From ITIN to SSN: What Changes for Your Family’s Tax Filing

After two years of waiting on her green card, Helen finally got her Social Security card. Her family assumed tax season would look the same — just with a different number. The reality is more complicated, and getting it wrong can shrink a refund or trigger an IRS notice.

Key Takeaways

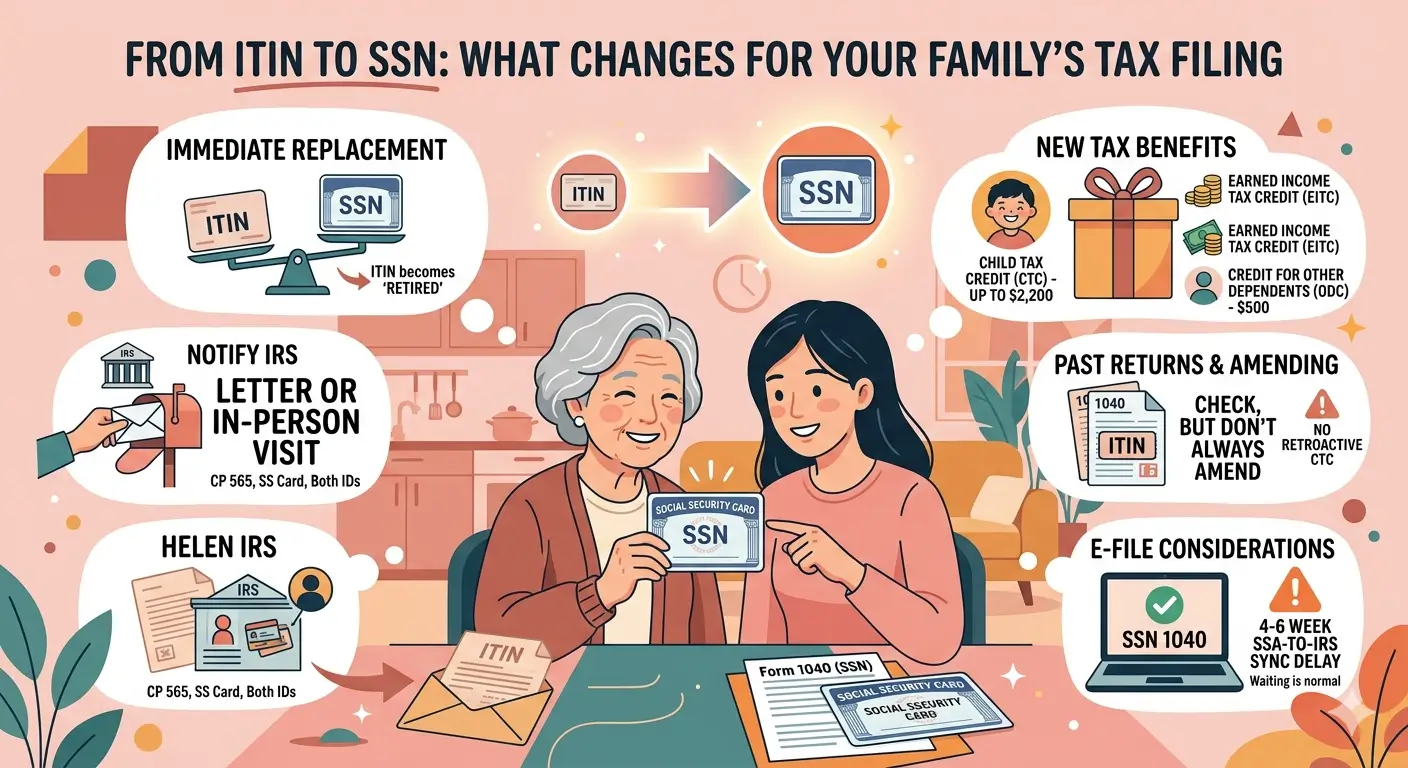

- Once your SSN is issued, every tax document going forward must use it — your ITIN is no longer valid.

- The IRS doesn’t merge ITIN and SSN records on its own. You have to notify them, in writing or in person.

- The Social Security Administration is a separate notification — needed to credit your past ITIN earnings to your future retirement benefit.

- The year your SSN arrives, new tax benefits may open up — Child Tax Credit, EITC, and others closed to ITIN filers.

- Past ITIN returns usually don’t need amending, but check for missing withholding credits or filing errors before assuming.

- Both CTC and EITC cannot be claimed retroactively for years when you only had an ITIN, even after your SSN arrives.

Table of Contents

- 1. Meet Helen

- 2. The Rule: SSN Replaces ITIN Immediately

- 3. Notifying the IRS — and the SSA

- 4. Filing the Year You Get Your SSN

- 5. New Benefits That Open Up

- 6. Past ITIN Returns: Amend or Leave Alone?

- 7. What to Check Right Now

- 8. EA Insight

- 9. Frequently Asked Questions

- 10. Related Articles

- 11. Official Resources

1. Meet Helen

Helen, 67, came to the U.S. from Seoul two years ago to live with her son David, his wife Sarah, and her granddaughter Lily, who turned eight last fall. Most mornings she walks Lily to the school bus. Most evenings dinner is on the table by the time David and Sarah get home from work.

Two years ago, when David sponsored her green card application (Form I-485), Helen knew the wait would be long. She got an ITIN so the family could claim her as a dependent. Tax seasons came and went. Then in early February, the EAD work permit arrived. A few weeks later, the Social Security card showed up in the mailbox.

Helen brought it to Sarah at the kitchen table.

Sarah wasn’t sure. Most families landing on this exact moment aren’t sure either. The transition has more pieces than people expect — and a few of them are easy to miss.

2. The Rule: SSN Replaces ITIN Immediately

The IRS rule is unambiguous. Once you receive your SSN, you must use it on every tax document immediately, and your ITIN is no longer valid for you. One person can’t have two active taxpayer identification numbers running in parallel.

Bottom line

From the day your SSN is issued, every tax form should carry only your SSN. Your ITIN is officially retired the moment you notify the IRS.

Here’s the part most people miss: receiving an SSN doesn’t automatically link your old ITIN tax history to it. Two separate files sit in the IRS database — one under your ITIN, one under your SSN — until you ask them to be merged. Skip that step and past withholding credits, reported income, and dependent claims may not flow through. The result can be a smaller refund, or an IRS notice that doesn’t make sense.

3. Notifying the IRS — and the SSA

Two notifications, two separate agencies. People often handle the first and forget the second.

IRS Method 1 — By Mail

Write a short letter that includes:

- Your full legal name

- Your current mailing address

- Your old ITIN

- Your new SSN

- A clear request: “Please combine my ITIN tax records with my new SSN.”

Attach a copy of your Social Security card. If you still have your CP 565 (the original ITIN assignment notice), attach that too.

Mail to:

IRS ITIN Operation

P.O. Box 149342

Austin, TX 78714-9342

IRS Method 2 — In Person

You can also visit a local IRS Taxpayer Assistance Center (TAC). Bring your original Social Security card and your CP 565. Most TACs are appointment-only — call ahead or use the office locator on irs.gov.

Don’t Forget the Social Security Administration

Notifying the IRS handles your tax records. It does not handle your future Social Security benefits. If you worked under your ITIN — even a part-time job for a single year — those earnings are sitting in SSA’s Earnings Suspense File, not credited to anyone’s retirement account.

To move them to your new SSN, visit your local SSA office with your W-2s from the ITIN years and request an earnings record transfer. This is a completely separate process from the IRS notification, and equally important for your long-term benefit calculation. For someone who worked years on an ITIN before getting their green card, this single step can change their retirement benefit decades down the road.

Don’t skip either step. Without the IRS notification, your past withholding credits and reported income don’t flow into your SSN account. Without the SSA notification, the work you did under your ITIN never counts toward your retirement benefit. Both fixes are simple now and frustrating to untangle later.

4. Filing the Year You Get Your SSN

Helen received her SSN in early February. The family is preparing this year’s return now. Use SSN or ITIN?

Answer: SSN.

The rule is straightforward. Once your SSN is issued, every Form 1040 you file from that point on uses it — regardless of which tax year the return covers. If your SSN arrived in February and you’re filing a return for the prior tax year in April, the return goes in under your new SSN.

| Item | What to Do |

|---|---|

| Form 1040 taxpayer ID | Use SSN (not ITIN) |

| W-2 still shows your old ITIN | Enter the W-2 as printed; put your SSN on Form 1040 (mismatch is allowed) |

| Tell your employer | Give them your new SSN; ask for a corrected W-2 (Form W-2c) if needed |

| E-file allowed? | Yes — the IRS system tolerates ITIN/SSN mismatch on supporting forms |

| Claimed as a dependent | Use SSN in the dependents section |

| ITIN going forward | Don’t use it on any tax form again |

Heads up on e-file rejection. Right after your SSN arrives, the e-file system can reject your return for the first 4–6 weeks. That’s how long it takes the Social Security Administration to push new SSN data through to the IRS. If your e-file rejects, wait 2–3 weeks and try again, or switch to paper filing. Don’t refile under the old ITIN — that creates a different problem entirely.

5. New Benefits That Open Up

Several tax benefits are closed to ITIN filers. The year your SSN arrives, some of those open up.

| Benefit | With ITIN | With SSN |

|---|---|---|

| Child Tax Credit (CTC) | Not available | Up to $2,200/child |

| Credit for Other Dependents (ODC) | $500 (allowed) | $500 (still allowed) |

| Earned Income Tax Credit (EITC) | Not available | Available if earnings qualify |

| Social Security work credits | Not earned | Earned with each paycheck |

For Helen specifically, CTC doesn’t apply — she’s 67, not a qualifying child. But she remains a qualifying relative under ODC ($500), which the family had already been claiming with her ITIN. The change for Helen is mostly behind the scenes: cleaner e-filing, faster processing, no risk of ITIN expiration delays.

The bigger shift comes if Helen starts working. With her EAD and SSN, any earned income she brings in could qualify the family for additional credits — and she begins building a Social Security work record from day one. That’s a real long-term benefit even if it doesn’t show up on this year’s refund.

Watch for EITC eligibility — going forward only

If Helen begins working with her EAD and the family’s combined earned income falls under the EITC limits, they may qualify for a credit they couldn’t claim before. EITC absolutely requires SSN — there’s no ITIN path. One important caveat: like the CTC, EITC cannot be claimed retroactively. The taxpayer, spouse, and any qualifying children must all have valid SSNs by the original due date of that year’s return (including extensions). Past ITIN years stay closed.

6. Past ITIN Returns: Amend or Leave Alone?

Most of the time, leave them alone. Once you send the ITIN-to-SSN notification, the IRS merges the records on its end. You don’t need to file Form 1040-X just to update the number on past returns.

Some situations do warrant a closer look at past returns.

| Situation | Amend? | Why |

|---|---|---|

| ITIN return was correct, no missing benefits | No | IRS will merge records via notification |

| CTC or EITC was missed in a past year because of ITIN | No (cannot be claimed retroactively) | SSN must have existed by the original due date of that year’s return |

| Income or deduction error on a past return | Worth reviewing | Fix the error and update the ID at the same time |

| Withholding credits that didn’t post under your ITIN | Worth reviewing | Three-year window for refund claims still applies |

The retroactive trap. Both Child Tax Credit and Earned Income Tax Credit cannot be claimed retroactively. The required SSN must have been issued before the original due date of the return (including extensions) for that tax year. Getting an SSN later doesn’t reopen past years. This rule is set by IRC §24(h)(7) for CTC and §32(m) for EITC, and neither is flexible.

And if you already filed this year’s return under your ITIN before your SSN arrived? File Form 1040-X to switch the return to your SSN, and send the ITIN-to-SSN merge notification at the same time. Doing both keeps your record clean.

7. What to Check Right Now

- Has your physical Social Security card arrived?

- Have you sent the IRS ITIN-to-SSN notification letter, or scheduled a TAC visit?

- Does the letter include your ITIN, your SSN, your full name, your address, and copies of your SS card and CP 565?

- If you worked under your ITIN, have you visited an SSA office to transfer those earnings to your SSN record?

- Does this year’s Form 1040 carry your SSN (not your ITIN)?

- If your W-2 still shows the ITIN, did you enter the W-2 as printed and put the SSN on Form 1040?

- Have you given your employer your new SSN and asked about a Form W-2c if needed?

- If e-file rejects, are you ready to wait 4–6 weeks or switch to paper filing?

- Have you checked which credits may now apply (CTC, EITC, others)?

- Did you review past ITIN returns for missing withholding credits or filing errors that could justify amending?

EA Insight

The ITIN-to-SSN transition trips people up in six predictable ways.

The first is skipping the IRS notification. Clients often think changing the number on this year’s tax return is enough. It isn’t. Without the notification letter or a TAC visit, your ITIN file sits separately from your SSN file in the IRS system. Past withholding credits and reported income don’t connect, and a refund that should have been larger comes back smaller — often with no obvious explanation.

The second is using both numbers in parallel after the SSN arrives. Once your SSN is issued, the ITIN is dead. Some people keep using the old ITIN out of habit, especially on state tax accounts or financial paperwork. Mixing the two creates duplicate records the IRS catches later.

The third is assuming the SSN unlocks past Child Tax Credit or EITC. It doesn’t. Both credits lock eligibility to the original due date of each year’s return. If a child or parent only had an ITIN at that deadline, that year’s credit stays closed even after everyone has SSNs.

The fourth is panicking when e-file rejects. The SSA-to-IRS data sync takes 4–6 weeks. A rejection in the first month after SSN issuance is normal — wait a few weeks and retry, or paper-file. The wrong move is to refile under the old ITIN, which creates a different problem and gets you nowhere.

The fifth — and one most people never hear about — is the Social Security earnings record. Wages earned and reported under an ITIN don’t post to your future Social Security benefit. They sit in something called the Earnings Suspense File at SSA. Notifying the IRS does not move them. You have to visit a Social Security Administration office in person, bring your W-2s from the ITIN years, and request that those earnings be transferred to your SSN record. For someone who worked years on an ITIN before getting their green card, this single step can meaningfully change their retirement benefit decades later.

The sixth is forgetting the state. Federal IRS notification doesn’t update your state tax records. Most states resolve this automatically when you file your next state return under your SSN — but check whether your state requires a separate notification, especially if you had withholding or estimated payments under your ITIN that need to follow you to the new number.

EA Summary

When your SSN arrives, four things happen at once: every future tax document switches to SSN, the IRS needs a written or in-person notification to merge your records, the SSA needs a separate visit to transfer your past earnings, and a few new tax benefits become available going forward. Past ITIN returns generally don’t need amending — but neither CTC nor EITC can be claimed retroactively for past ITIN years, no matter what.

Frequently Asked Questions

Does my ITIN expire automatically when I get an SSN?

Not automatically. The IRS retires your ITIN only after you notify them of the switch. Until then, both numbers technically exist in the system, which can cause matching issues.

Why do I need to notify the SSA separately?

Because the IRS and SSA keep separate records. The IRS handles your tax filings; the SSA tracks your lifetime earnings for retirement benefits. If you worked under an ITIN, those wages are in SSA’s Earnings Suspense File and won’t count toward your Social Security benefit until you ask SSA to transfer them to your new SSN.

How soon do I need to send the IRS notification?

There’s no statutory deadline, but sooner is better. Sending it before your next tax filing keeps the records cleanest.

I got my SSN mid-year. What number do I use for that year’s return?

Use your SSN. The timing within the year doesn’t matter — once issued, your SSN is what goes on Form 1040.

I already filed this year under my ITIN before my SSN arrived. What now?

File Form 1040-X to switch the return to your SSN, and submit the ITIN-to-SSN merge notification to the IRS at the same time.

Can I claim the Child Tax Credit or EITC for past years now that I have an SSN?

No. Both CTC and EITC require valid SSNs by the original due date of each year’s return (including extensions). Getting your SSN later doesn’t reopen past years for either credit.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.