What Is the Standard Deduction?

The standard deduction is a flat dollar amount the IRS lets you subtract from your adjusted gross income — no receipts, no itemizing required. It reduces your taxable income, which lowers your federal tax bill.

Key Takeaways

- The standard deduction is a fixed amount subtracted from your AGI — no documentation needed.

- The amount varies by filing status: Single, MFJ, Head of Household, and MFS each have different amounts.

- Taxpayers age 65 or older (or legally blind) qualify for an additional deduction on top of the base amount.

- You cannot take both the standard deduction and itemize — you choose one each year.

- About 90% of U.S. taxpayers use the standard deduction (Tax Policy Center estimate).

Table of Contents

- 1. What Is the Standard Deduction?

- 2. Standard Deduction Amounts by Filing Status

- 3. Additional Deduction: Age 65+ and Legally Blind Filers

- 4. How It Works on Your Tax Return

- 5. Standard Deduction vs. Itemizing: How to Decide

- 6. Who Cannot Take the Standard Deduction

- 7. EA Insight

- 8. People Also Ask

1. What Is the Standard Deduction?

When you file a federal income tax return, the IRS lets you reduce your taxable income through deductions. The standard deduction is the simplest option: a fixed dollar amount you subtract from your adjusted gross income (AGI), regardless of your actual expenses during the year.

Think of it as the IRS acknowledging that everyone has a baseline level of personal living costs — so it allows you to shield that portion of your income from federal tax. You don’t need to prove anything, track receipts, or report individual expenses. You simply claim the flat amount that corresponds to your filing status.

The opposite approach — itemizing deductions — lets you deduct specific expenses like mortgage interest, charitable donations, and state taxes paid. But itemizing requires detailed records and only saves you more money if your actual qualifying expenses exceed the standard deduction amount.

Standard Deduction — Quick Definition

A flat dollar amount the IRS lets you subtract from your AGI before calculating federal income tax.

It reduces your taxable income — not your tax bill dollar-for-dollar.

2. Standard Deduction Amounts by Filing Status

The IRS adjusts the standard deduction each year for inflation. The amounts below reflect the current tax year figures, as announced in IRS Revenue Procedure 2025-32. Always verify the latest numbers at IRS.gov before filing.

| Filing Status | Standard Deduction | Typically Used By |

|---|---|---|

| Single | $16,100 | Unmarried, no dependents |

| Married Filing Jointly (MFJ) | $32,200 | Married couples, one joint return |

| Married Filing Separately (MFS) | $16,100 | Married, separate returns |

| Head of Household (HoH) | $24,150 | Unmarried, supporting a qualifying person |

| Qualifying Surviving Spouse | $32,200 | Widowed within 2 yrs, dependent child |

Source: IRS Revenue Procedure 2025-32 (tax year 2026 inflation adjustments, filed in 2027).

🧮 Quick Deduction Check

Enter your AGI and filing status to see your estimated federal tax savings from the standard deduction.

3. Additional Deduction: Age 65+ and Legally Blind Filers

If you are 65 or older or legally blind, the IRS allows an extra amount on top of your base standard deduction. Each qualifying condition counts separately — so a filer who is both 65 and legally blind receives the additional deduction twice.

| Qualifying Condition | Single / HoH | MFJ (per qualifying spouse) |

|---|---|---|

| Age 65+ or Legally Blind (one condition) | + $2,050 | + $1,650 |

| Age 65+ and Legally Blind (two conditions) | + $4,100 | + $3,300 |

📌 OBBBA Senior Bonus Deduction — Temporary (2025–2028)

The One Big Beautiful Bill Act introduced a separate $6,000 bonus deduction per person for filers age 65 and older — available to both standard deduction takers and itemizers. It phases out based on your modified AGI (MAGI).

| Filing Status | Full $6,000 If MAGI ≤ | Phases Out Above | Gone Completely At |

|---|---|---|---|

| Single / HoH | $75,000 | $75,001 – $174,999 | $175,000 |

| Married Filing Jointly | $150,000 | $150,001 – $349,999 | $350,000 |

Phase-out rate: 6 cents lost per $1 of MAGI above the threshold. Confirm current eligibility and phase-out calculations at IRS.gov or with a tax professional, as implementation guidance may be updated.

4. How It Works on Your Tax Return

The standard deduction is claimed on Form 1040, Line 12. It is subtracted from your AGI to arrive at your taxable income, which appears on Line 15 — the number your actual federal tax is calculated from.

| Line 9 | Total Income |

| Line 11 | Adjusted Gross Income (AGI) |

| Line 12 | Standard Deduction (or itemized, whichever you choose) |

| Line 15 | Taxable Income ← Your tax is calculated here |

Example: Single Filer

| Wages (W-2) | $58,000 |

| AGI | $58,000 |

| Standard Deduction (Single) | − $16,100 |

| Taxable Income | $41,900 |

Federal income tax is calculated on $41,900 — not the original $58,000 earned.

The standard deduction reduces your taxable income, not your tax bill directly. The actual tax savings depend on your marginal tax bracket. For example, a $16,100 deduction in the 22% bracket saves approximately $3,542 in federal taxes — not the full $16,100.

For a deeper look at how taxable income is calculated from start to finish, see our article: What Is Taxable Income?

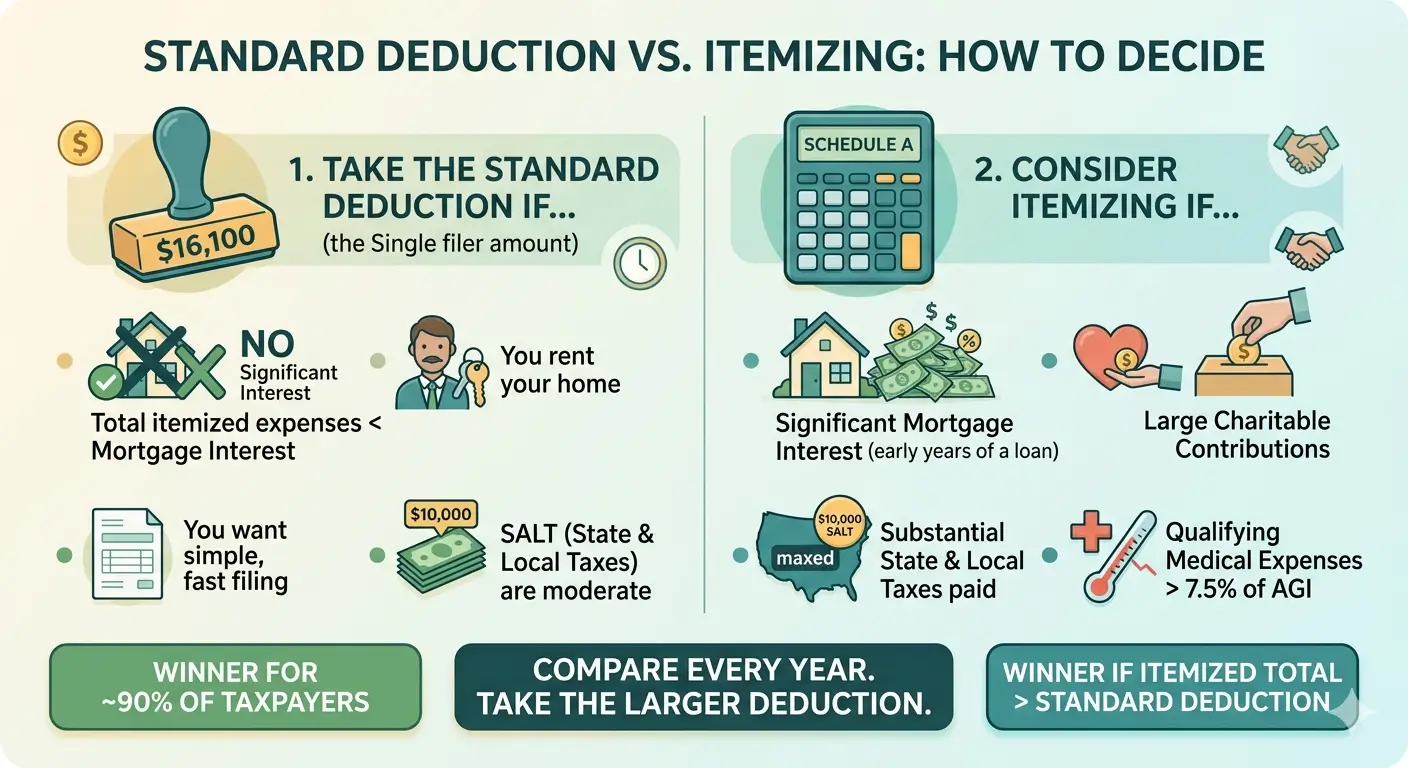

5. Standard Deduction vs. Itemizing: How to Decide

Each year, you choose between the standard deduction and itemizing — and you want to select whichever produces the larger deduction. You cannot combine both methods on the same return.

Take the Standard Deduction If…

- Your total itemized expenses add up to less than your standard deduction amount

- You rent your home and don't have significant mortgage interest to deduct

- You want simpler, faster filing with no need to track individual expenses

- Your state and local taxes (SALT) are moderate — the SALT deduction has a statutory cap, so very high state tax bills may not be fully deductible anyway

Consider Itemizing If…

- You paid significant mortgage interest (especially in the early years of a loan)

- You made large charitable contributions

- You paid substantial state and local taxes — check the current SALT deduction cap, as it has changed under recent legislation

- You had qualifying medical expenses exceeding 7.5% of your AGI

A Simple Check

Add up your mortgage interest (from Form 1098), state and local taxes paid, charitable donations, and qualifying medical expenses. If the total is higher than your standard deduction, itemizing saves you more. Otherwise, the standard deduction wins.

You can switch methods freely from year to year. Reviewing this comparison annually is a sound habit, especially after major life changes like buying or selling a home.

IRS Publication Reference

For a complete list of allowable itemized deductions, refer to IRS Publication 501 (Dependents, Standard Deduction, and Filing Information) and Schedule A (Form 1040).

6. Who Cannot Take the Standard Deduction

Most U.S. taxpayers qualify, but there are specific situations where the standard deduction is not available:

- You are a nonresident alien or a dual-status alien for the year

- You file a return for a period of less than 12 months due to a change in accounting period

- You are married filing separately and your spouse itemizes deductions — in this case, you must also itemize

- You file as an estate, trust, common trust fund, or partnership

Dependents Have a Different Calculation

If someone else can claim you as a dependent, your standard deduction is limited. It equals the greater of $1,350 or your earned income plus $450 — but cannot exceed the regular standard deduction for your filing status. This rule commonly applies to students with part-time income who are still claimed by their parents.

EA Insight

The first thing I check when comparing standard vs. itemized is mortgage interest. Homeowners in the early years of a 30-year loan often have enough interest to push their itemized total above the standard deduction — but only barely. By year ten or twelve, as the interest portion shrinks, the standard deduction almost always wins.

The second thing I look at is SALT. The state and local tax deduction has a statutory cap — and that cap has shifted significantly under recent legislation. Regardless of where the cap sits in a given year, the key question is the same: once your SALT hits the ceiling, itemizing only wins if mortgage interest plus charitable giving push you above the standard deduction threshold. 📌 Note: The SALT cap has changed under recent tax legislation and may change again. Always verify the current limit at IRS.gov before filing.

One strategy worth knowing: charitable contribution bunching. Instead of donating $5,000 every year, you donate $10,000 in odd years and nothing in even years. In the donation year, your itemized total may clear the standard deduction threshold — so you itemize and get the full deduction. In the off year, you take the standard deduction. Over a two-year cycle, you often come out ahead versus donating the same amount annually.

My rule of thumb: if your itemized deductions come within $2,000 of the standard deduction, take the standard. The time saved on recordkeeping is worth more than the marginal difference — and if you're ever audited, a return without Schedule A is far simpler to defend.

People Also Ask

Does the standard deduction reduce my tax bill dollar-for-dollar?

No. It reduces your taxable income, not your tax owed directly. The actual savings depend on your marginal tax bracket. In the 22% bracket, for example, a $16,100 deduction saves roughly $3,542 in federal taxes — not the full $16,100.

Can I take the standard deduction if I'm self-employed?

Yes. Self-employment business expenses are deducted on Schedule C before your AGI is calculated — they don't compete with the standard deduction. You can still claim the standard deduction on top of your Schedule C deductions.

Can married couples filing separately each take the standard deduction?

Only if both spouses use the same method. If one spouse itemizes, the other must also itemize — even if their itemized deductions are very small. This is one of the key disadvantages of the Married Filing Separately status.

Does taking the standard deduction affect my state taxes?

It can — and the answer varies by state. Some states require you to use the same method as your federal return; others let you choose independently. A few have their own standard deduction amounts, and some don't offer one at all. Always check your specific state's rules.

What is New York State's standard deduction?

New York State has its own standard deduction, which is separate from the federal amount and generally much lower. For example, for a single filer, the NY standard deduction is $8,000, and for married filing jointly it is $16,050. Because the NYS amounts are significantly below the federal figures, many New York residents who take the federal standard deduction still find it worthwhile to review itemizing at the state level — especially those with high property taxes or mortgage interest. Always check the NYS Department of Taxation and Finance for current state amounts.

Will the standard deduction keep increasing every year?

The IRS adjusts it annually using the Chained Consumer Price Index (C-CPI-U). It has increased consistently in recent years, though a decrease is technically possible in a deflationary environment. Current-year amounts are typically announced each fall. Check IRS.gov for the latest figures.

Related Articles

Official Resources

Updated: April 2026

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual situations vary. Always verify current figures at IRS.gov and consult a qualified tax professional (EA, CPA, or attorney) for advice specific to your situation.