What Is the Kiddie Tax?

The kiddie tax is not a separate tax. It is a set of rules that applies the parent’s marginal tax rate to a child’s unearned income above a certain threshold. The IRS introduced these rules to prevent families from shifting investment income into a child’s name to take advantage of lower tax brackets.

Key Takeaways

- The kiddie tax applies to a child’s unearned income — interest, dividends, capital gains, and other investment income. Earned income such as wages and salaries is not subject to the kiddie tax.

- For the 2026 tax year, the first $1,350 of unearned income is tax-free, the next $1,350 is taxed at the child’s rate, and anything above $2,700 is taxed at the parent’s marginal rate.

- It applies to children under 18, children who are 18 with earned income below half of their support, and full-time students aged 19 to 23 with earned income below half of their support.

- Investment income in custodial accounts such as UGMA and UTMA is the most common source of kiddie tax exposure.

- Income inside a 529 Plan is not subject to the kiddie tax when used for qualified education expenses.

Table of Contents

- 1. What Is the Kiddie Tax?

- 2. Why Was This Rule Created?

- 3. Who Does It Apply To?

- 4. How It Works: The Three-Tier Structure

- 5. How to File: Form 8615 vs. Form 8814

- 6. Income Not Subject to the Kiddie Tax

- 7. Trump Account and the Kiddie Tax

- 8. EA Insight

- 9. Frequently Asked Questions

- 10. Related Articles

- 11. Official Resources

1. What Is the Kiddie Tax?

The kiddie tax is not a separate category of tax. It is a set of rules under Internal Revenue Code §1(g) that taxes a portion of a child’s unearned income at the parent’s marginal tax rate instead of the child’s own lower rate.

Unearned income refers to income that does not come from work. This includes interest, dividends, capital gains, rental income, and royalties. If a child receives this type of income above a certain threshold, the excess is taxed as though the parent earned it.

Without this rule, a parent could transfer high-yield investments into a child’s name and have the resulting income taxed at the child’s 10% bracket. The kiddie tax effectively eliminates that advantage.

2. Why Was This Rule Created?

The kiddie tax was introduced in 1986 as part of the Tax Reform Act. At that time, high-income families were increasingly transferring investment assets into their children’s names to take advantage of lower tax brackets. Congress created the kiddie tax to limit this income-shifting strategy.

Since its introduction, the rule has been amended several times. The age threshold has been expanded, and the method for calculating the tax has changed. Under the current rules, unearned income above the threshold is taxed at the parent’s marginal rate — not at a flat trust rate or the child’s own rate.

3. Who Does It Apply To?

The kiddie tax applies when all of the following conditions are met:

Age requirement (one of the following):

- The child was under age 18 at the end of the tax year.

- The child was age 18 at the end of the tax year and did not have earned income that exceeded half of the child’s support.

- The child was a full-time student aged 19 to 23 at the end of the tax year and did not have earned income that exceeded half of the child’s support.

Income requirement:

- The child’s unearned income exceeded $2,700 for the 2026 tax year.

Other requirements:

- At least one of the child’s parents was alive at the end of the tax year.

- The child is required to file a tax return.

- The child does not file a joint return for the tax year.

Exception: If the child’s earned income exceeds half of their own support, the kiddie tax does not apply — even if the child is under 24 and a full-time student. For example, a 22-year-old college student who earned enough through an internship and part-time work to cover more than half of their living expenses would not be subject to the kiddie tax, regardless of how much unearned income they received.

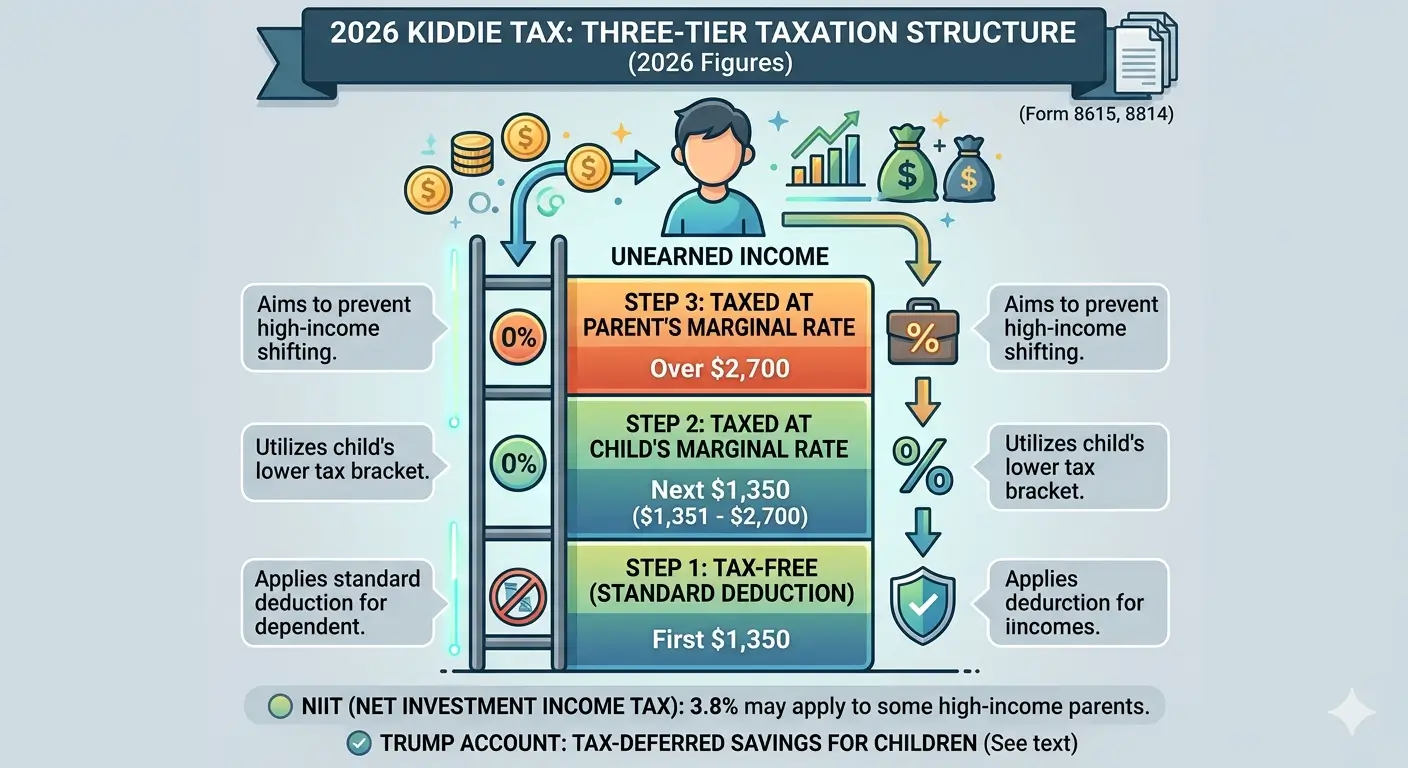

4. How It Works: The Three-Tier Structure

For the 2026 tax year, the kiddie tax divides a child’s unearned income into three tiers:

| Tier | Amount (2026) | How It Is Taxed |

|---|---|---|

| Tier 1 | First $1,350 | Tax-free (standard deduction for dependents) |

| Tier 2 | Next $1,350 ($1,351–$2,700) | Taxed at the child’s marginal rate |

| Tier 3 | Above $2,700 | Taxed at the parent’s marginal rate |

Source: IRS Rev. Proc. 2025-32, IRC §1(g)

Calculation Example

A 15-year-old has $5,000 in dividends and long-term capital gains from a UGMA account. The child has no other income. The parent’s marginal tax rate is 24%.

| Portion | Amount | Rate Applied | Tax |

|---|---|---|---|

| First $1,350 | $1,350 | 0% (standard deduction) | $0 |

| Next $1,350 | $1,350 | Child’s rate (10%) | $135 |

| Above $2,700 | $2,300 | Parent’s rate (24%) | $552 |

Total tax on $5,000 of unearned income: $687. If the same $5,000 had been earned in the parent’s own account and taxed entirely at 24%, the tax would be $1,200. The kiddie tax reduces the bill compared to the parent’s full rate, but it is far more than the child’s 10% rate alone would produce.

Note: The example above is simplified for clarity. If the child’s income consists of qualified dividends or long-term capital gains, the preferential capital gains rates (0%, 15%, or 20%) may apply instead of ordinary income rates. The actual rate is recalculated based on the parent’s tax bracket for that type of income, so the tax result can vary significantly depending on the composition of the child’s unearned income.

High-income families: If the parent’s modified adjusted gross income (MAGI) exceeds $250,000 (married filing jointly) or $200,000 (single), the child’s net investment income may also be subject to the 3.8% Net Investment Income Tax (NIIT) under IRC §1411.

5. How to File: Form 8615 vs. Form 8814

There are two ways to report the kiddie tax:

Option 1: Child Files Their Own Return — Form 8615

If the child’s unearned income exceeds $2,700, the child must file their own Form 1040 with Form 8615 attached. Form 8615 calculates the tax on the child’s unearned income using the parent’s marginal tax rate.

To complete Form 8615, the child’s return must include the parent’s name, Social Security Number, and filing status.

Option 2: Parent Includes the Child’s Income — Form 8814

If all of the following conditions are met, the parent may elect to include the child’s investment income on their own return using Form 8814:

- The child’s income consists only of interest, dividends, and capital gain distributions.

- The child’s gross income is less than $13,500 (2026).

- The child is under age 19 (or under age 24 if a full-time student).

- No estimated tax payments were made under the child’s name, and no federal income tax was withheld from the child’s income.

This option simplifies the filing process but may increase the parent’s overall tax liability.

| Feature | Form 8615 | Form 8814 |

|---|---|---|

| Who Files | Child files their own return | Parent includes on their return |

| Income Type Restriction | None | Interest, dividends, and capital gain distributions only |

| Gross Income Limit | None | Less than $13,500 |

| Advantage | More accurate tax calculation | Simplified filing process |

| Disadvantage | Requires a separate return for the child | May increase parent’s taxable income and affect other credits |

6. Income Not Subject to the Kiddie Tax

The following types of income are not subject to the kiddie tax:

- Earned income — wages, salaries, tips, and self-employment income from work the child performed.

- 529 Plan earnings — investment gains inside a 529 Plan are not taxed when used for qualified education expenses, and they are not subject to the kiddie tax.

- Roth IRA earnings — if the child has earned income and contributes to a Roth IRA, investment growth inside the account is not taxed until withdrawal.

- Tax-exempt interest — interest from municipal bonds and other tax-exempt sources.

Key point: The same $5,000 in investment returns could be fully subject to the kiddie tax if it came from a UGMA account — or completely tax-free if it grew inside a 529 Plan and was used for qualified education expenses. The account structure matters as much as the amount.

7. Trump Account and the Kiddie Tax

The Trump Account (IRC §530A), created under the One Big Beautiful Bill Act (OBBBA) signed in July 2025, is a new tax-deferred savings account for children under age 18. Contributions begin on July 4, 2026.

One of the most significant advantages of the Trump Account is its tax-deferral structure. In a UGMA or UTMA custodial account, dividends and capital gains generated each year are immediately subject to the kiddie tax. Inside a Trump Account, however, investment growth is not taxed until the funds are withdrawn. This means the annual kiddie tax burden that would otherwise apply to custodial account earnings can be deferred until the child reaches adulthood.

That said, employer pre-tax contributions to a Trump Account may trigger the kiddie tax at the parent’s marginal rate, and future withdrawals will be taxed as ordinary income. Investment options within the account are limited to low-cost mutual funds or ETFs that track a U.S. stock index, and the annual contribution limit is $5,000 for 2026 and 2027.

The Trump Account is a broader topic with its own eligibility rules, contribution mechanics, and distribution tax treatment. A dedicated article covering those details is planned separately.

EA Insight

There are three issues I see most often in practice when it comes to the kiddie tax.

The first is that parents do not realize their child has a filing obligation. Many assume that because the child’s income is small, no return is needed. But a dependent child may be required to file a tax return once unearned income exceeds just $1,350 — not $2,700. The $2,700 threshold is where the parent’s rate kicks in, but the filing obligation starts earlier. This catches families off guard, especially when a grandparent has transferred appreciated stock into a custodial account and a portfolio rebalancing triggers a large capital gain in a single year.

The second is the assumption that Form 8814 is always the better choice. Filing the child’s income on the parent’s return is simpler, but the child’s income is added directly to the parent’s AGI. That higher AGI can push income-limited credits — such as the Child Tax Credit or education credits — into phase-out territory. For families with college-age children, a higher parental AGI can also reduce FAFSA-based financial aid. When the child’s unearned income is well above $2,700, the hidden costs of Form 8814 often outweigh the convenience. Filing a separate return with Form 8615 is more work, but it frequently produces a better overall tax result.

The third is prevention. The most reliable way to avoid the kiddie tax entirely is to keep the child’s unearned income below the threshold. Investing in growth-oriented stocks rather than dividend-heavy holdings, using 529 Plans for education savings, and contributing to a Roth IRA when the child has earned income are all strategies that reduce kiddie tax exposure. Review the child’s total unearned income near year-end and manage it against the $2,700 line — that single habit can prevent surprises at filing time.

Frequently Asked Questions

Is the kiddie tax a separate tax?

No. The kiddie tax is not a separate category of tax. It is a rule that changes how a child’s unearned income above a certain threshold is taxed — by applying the parent’s marginal rate instead of the child’s own rate.

Does the kiddie tax apply to a child’s wages from a job?

No. Earned income — including wages, salaries, tips, and self-employment income — is not subject to the kiddie tax. The kiddie tax applies only to unearned income such as interest, dividends, and capital gains.

Is income inside a 529 Plan subject to the kiddie tax?

No. Investment earnings inside a 529 Plan are not taxed when used for qualified education expenses, and they are not subject to the kiddie tax.

What happens if my child’s unearned income is exactly $2,700?

The parent’s rate applies only to amounts above $2,700. At exactly $2,700, the amount taxed at the parent’s rate is $0. The first $1,350 is tax-free, and the remaining $1,350 is taxed at the child’s own rate.

If the parents are divorced, whose tax rate applies?

The IRS uses the custodial parent’s tax rate. If the custodial parent has remarried, the stepparent’s income may also factor into the rate calculation.

Can the Net Investment Income Tax (NIIT) apply on top of the kiddie tax?

Yes. If the child is required to file Form 8615, their net investment income may also be subject to the 3.8% NIIT. The NIIT thresholds are $250,000 of MAGI for married filing jointly and $200,000 for single filers.

Official Resources

- IRS Topic No. 553 — Tax on a Child’s Investment and Other Unearned Income (Kiddie Tax)

- IRS Form 8615 — Tax for Certain Children Who Have Unearned Income

- IRS Form 8814 — Parents’ Election to Report Child’s Interest and Dividends

- IRS Publication 929 — Tax Rules for Children and Dependents

- IRS Revenue Procedure 2025-32 — 2026 Inflation Adjustments

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.