Dependent Care FSA or the Tax Credit? Rachel’s 2026 Decision

You can use a Dependent Care FSA. You can claim the Dependent Care Credit. What you can’t do is use the same dollar twice — and starting in 2026, that decision matters more than it has in forty years.

Key Takeaways

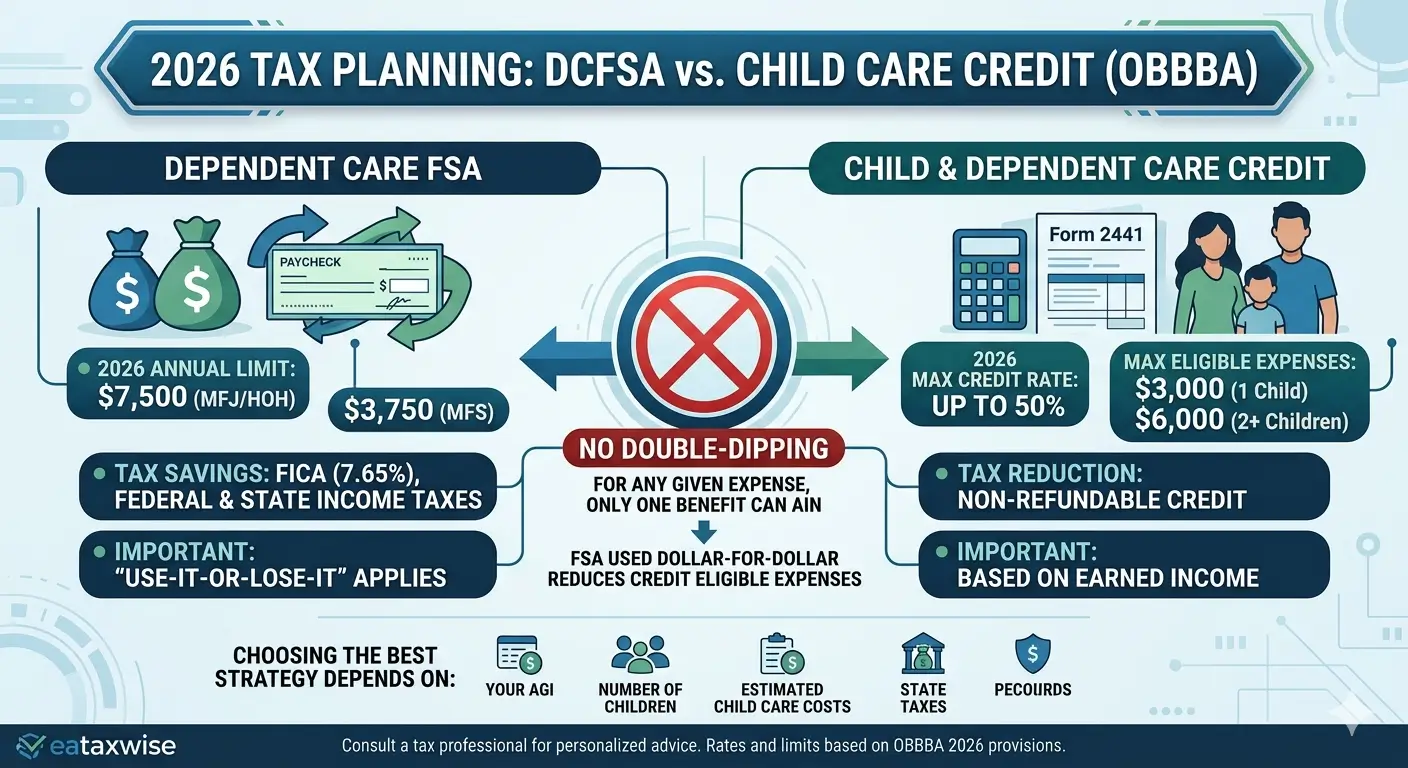

- A Dependent Care FSA and the Dependent Care Credit cannot apply to the same expense — the IRS calls this the no-double-dipping rule.

- Every dollar you contribute to an FSA reduces your Credit-eligible expenses by exactly that dollar.

- Starting in 2026, the FSA limit jumped from $5,000 to $7,500, and the maximum Credit rate climbed from 35% to 50% (OBBBA).

- Maxing the FSA at $7,500 wipes out your Credit eligibility regardless of how many children you have.

- Your employer must amend its cafeteria plan to actually offer the new $7,500 limit. It doesn’t happen automatically.

- The right choice depends on your AGI, number of children, FICA savings, and state credits — not on what worked last year.

Table of Contents

1. Meet Rachel

Rachel lives in Northern New Jersey. She and her husband Mike both work full time, and their three-year-old daughter Emma spends her days at a local daycare center. The monthly bill runs about $1,800. That’s $22,000 a year — more than they pay on most other line items.

For two years now, Rachel has been quietly maxing her Dependent Care FSA at $5,000. It was the path of least resistance: her HR portal made it easy to elect, the money came out pre-tax, and she stopped thinking about it. Then this year’s open enrollment landed in her inbox with a note she hadn’t seen before — “New for 2026: Dependent Care FSA limit increases to $7,500.”

A few days later she was at lunch with her friend Sarah, who’d been hearing different advice.

Now Rachel had two competing pieces of advice and no idea which one applied to her. Bump the FSA to $7,500? Drop it entirely and take the Credit? Try to do both somehow?

The good news: there’s a clear answer. The bad news: it isn’t the same answer for every family.

2. How Each Program Works

Two programs, two completely different mechanics. Walk through each before comparing them.

Dependent Care FSA (DCFSA)

A Dependent Care FSA is an employer-sponsored, pre-tax benefit account. You elect a contribution amount during open enrollment, your employer pulls that money out of your paycheck before withholding any taxes, and you reimburse yourself for qualified daycare expenses as they come up.

The “pre-tax” part does more work than people realize. FSA contributions skip federal income tax, Social Security and Medicare taxes (FICA — 7.65%), and most state income taxes. The Credit only reduces federal income tax. FICA doesn’t move.

| Item | Through 2025 | Starting 2026 (OBBBA) |

|---|---|---|

| Annual limit (Single / HoH / MFJ) | $5,000 | $7,500 |

| Annual limit (MFS) | $2,500 | $3,750 |

| Indexed for inflation? | No — limit is fixed until Congress changes it | |

| Use-it-or-lose-it | Yes — unspent funds forfeit at plan year end (some employers offer a 2.5-month grace period) | |

Important: The $7,500 limit isn’t indexed to inflation. Forty years ago Congress set the limit at $5,000 and walked away. Inflation ate more than half its real value before this update. The new $7,500 won’t compound either, so plan with that in mind.

Child and Dependent Care Credit (CDCTC)

The Dependent Care Credit is a non-refundable tax credit you claim on your return using Form 2441. Add up your qualifying daycare expenses, multiply by a percentage that depends on your AGI, and the result reduces your federal income tax dollar-for-dollar.

The qualifying-expense ceiling is $3,000 for one child and $6,000 for two or more. These caps haven’t changed under OBBBA. What did change is the percentage applied to those amounts.

| Item | Through 2025 | Starting 2026 (OBBBA) |

|---|---|---|

| Eligible expense cap (1 child) | $3,000 | |

| Eligible expense cap (2+ children) | $6,000 | |

| Maximum Credit rate | 35% | 50% |

| Minimum Credit rate | 20% | |

| Maximum Credit (1 child) | $1,050 | $1,500 |

| Maximum Credit (2+ children) | $2,100 | $3,000 |

| Refundable? | No — non-refundable, capped at your federal tax liability | |

Non-refundable matters: If your Credit calculates to $1,500 but you only owe $800 in federal tax, your benefit is $800. The remaining $700 doesn’t come back as a refund. The Child Tax Credit has a refundable piece (the Additional Child Tax Credit). The Dependent Care Credit doesn’t.

3. The No-Double-Dipping Rule

Here’s the rule that does most of the work in this post.

The rule

You cannot get a tax benefit twice on the same dollar of expense. Every dollar you spend through an FSA reduces your Credit-eligible expenses by exactly that dollar.

The math is simple. With one child, your Credit-eligible cap is $3,000. Put $3,000 in an FSA, and your remaining Credit-eligible amount is zero. Put $5,000 in an FSA — still zero. There’s no Credit to claim no matter how many extra dollars you contribute.

For two or more children, the cap is $6,000. Same logic. Once your FSA contribution hits $6,000, the Credit window closes.

| FSA contribution | Credit-eligible (1 child) | Credit-eligible (2+ children) |

|---|---|---|

| $0 | $3,000 | $6,000 |

| $2,000 | $1,000 | $4,000 |

| $3,000 | $0 (Credit closed) | $3,000 |

| $5,000 | $0 | $1,000 |

| $6,000 | $0 | $0 (Credit closed) |

| $7,500 (2026 max) | $0 | $0 |

The 2026 wrinkle: Under the new $7,500 limit, maxing your FSA shuts off the Credit entirely — no matter how many children you have. Before 2026 the math was friendlier. You could max a $5,000 FSA and still keep $1,000 of Credit eligibility with two kids. That cushion is gone.

4. Rachel’s Numbers — Three Options

Setting up Rachel’s facts:

| Item | Rachel’s situation |

|---|---|

| Filing status | Married Filing Jointly |

| Combined AGI | $120,000 |

| Qualifying children under 13 | 1 (Emma, age 3) |

| Annual daycare cost | $22,000 |

| Marginal federal rate | 22% |

| NJ state rate (effective) | ~5.525% |

One detail matters before the math starts. Under OBBBA, MFJ AGI of $120,000 lands in the 35% Credit rate band ($45,001 to $150,000). In 2025 that same AGI would have given Rachel only 20%. The Credit got genuinely better for her — the question is whether it got better than the FSA.

Option A — Max the FSA at $7,500

| Component | Amount |

|---|---|

| Federal income tax saved (22% × $7,500) | $1,650 |

| FICA saved (7.65% × $7,500) | $574 |

| NJ state tax saved (~5.525% × $7,500) | $414 |

| Dependent Care Credit | $0 (FSA exceeds the $3,000 cap) |

| Total benefit | ~$2,638 |

Option B — Skip the FSA, Take the Credit

| Component | Amount |

|---|---|

| FSA savings | $0 |

| Credit-eligible expense | $3,000 (one-child cap) |

| Credit rate (MFJ AGI $120K under OBBBA) | 35% |

| Federal Credit ($3,000 × 35%) | $1,050 |

| Total benefit | $1,050 + state Credit if applicable |

Option C — Split: $2,000 FSA + Credit on the Rest

| Component | Amount |

|---|---|

| FSA savings ($2,000 × ~35.2% combined rate) | ~$704 |

| Remaining Credit-eligible | $1,000 ($3,000 − $2,000) |

| Federal Credit ($1,000 × 35%) | $350 |

| Total benefit | ~$1,054 |

Side-by-Side Comparison

| Strategy | FSA savings | Credit | Total benefit |

|---|---|---|---|

| A: FSA $7,500 | ~$2,638 | $0 | ~$2,638 ✓ |

| B: Credit only | $0 | $1,050 | $1,050 |

| C: $2,000 FSA + Credit | ~$704 | $350 | ~$1,054 |

Rachel’s takeaway

At AGI $120,000 MFJ with one child, the FSA wins by a wide margin. The Credit got better in 2026, but FSA contributions still skip FICA and state income tax, and they apply to the full $7,500 instead of being capped at $3,000. That math doesn’t tip until your AGI is much lower or your number of kids is higher.

5. What OBBBA Changed in 2026

Two simultaneous changes, neither of which makes sense without the other.

Change 1 — FSA Limit $5,000 → $7,500

The first real adjustment in forty years. Married filing separately also moves up, from $2,500 to $3,750. Neither limit is indexed for inflation, so this is the new ceiling indefinitely.

Change 2 — Credit Maximum 35% → 50%, with a New Phase-Down

The maximum Credit rate climbs from 35% to 50%. The phase-down structure also shifted, with much friendlier middle-income treatment before bottoming out at 20%.

Single / Head of Household:

| AGI band | Through 2025 | Starting 2026 (OBBBA) |

|---|---|---|

| $0–$15,000 | 35% | 50% |

| $15,001–$45,000 | Phases 35% → 20% | Phases 50% → 35% |

| $45,001–$75,000 | 20% | 35% |

| $75,001–$105,000 | 20% | Phases 35% → 20% |

| $105,000+ | 20% | 20% |

Married Filing Jointly:

| AGI band | Through 2025 | Starting 2026 (OBBBA) |

|---|---|---|

| $0–$15,000 | 35% | 50% |

| $15,001–$45,000 | Phases 35% → 20% | Phases 50% → 35% |

| $45,001–$150,000 | 20% | 35% |

| $150,001–$210,000 | 20% | Phases 35% → 20% |

| $210,000+ | 20% | 20% |

The middle-income story: Under prior law, anyone above $43,000 AGI was stuck at 20%. Under OBBBA, MFJ filers up to $150,000 get a flat 35% Credit rate. That’s a meaningful change for working families — but as Rachel’s case shows, it doesn’t always beat the FSA.

6. Which Should You Choose?

Four variables drive the decision.

AGI

Lower AGI favors the Credit (50% or 35% rates). Higher AGI favors the FSA (higher marginal rates plus FICA savings).

Number of Children

One child caps Credit-eligible expenses at $3,000. Two or more children doubles that to $6,000. More kids means more room to combine FSA and Credit.

FICA Savings

This is the FSA’s secret weapon. The Credit reduces only federal income tax. The FSA also skips 7.65% in payroll taxes. For high-income families this often makes the difference.

Use-It-Or-Lose-It Risk

FSA dollars not spent during the plan year are forfeited (some employers offer a 2.5-month grace period). If your daycare costs are likely to drop mid-year — your child moves to school, you switch caregivers, you change jobs — that’s an FSA risk the Credit doesn’t have.

Rough rules for 2026 (MFJ)

AGI $150,000 and up: FSA max almost always wins.

AGI $75,000 to $150,000: Run all three options. The split strategy is worth checking, especially with two or more kids.

AGI under $75,000: Credit-heavy strategy usually wins.

These are starting points, not answers. State income tax, marginal rate, actual daycare spending, and employer plan terms can all flip the math.

State Credits add to the math: New York runs a State Child and Dependent Care Credit worth 20% to 110% of the federal Credit (income-dependent). New Jersey, California, and Massachusetts have their own versions. These state Credits piggyback on your federal Credit — choose Credit federally, and your state benefit grows with it. When comparing FSA against Credit, do the math with the full state-plus-federal benefit, not just the federal piece.

7. What to Check Right Now

- Do you have a child under 13 (or a dependent unable to self-care)?

- Do both spouses have earned income? (Exceptions: full-time student or disabled spouse)

- Does your employer actually offer a Dependent Care FSA?

- Has your employer amended its cafeteria plan to allow the new $7,500 limit? (This is not automatic — verify in the SPD or with HR)

- What’s your projected daycare cost vs. your planned FSA contribution? (use-it-or-lose-it)

- What’s your Credit rate at your AGI? (Use the Single or MFJ table above)

- Have you compared all three options — FSA max, Credit only, split strategy?

- On Form 2441, did you subtract Box 10 (FSA contributions) from your Credit-eligible expenses?

- Does your state offer a Dependent Care Credit on top of the federal one? (NY, NJ, CA, MA, and others do)

EA Insight

A few patterns I see every filing season — and one new trap that’s specific to 2026.

The first one is the easiest to fix and the easiest to miss. When you take FSA reimbursements during the year, your W-2 reports that amount in Box 10. On Form 2441, that Box 10 amount has to come off your Credit-eligible expenses. Tax software usually handles this automatically, but I still see returns where someone overrode the calculation or used a number from a paystub instead of the W-2. The IRS catches it through computer matching, and the CP2000 notice arrives months later.

The second pattern is the FSA-default problem. Through 2025, maxing the FSA was almost always the right answer for working parents. That became the conventional wisdom in HR departments and personal finance articles. With OBBBA’s Credit increase, it’s no longer automatic for middle-income families with two or more kids. I’m having more “let me actually run the numbers” conversations this year than I’ve had in a long time.

A note for couples considering Married Filing Separately. The FSA limit drops to $3,750 per spouse, but the bigger trap is on the Credit side — MFS filers generally cannot claim the Dependent Care Credit at all. There’s a narrow exception for spouses who’ve lived apart for the last six months of the year, but most couples filing MFS to chase a different tax outcome will lose the Credit entirely. Run MFJ versus MFS with both effects in the picture, not just the rate tables.

The 2026 trap is the one I’m most worried about for this open enrollment cycle. The $7,500 FSA limit isn’t automatic. Your employer has to amend its Section 125 cafeteria plan and update its open enrollment materials before you can elect more than $5,000. I had a client elect $7,500 in her HR portal because the email mentioned the new limit — but her employer hadn’t actually amended the plan, and her cap stayed at $5,000 in January. The extra $2,500 election rolled back, and she’d already enrolled her son in a more expensive program assuming the higher contribution. Verify the plan document, not just the talking points.

EA Summary

A Dependent Care FSA and the Dependent Care Credit both reduce your tax bill, and you can use both — just not on the same dollar. FSA contributions reduce your Credit-eligible expenses dollar-for-dollar, and a fully-funded $7,500 FSA wipes out the Credit no matter how many children you have. OBBBA pushed the maximum Credit rate to 50% in 2026, making the Credit more attractive for lower- and middle-income families. The FSA still wins for higher earners because of FICA savings. Run the numbers every open enrollment with three things in front of you: your AGI, your child count, and confirmation that your employer actually adopted the new $7,500 limit.

Frequently Asked Questions

If I’m using an FSA, can I claim any of the Dependent Care Credit?

Partially yes — as long as your FSA contribution is below the Credit-eligible cap ($3,000 for one child, $6,000 for two or more). An FSA of $2,000 with two kids leaves $4,000 of eligible expenses for the Credit. Once your FSA contribution hits or exceeds the cap, no Credit is available.

Can my spouse and I each contribute to a Dependent Care FSA at our separate employers?

You can each elect through your own employer, but the combined household limit is $7,500 for MFJ filers. You cannot double up to $15,000 across two FSAs. You also can’t submit the same expense for reimbursement under both FSAs.

Is the Dependent Care Credit always better in 2026?

Not always. Higher-income families often still come out ahead with the FSA because of the 7.65% FICA savings and higher marginal rates. As a rough cut, MFJ filers under $150,000 AGI should run the comparison. Above $150,000, the FSA usually wins.

Does my spouse need to work for either of these to apply?

Generally yes — both spouses need earned income. The exceptions are narrow: full-time student status or being physically or mentally incapable of self-care. In those cases the IRS imputes $250 per month (one child) or $500 (two or more) of earned income for the qualifying spouse.

Are summer day camps eligible expenses?

Day camps yes, overnight camps no. The expense has to be incurred so you can work or look for work, which excludes overnight programs.

What if my employer didn’t adopt the new $7,500 limit?

You’re stuck at $5,000. OBBBA permitted the higher limit but didn’t require it. Some employers — especially those with nondiscrimination testing concerns — chose not to amend their plan. Check your Summary Plan Description or ask HR directly. Don’t rely on open enrollment talking points.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.