When Your College Senior Turns 24: Why You Can’t Claim Them Anymore

For two decades, Linda has filed her taxes the same way. This year, the answer changes. One date on the calendar erases a $500 credit, drags her son’s side gig into self-employment territory, and forces the family to untangle two separate returns instead of one.

Key Takeaways

- Full-time college student or not — once your child reaches age 24 by December 31, the Qualifying Child path closes.

- Qualifying Relative is the fallback, but only if the child’s gross income stays under $5,300 in 2026.

- Miss both tests and you lose the $500 Credit for Other Dependents along with any chance of claiming the child.

- 1099-NEC income from DoorDash, Uber, or freelance work is self-employment — Schedule C plus 15.3% SE tax kicks in at $400 of net earnings.

- When the child files separately, the “Can be claimed as a dependent” checkbox has to match what the parents do, or both returns get rejected.

Table of Contents

- 1. Meet Linda

- 2. The IRS Rule — Qualifying Child’s Four Tests

- 3. Case Breakdown — Applying the Rule to Ethan

- 4. What If the Numbers Were Different?

- 5. The DoorDash Surprise — 1099-NEC Hits Hard

- 6. The Checkbox That Wrecks E-File

- 7. What to Check Right Now

- 8. EA Insight

- 9. Frequently Asked Questions

- 10. Related Articles

- 11. Official Resources

1. Meet Linda

Linda lives in Brooklyn. Every spring for the last twenty-something years, she’s filed a joint return with her husband David and listed their oldest son Ethan as a dependent. She’s never thought twice about it. Ethan is in his senior year of college, applying to medical schools, still living in the dorms most of the year and coming home between terms. The Parks pay for everything — tuition, rent, groceries, the works.

This year was supposed to be no different. Right before April 15, David filed Form 4868 to extend the return. The plan was to wrap things up sometime in August, no rush.

Then the mail came. A W-2 in Ethan’s name. And a 1099-NEC.

Linda walked into the EA office holding the paperwork. Her question was simple. “We can still claim Ethan as a dependent like every other year, right?”

The answer was no. And not for one reason — for three, all stacking on top of each other.

2. The IRS Rule — Qualifying Child’s Four Tests

To claim someone as a dependent, the IRS requires them to fit into one of two boxes: Qualifying Child or Qualifying Relative. The rules sit in IRC §152 and Publication 501.

Qualifying Child has four tests, and a child has to pass all four:

- Relationship — your child, grandchild, sibling, half-sibling, or a descendant of any of these

- Age — under 19, or under 24 if a full-time student, or any age if permanently and totally disabled

- Residency — lived with you more than half the year (school counts as a temporary absence, so dorm life still qualifies)

- Support — the child didn’t provide more than half their own support

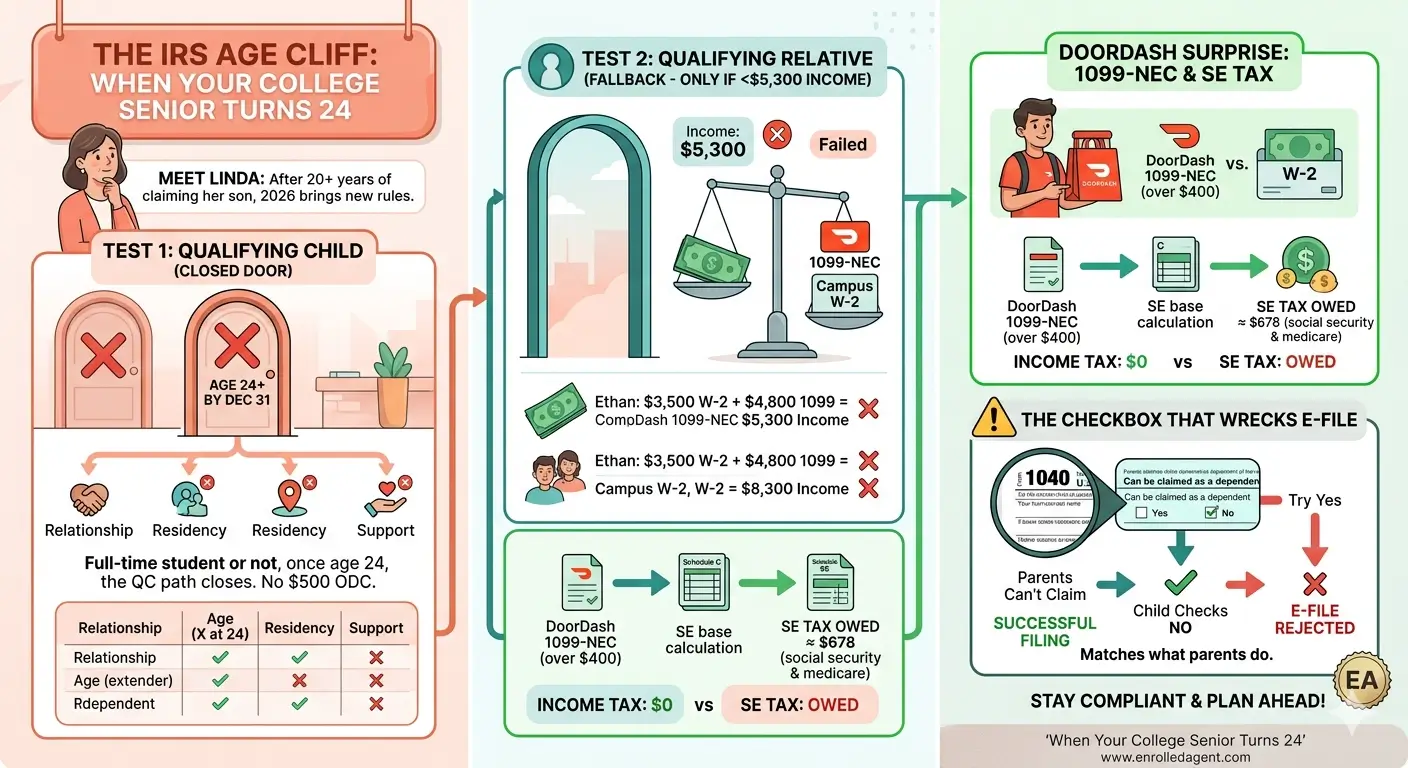

The age test is the cliff most parents don’t see coming. “Under 24” means the child has not yet reached their 24th birthday by December 31 of the tax year. Hit 24 anywhere in that calendar year — even on December 31 itself — and the Qualifying Child door closes.

Bottom line

Your full-time college student stops being a Qualifying Child the moment they turn 24, no exceptions for tuition you’re still paying or bedrooms still kept ready.

If the Qualifying Child path closes, Qualifying Relative is the next door to try. It has its own four tests:

- Not a Qualifying Child of you or anyone else

- Either a relative on the IRS list, or someone who lived with you all year

- Gross income under $5,300 for 2026 (the limit adjusts for inflation each year)

- You provided more than half their total support

That income limit is the second cliff. It moves a little each year — $5,050 in 2024, $5,200 in 2025, and $5,300 in 2026. Cross it by a dollar and the Qualifying Relative door shuts too.

3. Case Breakdown — Applying the Rule to Ethan

Ethan turned 24 in November of last year. So on December 31, he was 24 years old — past the cliff.

| Qualifying Child Test | Ethan’s Situation | Pass? |

|---|---|---|

| Relationship | Linda’s biological son | ✓ |

| Age | 24 on December 31 | ✗ |

| Residency | Dorm during semester, home during breaks | ✓ |

| Support | Parents covered tuition + living costs | ✓ |

Three checkmarks. One X. The age test alone ends it — and there’s no overriding it.

So the next stop is Qualifying Relative. Ethan’s earnings for the year added up to $3,500 from the campus internship plus $4,800 from DoorDash. Total gross income: $8,300.

| Qualifying Relative Test | Ethan’s Situation | Pass? |

|---|---|---|

| Not a Qualifying Child | Failed age test above | ✓ |

| Relationship | Biological son | ✓ |

| Gross income | $8,300 (limit: $5,300) | ✗ |

| Support | Parents covered more than half | ✓ |

Two cliffs, two falls. Ethan fails on age and on income. Either failure alone would end it.

The result on the Parks’ return:

- Child Tax Credit ($2,200) — already off the table since Ethan turned 17 years ago

- Credit for Other Dependents ($500) — gone, because there’s no dependent to claim

- The dependent line on Form 1040 stays empty

Important: If Ethan’s 24th birthday had landed on January 2 of the following year instead of November of last year, the answer flips. Same kid, same tuition, same dorm — different outcome. The IRS doesn’t bend on this. Code §152, Publication 501, and every IRS examiner read the calendar the same way.

4. What If the Numbers Were Different?

A. Ethan was 23 on December 31

Full-time student plus age 23 keeps the Qualifying Child status alive. The $8,300 income wouldn’t matter — Qualifying Child has no gross income test. (The only related rule is that the child can’t have provided more than half their own support, which $8,300 doesn’t come close to.) Linda gets the $500 ODC.

Practical point

A child’s earnings rarely break Qualifying Child status. Age does.

B. Ethan is 24 but only earned $5,000

The age cliff still closes the Qualifying Child door. But the Qualifying Relative door swings open — $5,000 sits below the $5,300 limit, and the other tests pass. Linda still gets the $500 ODC.

C. Ethan dropped out of school last year

Without full-time student status, the Qualifying Child age cap drops to 19. He’s been past that for years. Only Qualifying Relative is on the table, and the $5,300 income test decides everything.

D. Ethan has a permanent disability

The age test disappears entirely. Qualifying Child stays available regardless of how old he is, as long as the other tests pass.

E. Linda is a single parent filing as Head of Household

This is where the cliff hits hardest. HOH status often hinges on having a qualifying person in the household — typically the child being claimed as a dependent. When that child crosses 24 and the dependent claim disappears, HOH eligibility can disappear with it, dropping the standard deduction from $24,150 to $16,100 and pushing the parent into less favorable tax brackets. The lost $500 ODC is small compared to that swing. A single parent in this situation should look hard at whether another qualifying person remains in the household before assuming HOH still applies.

5. The DoorDash Surprise — 1099-NEC Hits Hard

The dependent question is only half of what landed on the table. Ethan’s $4,800 from DoorDash isn’t a side job in the IRS’s view. It’s self-employment income, full stop. Different forms, different tax, different deadline mindset.

Three things follow automatically from a 1099-NEC over $400 in net earnings:

- Schedule C — Profit or Loss from Business, where the income and any deductible expenses (mileage, phone share, supplies) get reported

- Schedule SE — Self-Employment Tax, the Social Security and Medicare portion that wage earners normally split with their employer

- 15.3% SE tax — 12.4% Social Security plus 2.9% Medicare, applied to 92.35% of net earnings

Running Ethan’s numbers (with no expenses claimed, since he didn’t track mileage):

| Step | Calculation | Amount |

|---|---|---|

| DoorDash gross | 1099-NEC | $4,800 |

| SE base | $4,800 × 92.35% | $4,433 |

| SE tax owed | $4,433 × 15.3% | ≈ $678 |

That $678 is its own animal — separate from federal income tax, separate from state tax. Even if income tax comes out to zero, SE tax stands.

And income tax does come out to zero in Ethan’s case. He’s no longer a dependent (his parents can’t claim him), so he files as a regular single filer with the full 2026 standard deduction of $16,100. His $8,300 in earnings sits well below that. Federal income tax: $0. SE tax: $678. He still owes the IRS, just through a different door.

6. The Checkbox That Wrecks E-File

One small box on Form 1040 causes more rejected returns than almost anything else: “Someone can claim you as a dependent.” It sits near the standard deduction section, easy to overlook, and the wrong answer here is what triggers e-file rejections in family situations.

The rule is about eligibility, not what actually happened on the parent’s return:

- Parents can claim the child and do — child checks Yes

- Parents can claim the child but choose not to — child still checks Yes (the eligibility decides it)

- Parents can’t claim the child at all — child checks No

Ethan is in the third bucket. The Parks aren’t eligible to claim him. So Ethan checks No on his own return, files as an unclaimed single filer, and uses the full $16,100 standard deduction.

Important: If Linda had decided to “try” listing Ethan as a dependent anyway while Ethan also filed his own return, the IRS system catches the SSN on both returns and rejects whichever one comes second. One Social Security number, one slot per year — claimed by parents or used by the child as an independent filer, never both. Once that rejection happens, the family ends up paper-filing, which means weeks of waiting and a lot of room for error.

7. What to Check Right Now

- Confirm your child’s age as of December 31, not their age now

- Verify full-time student status — at least 5 months enrolled during the year

- Add up everything: W-2 wages, 1099-NEC, 1099-K, bank interest, brokerage gains. Compare to $5,300

- If there’s a 1099-NEC or 1099-K, expect Schedule C and Schedule SE on the child’s return

- Decide together (parents and child) who’s claiming what — before either return goes in

- Make sure the “Can be claimed as a dependent” checkbox on the child’s return matches reality

- If extension was filed, remember the child has their own deadline to think about — separately

EA Insight

Between April and August, this is one of the most common conversations I have with parents. Some version of “We’ve claimed our oldest every year — what changed?” The answer almost always comes down to one of two cliffs: the 24th birthday or the gross income limit. The Linda-and-Ethan situation is the version where both cliffs hit at once.

A different family I worked with last year had a daughter who turned 24 on December 28. The parents had filed a draft return claiming her, then came in to sign. We caught it before the e-file went out. Three days the other direction and she’d still be a Qualifying Child. There’s no “rounding” with this rule — it’s the calendar date or nothing.

The 1099-NEC piece is what most parents underestimate. A college student with $2,800 of tutoring or DoorDash income owes around $400 in SE tax — which they almost never know about. When the student doesn’t file, a CP2000 letter shows up in the mail the following year with the SE tax, plus penalties and interest. By that point, the parents have usually already filed and moved on, and the kid has graduated and changed addresses. Cleanup takes months.

When a child crosses 24 for the first time, sit down together and split the work in advance. Who claims whom, what each return shows on the dependent checkbox, who handles the 1099-NEC. Twenty minutes of coordination saves a paper-file rejection cycle and a CP2000 letter eighteen months later.

One more thing worth checking — your state return may handle dependents differently than the federal side, so the state filing status and any state-level education credits deserve a second look when a child crosses 24.

EA Summary

Two cliffs decide whether a college student stays a dependent: the 24th birthday by December 31, and the $5,300 gross income limit for 2026. Cross either one and CTC, ODC, and dependent status all disappear together — regardless of who pays tuition. A 1099-NEC over $400 triggers self-employment tax of its own, on the child’s return, completely separate from the parents’.

Frequently Asked Questions

My child turns 24 on December 31. Are they still my dependent that year?

No. The IRS treats a child as having reached age 24 on their 24th birthday, so a December 31 birthday means they’re 24 at year-end and Qualifying Child status is gone. Qualifying Relative is the only remaining path, and it depends on the gross income test.

Does graduate school count as full-time student status?

Yes — undergraduate or graduate, both count toward the full-time student test. The age cap stays at 24 either way. A grad student who turns 24 hits the same cliff as an undergrad.

My child has a W-2 and a 1099-NEC. How do they file?

Both go on a single Form 1040. W-2 wages report on Line 1a. The 1099-NEC flows through Schedule C, with any business expenses subtracted. If the Schedule C net profit is $400 or more, Schedule SE follows for the self-employment tax.

My child missed the April 15 deadline. What happens?

If they owe tax (likely, given SE tax), failure-to-file penalties run 5% per month up to 25%, plus failure-to-pay penalties of 0.5% per month, plus interest. If they’re owed a refund, no penalties — but the refund must be claimed within three years or it’s forfeited.

My child has an ITIN, not an SSN. Does that change anything?

CTC requires an SSN, so an ITIN-holder doesn’t qualify. The $500 Credit for Other Dependents, though, is available for ITIN dependents who otherwise meet the dependency tests. The Qualifying Relative gross income limit applies the same way regardless of identification number type.

If we don’t claim our college student, can they claim education credits themselves?

Yes. American Opportunity Credit or Lifetime Learning Credit moves to whoever claims the student. If the parents can’t claim the child as a dependent, the child can claim those credits on their own return — though they need actual tax liability for AOTC’s nonrefundable portion to matter, and the refundable 40% has its own rules. Worth running both scenarios before deciding.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.