The Pastor Who Thought He Owed Tax — and Got $8,500 Back Instead

A small church-plant pastor’s family of four earned about $36,000 last year. They didn’t owe a dollar of federal income tax. The IRS sent them a refund check for nearly $8,500. Here’s how the Earned Income Credit makes that math work.

Key Takeaways

- The Earned Income Credit (EIC) rewards work — for low- and moderate-income families, earning more (up to a point) means a bigger credit, not a smaller one.

- A married couple filing jointly with two qualifying children can receive up to $7,316 in EIC for 2026.

- EIC is fully refundable. If your tax liability is zero, you still get the credit as a cash refund.

- EIC and the Child Tax Credit stack — combined, a low-income family of four can take home $9,000+ in refundable credits.

- Every person on the return — taxpayer, spouse, and each qualifying child — must have a valid SSN. ITINs do not qualify for EIC, and after OBBBA, ITIN parents no longer qualify for CTC either.

- You must file a return to claim it. No filing, no credit — even if you owe nothing.

Table of Contents

- 1. Meet David and Rachel

- 2. The Rule: What the EIC Actually Does

- 3. How the EIC Phase-In and Phase-Out Work

- 4. Running the Numbers on David’s Return

- 5. Who Qualifies for the EIC

- 6. Mistakes That Cost Families Thousands

- 7. What to Check Right Now

- 8. EA Insight

- 9. Frequently Asked Questions

- 10. Related Articles

- 11. Official Resources

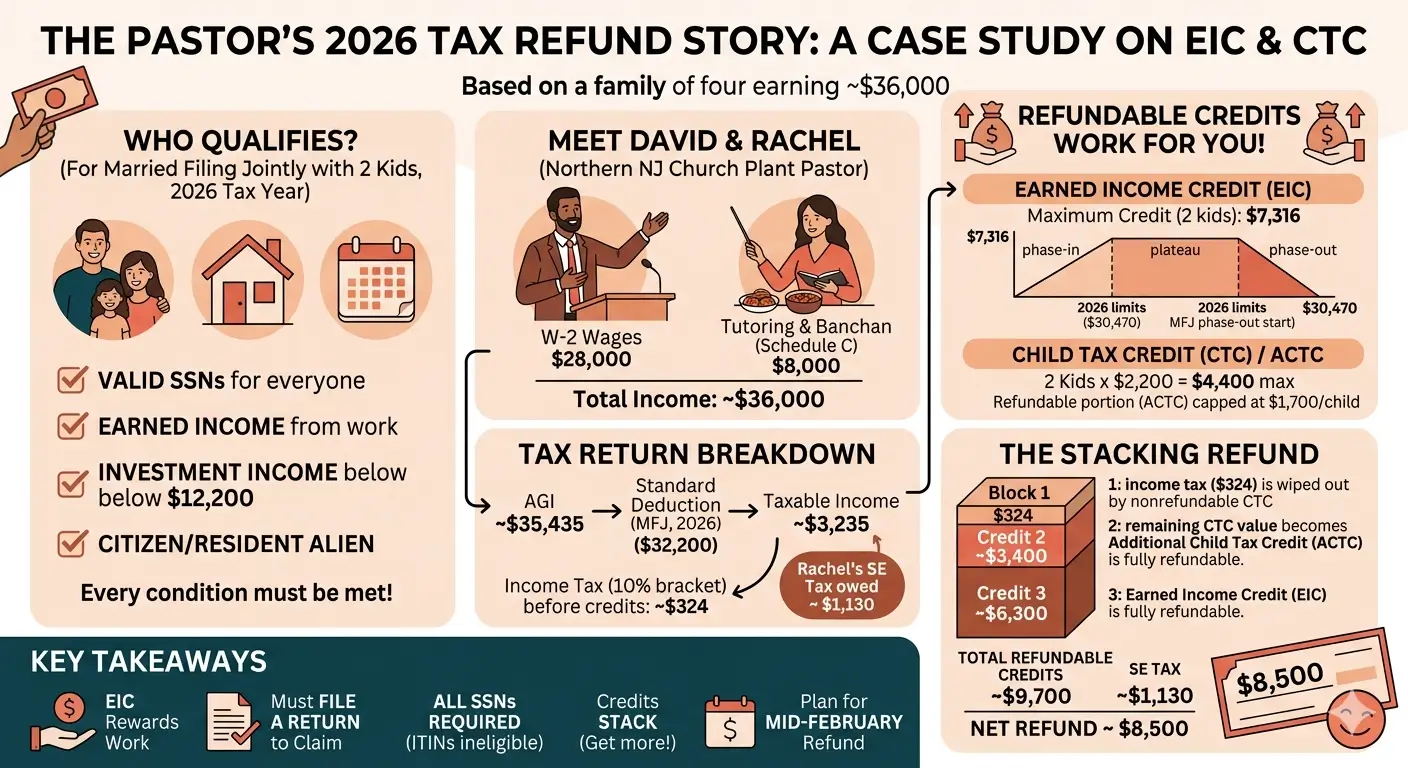

1. Meet David and Rachel

David pastors a small church plant in northern New Jersey. The congregation is young, the building is rented, and the salary line in the church budget is whatever’s left after rent and utilities. His W-2 last year showed Box 1 wages of $28,000.

His wife Rachel keeps things running at home with their two elementary-aged kids. She also tutors Korean to a handful of neighborhood students after school and sells homemade banchan to families at the church. The tutoring and banchan together brought in about $8,000 of net income for the year. No 1099s. No W-2. Just cash and Venmo.

Everyone in the family — David, Rachel, and both kids — has a valid Social Security number.

That sentence comes up in my office almost every season — usually from a pastor, a part-time worker, or a family with one income. The instinct sounds reasonable. It’s also expensive. David’s family didn’t owe the IRS a dollar of federal income tax. The IRS owed them close to $8,500.

2. The Rule: What the EIC Actually Does

The Earned Income Credit (also called EITC) is a federal tax credit for working people whose earnings fall below certain limits. It has been part of the tax code since 1975 and is one of the largest anti-poverty programs in the country. For 2026, qualifying families with two children can receive up to $7,316.

Bottom line

The EIC is a credit for people who work but don’t earn much. If the credit exceeds the tax you owe, the IRS refunds the difference to you in cash.

Two things make the EIC unusual. First, it is fully refundable. Most credits stop helping you once your tax bill hits zero — anything beyond that is wasted. EIC keeps going. Owe $0 in tax and qualify for $6,000 in EIC? You get a $6,000 check.

Second, the credit is built on earned income. The more you work — up to a certain point — the larger the credit grows. It’s structured to reward employment, not just to subsidize low income. That’s why investment income, retirement distributions, unemployment, and gifts don’t count toward earned income for EIC purposes.

3. How the EIC Phase-In and Phase-Out Work

The EIC has three zones, and understanding them is the difference between guessing your refund and knowing it.

Phase-in zone. Starting from the first dollar of earned income, the credit grows as you earn more. For a married couple with two kids, the phase-in rate is 40 cents on every dollar earned. So $10,000 of earned income generates roughly $4,000 in EIC, not $7,316.

Plateau zone. Once earned income reaches a certain threshold, the credit hits its maximum and stays flat. For 2026, a family with two children reaches the $7,316 maximum at about $17,880 of earned income.

Phase-out zone. Past a higher threshold, the credit shrinks. For married couples filing jointly with two children, phase-out begins around $30,470 of earned income (or AGI, whichever is higher) and the credit zeroes out completely at $65,899.

2026 EIC Maximum Credit by Family Size

| Qualifying Children | Max Credit (2026) | MFJ Phase-Out Ends |

|---|---|---|

| None | $664 | $26,820 |

| 1 | $4,427 | $58,863 |

| 2 | $7,316 | $65,899 |

| 3 or more | $8,231 | $70,244 |

Important: The EIC also has a hard ceiling on investment income. For 2026, if your interest, dividends, capital gains, and certain rental income exceed $12,200 in total, you cannot claim the EIC at all — regardless of how low your wages are. This trips up self-employed people and small landlords more often than wage earners.

4. Running the Numbers on David’s Return

Here’s what the return looks like once we work it through.

| Item | Amount |

|---|---|

| David’s W-2 wages (Box 1) | $28,000 |

| Rachel’s Schedule C net profit | $8,000 |

| Less: deductible half of SE tax | ($565) |

| Adjusted Gross Income (AGI) | ~$35,435 |

| Standard deduction (MFJ, 2026) | ($32,200) |

| Taxable income | ~$3,235 |

Step 1 — The income tax bill

Taxable income of about $3,235 falls entirely inside the 10% bracket. Federal income tax before credits: roughly $324.

Step 2 — Self-employment tax (separate from income tax)

Rachel’s $8,000 of self-employment net profit triggers SE tax: about $1,130. Half of that is already deducted above the line in computing AGI. SE tax is paid alongside income tax on the return — it doesn’t get wiped out by credits the way income tax does.

Step 3 — The credits stack up

| Credit | Amount | Refundable? |

|---|---|---|

| Child Tax Credit (2 kids × $2,200) | $4,400 max | Mostly no — limited by tax |

| Additional CTC (refundable portion) | ~$3,400 | Yes — capped at $1,700/child |

| Earned Income Credit (2 kids, MFJ) | ~$6,300 | Fully refundable |

The CTC first wipes out the $324 income tax bill. Most of the remaining $4,400 of CTC value is unused as a nonrefundable credit, but it isn’t lost — it converts into the Additional Child Tax Credit (ACTC). ACTC equals 15% of earned income above $2,500, capped at $1,700 per qualifying child. For David and Rachel: (35,435 − 2,500) × 15% = $4,940, capped at 2 × $1,700 = $3,400.

On top of that, EIC at an earned income of about $35,435 for a MFJ couple with two kids works out to roughly $6,300 — phase-out has started, but the credit is still substantial.

Step 4 — The bottom line

Estimated Refund Summary

Income tax owed: $324 → wiped out by CTC

SE tax owed: ~$1,130

ACTC refundable: ~$3,400

EIC refundable: ~$6,300

Net refund: roughly $8,500 ($9,700 in credits minus $1,130 SE tax, plus a small adjustment)

That’s nearly a quarter of David’s W-2 income, returned to the family in a single check. And every dollar of it was at risk if they had simply skipped filing.

5. Who Qualifies for the EIC

Every condition below has to be met. Missing one disqualifies the credit entirely.

| Requirement | Detail |

|---|---|

| Earned income | At least $1 of wages or net self-employment income |

| Valid SSN | Taxpayer, spouse, and every qualifying child must have one. ITINs do not qualify. |

| Filing status | MFJ, Single, HOH, or Qualifying Surviving Spouse — never MFS |

| Citizenship/residency | U.S. citizen or resident alien for the entire year |

| Investment income cap | $12,200 or less for 2026 |

| No Form 2555 | Claiming the foreign earned income exclusion disqualifies you |

| Qualifying child rules | Under 19 (24 if full-time student), lived with you more than half the year, relationship test |

SSN rules — easy to confuse: The EIC has always required valid SSNs for the taxpayer, spouse, and each qualifying child. The Child Tax Credit used to be more lenient — a parent with an ITIN could still claim CTC if the child had an SSN. The One Big Beautiful Bill Act changed that. Beginning with 2025 returns, the CTC also requires the taxpayer (and spouse, if married) to have a valid SSN. If anyone on the return is ITIN-only, both EIC and CTC are off the table.

6. Mistakes That Cost Families Thousands

“Our income is too low to bother filing”

The single most expensive mistake. The EIC and ACTC are claimed through filing. Skip the return and you skip the refund — and you may not even know what you walked away from. David’s family would have lost $8,500 by not filing.

Leaving self-employment income off the return

Rachel’s tutoring and banchan income belongs on Schedule C. Leaving it off causes two problems. The earned income figure used for EIC drops, shrinking the credit. And if the IRS later identifies the unreported income, the entire EIC can be clawed back — sometimes with a 2-year or 10-year disallowance penalty on top.

Filing Married Filing Separately

MFS used to disqualify the EIC outright. The rules loosened slightly — separated spouses living apart can sometimes still claim it — but for a couple living together like David and Rachel, MFS still kills the credit. MFJ is almost always the right answer for low-income families.

Practical point

Returns claiming EIC or ACTC are held by law until mid-February under the PATH Act. Even if you e-file in late January, expect refunds around late February or early March. Plan cash flow accordingly — don’t promise a landlord that the refund is coming on February 1.

Missing the three-year window on past returns

Refunds — including EIC and ACTC — must be claimed within three years of the original due date. A 2023 return generating an EIC refund needs to be filed by April 15, 2027. After that, the money belongs to the Treasury permanently.

7. What to Check Right Now

- Confirm everyone on the return — taxpayer, spouse, every claimed child — has a valid SSN.

- Add up all earned income for the year, including cash side work and self-employment.

- If filing status is MFS, look at whether MFJ is possible. EIC is unavailable to most MFS filers.

- Check that any claimed child lived with you in the U.S. more than half the year.

- Add up investment income — interest, dividends, capital gains, certain rental income — and make sure it’s at or below $12,200.

- If self-employment income exists, get receipts and mileage records together for Schedule C.

- Look back at the last three years. If a return wasn’t filed in a year you might have qualified, check whether the three-year window is still open.

- Plan around mid-February — don’t expect EIC/ACTC refunds before then.

EA Insight

A few years ago a family came to me — pastor, stay-at-home mom, three kids — who hadn’t filed in four years. The husband was convinced he owed the IRS money and was scared to file. We pulled wage and income transcripts, reconstructed the returns, and filed three back years inside the three-year refund window. The combined EIC and ACTC refunds came to just over $24,000. The fourth year was past the window. That money was gone — permanently — because no return had ever been filed for it.

The pattern repeats. Low-income families who most need the credit are the ones least likely to claim it, because the conventional wisdom says “if you don’t owe, you don’t file.” For working families with kids and SSNs, that wisdom is exactly backward.

A second pattern: cash-side income. A spouse who tutors, cleans houses, sells food, or drives part-time hands me a year-end summary that’s missing thousands of dollars they “didn’t think counted.” It always counts. And reporting it usually increases the refund through EIC, not decreases it. Underreporting is the worst of both worlds — it shrinks the legitimate credit and creates audit exposure.

A third pattern, newer: the OBBBA SSN rules on CTC catching people off guard. Mixed-status families who have been claiming CTC every year on the strength of their kids’ SSNs are now seeing the credit disappear because the parent files with an ITIN. If anyone in the household has been weighing whether to pursue work authorization and an SSN, the math just changed — significantly.

EA Summary

A working family of four earning $36,000 with two kids and valid SSNs across the household is sitting on roughly $8,500 in refundable federal credits — every year. Claiming it requires three things: filing the return, reporting all earned income (including cash side work), and confirming that everyone listed has a valid SSN. Skip any one of them and the credit shrinks or disappears. Low income isn’t a reason to skip filing. For families like David’s, it’s the reason to file.

Frequently Asked Questions

What counts as “earned income” for the EIC?

Earned income includes wages, salaries, tips, and net self-employment income (gross receipts minus business expenses, before SE tax). It does not include unemployment compensation, Social Security or SSDI benefits, retirement plan distributions, pension income, alimony, child support, interest, dividends, or capital gains. Even if a family’s bank account looks comfortable from a pension, only the earned portion drives the EIC calculation.

My spouse has an ITIN, not an SSN. Can we still get the EIC?

No. On a joint return, both spouses must have valid SSNs. The same rule applies to each child claimed for the EIC. After OBBBA, this also applies to the Child Tax Credit — a parent’s ITIN now blocks both credits.

Can I claim the EIC and the Child Tax Credit in the same year?

Yes. They’re separate credits with different rules and different calculations. Most low- and moderate-income working families with children qualify for both, and the credits stack.

Does cash income from tutoring or selling food count?

Yes. Net earnings from self-employment — gross receipts minus business expenses — count as earned income. Report it on Schedule C even if no 1099 was issued. You’ll also owe self-employment tax on it, but that’s separate from the EIC calculation.

Are pastors taxed differently?

In some ways, yes. Ministers have a dual tax status — treated as employees for income tax (often W-2) but as self-employed for Social Security and Medicare (paid via SE tax, not FICA). Housing allowance has its own rules. This article uses a simplified W-2 setup; minister-specific tax issues are covered in a separate post.

When can I expect my refund if I claim the EIC?

Federal law (the PATH Act) bars the IRS from issuing EIC or ACTC refunds before mid-February, regardless of how early the return is filed. For 2026 returns, early e-filers with direct deposit typically see refunds posted in late February or early March.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. The case described is based on a composite of real practice scenarios with all identifying details changed. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.