What Is the Saver’s Credit?

The Saver’s Credit is a federal tax credit that rewards low- and moderate-income workers for contributing to a retirement account. Unlike a deduction, it reduces your actual tax bill — dollar for dollar. If you have earned income and contribute to an IRA or 401(k), this credit may cut what you owe by up to $1,000 — or $2,000 if you file jointly.

Key Takeaways

- The Saver’s Credit (officially, the Retirement Savings Contributions Credit) is a nonrefundable tax credit for eligible retirement account contributions.

- The credit rate is 50%, 20%, or 10% of the first $2,000 you contribute ($4,000 for joint filers), depending on your AGI and filing status.

- Maximum credit: $1,000 per person ($2,000 married filing jointly).

- You must be 18 or older, not a full-time student, and not claimed as a dependent on another return.

- Rollover contributions do not count. Recent retirement account distributions can reduce your eligible contribution amount.

- If you contribute to a Traditional IRA or 401(k), you may receive both a deduction and a credit for the same contribution.

- Starting with 2027 tax returns, the Saver’s Credit for retirement contributions is replaced by the Saver’s Match — a direct government deposit into your retirement account.

Table of Contents

- 1. What Is the Saver’s Credit?

- 2. Who Qualifies?

- 3. How the Credit Rate Works

- 4. Which Contributions Count?

- 5. The Distribution Reduction Rule

- 6. Nonrefundable — What That Means in Practice

- 7. The Double Benefit: Deduction + Credit

- 8. Saver’s Match: What Changes in 2027

- 9. EA Insight

- 10. Frequently Asked Questions

- 11. Related Articles

- 12. Official Resources

1. What Is the Saver’s Credit?

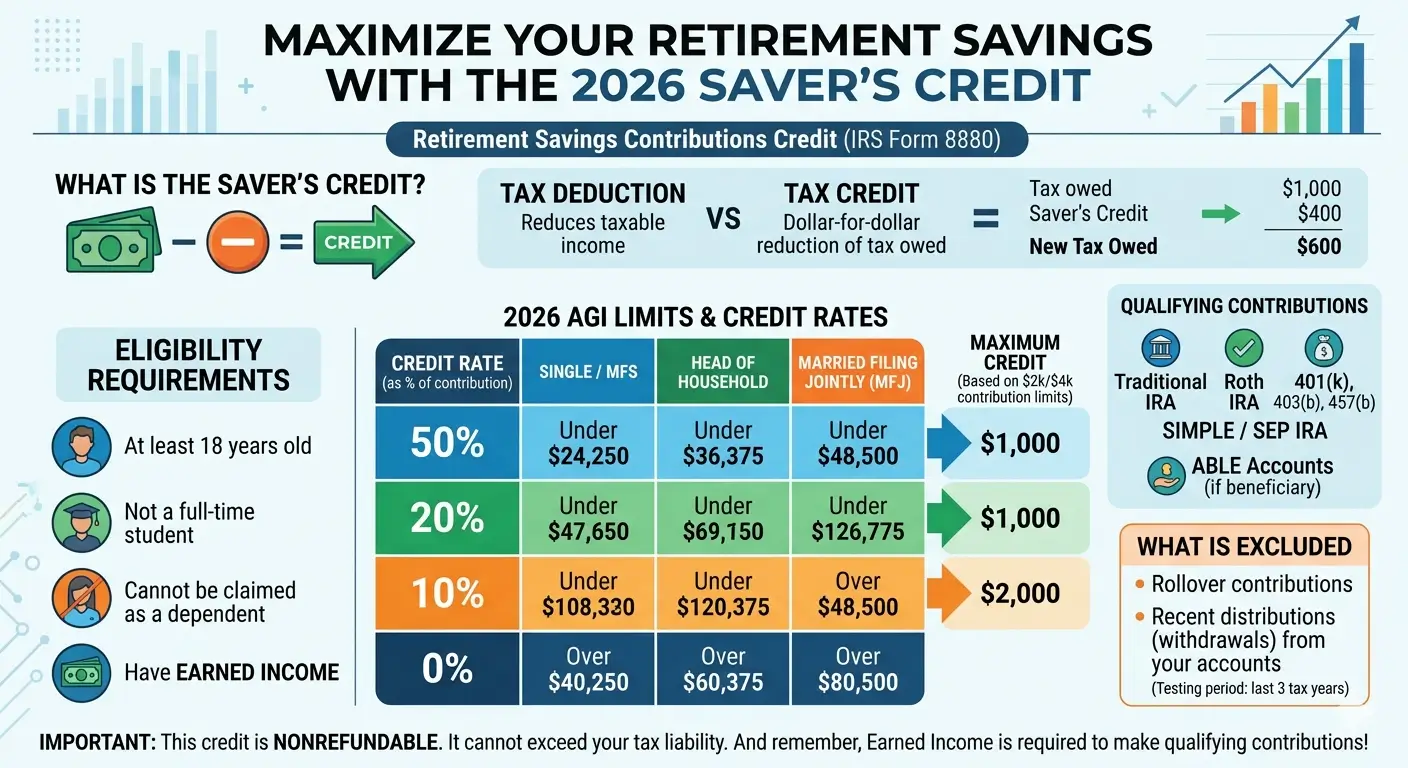

The Saver’s Credit — formally called the Retirement Savings Contributions Credit — is a federal tax credit available to lower- and middle-income workers who contribute to a qualified retirement account. It is claimed using Form 8880 and reported on Schedule 3 of Form 1040.

Unlike a tax deduction, which reduces your taxable income, a tax credit reduces the amount of tax you actually owe. The Saver’s Credit is a direct, dollar-for-dollar reduction of your federal tax liability. If you owe $800 in federal taxes and qualify for a $500 Saver’s Credit, your tax bill drops to $300.

The credit is designed to encourage workers with earned income to save for retirement — specifically those for whom saving can be difficult because of income constraints. To contribute to most retirement accounts, you need earned income, such as wages, salaries, or self-employment income. Because the credit is tied to those contributions, it is closely linked to the concept of earned income: it rewards workers who are actively saving a portion of what they earn.

2. Who Qualifies?

To claim the Saver’s Credit, you must meet three baseline requirements in addition to falling within the AGI limits described in the next section.

| Requirement | Details |

|---|---|

| Age | You must be at least 18 years old by December 31 of the tax year. |

| Dependency status | You cannot be claimed as a dependent on another person’s tax return. |

| Student status | You cannot be a full-time student during any part of five calendar months of the tax year. This includes technical and trade schools but excludes online-only programs, correspondence courses, and on-the-job training. |

If you meet all three requirements, your AGI then determines whether you qualify and what credit rate applies.

3. How the Credit Rate Works

The Saver’s Credit applies at one of three rates — 50%, 20%, or 10% — based on your AGI and filing status. The lower your income, the higher the rate. Once your AGI exceeds the threshold for your filing status, the credit drops to zero.

The credit rate applies to the first $2,000 of eligible contributions per person ($4,000 for married filing jointly). The maximum credit per person is therefore $1,000 ($2,000 for joint filers). These AGI thresholds are indexed for inflation and updated annually by the IRS.

| Credit Rate | Single / MFS | Head of Household | Married Filing Jointly |

|---|---|---|---|

| 50% | $0 – $24,250 | $0 – $36,375 | $0 – $48,500 |

| 20% | $24,251 – $26,250 | $36,376 – $39,375 | $48,501 – $52,500 |

| 10% | $26,251 – $40,250 | $39,376 – $60,375 | $52,501 – $80,500 |

| 0% | Over $40,250 | Over $60,375 | Over $80,500 |

Important: These AGI thresholds are adjusted annually by the IRS for inflation. Check IRS Notice 2025-67 or the current Form 8880 instructions for the most up-to-date figures.

Notice how narrow the income bands are — particularly the transition from 50% to 20% to 10%. A relatively small difference in AGI can drop your credit rate significantly. This is why pre-tax retirement contributions matter: reducing your AGI through a Traditional IRA or 401(k) deferral can push you into a higher credit bracket.

Example: A single filer with an AGI of $24,000 who contributes $2,000 to a Roth IRA qualifies for the 50% rate. Credit = $2,000 × 50% = $1,000. The same filer with an AGI of $25,000 qualifies for only the 20% rate. Credit = $2,000 × 20% = $400. A $1,000 difference in AGI reduces the credit by $600.

4. Which Contributions Count?

The following types of contributions are eligible for the Saver’s Credit:

- Traditional IRA and Roth IRA contributions

- Elective deferrals to a 401(k), 403(b), governmental 457(b), SARSEP, or SIMPLE plan

- Voluntary after-tax contributions to a qualified retirement plan or 403(b) annuity

- Contributions to a federal Thrift Savings Plan (TSP)

- Contributions to a 501(c)(18)(D) plan

- Contributions to an ABLE account for which you are the designated beneficiary

Contributions to a Roth IRA are eligible even though they are made with after-tax dollars and do not reduce your AGI. This is one of the few cases where a Roth contribution provides a direct tax benefit in the year it is made.

What does not count: Rollover contributions — transferring funds from one retirement account to another — are not eligible. Only new contributions (fresh money going into an account) qualify. Employer matching contributions and profit-sharing contributions also do not count.

5. The Distribution Reduction Rule

Your eligible contribution amount for the Saver’s Credit may be reduced by certain distributions you received from retirement accounts. Specifically, the IRS looks at distributions taken during a defined testing period: the two years before the tax year plus the current year up to the filing deadline (including extensions).

For example, if you took a $1,000 distribution from your IRA in a prior year and contributed $2,000 to a retirement account in the current year, your net eligible contribution for the credit is reduced to $1,000.

| Scenario | Calculation | Eligible Contribution for Credit |

|---|---|---|

| Contributed $2,000, no prior distributions | $2,000 – $0 | $2,000 |

| Contributed $2,000, prior distribution of $800 | $2,000 – $800 | $1,200 |

| Contributed $2,000, prior distribution of $2,500 | $2,000 – $2,500 = negative | $0 (credit eliminated) |

Certain distributions are excluded from this calculation — including distributions that are rolled over to another plan, distributions from an inherited IRA by a non-spousal beneficiary, and distributions from a military retirement plan (other than the TSP). Review the current Form 8880 instructions for the complete list of excluded distributions.

6. Nonrefundable — What That Means in Practice

The Saver’s Credit is a nonrefundable tax credit. This means it can reduce your federal tax liability to zero, but it cannot produce a refund on its own. If the credit exceeds what you owe, the excess is lost — it does not carry forward to future years and is not paid out to you.

| Tax Owed (Before Credit) | Saver’s Credit | Result |

|---|---|---|

| $800 | $500 | Tax reduced to $300 |

| $1,000 | $1,000 | Tax reduced to $0 |

| $400 | $1,000 | Tax reduced to $0 — $600 credit is lost |

Taxpayers at the lowest income levels — those who may owe little or no federal income tax due to the standard deduction and other credits — may find that the Saver’s Credit provides limited benefit in dollar terms. This is a structural limitation of nonrefundable credits. The Saver’s Match, which takes effect in 2027, is specifically designed to address this by depositing money directly into retirement accounts regardless of tax liability.

7. The Double Benefit: Deduction + Credit

One of the most underutilized features of the Saver’s Credit is that it can be combined with a tax deduction for the same contribution. If you contribute to a Traditional IRA or make a pre-tax 401(k) deferral, that contribution may reduce your AGI — and that lower AGI may then qualify you for a higher Saver’s Credit rate.

How it works: A Traditional IRA contribution lowers your AGI, which may push you from the 10% credit bracket into the 20% or 50% bracket. You receive both the deduction (which lowers your taxable income) and the credit (which directly reduces your tax bill) from the same contribution.

Roth IRA contributions do not reduce your AGI, so they do not create this AGI-lowering effect. However, Roth contributions still qualify for the credit if your AGI already falls within the eligible range. In that case, you receive the credit without an AGI deduction — a different combination, but still a significant benefit.

8. Saver’s Match: What Changes in 2027

Under the SECURE 2.0 Act of 2022, the Saver’s Credit for retirement account contributions is scheduled to be replaced by the Saver’s Match beginning with 2027 tax returns (filed in 2028). The current Saver’s Credit structure for qualified retirement contributions applies through tax year 2026.

Here is how the two programs compare:

| Feature | Saver’s Credit (through 2026) | Saver’s Match (from 2027) |

|---|---|---|

| Form of benefit | Reduces your tax bill | Government deposits funds directly into your retirement account |

| Benefit if tax owed is $0 | No benefit (nonrefundable) | Full benefit still paid into account |

| Maximum benefit | $1,000 / $2,000 (MFJ) | $1,000 (50% match on up to $2,000) |

| Form used | Form 8880 | Separate form (to be issued) |

Starting with 2027 returns, Form 8880 will continue to be used only for Saver’s Credit claims on ABLE account contributions, which are permanently retained under P.L. 119-21 and are not converted to the Saver’s Match. For ABLE contributions from 2027 onward, the maximum qualifying contribution also increases from $2,000 to $2,100.

EA Insight

The Saver’s Credit is one of the most consistently overlooked credits in practice. I see it missed most often by seasonal and part-time workers, recent graduates in their first jobs, and households where one spouse works and the other does not — situations where income happens to fall squarely in the eligible range, but the taxpayer doesn’t realize the credit exists.

The most common mistake I see is with the distribution reduction rule. A taxpayer takes a hardship distribution one year because they need the money, then contributes again the following year. They expect the full credit — but the prior distribution partially or entirely offsets their new contribution for credit purposes. The credit can disappear even when the taxpayer did everything right in the current year. If you have taken any retirement account distributions in the past two to three years, check whether they affect your Form 8880 calculation before assuming you qualify.

The double benefit — getting both a Traditional IRA deduction and the Saver’s Credit from the same contribution — is genuinely powerful for eligible taxpayers. Pre-tax retirement contributions lower AGI, which can move a taxpayer from the 10% bracket into the 20% or even 50% bracket. The actual after-tax cost of saving $2,000 for retirement can be surprisingly low once both benefits are applied.

One planning note: for taxpayers who are currently in the eligible income range, the AGI brackets are cliff-based — there is no gradual phase-out, just a sharp drop from one rate to the next. A Traditional IRA contribution made before the filing deadline can lower AGI and preserve access to a higher credit rate. This is worth a calculation before writing that contribution off as optional.

Frequently Asked Questions

Do I need earned income to claim the Saver’s Credit?

Indirectly, yes. The Saver’s Credit requires a qualifying contribution to a retirement account — and most eligible accounts, including Traditional and Roth IRAs, require earned income (wages, self-employment income, etc.) in order to contribute. Without earned income, you generally cannot make IRA contributions, and therefore cannot generate the contribution that triggers the credit.

Can I claim the Saver’s Credit for a Roth IRA contribution?

Yes. Roth IRA contributions qualify for the Saver’s Credit even though they are made with after-tax dollars. Note that Roth contributions do not reduce your AGI, so they do not provide the same double benefit as Traditional IRA or pre-tax 401(k) contributions.

What happens if I am in the 50% bracket but only owe $300 in taxes?

Because the Saver’s Credit is nonrefundable, the credit is limited to the amount of tax you owe. In this example, even if your calculated credit is $1,000, only $300 will be applied — reducing your tax to zero. The remaining $700 is not refunded and does not carry forward.

Does my employer’s matching contribution count toward the credit?

No. Only your own contributions count — your elective deferrals or personal IRA contributions. Employer matching contributions, profit-sharing contributions, and rollover amounts are excluded from the calculation.

What is the AGI used to determine the credit — before or after IRA deductions?

The AGI used on Form 8880 is the figure on line 11 of Form 1040 — which is your gross income after above-the-line adjustments, including any deductible Traditional IRA contribution. This means that making a deductible IRA contribution can lower the AGI figure used to determine your credit rate, potentially qualifying you for a higher rate.

I am a part-time student. Can I still claim the credit?

Possibly, yes. The student exclusion applies only to full-time students — those enrolled full-time for any part of five calendar months of the tax year. Part-time students are not disqualified from the credit as long as the other eligibility conditions are met.

What is the Saver’s Match and when does it start?

The Saver’s Match replaces the Saver’s Credit for qualified retirement contributions beginning with 2027 tax returns. Instead of a tax credit, the government will deposit a matching contribution of up to 50% of your retirement savings (up to $1,000) directly into your retirement account. Unlike the current credit, the Saver’s Match is not limited by your tax liability — it can benefit workers who owe little or no federal income tax.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.