She Filed Her Own Taxes and Owed $100 — Until We Found $7,200 on Her Pay Stub

A new OBBBA deduction can shave thousands off the tax bills of millions of hourly workers. But for the 2025 tax year, your W-2 doesn’t tell you it exists. If you don’t open your final pay stub, the deduction disappears as if it were never there.

Key Takeaways

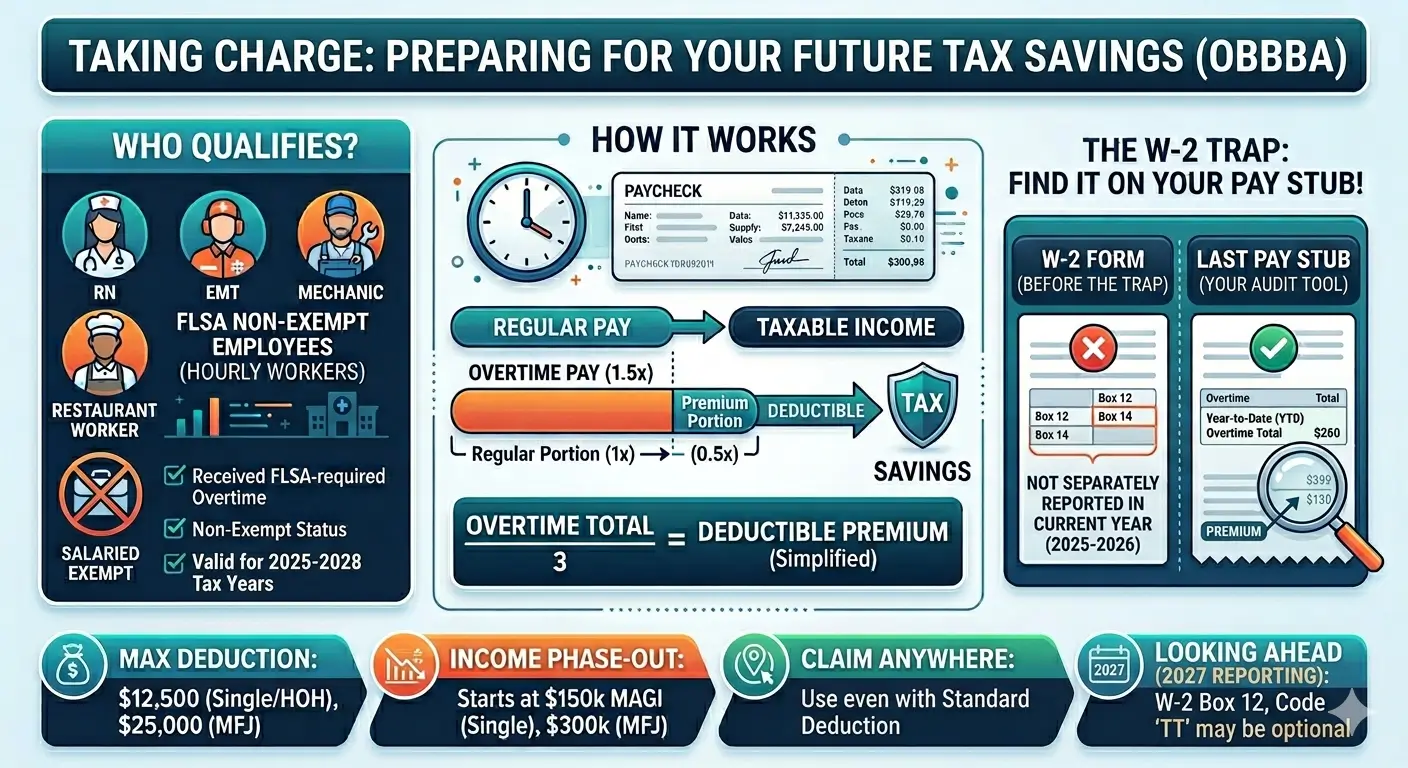

- The new OBBBA Qualified Overtime Pay Deduction covers only the premium portion of FLSA-required overtime — the “half” in “time-and-a-half.” The cap is $12,500 for Single and Head of Household filers.

- You must be an FLSA non-exempt employee to qualify. Hourly RNs, EMTs, mechanics, and restaurant workers typically qualify; salaried exempt employees do not.

- For 2025, employers are not required to report this on your W-2. Many self-filers never realize the deduction exists.

- Divide your last pay stub’s YTD overtime total by 3 to get your premium. IRS Notice 2025-69 explicitly allows this self-calculation method.

- The deduction is claimed on the new Schedule 1-A, separate from the standard deduction. It phases out once MAGI exceeds $150,000 (Single/HOH).

Table of Contents

1. Meet Jessica

Jessica is 36, a registered nurse working night shifts in the ICU of a New York City hospital. Nine years on the floor. She finalized her divorce five years ago, and now lives with her fifteen-year-old son.

Last year, she picked up a lot of overtime. Night shifts were standard; weekend call-ins, she rarely turned down. Holidays — she actually volunteered. Tutoring fees for her son, the mortgage, the car insurance — one or two extra OT shifts could buy her a month of breathing room.

This January, she did what she had done every year. She entered her W-2 into TurboTax. The result was not what she expected.

— Jessica

She checked the W-2 again and again. Box 1, Box 2, Box 3, Box 5 — the same kind of numbers she had seen every year. Her data entry was correct. The result was different. Eventually, she called our office.

2. The IRS Rule — A New Deduction for Overtime Pay

The One Big Beautiful Bill Act (OBBBA), enacted in July 2025, created a new deduction for hourly workers: the Qualified Overtime Pay Deduction under Internal Revenue Code §225. It did not exist before, and it applies on a temporary basis from 2025 through 2028.

Only the premium portion of FLSA-required overtime qualifies — the part above your regular rate. Think of “time-and-a-half.” The “half” qualifies. The “time” does not.

Bottom line

The deduction applies to the OT premium, not the entire OT paycheck. If an RN with a $48 regular rate is paid $72 per hour for overtime, only $24 per hour is deductible.

Two conditions must be met.

First, the worker must be FLSA non-exempt. This typically includes hourly occupations such as RNs, CNAs, EMTs, mechanics, and restaurant staff. Salaried exempt employees are not eligible.

Second, the overtime itself must be FLSA-required overtime. State-law overtime and overtime owed under a collective bargaining agreement don’t count. California’s daily 8-hour overtime is a common trap here — it isn’t FLSA-based, so it falls outside this deduction.

Limits and phase-out:

| Filing Status | Maximum Deduction | MAGI Phase-out Start |

|---|---|---|

| Single / HOH | $12,500 | $150,000 |

| Married Filing Jointly | $25,000 | $300,000 |

Above the phase-out threshold, the deduction is reduced by $100 for every $1,000 of MAGI in excess of the limit.

The deduction is claimed on Schedule 1-A and works independently of the standard or itemized deduction. Standard deduction filers get it too. One important detail: it’s a below-the-line deduction. It reduces your taxable income, but it doesn’t lower AGI.

Important: Beginning with tax year 2026, qualified overtime compensation will be reported on your W-2 in Box 12 with code TT. For tax year 2025, however, employers are not required to report it separately. Some employers may voluntarily list it in Box 14 as “QUAL OT” or provide a separate statement; many will not. Without that disclosure, self-filers walk past the deduction entirely.

3. Reading Her Pay Stub — Where the $7,200 Was Hiding

Jessica brought her W-2 and her last pay stub. She set them on the table and said, before we had even looked:

We opened the W-2. Box 1 (Wages, tips, other comp): $103,500. Box 2 (Federal income tax withheld): $8,332. Boxes 3 and 5 looked normal. Every number matched what she had typed into TurboTax.

The problem was not a data-entry error. The problem was missing information.

Step 1 — Box 14 was empty

We checked Box 14 on her W-2 — the box labeled “Other.” Some employers use this box to flag qualified overtime premium with a code such as “QUAL OT” or “OBBBA OT.” Jessica’s Box 14 was empty.

That isn’t unusual. For tax year 2025, employers and other payers are not required to report qualified overtime compensation separately on Forms W-2, 1099-NEC, and 1099-MISC. Reporting was voluntary, and most employers’ payroll systems weren’t ready in time. Beginning with tax year 2026, the reporting is mandatory through the new Box 12 code TT.

Jessica’s case wasn’t unusual at all. It was ordinary in a way that hurts self-filers: information your W-2 doesn’t show is, to a self-filer, information that doesn’t exist.

Step 2 — The last pay stub

We turned to her December 31 pay stub. The Year-to-Date Earnings section held the number we were looking for.

| YTD Earnings | Amount |

|---|---|

| Regular | $96,300.00 |

| Overtime (1.5×) | $21,600.00 |

| Holiday | $0.00 |

| Shift Differential | $0.00 |

| Total Gross | $117,900.00 |

Her regular rate ran about $48 per hour. Overtime paid at 1.5× — $72 per hour. So that $21,600 of OT pay breaks down into two pieces: $48 per hour for the time she worked, plus $24 per hour as the premium on top.

Premium calculation (allowed under IRS Notice 2025-69)

$21,600 ÷ 3 = $7,200 deductible premium

For time-and-a-half OT, the premium is exactly one-third of the total OT pay. The 1.5× total is composed of 1× regular + 0.5× premium, so the premium portion equals total ÷ 3.

Note: The $103,500 in W-2 Box 1 doesn’t match the $117,900 Total Gross on her pay stub. That’s because pre-tax 401(k) contributions, pre-tax health premiums, and similar items get pulled out before Box 1 is calculated. Don’t use Box 1 to figure your premium — use the OT line on your pay stub.

Step 3 — Entering Schedule 1-A

We entered $7,200 on Line 7 (qualified overtime compensation) of Schedule 1-A, a new attachment to Form 1040 introduced for tax year 2025. Schedule 1-A is a single form that consolidates the four new OBBBA deductions: qualified overtime, qualified tips, car loan interest, and the senior deduction. Standard deduction filers and itemizers use it the same way.

That $7,200 doesn’t touch her AGI, but it does come off her taxable income. Jessica sits in the 22% bracket, which works out to roughly $1,584 in federal tax savings ($7,200 × 22%).

Before vs. After — the refund swing

| Line Item | Self-Filed Return | EA-Prepared Return |

|---|---|---|

| W-2 Box 1 Wages | $103,500 | $103,500 |

| Standard Deduction (HOH) | ($24,150) | ($24,150) |

| Qualified OT Premium (Schedule 1-A) | $0 | ($7,200) |

| Taxable Income | $79,350 | $72,150 |

| Federal Income Tax | $10,632 | $9,048 |

| Child Tax Credit (son, age 15) | ($2,200) | ($2,200) |

| Total Tax Liability | $8,432 | $6,848 |

| Federal Withholding (Box 2) | ($8,332) | ($8,332) |

| Result | $100 owed | $1,484 refund |

Bottom line

From $100 owed to $1,484 refund — a swing of $1,584. The premium portion of nearly 250 OT hours she had worked through the year came back to her in full.

Jessica looked at the comparison table for a long time. Then she said:

Most RNs build $7,000 to $10,000 of OT premium in a year. Most self-filers, looking at an empty Box 14, conclude the deduction simply doesn’t apply to them — and file accordingly.

Before Jessica left the office, we handed her a one-page note. “Show this to your coworkers.” The note read as follows.

4. What to Check Right Now

If you work hourly and put in overtime, run through these five checks before filing your 2025 return.

- ✅ Pull your last pay stub of 2025 (the one ending closest to December 31). In the YTD Earnings section, locate the line labeled “Overtime” or “OT” — that figure is the year’s total.

- ✅ Check W-2 Box 14. Some employers list “QUAL OT” or “OBBBA OT” here. An empty Box 14 doesn’t disqualify you — you can calculate the premium from the pay stub.

- ✅ Confirm you are FLSA non-exempt. If you’re paid hourly and earn 1.5× for hours over 40 in a workweek, you almost certainly qualify. Salaried exempt employees do not. When in doubt, ask HR or payroll.

- ✅ Calculate your premium. Divide total time-and-a-half OT pay by 3 to get the deductible premium. For double-time OT, divide by 4.

- ✅ Enter it on Schedule 1-A. This new attachment to Form 1040 is available to both standard deduction and itemizing filers. The cap is $12,500 for Single/HOH.

EA Insight

In OBBBA’s first filing season, the most common error I’ve caught on self-prepared returns coming through our office for review hasn’t been missed mortgage interest, or a misentered dependent. It’s been this — a missed overtime deduction. Information the W-2 didn’t show was, for the self-filer, information that didn’t exist.

The difficulty here isn’t legal complexity. It’s information asymmetry. Tax year 2025 is the last year an employer isn’t required to flag this premium on the W-2. “Not required” doesn’t mean “not eligible,” though. IRS Notice 2025-69 explicitly authorizes a self-calculation method using pay stubs. A taxpayer who qualifies — but skips the deduction because the W-2 is silent — is exactly the person Congress designed this provision to reach.

Starting in 2026, qualified overtime will appear automatically in Box 12 code TT. Don’t assume the system will be perfect in year one. We are already seeing payroll vendors put total OT pay into the OBBBA field instead of the premium portion. If you copy that figure straight onto Schedule 1-A, you will inflate your deduction by 3×. The pay stub remains the verification anchor either way.

One more thing — this deduction is federal only. State income tax is separate. Some states automatically conform to OBBBA; others have decoupled and require an add-back. Check your state’s position before filing.

There’s a new line on the document checklist we send clients before tax season now. “Last pay stub of the year.” That one line is what got Jessica her $1,484 back.

EA Summary

For tax year 2025, OBBBA’s Qualified Overtime Pay Deduction is the deduction your W-2 won’t help you find. If you’re hourly and you put in overtime, your last pay stub holds the answer — divide the YTD overtime figure by 3, and that’s your deductible premium. If you self-filed and ended up owing money, pull the return back out. One pay stub can flip the result.

Frequently Asked Questions

My W-2 Box 14 is empty. Does that mean I’m not eligible for the deduction?

No. An empty Box 14 does not disqualify you. For tax year 2025, employers are not required to separately report qualified overtime compensation, and individuals who do not receive that information may calculate it themselves using methods described in Notice 2025-69 and the Schedule 1-A instructions. Divide the YTD overtime total on your last pay stub by 3 to get the deductible premium.

What’s the difference between “overtime pay” and “overtime premium”?

Overtime pay is everything you receive for those OT hours. The premium is just the part that sits above your regular rate. If your regular rate is $48 and OT is paid at $72 per hour, $48 of that $72 is regular-rate compensation; $24 is the premium. For straight time-and-a-half OT, the premium ends up being one-third of total OT pay.

I’m paid double-time (2×) for overtime. How do I calculate my premium?

If you receive double-time, the deductible premium is limited to the FLSA-required half-time portion only. Premium paid above that — required by a CBA or state law — does not qualify. The shortcut: divide total time-and-a-half OT pay by 3, or divide total double-time OT pay by 4. Example: an employee with a $20 regular rate paid $40 per hour for OT can deduct $10 per hour ($20 × 0.5). On $28,000 of double-time OT pay, the deductible amount is $28,000 ÷ 4 = $7,000.

I take the standard deduction. Can I still claim this overtime deduction?

Yes. The qualified overtime deduction is available for both itemizing and non-itemizing taxpayers. It’s claimed on the new Schedule 1-A separately from your standard or itemized deduction. Note that it reduces taxable income but does not reduce AGI.

Does this deduction reduce my Social Security and Medicare taxes too?

No. Overtime wages are not exempt from Social Security and Medicare taxes for either the employee or the employer; even when the deduction applies, the employee’s share is still withheld from total wages and the employer matches and pays it to the IRS. The OBBBA deduction applies to federal income tax only. State and local treatment varies — some states conform to the federal deduction, others have decoupled and require an add-back.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.