low three thousands. He was ready to owe maybe $2,500.

In March he opened TurboTax, imported his 1099-B, and stared at the screen. The capital gain figure was $118,800. Almost five times what he’d calculated.

“I figured I cleared about twenty-five grand. Maybe owe two or three thousand. Then the 1099-B came.”

2. The Wash Sale Rule — Section 1091

The rule lives in Internal Revenue Code §1091. The mechanics are simple. The consequences aren’t.

Sell a stock at a loss. Look at the calendar. If you bought — or buy — the same stock (or one the IRS treats as “substantially identical”) within 30 days before or 30 days after that loss sale, the loss is disallowed for that year.

Notice both directions. The window opens 30 days before the sale, includes the sale day, and runs 30 days after. Sixty-one days total. A January 5 purchase can wash-sale a January 28 loss. “I didn’t sell anything in December” doesn’t save you.

A disallowed loss isn’t gone forever — usually. The amount tacks onto the cost basis of the replacement shares. When you eventually sell those shares, the embedded loss comes back through. It’s a deferral, not a disappearance.

That last sentence has one giant exception. Hold that thought for Section 4.

3. David’s Case — Where the Math Broke

Here’s what David’s 1099-B actually showed:

| Line Item | Amount |

|---|---|

| Total realized gains | $128,400 |

| Total realized losses | ($104,200) |

| David’s expected net | $24,200 |

| Wash sale loss disallowed (Box 1g) | $94,600 |

| Allowed losses | ($9,600) |

| Actual taxable gain | $118,800 |

$94,600 of his losses got blocked. Only $9,600 came through.

Now the income side. David’s W-2 of $185,000 plus $118,800 of trading gain pushed his marginal income into the 32% federal bracket and a slice of it into 35%. Most of his trades closed inside a year, so the gains were short-term — taxed at ordinary rates, not the long-term capital gains rates he’d been using in his head.

Federal tax on the trading slice landed around $36,800. NIIT at 3.8% on the investment-income portion added another $3,900. Washington state has no income tax, so nothing on that line. Round it together: just over $40,000 of additional tax on a year David thought had cleared $24,000.

⚠ Brokers only see their own accounts. Robinhood doesn’t know what you bought at Fidelity. If the same ticker is moving across two brokers, each 1099-B may look clean on its own — but combined, they can hide wash sales neither broker reported. Reconciling that is your job, not theirs.

4. What If the Situation Were Different

A. He waited 31 days before rebuying

The window closes on day 31. Same loss, no rebuy inside the window — full $94,600 deductible. David’s actual taxable gain would have been around $24,000 instead of $118,800. The tax hit drops below $9,000. A thirty-thousand-dollar swing on a calendar.

B. He bought the replacement in his IRA

This is where the rule turns ugly. Rev. Rul. 2008-5 says: when a wash sale gets triggered by a purchase inside an IRA, the disallowed loss does not get added to the IRA shares’ basis. IRAs don’t have basis the way taxable accounts do. The loss isn’t deferred — it’s permanently destroyed.

Sell NVDA at a loss in your taxable Schwab account on Tuesday. Buy NVDA in your Roth IRA at Fidelity on Thursday. The loss is gone. No future basis bump. No recovery. Nothing.

C. His spouse bought it in her account

Spouses count as the same taxpayer for wash sale purposes. If David’s wife bought NVDA in her own brokerage during the 61-day window, his loss still gets disallowed. And filing MFS doesn’t save you — the rule looks at the economic relationship, not the filing status.

D. He used options instead

§1091 covers stocks, securities, and contracts or options to acquire them. An in-the-money call on the same underlying is almost certainly substantially identical. Switching from common stock to a deep ITM call as your “replacement” isn’t an escape hatch.

5. Limits, Gray Areas, and the Crypto Question

“Substantially identical” — the part that’s never been clearly defined

Same company’s common stock: clearly identical. Different companies: clearly not. The middle is fuzzy.

Two ETFs tracking the same index (SPY and VOO, both S&P 500): the IRS has never issued definitive guidance, and most practitioners treat the swap as risky enough to avoid. Two ETFs tracking different indexes (S&P 500 and Russell 2000): generally considered safe replacements. Selling an index ETF and buying one of its individual holdings doesn’t trigger the rule — selling QQQ at a loss and buying NVDA isn’t a wash sale, since an ETF and one of its 100 underlying names aren’t substantially identical.

Crypto — the loophole that may be closing

As of April 2026, the wash sale rule does not apply to spot cryptocurrency. The IRS classifies digital assets as property, and §1091 reaches only stocks and securities. Sell Bitcoin at a loss on Monday, buy it back on Tuesday, claim the full loss — legal under current law.

That picture is shifting. A bipartisan congressional discussion draft introduced in late 2025 would expand §1091 to cover digital assets. The proposal is gathering stakeholder feedback and has been signaled to advance during 2026. If it passes, the crypto wash-sale exemption ends.

Spot Bitcoin ETFs are already different territory. Products like IBIT and FBTC are securities, even though they hold crypto, so brokers routinely apply wash sale adjustments to them on Form 1099-B. If your crypto exposure runs through an ETF, treat it as stock for wash sale purposes.

Mark-to-market traders (§475(f) election)

Traders who qualify as a trader in securities and make a §475(f) mark-to-market election aren’t subject to wash sale rules at all. The qualification bar is high — substantial activity, regular and continuous, primary livelihood — and the election is hard to reverse once made. High-volume retail trading doesn’t automatically meet the standard, no matter how active your account looks.

6. What to Check Right Now

- Pull every 1099-B you received and look at Box 1g — Wash Sale Loss Disallowed. Compare it to your gut sense of the year. If it’s bigger than you expected, your tax bill probably is too.

- If you trade the same ticker across multiple brokers, build your own combined spreadsheet. Brokers don’t reconcile wash sales across each other.

- Stop trading the same security in your taxable account and your IRA. The cost of one accidental cross-account wash sale is the entire loss, permanently.

- If you’re married — jointly or separately — your spouse’s account counts. Make sure you’re not unknowingly trading the same names.

- For tax-loss harvesting: wait 31 days before rebuying, or rotate into a security tracking a meaningfully different index. A single stock inside an index ETF is safe. A different ETF on the same index is not.

- Year-end loss sells in late December that get rebought in early January are the single most common way taxpayers wash-sale themselves. If you’re going to do it, do it deliberately and price in the consequence.

💡 EA Insight

The reason wash sales blindside people isn’t the rule itself. It’s that the rule runs against the way active traders think.

A couple in their early sixties came to me last fall. Husband running his own IRA, getting close to retirement. He’d been holding a biotech stock that tanked, and in October he cleaned it out of his taxable account at a $62,000 loss. Same week, he opened a new position in the same biotech inside his Roth IRA. His thinking was straightforward: harvest the loss in the taxable, ride the recovery in the Roth.

When he came in the following March expecting to claim that $62,000, I had to print Rev. Rul. 2008-5 and walk him through it line by line. The loss wasn’t deferred. It was gone. His face went somewhere I’d rather not see again.

Three things I find myself repeating to active trader clients:

“I didn’t sell in December, so no wash sales.” The window opens before the sale. A January 5 purchase can wash-sale a January 28 loss. The forward-looking 30 days catches less than half of these cases.

“It’s just a deferral, I’ll get it back later.” True for taxable. False for IRAs. Worth saying twice.

“My broker handles all this.” Your broker handles their own account. Cross-broker, IRA, spouse, and any LLC you control are all invisible to them.

Here’s the part most people don’t realize: the window for fixing wash sale exposure isn’t tax season — it’s mid-December. By the time the 1099-B shows up in February, every disallowance is already locked in. Nothing can be undone. But in mid-December you still have 31-day room. You can pull together every account you and your spouse trade, identify the loss positions you’ve already sold and the names you’ve rebought too quickly, and either wait the calendar out or accept the disallowance with eyes open. That two-week window in December is when wash sales actually get fixed. The April conversation is just damage assessment.

In Short

The wash sale rule doesn’t usually take your loss away — it takes away your right to choose when you use it. In a taxable account, the loss is deferred. In an IRA, it’s destroyed. If you trade actively, the only number on your 1099-B that matters more than your gain is Box 1g. Look at it before you file.

FAQ

Does a disallowed wash sale loss disappear forever?

In a taxable brokerage account, no. The disallowed amount adds to the cost basis of your replacement shares and comes back when you eventually sell them. The exception is wash sales triggered by IRA purchases (Rev. Rul. 2008-5), where the loss is permanently destroyed.

Does the wash sale rule apply to crypto?

Not as of April 2026. Spot cryptocurrency is property, not a security, so §1091 doesn’t reach it. Pending legislation could change that within the year. Spot Bitcoin ETFs and other crypto exposure held through securities are already subject to the rule.

Are options included?

Yes. Options on the same underlying — particularly in-the-money calls — are typically treated as substantially identical. You can’t sidestep a wash sale by switching from stock to options on that stock.

Is the 30-day window measured in trading days or calendar days?

Calendar days. Weekends and holidays count.

Do my spouse’s trades trigger a wash sale on my account?

Yes. Spouses are treated as the same taxpayer for wash sale purposes, and this applies whether you file jointly or separately.

Is selling SPY and buying VOO a wash sale?

Gray area. Both track the S&P 500, and the IRS has never issued a clear ruling on whether index ETFs tracking the same benchmark are substantially identical. Most practitioners treat the swap as risky and recommend rotating to a different index entirely.

My broker shows no wash sales — am I clear?

Only within that broker. If you traded the same ticker at another broker, in your IRA, or your spouse traded it, the wash sale exists but isn’t on any single 1099-B. You’re responsible for combining the picture.