What Is a W-4? Employee’s Withholding Certificate Explained

Form W-4 tells your employer how much federal income tax to withhold from your paycheck. Fill it out correctly, and you can avoid a surprise tax bill in April — or stop giving the government an interest-free loan all year.

Key Takeaways

- Form W-4 is the Employee’s Withholding Certificate — you give it to your employer, not the IRS.

- The form uses a five-step structure. Only Steps 1 and 5 are required; Steps 2 through 4 apply only when specific situations exist.

- Since the 2020 redesign, withholding allowances no longer exist. The current system calculates withholding based on income, dependents, and deductions.

- The 2026 W-4 reflects changes from the One Big Beautiful Bill Act (OBBBA): the Child Tax Credit rises to $2,200 per child, and a new expanded Deductions Worksheet covers qualified tips, overtime, and auto loan interest.

- If you leave Steps 2 through 4 blank, your employer withholds based on the standard deduction for your filing status.

- You should update your W-4 whenever a major life event occurs — marriage, divorce, a new child, a second job, or a significant income change.

Table of Contents

1. What Is Form W-4?

IRS Form W-4, officially titled Employee’s Withholding Certificate, is a document you complete and give to your employer so they can withhold the correct amount of federal income tax from each paycheck.

An important distinction: the W-4 does not determine how much tax you owe. Your total tax liability is calculated when you file your return. What the W-4 controls is timing — how much of that tax is taken out of your pay throughout the year.

If your employer withholds too little, you may owe a balance (and possibly an underpayment penalty) when you file. If they withhold too much, you get a refund — but that means you had less money available in every paycheck. In effect, you gave the government an interest-free loan.

The goal is to get as close to break-even as possible: owe nothing, receive little to no refund, and keep your cash flow steady all year.

2. Who Needs to Fill Out a W-4?

Every employee must complete a W-4 when starting a new job. Your employer uses the information on the form to run payroll withholding calculations for federal income tax.

If you are already employed and have a W-4 on file, you do not need to submit a new one every year. Your current form stays in effect until you choose to update it. However, if your financial or personal situation has changed, submitting an updated W-4 can prevent over- or under-withholding.

Freelancers, independent contractors, and self-employed individuals do not use Form W-4. They submit Form W-9 to their clients and pay federal income tax through quarterly estimated tax payments (Form 1040-ES) instead.

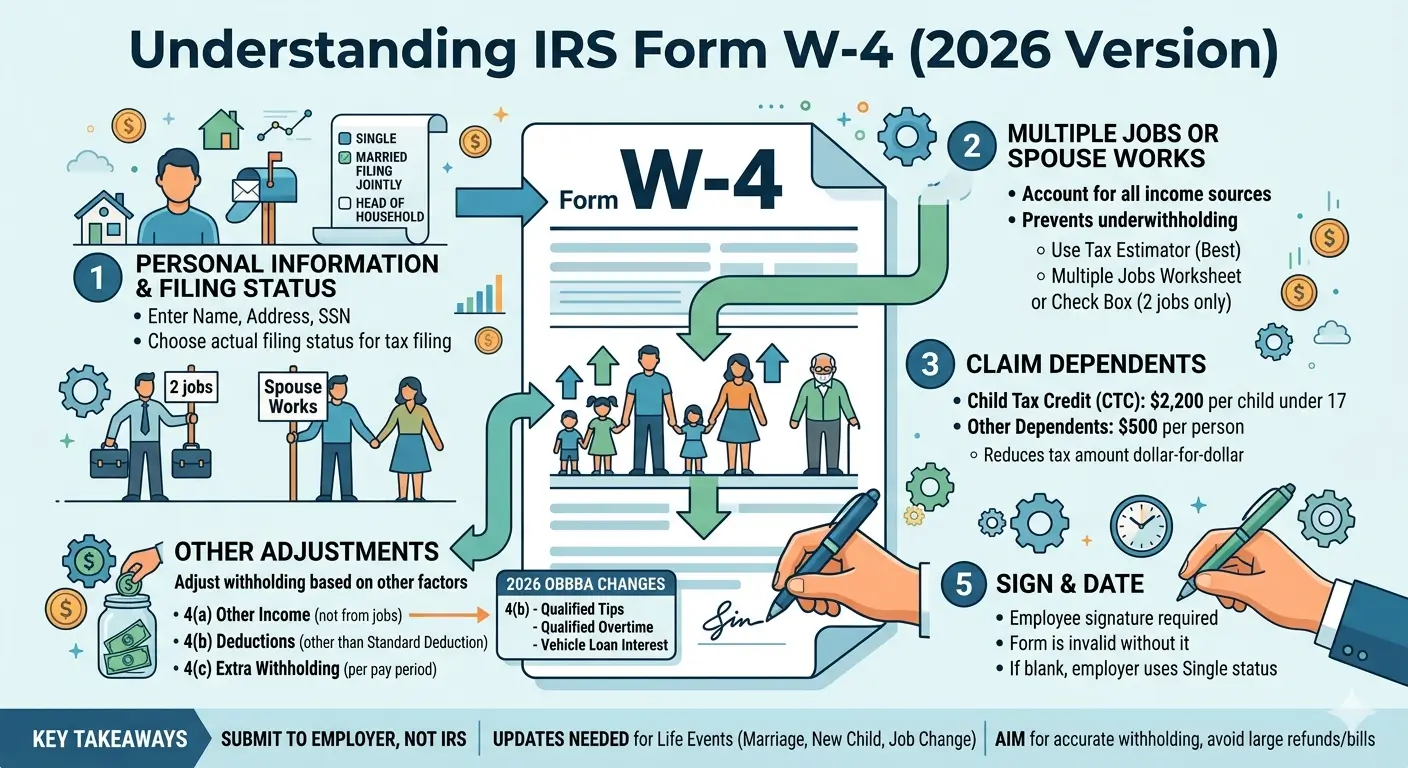

3. The Five Steps of Form W-4

The current W-4 is organized into five steps. The IRS only requires Steps 1 and 5. Steps 2 through 4 are completed only when they apply to your situation.

Step 1 — Personal Information (Required)

Enter your name, address, Social Security number, and filing status. You can choose from Single, Married Filing Jointly, Married Filing Separately, or Head of Household. Select the same filing status you plan to use on your tax return — this determines the standard deduction and tax rate tables your employer applies to your withholding.

Step 2 — Multiple Jobs or Spouse Works

Complete this step only if you hold more than one job at the same time, or if you are married filing jointly and your spouse also works. The IRS provides three options:

Option (a) — Use the IRS Tax Withholding Estimator at irs.gov/W4App. This is the most accurate method and keeps your details private from your employer.

Option (b) — Complete the Multiple Jobs Worksheet on page 3 of the form. This is accurate but requires manual calculation.

Option (c) — Check the box if there are only two jobs total (yours and your spouse’s, or two of your own). This is the simplest option but assumes both jobs pay similar wages, so it may be less precise.

When you have multiple jobs, complete Steps 3 and 4 on the W-4 for the highest-paying job only. Leave those steps blank on the W-4 for the other job(s).

Caution: Skipping Step 2 is one of the most common W-4 mistakes. If both spouses work and neither accounts for the other’s income, each employer withholds as if that paycheck is the household’s only income. The result is significant under-withholding — and a tax bill in April.

Step 3 — Claim Dependents

This step reduces your withholding based on tax credits you expect to claim.

Line 3(a): Multiply the number of qualifying children under age 17 by $2,200 (the Child Tax Credit amount for the current tax year).

Line 3(b): Multiply the number of other dependents by $500.

Add Lines 3(a) and 3(b) together and enter the total. This amount directly reduces the federal income tax withheld from each paycheck, resulting in higher take-home pay.

Income limits apply: the full credit is available for single filers with income up to $200,000 and married filing jointly filers up to $400,000. Beyond those thresholds, the credit begins to phase out.

Step 4 — Other Adjustments

Line 4(a) — Other income: If you expect income this year that will not have tax withheld — such as interest, dividends, or retirement distributions — enter the estimated amount here. This increases withholding from your paycheck to cover the additional income.

Line 4(b) — Deductions: If you plan to claim deductions beyond the standard deduction (such as itemized deductions or new deductions under the OBBBA), use the Deductions Worksheet on page 4 to calculate the amount and enter it here. If you skip this line, your employer withholds based on the standard deduction for your filing status.

| Filing Status | Standard Deduction |

|---|---|

| Single / Married Filing Separately | $16,100 |

| Married Filing Jointly | $32,200 |

| Head of Household | $24,150 |

Line 4(c) — Extra withholding: Enter any additional dollar amount you want withheld from each pay period. This is useful if you consistently owe tax at filing time and want to increase withholding to avoid that.

Step 5 — Sign and Date (Required)

Your signature is required for the form to be valid. If you submit a W-4 without signing it, your employer must disregard it and calculate withholding as if you are Single with no other entries — which typically results in the highest withholding rate.

4. What Changed on the 2026 W-4?

The 2026 Form W-4 retains the same five-step structure introduced in 2020 but includes several updates driven by the One Big Beautiful Bill Act (OBBBA). The form has expanded from four pages to five pages (including instructions).

| Item | Previous | 2026 W-4 |

|---|---|---|

| Child Tax Credit (Step 3) | $2,000 per child | $2,200 per child |

| Deductions Worksheet (Step 4b) | Less than half a page | Full page |

| New Deduction Lines | None | Qualified tips, overtime, auto loan interest |

| Exempt Status | Write “Exempt” by hand | Dedicated checkbox + certification |

| Total Pages | 4 | 5 |

The biggest change is in the Deductions Worksheet (linked to Step 4b), which now includes lines for three new OBBBA provisions:

Qualified tips: If your total income is below $150,000 ($300,000 for married filing jointly), you can enter an estimate of qualified tips up to $25,000.

Qualified overtime compensation: Under the same income thresholds, you can enter the “half” portion of time-and-a-half overtime pay, up to $12,500 ($25,000 if married filing jointly).

Passenger vehicle loan interest: Interest paid on a qualifying new auto loan can now be included as a deduction on the worksheet.

These additions allow employees with tip income, overtime pay, or new car loans to reduce over-withholding throughout the year rather than waiting for a refund at filing time.

The form also adds a dedicated checkbox for claiming exempt status, replacing the previous method of writing “Exempt” in the space below Step 4(c). To claim exemption, you must certify that you had no federal income tax liability in the prior year and expect none in the current year.

5. When Should You Update Your W-4?

There is no annual requirement to submit a new W-4. Your current form remains in effect until you replace it. However, certain life events can significantly change your tax situation, making an update worthwhile:

Marriage or divorce — Your filing status changes, which affects standard deduction amounts and tax rate brackets.

Birth or adoption of a child — You may qualify for the Child Tax Credit, reducing your tax liability.

Starting a second job or side income — Additional income without adjusted withholding often leads to under-withholding.

Spouse starts or stops working — Household income changes affect the correct withholding level.

Major income change — A promotion, bonus, or job loss can shift you into a different tax bracket.

Buying a home — Mortgage interest may increase your deductions, potentially lowering the withholding you need.

Last year’s result was off — If you received a very large refund or owed a significant amount, your current W-4 likely needs adjustment.

The IRS provides a free Tax Withholding Estimator at irs.gov/W4App. It walks you through your income, deductions, and credits, then generates a recommended W-4 configuration. Using it once a year takes about 15 to 25 minutes and can meaningfully improve the accuracy of your withholding.

6. W-4 vs. W-2: What’s the Difference?

These two forms are closely related but serve very different purposes. The W-4 is an input — it sets the rules for withholding. The W-2 is an output — it reports what actually happened during the year.

| Form W-4 | Form W-2 | |

|---|---|---|

| Who completes it? | Employee | Employer |

| When? | At hire (+ updates as needed) | After year-end (by January 31) |

| Purpose | Set withholding amount | Report wages and taxes withheld |

| Submitted to | Employer only | Employee + IRS + SSA |

7. Common Mistakes to Avoid

Skipping Step 2 when both spouses work. This is the single most common cause of under-withholding for married couples. Without Step 2, each employer withholds as though the employee’s paycheck is the only household income.

Choosing the wrong filing status. The filing status on your W-4 should match the one you plan to use on your tax return. Selecting a different status creates a mismatch between withholding and actual tax liability.

Not updating after a life change. A W-4 from five years ago may no longer reflect your current income, deductions, or family situation. Even small changes can add up over 12 months of paychecks.

Claiming exempt incorrectly. You can only claim exemption from withholding if you had zero federal income tax liability last year and expect zero this year. If that is not your situation and you check the exempt box, you will owe the full year’s tax plus potential penalties when you file.

Sending the W-4 to the IRS. Form W-4 goes to your employer — not to the IRS. Your employer keeps it on file and uses it for payroll calculations.

EA Insight

Most people fill out their W-4 on their first day at a new job, rushing through it while completing a stack of HR paperwork. They check Step 1, sign Step 5, and never look at it again. For a single person with one job and no dependents, that actually works fine — the default withholding is reasonably accurate.

But the moment your situation gets more complex — a working spouse, a second job, children, or side income — the default settings are almost certainly wrong. The most frequent problem I see is dual-income couples who skip Step 2. Each employer withholds tax as if their paycheck is the only income in the household. The combined under-withholding often results in an unexpected tax bill of $2,000 to $5,000 in April.

Starting this year, the expanded Deductions Worksheet also matters for workers who earn tips or overtime. If you qualify for these new deductions, filling out the worksheet tells your employer to withhold less — putting that money in your paycheck now instead of making you wait for a refund. The IRS Tax Withholding Estimator at irs.gov/W4App is the most reliable way to get your W-4 right. It takes about 15 minutes once a year, and that small investment of time directly affects every paycheck you receive.

Frequently Asked Questions

What happens if I don’t submit a W-4?

Your employer is required to withhold federal income tax as if you are Single with no other adjustments. If you have a family, dependents, or deductions, this default will almost certainly result in more tax being withheld than necessary.

Do I need to file a new W-4 every year?

No. Your existing W-4 remains in effect until you submit a replacement. However, if your income, filing status, or family situation has changed, reviewing and updating your W-4 annually can help keep your withholding accurate.

Do freelancers fill out a W-4?

No. Form W-4 is for employees who receive wages from an employer. Freelancers and independent contractors submit Form W-9 to their clients and pay federal income tax through quarterly estimated payments using Form 1040-ES.

Does checking “Exempt” mean I don’t owe any tax?

No. Claiming exempt means no federal income tax is withheld from your paychecks — it does not eliminate your tax obligation. You qualify only if you had zero federal income tax liability last year and expect zero this year. If you claim exempt incorrectly, you will owe the full amount of tax when you file, plus potential penalties and interest.

What happened to withholding allowances?

Withholding allowances were eliminated from Form W-4 starting in 2020. The change was prompted by the Tax Cuts and Jobs Act (TCJA) of 2017, which suspended personal exemptions. The current form uses a five-step structure based on income, dependents, and deductions instead of the old allowance system.

Can my employer tell me how to fill out my W-4?

Your employer can answer general questions about the form, but they cannot fill it out for you or advise you on what specific entries to make. For personalized guidance, use the IRS Tax Withholding Estimator or consult a tax professional.

Related Articles

Official Resources

Disclaimer

This article provides general information about IRS Form W-4 based on federal tax rules. It is not tax advice. Individual circumstances vary, and tax laws may change. For guidance specific to your situation, consult a qualified tax professional such as an Enrolled Agent (EA) or CPA. Standard deduction amounts and credit figures referenced in this article are based on current IRS guidance and may be updated in future years.