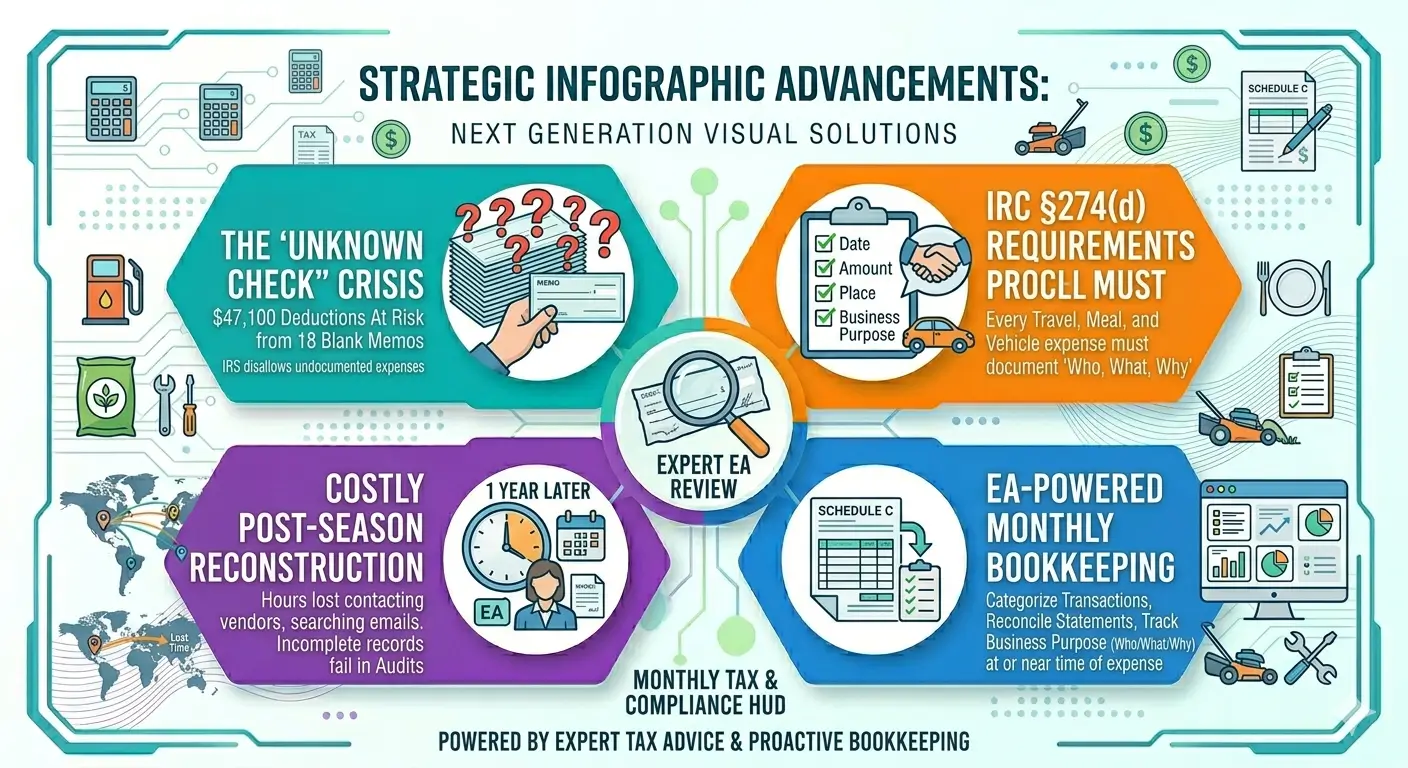

47 Checks, 18 Mysteries: Why “I’ll Remember Later” Fails the IRS

Every January, the same checkbook lands on my desk. The business owner wrote check #1247 last April, the memo line is blank, and now neither of us knows what it paid for. The IRS doesn’t accept “I think it was fertilizer” as a deduction.

Key Takeaways

- The IRS requires contemporaneous records, not after-the-fact memory — IRC §6001.

- Travel, meals, gifts, and vehicle expenses face a stricter standard under IRC §274(d): amount, time, place, business purpose, and business relationship.

- The Cohan rule — which allows reasonable estimation — does not apply to §274(d) items.

- When 18 out of 47 checks have blank memo lines, you’re not running a deduction strategy. You’re running a hope strategy.

- Reconstructing records eight months later is sometimes possible. It’s never as good as writing it down at the time.

Table of Contents

- 1. Meet Mary — January’s Checkbook

- 2. What the IRS Actually Requires

- 3. Case Breakdown — 47 Checks, 18 Mysteries

- 4. What If the Situation Changes?

- 5. The Real Standard for “Adequate Records”

- 6. What to Check Right Now

- 7. EA Insight

- 8. Frequently Asked Questions

- 9. Related Articles

- 10. Official Resources

1. Meet Mary — January’s Checkbook

Mary runs a small landscaping company in New Jersey with two employees. From April through October she works sixty-hour weeks. In winter she services her equipment and starts thinking about tax season — usually around the second week of January.

Every January, I get the same email from her.

Here’s the problem. Last April, Mary wrote a check for $3,200. The memo line was blank. When I asked her about it in January, she paused for a long time on the phone.

She never got back to me. Not with an answer, anyway.

2. What the IRS Actually Requires

The tax code is clear about this, and it’s been clear for a long time.

IRC §6001 requires every taxpayer to keep records sufficient to substantiate income and deductions. This isn’t a suggestion. It’s a statutory duty, and the burden of proof sits with the taxpayer — not the IRS.

For certain categories of expense, the bar is even higher. IRC §274(d) applies to travel, meals, gifts, and listed property (which includes business vehicles). For these items, you must record five things at or near the time of the expense:

| Element | What You Must Record |

|---|---|

| Amount | The exact dollar figure |

| Time | The date of the expense |

| Place | Where the expense occurred |

| Business Purpose | Why the expense was necessary for the business |

| Business Relationship | For meals and gifts, who was present and their connection |

Bottom line

Without contemporaneous records for §274(d) items, the deduction can be denied — even when you have the receipt in hand.

A common pushback I hear from business owners: “What about the Cohan rule? Doesn’t that let me estimate deductions when records are missing?” The Cohan rule does exist, and it sometimes helps with ordinary business expenses. It doesn’t help here. Congress carved out §274(d) specifically to override Cohan for these categories. Estimation doesn’t work for vehicles, meals, travel, or gifts.

3. Case Breakdown — 47 Checks, 18 Mysteries

When I finished reconciling Mary’s checkbook for the year, here’s what we had.

| Category | Count | Amount |

|---|---|---|

| Clearly business (memo or receipt matched) | 20 | $38,400 |

| Probably business (needed verification) | 5 | $11,200 |

| Unknown — Mary couldn’t recall | 18 | $47,100 |

| Personal (written from the wrong checkbook) | 4 | $2,300 |

| Total | 47 | $99,000 |

The $47,100 in unknown checks is where it gets painful. One was the $3,200 from April. Two others, written six weeks apart, were each $1,850 to what looked like the same supplier. Mary said, “I think those were probably fertilizer orders.”

Probably doesn’t survive an audit.

We did what we could. I asked Mary to:

- Search her email for the three days before and after each transaction date

- Look for invoices matching each dollar amount

- Contact suppliers directly and request duplicate copies

It took three weeks. The filing deadline kept getting closer, and we ended up filing Form 4868 for an extension just to give us breathing room.

Important: Reconstructing records after the fact is sometimes accepted by the IRS — but it’s never given the same weight as contemporaneous documentation. The outcome depends heavily on the auditor’s discretion and the quality of your corroborating evidence.

4. What If the Situation Changes?

Variation A: Receipt Yes, Memo No

A surviving receipt covers amount, time, and place. It doesn’t always cover business purpose. A $400 charge at Home Depot looks identical whether you bought irrigation parts for a client’s yard or a new patio set for your house. Without a note explaining which one it was, you’re rebuilding the story from memory months later.

Practical point

Two seconds of writing on a receipt — “irrigation parts, Henderson job” — eliminates an hour of detective work in January.

Variation B: Everything on Debit Card or Online

This is easier, but not solved. Bank statements show the vendor name automatically, so identifying where the money went is straightforward. The harder question — why — still requires a separate record. Especially for vehicle, meal, and travel expenses, the statement alone won’t satisfy §274(d).

Variation C: Cash-Heavy Operations

This is the hardest scenario. No receipt means no substantiation, full stop. For businesses that take cash payments to vendors or pay day laborers in cash, the only workable approach is daily — receipts into an envelope, a brief note on each one, photographed or scanned that night.

5. The Real Standard for “Adequate Records”

IRS Publication 463 (Travel, Gift, and Car Expenses) and Publication 583 (Starting a Business and Keeping Records) lay out what “adequate records” actually means. It’s more specific than most business owners realize.

You need one of the following, written at or near the time of the expense:

- An account book, diary, log, statement of expense, trip sheet, or similar record

- Documentary evidence that supports each element — receipts, cancelled checks, paid bills

The phrase the IRS keeps returning to is “at or near the time.” A note written eight months after the transaction doesn’t meet that standard. A reconstruction built from emails and bank records can sometimes get close, but it carries less weight and invites more scrutiny.

Important: Don’t confuse recordkeeping with tax preparation. A CPA or EA preparing your return is working from whatever records you provide. If those records are 47 checks with 18 blank memos, no preparer can fix that at the deadline.

6. What to Check Right Now

- Of your last month’s checks, how many memo lines are blank?

- Are any debit card charges mixed between personal and business on the same statement?

- Do you have a system for saving cash receipts daily, not weekly?

- Is your vehicle mileage being tracked at the time of each trip — app, notebook, or log?

- For business meals, do you record who was present and what was discussed?

- Is anyone reconciling your bank statements every month?

- Are your books being closed monthly, or are you waiting until January to figure it all out?

EA Insight

Mary isn’t unusual. Every January, similar checkbooks land on my desk — different industries, same problem. Landscapers, contractors, salon owners, small restaurants. The names change. The blank memo lines don’t.

What I find most frustrating is that these owners aren’t careless. They’re busy. From April through October, Mary is on jobsites at 6 a.m. Filling in a memo line on check #1247 in the middle of a workday simply doesn’t happen. By December, even she can’t tell you what she bought in April.

Here’s the math I share with every client who resists monthly bookkeeping. Suppose $10,000 of vehicle or meal expenses gets disallowed under §274(d). For a self-employed owner in the 24% federal bracket, the tax hit isn’t just $2,400. Self-employment tax adds another 15.3%, and state income tax piles on top. You’re looking at roughly $3,900 to $4,500 in additional federal tax alone — for one disallowed category, in one year. Monthly bookkeeping costs a fraction of that.

The deeper issue is that recordkeeping isn’t a paperwork problem. It’s a cash-flow problem disguised as a paperwork problem. Owners who can’t tell you what they spent last April also can’t tell you what their gross margin was, which jobs were profitable, or whether they’re paying themselves too much or too little. The checkbook is the symptom. The missing financial picture is the disease.

EA Summary

Blank memo lines from eight months ago can’t be filled in from memory. The IRS demands contemporaneous records under §6001, and §274(d) raises the bar even higher for vehicles, meals, travel, and gifts. Owners who close their books monthly save two things in April — taxes, and sleep.

Don’t let next January look like Mary’s.

If you’re running a small business with a Schedule C and your books are reviewed once a year — at deadline pressure — you already know the cost. Monthly bookkeeping by an Enrolled Agent means transactions are categorized while you still remember them, Schedule C lines are mapped correctly, and §274(d) documentation is in place before the IRS ever asks.

Send one month of bank statements and your latest P&L. I’ll review them and tell you, in writing, what’s working and what isn’t. Free, no obligation.

An Enrolled Agent who keeps your books — built the way the IRS reads them.

Frequently Asked Questions

If I have a receipt, isn’t a blank memo line fine?

A receipt typically proves amount, time, and place. For §274(d) items, you also need to document business purpose — and for meals or gifts, the business relationship of anyone present. A receipt alone is rarely complete substantiation.

Can’t I just use the Cohan rule to estimate?

For ordinary business expenses under §162, the Cohan rule may allow limited estimation. It does not apply to §274(d) categories — travel, meals, gifts, and listed property including vehicles. Congress specifically excluded these from estimation.

Are reconstructed records accepted?

Sometimes, but not equivalently. The IRS may accept reconstruction supported by emails, calendar entries, invoices, and similar corroborating evidence — though the outcome depends on the auditor and the strength of the supporting documentation. Reconstructed records always carry less weight than records created at the time.

What does monthly bookkeeping actually involve?

Each month, the bookkeeper categorizes every transaction from bank and credit card statements, separates business from personal, maps each item to the correct Schedule C line, and reconciles balances. Once a month is closed, those records aren’t revisited in January.

Why isn’t an annual tax preparer enough?

A tax preparer works from records you provide. If those records are unreconciled or incomplete, the preparer either spends weeks reconstructing them at peak season — at peak pricing — or files what’s available and hopes nothing gets questioned. Neither option is ideal. Bookkeeping and tax preparation are different functions.

How much can a single §274(d) disallowance actually cost?

For a self-employed owner, a disallowed $10,000 in vehicle or meal expenses can generate roughly $3,900–$4,500 in additional federal tax once you add income tax and self-employment tax (15.3%). State tax adds more. A single audit adjustment in one category can wipe out a year’s worth of bookkeeping fees several times over.

Official Resources

Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently. The story of “Mary” is a composite based on common patterns observed in practice and does not represent any specific client. Always consult a qualified tax professional for advice specific to your individual situation. eataxwise.com and its author are not responsible for any actions taken based on the information provided in this article.