The Uber Driver Who Got His First 1099

Marcus drove for Uber and DoorDash all year. Then two 1099-NECs landed in his mailbox in January — and he realized nobody had been withholding his taxes.

Key Takeaways

- Gig platform income is self-employment income. The platform doesn’t withhold federal tax, Social Security, or Medicare for you.

- You report the income and your business expenses on Schedule C. The bottom line — net profit — is what gets taxed.

- The standard mileage deduction is usually the largest expense for a driver. The 2026 rate is 72.5 cents per business mile.

- On top of regular income tax, you owe Self-Employment tax of 15.3% on net profit. Half of that is deductible.

- If you’ll owe $1,000 or more for the year, the IRS expects quarterly estimated payments. Skip them and you’ll likely owe a penalty.

Table of Contents

- 1. Meet Marcus

- 2. W-2 vs. 1099 — Why It Changes Everything

- 3. Schedule C — How the Math Actually Works

- 4. The Deductions a Driver Has to Catch

- 5. Self-Employment Tax — What the 15.3% Really Is

- 6. QBI and Quarterly Payments — Don’t Leave These on the Table

- 7. What to Check Right Now

- 8. EA Insight

- 9. Frequently Asked Questions

- 10. Related Articles

- 11. Official Resources

1. Meet Marcus

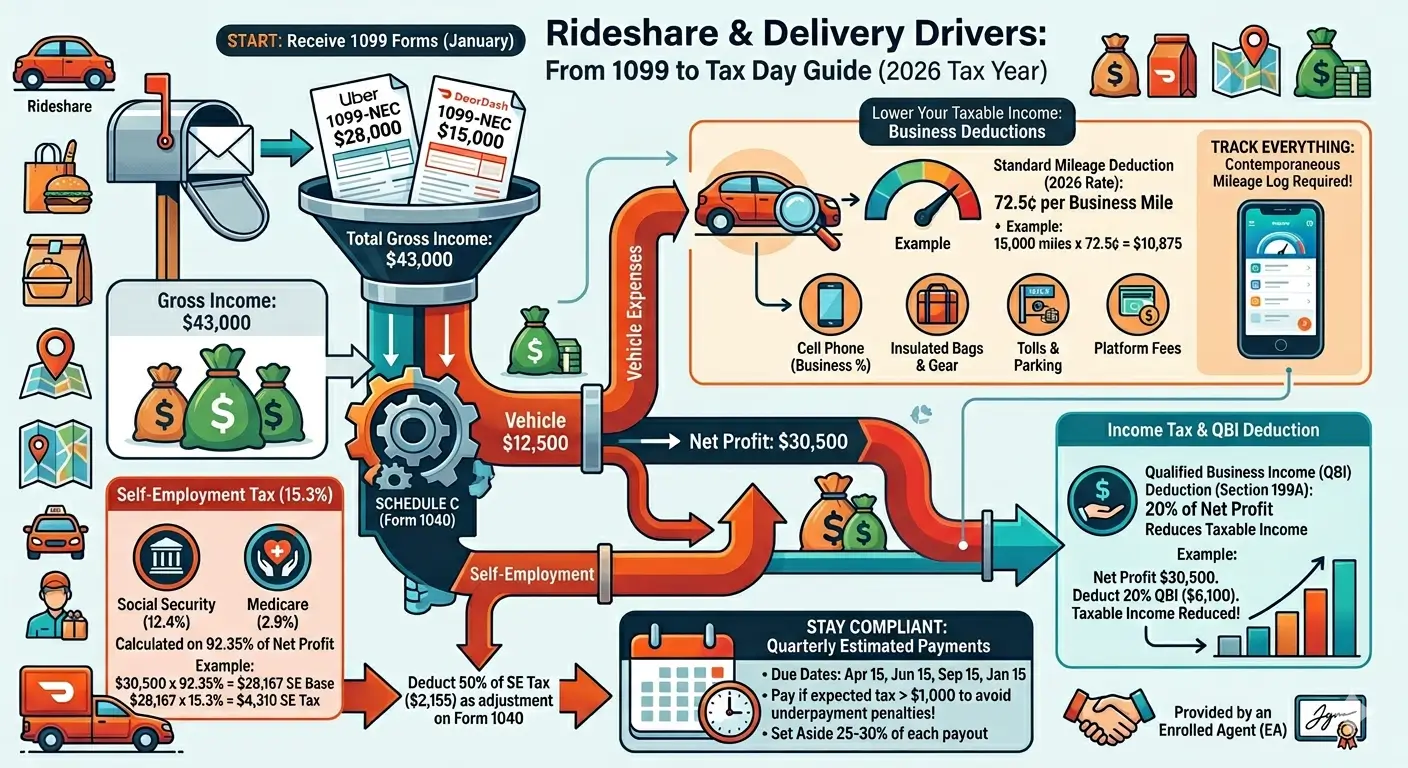

Marcus is in his early thirties. He drives for Uber during the day and switches to DoorDash in the evenings. Last year he took home about $43,000 between the two apps, which felt like decent money for a year of long hours. Then January arrived, and so did the mail.

Marcus isn’t unusual. Anyone who drives for Uber, Lyft, DoorDash, Instacart, or Amazon Flex ends up in the same spot the first year. The platforms classify drivers as independent contractors, not employees. That single classification rewires the entire tax picture.

2. W-2 vs. 1099 — Why It Changes Everything

A W-2 employee has a payroll department doing a lot of invisible work. Federal income tax gets withheld every paycheck. Social Security and Medicare get split fifty-fifty with the employer. By April, most of the tax is already paid.

An independent contractor has none of that. Marcus got his gross earnings deposited week after week, and not a dollar was set aside for the IRS. He’s the worker and the employer at the same time, which means he owes both halves of the payroll tax himself.

| Category | W-2 Employee | 1099 Independent Contractor |

|---|---|---|

| Income tax withholding | Employer withholds each paycheck | None — driver pays directly |

| Social Security + Medicare | Split with employer (7.65% each) | Driver pays full 15.3% |

| Business expense deductions | Generally not allowed | Fully deductible on Schedule C |

| Tax form received | W-2 | 1099-NEC (or 1099-K) |

Bottom line

Getting a 1099 means the IRS is telling you: “You’re running a business now. Handle it accordingly.”

Marcus pulled in $28,000 from Uber and $15,000 from DoorDash. Total gross: $43,000. That number is where his tax return starts, not where it ends.

3. Schedule C — How the Math Actually Works

Schedule C is the form sole proprietors use to report business income and expenses. The structure is simpler than the form length suggests: total revenue, minus business expenses, equals net profit. The net profit number is what the rest of the return runs on.

Combine the income

Marcus has two 1099-NECs, but he files one Schedule C. The IRS allows a single Schedule C when the activities are part of the same trade or business. Driving for Uber and delivering for DoorDash both count as the same activity — driving for hire. If Marcus also did freelance graphic design on the side, that would be a separate business and a separate Schedule C.

One Schedule C or two? Same line of work, one Schedule C. Different lines of work, separate Schedule Cs. A driver who also runs a small Etsy shop has two distinct businesses.

Subtract the business expenses

Gross income isn’t taxable income. Expenses incurred to run the business — gas, mileage, phone bills, supplies, fees — come off the top. The deductions section is where most drivers either save thousands or leave thousands on the table.

What’s left is net profit

Net profit drives both the income tax calculation and the Self-Employment tax calculation. Here’s how Marcus’s year shapes up after he tracks his expenses properly.

| Line item | Marcus’s number |

|---|---|

| Uber gross earnings (1099-NEC) | $28,000 |

| DoorDash gross earnings (1099-NEC) | $15,000 |

| Gross income | $43,000 |

| Business expenses (mileage + other) | – $12,500 |

| Net profit | $30,500 |

So Marcus earned $43,000, but only $30,500 hits the tax engine. That gap of $12,500 isn’t a loophole. It’s the cost of running his business — and tracking those costs is how he stops handing the IRS more than he owes.

4. The Deductions a Driver Has to Catch

For a rideshare or delivery driver, the single biggest deduction is mileage. Nothing else comes close.

Standard mileage — the big one

The 2026 IRS standard mileage rate is 72.5 cents per business mile. If Marcus logged 15,000 business miles last year, the math is straightforward:

15,000 miles × $0.725 = $10,875 in mileage deduction.

That single line item wipes out a quarter of his gross income before the IRS even gets a look. A serious full-time driver might log 25,000 to 40,000 business miles and stack up an even bigger deduction.

The catch: the deduction only counts if you have a contemporaneous mileage log. Date, starting point, ending point, business purpose, miles driven. Apps like Stride, Everlance, and MileIQ do this in the background. A retroactive estimate written the night before filing won’t survive an audit.

Standard mileage vs. actual expenses

Drivers can choose between the standard mileage rate and the actual expense method, which adds up gas, oil changes, insurance, depreciation, and so on. For most gig drivers using a personal car, standard mileage wins on both math and paperwork. There’s a wrinkle worth knowing though — if you start the first year on the actual expense method, you generally can’t switch back to the standard mileage rate for that vehicle. Starting with standard mileage keeps your options open.

The smaller deductions that add up

| Expense | Notes |

|---|---|

| Cell phone bill | Deduct the business-use percentage |

| Phone mount, charger, dashcam | 100% if used only for driving |

| Insulated delivery bags | Required gear for food delivery |

| Tolls and parking | Deductible on top of mileage |

| Platform fees and commissions | Only if not already netted out of your 1099 |

| Tax software or preparer fees | The business portion is deductible |

None of these are huge on their own. Together they often add another $1,000 to $2,000 in deductions. Hold onto receipts — a photo on your phone is fine, as long as you can find it later.

5. Self-Employment Tax — What the 15.3% Really Is

Here’s the part that catches first-time filers off guard. Self-Employment tax sounds like a separate, scary thing. It isn’t. It’s just Social Security and Medicare — the same payroll taxes a W-2 worker pays — except the gig driver pays both halves.

| Component | Rate | Note |

|---|---|---|

| Social Security (OASDI) | 12.4% | Applies to net earnings up to $184,500 for 2026 |

| Medicare | 2.9% | No income cap |

| Combined SE tax | 15.3% | Applied to 92.35% of net profit |

How Marcus’s SE tax actually calculates

The 15.3% rate applies to 92.35% of net profit, not the full amount. The 92.35% figure exists because the law treats half of SE tax as a business expense — it’s the same accommodation a W-2 employer gets when calculating its own payroll burden.

$30,500 net profit × 92.35% = $28,167 (SE tax base)

$28,167 × 15.3% = $4,310 in Self-Employment tax

And there’s a partial offset. Marcus gets to deduct half of that SE tax — about $2,155 — on the front of Form 1040 as an adjustment to income. It’s an above-the-line deduction, so he gets it whether or not he itemizes. It doesn’t reduce the SE tax itself, but it does shrink the income tax that gets piled on top.

Bottom line

SE tax isn’t a new tax. It’s the payroll tax a W-2 worker never sees, fully visible for the first time.

6. QBI and Quarterly Payments — Don’t Leave These on the Table

Two more things every gig driver needs on the radar. One saves money. The other prevents penalties.

The QBI deduction (Section 199A)

Section 199A lets self-employed taxpayers deduct up to 20% of their qualified business income. For Marcus, that’s 20% of $30,500, or roughly $6,100 knocked off his taxable income before the income tax brackets even apply.

The deduction has income limits, but they don’t affect a driver at Marcus’s income level. For 2026, the full 20% is available below $201,775 of taxable income for single filers ($403,500 for married filing jointly). The One Big Beautiful Bill Act made QBI permanent, so the deduction isn’t going anywhere.

Quarterly estimated payments

This is where first-year filers get burned. The IRS doesn’t wait until April. If you expect to owe $1,000 or more for the year, the IRS expects you to pay as you go — quarterly. Skip the quarterly payments and you’ll likely face an underpayment penalty even if you pay everything in full on April 15.

| Quarter | Income period | Payment due |

|---|---|---|

| Q1 | January – March | April 15 |

| Q2 | April – May | June 15 |

| Q3 | June – August | September 15 |

| Q4 | September – December | January 15 (next year) |

Marcus pays his quarterly estimates using Form 1040-ES. He can mail a check with the voucher, pay through IRS Direct Pay from his bank account, or set up an EFTPS account for automatic withdrawals. A practical rule of thumb: set aside roughly 25% to 30% of every gig payment in a separate savings account, and the quarterly bill is already covered.

7. What to Check Right Now

- Pulled the 1099-NEC (or 1099-K) from every platform you drove for last year — Uber, Lyft, DoorDash, Instacart, Amazon Flex, all of them

- Mileage tracker app installed and recording, even if you’re starting mid-year

- Receipts saved for phone bill, mounts, dash cam, insulated bags, tolls, parking

- One Schedule C started for all driving income, with gross income and expenses entered separately

- Self-Employment tax (Schedule SE) calculated, and half of it deducted as an adjustment to income

- QBI deduction (Section 199A) applied — 20% of net profit for most drivers

- Quarterly estimated payments scheduled in your calendar — April 15, June 15, September 15, January 15

- A separate savings account holding 25% to 30% of every gig payment for taxes

EA Insight

Four mistakes I see again and again on first-year gig returns.

One: no mileage log. A driver shows up in March with a guess — “I think I drove around 18,000 miles last year.” Without a contemporaneous log, that number is exposed in an audit. Install a tracker today, even if the year’s already half over. Some deduction is better than none, and next year is fully covered.

Two: counting commute miles as business miles. The drive from home to your first pickup of the day is generally personal commuting, not business. The clock starts when you accept your first ride or delivery. The home-office exception can change this, but most gig drivers don’t qualify for it, so the safe default is to exclude that first leg.

Three: double-deducting platform fees. Uber and DoorDash often report your gross fares on the 1099, then list service fees separately in your earnings statement. If the 1099 number is gross, you can deduct fees. If the 1099 number is already net, deducting them again is double-dipping. Pull the year-end summary from each app and reconcile before you file.

Four: skipping quarterly payments the first year. The most painful client conversations I have are with first-year drivers who owe $5,000 to $7,000 in April with nothing set aside. The fix is mechanical, not emotional — open a separate savings account, drop a percentage of every payout in there, send it to the IRS four times a year. Once the system is set up, it runs on autopilot.

EA Summary

A 1099 from Uber or DoorDash means you’re running a business, even if it doesn’t feel that way. You report income and expenses on Schedule C, pay 15.3% Self-Employment tax on the net profit, and claim the 20% QBI deduction to bring your taxable income down. Track mileage from day one, set aside roughly a quarter of each payout for taxes, and pay quarterly. Marcus’s panic about that first 1099 turned into a workable system in about an hour. Yours can too.

Frequently Asked Questions

If I drive for Uber and DoorDash, do I file two Schedule Cs?

No. Driving for both falls under the same trade or business — driving for hire — so one Schedule C combines the income and expenses. Two Schedule Cs come into play only when the activities are genuinely different lines of work.

I didn’t receive a 1099 because I earned under the threshold. Do I still report the income?

Yes. The reporting threshold determines when a platform must issue a 1099. It does not determine whether the income is taxable. All gig earnings are reportable, and net self-employment income of $400 or more triggers Self-Employment tax filing.

My car is also my personal car. Can I still deduct mileage?

Yes — you deduct only the business-use portion. The mileage log is what separates the business miles from the personal miles like grocery runs and commuting. Without that separation, the deduction collapses.

Why is the tax bill so much bigger than what a W-2 employee pays at the same income?

Two reasons. First, no employer is paying half of Social Security and Medicare for you. Second, no withholding has been happening all year, so the full bill arrives at once. The total tax burden is similar in percentage terms — it just lands differently.

Are there ways to lower the tax bill beyond mileage and QBI?

A SEP-IRA or Solo 401(k) contribution can shelter a meaningful portion of self-employment income. Self-employed health insurance premiums are deductible above the line. If business use of a home office qualifies, it adds another deduction. None of these change the fact that mileage is doing most of the heavy lifting for a driver, but they stack on top.

What happens if I just file in April and skip the quarterly payments?

If you owe $1,000 or more for the year, the IRS adds an underpayment penalty to the bill. The penalty is calculated quarter by quarter based on what you should have paid each period. It’s not catastrophic, but it’s a recurring cost that’s easy to avoid.

What if I got a 1099-K from Uber instead of a 1099-NEC?

Different form, same outcome. The 1099-NEC reports the platform’s payments to you as a contractor. The 1099-K reports payment-card and third-party-network transactions processed on your behalf. Some platforms issue one, some issue the other, some issue both. The income still gets reported on Schedule C either way. One thing to watch: starting in 2026 the 1099-NEC threshold rises to $2,000 and the 1099-K threshold returns to $20,000 and 200 transactions, so a part-time driver earning a smaller amount might not receive any form at all. The income is still reportable.

Does state tax work the same way?

Mostly the same on the income side — most states tax the same Schedule C net profit, just on a separate state return. The wrinkles are local. New York City charges Unincorporated Business Tax on some self-employed residents. California has a state-level minimum tax that hits LLCs. A handful of states have no income tax at all. Check your state’s department of revenue or a local preparer before assuming the federal numbers carry straight over.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.